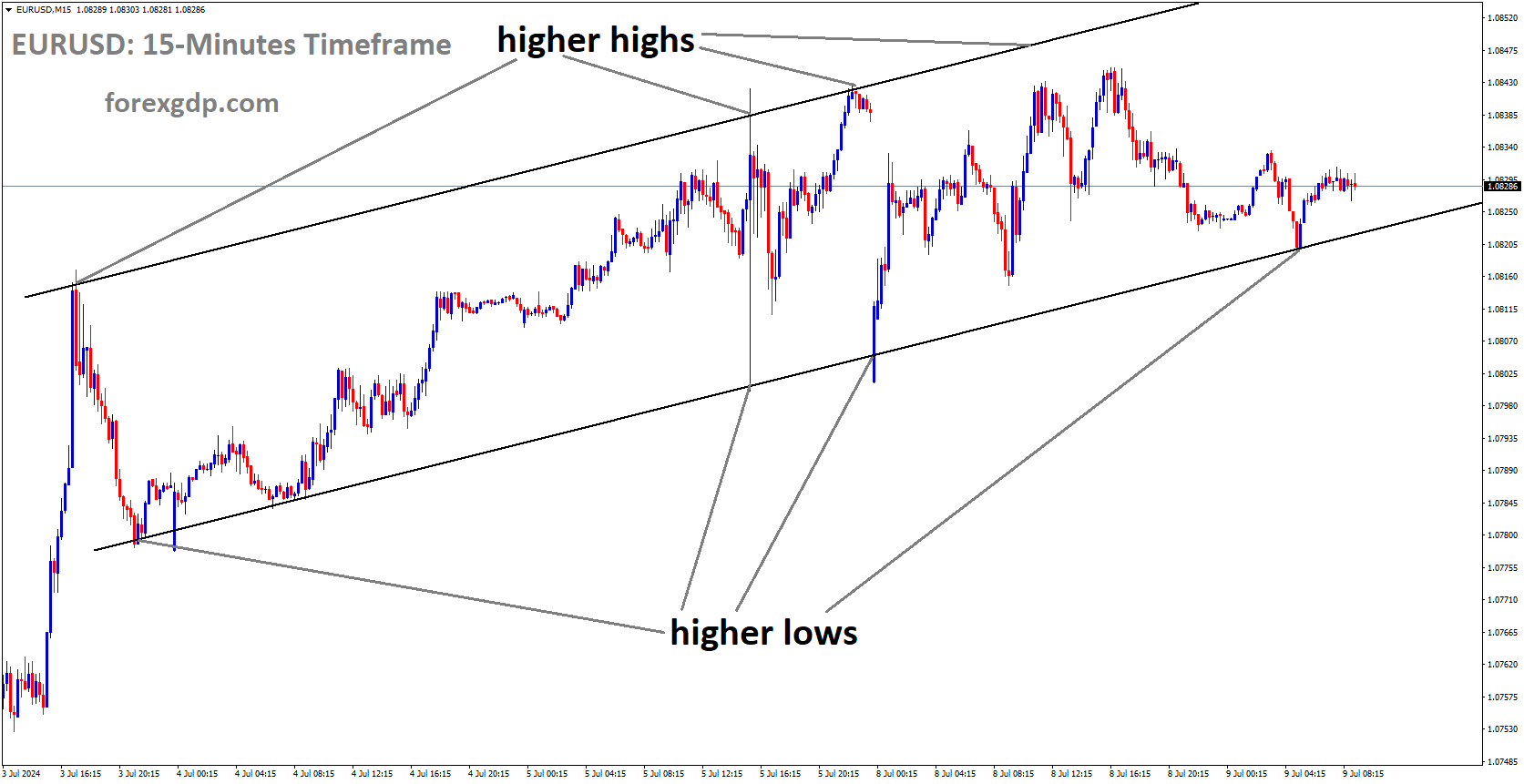

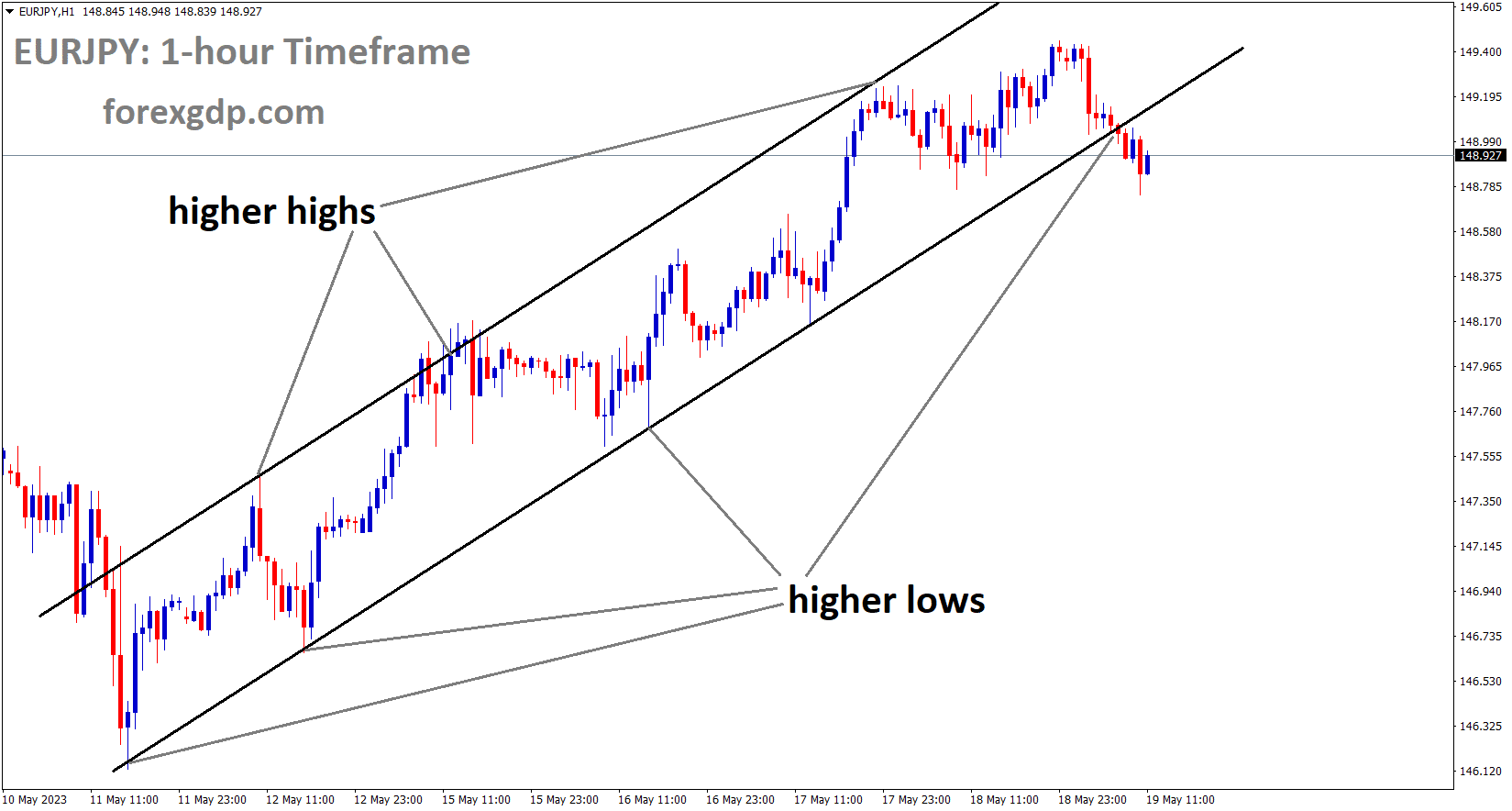

EURJPY Analysis

EURJPY is moving in an Ascending channel and the market has reached the higher low area of the channel.

According to ECB Vice President Luis De Guindos, since the cost of services has increased in the Euro area, the central bank will need to raise interest rates in the near future to reduce inflation. For further movements of the EURUSD, today’s events include the release of the ECB’s monthly bulletin and Powell’s speech as chair of the FED. US President Joe Biden’s meeting on Sunday will resolve the US Debt ceiling issue.

The Euro pair captures the market’s cautious attitude prior to this week’s major occasion, namely the speech by Fed Chairman Jerome Powell. Anxiety about US President Joe Biden’s promised announcement to prevent the default on Sunday as well as worries about the European Central Bank Bulletin are other things that are rattling the Euro bears

Vice President of the European Central Bank Luis de Guindos stated in a speech that “The ECB is most concerned about inflation in the services sector. The decision-maker also mentioned that there is still room for rate increases. The Monthly Economic Bulletin from the European Central Bank will likely determine how long the Euro bears maintain control. More importantly, US President Joe Biden said that a decision to avoid a default must be made by Sunday, making Fed Chairman Jerome Powell’s speech and debt ceiling negotiations crucial.

