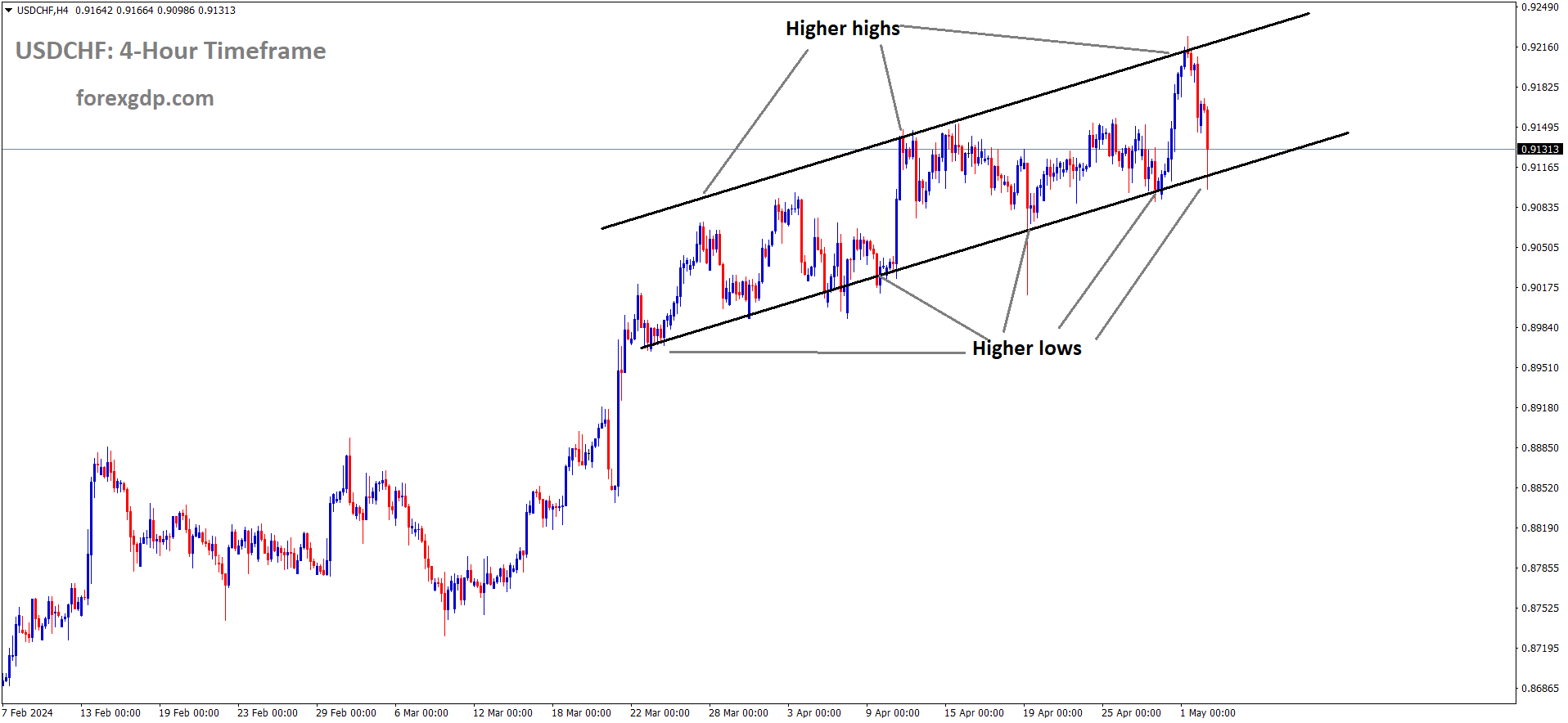

USDCHF is moving in an Ascending channel and the market has reached the higher low area of the channel

USDCHF – stays subdued under 0.9150 post-Swiss CPI update

The Swiss Franc is appreciated against counter pairs after the Swiss inflation came at 1.4% YoY versus 1.0% YoY printed in the March month. On Monthly basis, reading rose to 0.30% in the April month versus 0.10% is expected.

The USD/CHF pair experienced downward pressure on Thursday, influenced by robust Swiss inflation data. Currently hovering around 0.9110, the pair is down 0.48% for the day. The US Dollar (USD) weakened following the US Federal Reserve’s decision to maintain interest rates at their current levels, further contributing to the pair’s decline.

Switzerland’s inflation figures for April, released by the Federal Statistical Office of Switzerland, exceeded expectations. The Swiss Consumer Price Index (CPI) climbed to 1.4% year-on-year (YoY) in April, up from 1.0% in March. On a monthly basis, the Swiss CPI saw a 0.3% increase in April, surpassing the market consensus of 0.1%. Consequently, the Swiss Franc (CHF) attracted buyers, causing the USD/CHF pair to test the support level at 0.9100.

The US Federal Reserve’s decision on Wednesday to keep interest rates unchanged was influenced by persistently high inflation levels in recent months. Fed Chair Jerome Powell emphasized that the Fed would refrain from cutting interest rates until there is “greater confidence” that inflation is slowing sustainably toward the 2% target. Powell also indicated that interest rates are currently “restrictive” enough, and it is “unlikely” that the Fed will raise rates again in this economic cycle. These remarks weighed on the Greenback, creating headwinds for the USD/CHF pair.

Market participants await the release of US employment data on Friday, particularly the Nonfarm Payrolls (NFP) report for April. Analysts expect the report to show an addition of 243,000 jobs in the US economy, with the Unemployment Rate projected to remain unchanged at 3.8% for the same period.

XAUUSD – Powell’s Remarks Propel Gold Prices Skyward

The Gold prices are surged to $2300 after the FED Powell Dovish policy settings in the last day meeting. Powell said Balance sheet reductions cap level to $25 Billion from $60 billion in the previous cap level. Increasing Government Debts and floating more money in the market makes US Dollar down against Gold.

XAUUSD Gold price has broken the Ascending channel in downside

Gold prices surged above the $2,300 mark on Wednesday following the Federal Reserve’s decision to maintain interest rates and reduce the pace of its balance sheet reduction. Fed Chair Jerome Powell’s comments, particularly his lack of guidance on future rate cuts, further fueled the rally in gold prices.

Powell emphasized the need for confidence in inflation trending towards the 2% target before considering rate cuts, citing insufficient evidence from recent inflation data. He also mentioned the Fed’s intention to decide on monetary policy on a meeting-by-meeting basis and highlighted the adjustment in balance sheet policies to ensure a smooth transition for money markets.

The Fed’s decision to keep rates unchanged at 5.25%-5.50% reflected a balanced view on risks associated with achieving its dual mandate of employment and inflation. Despite noting progress on inflation, recent data suggested a slowdown in this progress. Additionally, the Fed announced a significant change in its balance sheet policies, reducing the monthly reduction of holdings in US Treasury securities from $60 billion to $25 billion starting in June.

Gold prices remained firm amid a steady US dollar and falling US Treasury bond yields. The decline in the US 10-year Treasury bond yield to 4.653% boosted gold prices, while the US Dollar Index (DXY) remained relatively unchanged. Mixed readings in US manufacturing business activity, as indicated by the S&P Global Manufacturing PMI and the ISM Manufacturing PMI, added to market uncertainty.

April’s ADP Employment Change report showed an increase in jobs, albeit below expectations, while the JOLTS Job Openings for March decreased to the lowest level reported. Mixed economic data continued with GDP missing expectations, raising concerns about inflationary trends.

Looking ahead, market focus will be on the US Bureau of Labor Statistics (BLS) Nonfarm Payrolls figures for April, expected to show a slight decrease from March. Traders anticipate the fed funds rate to finish 2024 slightly higher, reflecting ongoing uncertainty in monetary policy.

EURUSD – unsettled after Fed ahead of NFP Friday

The Manufacturing Purchasing manager index from Europe is scheduled today and is expected inline with preliminary Figures already come in. Manufacturing rises only 24% in the overall Euro zone economy. Ahead of US NFP Data scheduled tomorrow, Euro moving stronger against USD.

EURUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

On Wednesday, the EUR/USD currency pair traversed familiar terrain as the US Federal Reserve (Fed) opted to maintain interest rates, aligning with the expectations of many investors. Nevertheless, market participants were eager for additional indications of potential future rate cuts from the US central bank. Presently, rate markets are foreseeing the likelihood of a solitary rate reduction for the year, anticipated to occur in November.

During his speech, Fed Chair Jerome Powell conveyed that it is improbable that the next policy rate adjustment would be an increase, implying a dovish stance.