Japan’s CPI data came in at 3.5%, up from 3.2% the previous month and an estimated 2.5% drop. Core CPI increased to 4.1% from 3.8% in the previous reading. The Bank of Japan’s ultra-dovish policy has kept inflation at a higher level.

Amid optimism regarding US debt-ceiling issues, Asian markets are displaying tremendous strength. S&P500 futures have carried over their gains from Asia. Investors are confident that either a bipartisan agreement between White House and Republican leaders will prevent the US Treasury from defaulting, or that US President Joe Biden will exercise his 14th Amendment right, as evidenced by the back-to-back bullish settlements in US equities. Japan’s Nikkei index rose 0.73% at the time of publication, while SZSE Component gained 0.51%, Hang Seng fell 1.21%, and Nifty50 fell 0.31%. Asian markets have risen due to Japanese stocks as the Bank of Japan is expected to maintain its ultra-dovish stance despite an acceleration in inflationary figures. The street was expecting a decline to 2.5%, but the national headline Consumer Price Index increased to 3.5% from the previous release’s 3.2%. Contrary to expectations of 3.4% and the prior release of 3.8%, the core CPI, which excludes prices for food and energy, increased to 4.1%.

The Japanese economy’s resilience, as evidenced by strong corporate earnings growth and the Gross Domestic Product, has given the Nikkei 225 index new life. Before the People’s Bank of China (PBoC), which is scheduled to make an interest rate decision next week, Chinese stocks are anticipated to remain on edge. The PBoC is anticipated to continue its expansionary policy as the Chinese economy is expected to recover soon following a protracted period of lockdown caused by pandemic controls. Xi Jinping, the president of China, also declared on Friday that his nation would “expand trade facilitation measures and strengthen bilateral investment treaties with Central Asian countries.” He continued by saying that Central Asia has the prerequisites, conditions, and capacity to develop into a key node for connectivity across Eurasia.

GOLD Analysis

XAUUSD Gold price is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

Gold prices fell sharply this week from their highs due to stronger-than-expected US domestic data, a possible increase in the US debt ceiling limit, and optimism that the US will avoid a national default this week. Rate cuts in the United States are expected in the second half of 2023, raising the possibility of a recession.

Gold prices fell for the third consecutive session on Thursday, reaching their lowest level since the beginning of April. XAUUSD was down 1.4% to $1,960 in early afternoon trading in New York, dragged down by US dollar strength and rapidly rising bond yields following encouraging macro data and news that the US Congress is making progress in negotiations to raise the debt ceiling. Focusing on today’s catalysts, weekly unemployment claims and the Philadelphia Fed’s manufacturing production for May were both much lower than expected, reinforcing the view that business activity remains remarkably resilient despite numerous headwinds such as tightening lending standards, sticky inflation, and nonstop recession talk in financial media.

SILVER Analysis

XAGUSD Silver Price has broken the Descending channel in upside.

With the economy performing better than expected, the market is gradually pricing out the aggressive easing that was discounted for the second half of 2023 in the immediate aftermath of the banking sector turmoil that erupted in the United States in March. Despite reservations, it appears that traders are repositioning for a higher for longer interest rate regime, a key risk for precious metals.Optimism about a deal to raise the US borrowing cap and avoid a federal default appeared to hurt safe-haven assets, including gold. In context, sentiment improved after House Speaker Kevin McCarthy stated that the lower chamber of Congress could vote on a deal as soon as next week, indicating that talks are progressing. Although gold’s fundamentals remain somewhat positive, the situation could change. For example, if the US economy stabilises and avoids a recession, interest rates may remain high for longer than previously anticipated. This scenario would undercut non-yielding assets while strengthening the US dollar. As a result, traders should keep a close eye on incoming data in the coming weeks and months.

USDCHF Analysis

USDCHF has broken the Box pattern in upside.

The AT1 Tier Bondholders of Credit Suisse, with $17 billion in debt, lost 3 billion Swiss francs when the company announced a merger with UBS, according to a review of its credit default swaps by the European Body. As a solution for the losses brought on by the merger, the CDDC committee is currently providing a secure payout to holders.