On Thursday, attention turns to the final Eurozone Manufacturing Purchasing Managers’ Index (PMI) figures from IHS Markit, with market projections anticipating figures to mirror the preliminary readings. Manufacturing currently constitutes less than a quarter of the overall European economic activity.

Market sentiment is poised to be significantly influenced by the release of the US Nonfarm Payrolls (NFP) report on Friday. Analysts anticipate the report to indicate an addition of 243,000 jobs in April, a decline from the previous month’s figure of 303,000. Investors will closely scrutinize any revisions to the data amid ongoing layoffs affecting various sectors of the US economy. Moreover, market participants are keenly observing the Average Hourly Earnings Month-over-Month (MoM) data for April, hoping for a stable reading at 0.3%, as wages remain a focal point amidst prevailing concerns about broad-based inflation.

USDJPY – JPY rebounds from intraday low, maintains negative stance around mid-155.00s against USD

The Japan Top currency Diplomat Masato Kanda said intervention history will give in the data format by the end of this month. The minutes of Japan Monetary policy meeting outcome is BoJ continue to loose monetary policy stance inorder to help demand driven economy in the Japan.

USDJPY is moving in an Ascending channel and the market has reached the higher low area of the channel

The Japanese Yen (JPY) faced significant selling pressure on Thursday, pulling back from its over two-week high achieved the day before. This downturn was prompted by speculation of a potential intervention by Japanese authorities, marking the second time this week such action was considered. Investors anticipate that the substantial interest rate differential between Japan and the United States (US) will persist for the foreseeable future. This sentiment, coupled with a generally optimistic atmosphere in the equity markets, dampens demand for the safe-haven JPY.

Meanwhile, Federal Reserve (Fed) Chair Jerome Powell tempered expectations of further interest rate hikes despite lingering concerns about persistent inflation. This cautious stance from the Fed keeps the US Dollar (USD) under pressure near a two-week low recorded last Friday, limiting the upside potential for the USD/JPY pair. Market participants are now closely monitoring US macroeconomic data, including Challenger Job Cuts, Weekly Initial Jobless Claims, and Trade Balance figures, for directional cues. However, all eyes remain on the highly anticipated US Nonfarm Payrolls (NFP) report scheduled for release on Friday.

In related market movements, the Japanese Yen saw some buying interest, possibly initiated by Japan’s Ministry of Finance, leading to a sharp decline in the USD/JPY pair to its lowest level in over two weeks during the late US trading session on Wednesday. However, the momentum faltered around the 153.00 level. Japan’s top currency diplomat, Masato Kanda, refrained from confirming any intervention by authorities in the foreign exchange market and indicated that intervention data would be disclosed at the end of the month.

Minutes from the Bank of Japan’s March policy meeting, released on Thursday, underscored the central bank’s commitment to supporting the economy financially to achieve a sustainable recovery driven by domestic demand. The Federal Reserve’s decision to maintain its forward guidance unchanged during Wednesday’s meeting, suggesting a potential easing of borrowing costs later this year, was interpreted as dovish. This contributed to a decline in the US Dollar overnight, although futures traders are pricing in less easing compared to the projections of the US central bank.

Furthermore, a positive sentiment prevailing in the US equity markets diverted flows away from the safe-haven JPY, providing an additional lift to the USD/JPY pair on Thursday ahead of the release of second-tier US economic data. However, market focus remains primarily on the US jobs report on Friday, which is expected to exert a significant influence on the short-term dynamics of the USD and offer meaningful direction to the currency pair.

USDCAD – Macklem: BoC Unconstrained by Fed’s Actions

The Bank of Canada Governor Macklem said we do not copy of FED Policy settings move, we have our economy style, inflation is easing in the Canada as we expected, Still Core CPI has to come down to our target. Monetary policy settings are really worked to help inflation to cool down. GDP is expected as 1.5% in 2024 and 2.0% in 2025 and 2026. Rate cuts are possible in the June month if data comes to our target.

USDCAD is moving in an Ascending channel and the market has reached the higher low area of the channel

Bank of Canada (BoC) Governor Tiff Macklem made headlines with remarks on Wednesday, emphasizing that the BoC maintains independence from the Federal Reserve (Fed) in its policy decisions, reflecting their distinct economic circumstances.

Key points from Macklem’s statement include:

- BoC is nearing the potential for rate cuts.

- GDP growth projections: 1.5% in 2024, followed by 2.0% in both 2025 and 2026.

- Recent data reinforces confidence in a sustained decline in inflation since January.

- BoC anticipates a gradual easing of core inflation.

- Signs of an uptick in growth are evident in the Canadian economy.

- The effectiveness of monetary policy is apparent.

- BoC retains autonomy in its decisions and is not obligated to mirror the Fed’s actions.

USD INDEX – Jerome Powell Speaks on Steady Interest Rates

The US FED Powell speech after the rates keep unchanged at 5.25%-5.50% is inflation is too higher from our target, Labour supply exceeded demand in the US economy. We see dual mandate on monetary policy changes. So when inflation come to our target 2% is hardly to forecast from our side. Rate cuts too little, too much, too soon, too late is harmful for US economy, So when inflation and unemployment rate come to our target 2% then only we do rate cuts in the monetary policy settings. Markets are dovish reacted to Powell speech last day. Already known expectations before the monetary policy settings, So Markets are moved higher before the speech and fallen after the speech.

USD Index is moving in the Box pattern and the market has reached the resistance area of the pattern

Federal Reserve Chairman Jerome Powell provided insights into the decision to maintain the policy rate, specifically the federal funds rate, within the unchanged range of 5.25%-5.5%. He elaborated on this stance and addressed inquiries during the post-meeting press conference.

Join us for live updates covering the Federal Reserve’s interest rate determination.

Here are key quotes from the Fed meeting press conference:

– Powell emphasized the progress towards the dual goals of the economy.

– He acknowledged the substantial easing of inflation over the past year but underscored its persistent elevation.

– The uncertainty surrounding the path to further inflation progress was highlighted.

– Powell discussed the impact of the current restrictive stance on inflation and the economy.

– The balance of risks in achieving dual goals was assessed, noting a lack of inflation progress.

– Attention to inflation risks and the strength of private domestic final purchases was reiterated.

– The tightness of the labor market was acknowledged, alongside observations on wage growth and labor demand.

– Powell emphasized the importance of incoming inflation data and the anchored nature of longer-term inflation expectations.

– The policy actions were reaffirmed to be guided by the dual mandate.

– Powell addressed the uncertainty of the economic outlook and the cautious approach towards rate cuts until greater confidence in inflation reaching 2% is attained.

– The potential risks associated with policy adjustments were discussed.

– The decision-making process was underscored to be data-dependent.

– Measures to slow the runoff of the balance sheet were explained to ensure market stability.

– The connection between policy restrictiveness, inflation, and the labor market was highlighted.

– Powell emphasized the importance of data in determining future policy actions, including potential rate cuts or hikes.

Additionally, the Fed’s decision to maintain the policy rate was confirmed in its statement following the April 30 – May 1 meeting. The statement addressed the lack of significant progress towards the 2% inflation target and outlined adjustments to the quantitative tightening strategy, including a reduction in the Treasury redemption cap.

Key points from the Fed’s policy statement include:

– Maintenance of the mortgage-backed securities redemption cap and reinvestment of excess MBS principal payments into Treasuries.

– Improved balance of risks to achieving employment and inflation goals.

– Continued elevation of inflation despite easing over the past year.

– Unanimous support for the policy decision among the Fed members.

GBPUSD – climbs above 1.2500 as Fed maintains stable rates

The BoE is expected to rate cuts in the June or August month meeting is possible, BoE Bailey expected inflation will returned to 2%target in April month, On contrary, BoE Chief economist Huw Pill said early rate cuts will harm the economy more than too late rate cuts.

GBPUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

The GBP/USD pair is currently gaining ground, hovering around 1.2535 during the early Asian trading hours on Thursday. This upward movement is primarily driven by a notable depreciation in the value of the US Dollar (USD) following the decision by the US Federal Reserve (Fed) to maintain its key interest rate unchanged.

As widely predicted, the Fed opted to keep its benchmark rate within the range of 5.25%–5.50% during its May meeting on Wednesday, marking its highest level in over twenty years. The central bank emphasized that it would refrain from cutting interest rates until it has greater confidence that inflation is consistently moving towards its targeted 2% level.

Fed Chair Jerome Powell, speaking at the press conference, indicated that a rate hike is unlikely to be the next policy move. These statements elicited a mildly dovish response from the markets, resulting in a decline in the value of the US Dollar and providing support to the GBP/USD pair.

Despite persistent inflationary pressures and a robust economic outlook, market expectations suggest only one rate cut by the Fed in November, according to the CME FedWatch. Additionally, the Fed announced a slower reduction in its bond portfolio, with plans to decrease its monthly holdings in US Treasury securities from $60 billion to $25 billion, starting in June.

Conversely, investors anticipate the Bank of England (BoE) to consider lowering borrowing costs in either the June or August meetings. BoE Governor Andrew Bailey expressed confidence in the return of headline inflation to 2% by April. However, BoE Chief Economist Huw Pill cautioned against the risks of implementing interest rate cuts too hastily, lending some support to the Pound Sterling (GBP).

AUDUSD – Aus Trade Surplus Shrinks to 5,024M MoM in April vs. Expected 7,370M

The Australian Trade surplus data came at narrowed to 5024M versus 7380M expected and 7270M printed in the March month. Exports grew at 0.10% in the march month from -2.2% printed in the previous month. Imports grew at 4.2% in the April month and 4.8% printed in the previous month.

AUDUSD is moving in the Descending channel and the market has reached the lower high area of the channel

The most recent data released by the Australian Bureau of Statistics indicates that Australia’s trade surplus for the month of April narrowed to 5,024 million compared to the anticipated figure of 7,370 million. This decrease follows the previous surplus of 7,280 million.

Delving deeper into the data, it shows that Australia’s exports of goods and services in March remained relatively unchanged, with a marginal increase of 0.1% compared to the previous month’s decline of 2.2%. On the other hand, imports of goods and services experienced a growth of 4.2% in April compared to the previous month’s figure of 4.8%.

NZDUSD – maintains advances post-Fed verdict

The FED Powell Dovish remarks on Policy settings yesterday makes NZ Dollar stronger against USD. The FED Borrowing cost numbers are higher to $25 Billion storage from $60 Billion storage of Bonds. So FED Buying power increases shows Economy moved in fast pace and keep the rates at higher pace.

NZDUSD is moving in the Descending channel and the market has reached the lower high area of the channel

Following the Federal Reserve’s (Fed) decision to maintain interest rates within the 5.25-5.50% range, the NZD/USD pair experienced a surge in momentum. The decision, widely anticipated, saw Chair Jerome Powell adopting a cautious stance, emphasizing the central bank’s data-driven approach and signaling a dovish tone to the markets. This resulted in a significant sell-off of the US Dollar (USD) by investors.

Chair Powell underscored the need for further evidence to instill confidence in initiating rate cuts, highlighting that progress towards the inflation target had stalled in recent months. He emphasized that the Fed would maintain its current policy stance until economic data aligned with the bank’s forecasts, suggesting a readiness to consider rate cuts if warranted by incoming data.

In terms of market expectations, there has been a notable shift away from anticipating rate cuts in June or July, with projections now leaning towards a potential easing cycle starting in September or November. This adjustment reflects the evolving economic landscape and the Fed’s cautious approach to monetary policy adjustments in response to prevailing economic conditions.

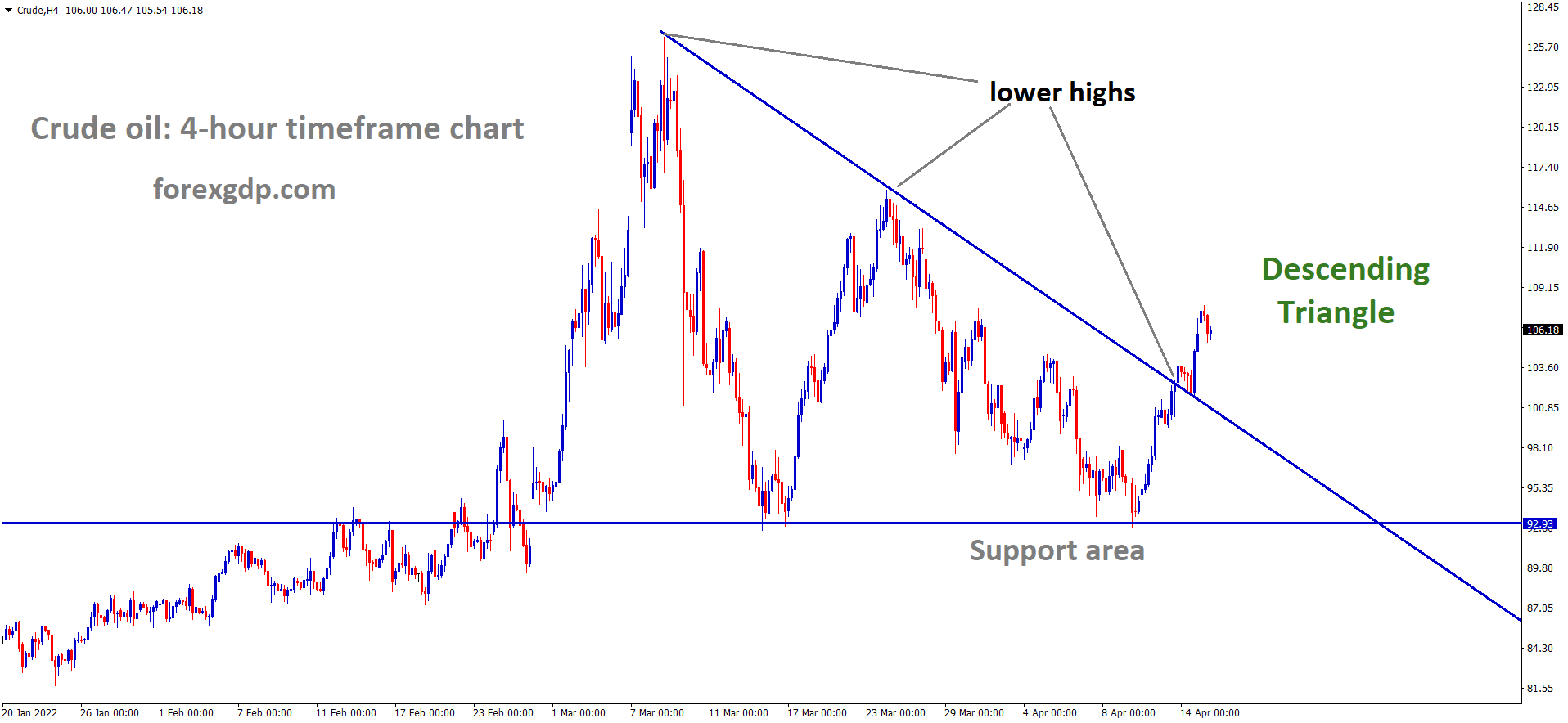

CRUDE OIL – Dips as WTI falls under $80 after Fed meeting

The Crude oil prices are tumbled after the FED meeting due to US have $30 million Barrels as inventories this year so far. Week end April 26, EIA reported 7.265 Million Barrels reserves from -2.36 Million Barrels expected and -6.368 Million barrels reported in the last week.

XTIUSD Crude oil price is moving in an Ascending channel and the market has reached the higher low area of the channel

West Texas Intermediate (WTI) crude oil, a benchmark for US oil prices, experienced a downturn, slipping below the $80.00 per barrel mark on Wednesday. This decline was attributed to the ongoing imbalance between supply and demand in the US crude oil market, compounded by the cautious stance of the US Federal Reserve (Fed) regarding potential rate cuts.

While global markets were attentive to the Fed’s latest decisions on interest rates, the Energy Information Administration (EIA) released its weekly report on US crude oil inventories. The data revealed a notable increase of 7.265 million barrels for the week ending April 26, which starkly contrasted with the anticipated decrease of 2.3 million barrels and surpassed the previous week’s decline of 6.368 million barrels.

This surplus in crude oil stocks, as indicated by the EIA, mirrors findings from earlier reports by the American Petroleum Institute (API) earlier in the week. The substantial buildup in crude oil inventories reported by the EIA represents the largest weekly increase since February 9. Throughout April, US crude oil stocks, monitored by the EIA, surged by 9.473 million barrels, while the overall US crude oil production, also monitored by the EIA, has exceeded demand by almost 30 million barrels since the start of the year.

In its recent announcement on interest rates, the Fed opted to maintain the status quo, aligning with market expectations. However, persistent challenges in curbing inflation have limited the Fed’s flexibility in implementing rate cuts. Market attention is now turning to the upcoming US Nonfarm Payrolls (NFP) labor report scheduled for Friday, as it promises insights into the current state of the US economy.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!