After regulators eliminated the bank’s junior bondholders in a state-aided merger with UBS, a European body that reviews disputes in the credit default swaps market announced on Thursday that it will discuss whether a bankruptcy credit event occurred at Credit Suisse. The EMEA Credit Derivatives Determination Committee announced on its website that it will meet on Friday to discuss the new query brought up by an investor on Thursday. In the first global bank rescue since the 2008 financial crisis, holders of Credit Suisse’s $17 billion in Additional Tier 1 bonds were wiped out in March by a 3 billion Swiss franc merger. The transaction broke with a long-standing convention that gave bondholders preference over shareholders in the event of a debt recovery, leading to hundreds of lawsuits.

AUDCHF Analysis

AUDCHF is moving in the Box pattern and the market has reached the resistance area of the pattern.

A credit event can take many different forms, and if the CDDC confirms it, it could result in a payout on credit default swaps that protect against losses from exposure to corporate or sovereign debt. Wednesday saw the end of one of the avenues CDS holders were pursuing to obtain a payout when the CDDC determined in response to another query that a Governmental Intervention credit event had not taken place.

USD Index Analysis

USD index is moving in an Ascending channel and the market has fallen from the higher high area of the channel.

Over the last two weeks, the US Dollar Index has risen by 2.2%, its best 10-day performance since September 2022.US Congressmen on Capitol Hill are putting together a voting system for a bipartisan agreement to raise the US debt ceiling limit and avoid default.

US initial jobless claims were lower than expected, strengthening the US dollar against other currencies.

On Thursday, the US Dollar surged higher, extending its recent winning streak. The DXY Dollar Index has gained about 2.2% in the last two weeks. Since September 2022, this is the best 10-day performance. Let us take a closer look at the last 24 hours and what is in store for the rest of the week. Unsurprisingly, the 2-year Treasury yield has risen above 8.5% in the last two weeks, marking the best performance in this time period since September 2022. Rising short-term bond yields can be interpreted as an indication of growing confidence in the US economy. During Thursday’s Wall Street session, reports circulated that Congressmen on Capitol Hill are working on a short-term plan to vote on a bipartisan deal to raise the debt ceiling, potentially averting a default.

Meanwhile, timely labor-market data indicated signs of improvement. Last week, initial jobless claims unexpectedly fell to 242k. Economists predicted a 251k increase. Nonetheless, both figures are lower than the previous +264k print. As a result, financial markets continued to price in Federal Reserve rate cuts in the near term, despite a still-tight labour market and sticky underlying inflation. In the one year since last Wednesday, nearly two rate cuts have been removed from the outlook. This is most likely why the US Dollar has risen. With only 24 hours left, all eyes will be on a policy panel speech from Chair Jerome Powell and former Chair Ben Bernanke. If the former continues to cool near-term Fed rate cut bets, the USD’s impressive rally could gain traction.

GBPUSD Analysis

GBPUSD has broken the Ascending channel in downside.

Following inquiries from the UK Parliament Treasury committee regarding Bond sales by the Bank of England for the Quantitative Easing programme, the GBP fell. With more rate increases, the UK economy will suffer more Therefore, quantitative tightening measures will be implemented, and the Bank of England might stop raising interest rates in the coming months. After the Bank of England’s rate hikes were questioned, the value of the pound fell.

In order to take advantage of the market’s consolidation before the important events, GBPUSD licks its wounds close to 1.2410. Despite this, the US Dollar gained ground the day before, pushing the Pound Sterling to its lowest points in three weeks. The Bank of England (BoE) officials’ inability to defend the hawkish moves amid worries about the detrimental economic effects of tighter monetary policy also put pressure on the Cable pair. Top BoE officials were grilled on Thursday about the central bank’s sales of bonds purchased through its quantitative easing programme by the Treasury Select Committee of the UK parliament. BoE Governor Andrew Bailey, Deputy Governors Dave Ramsden, and Ben Broadbent were among them. If we carefully examine their claims, we find that they all support quantitative tightening while remaining silent about additional steps in that direction out of concern for the effects on the economy. In contrast, the US Dollar Index (DXY) increased to its highest levels since early March after the market reduced its bets on the US Federal Reserve (Fed) cutting interest rates in 2023 and increased its odds of the Fed raising rates by 0.25% in June as a result of stronger US data and hawkish Fed talks. The latest obstacles to the US debt ceiling agreement and conflicting worries about US-China relations, however, appear to nudge greenback buyers and enable the pair to consolidate the weekly losses during a sluggish session.

Fears of the US default and Sino-American tension rank among the DXY’s main obstacles. In addition to citing the influential US decision-makers, the House Freedom Caucus, Reuters also issued a warning. The news reported that “the small but mighty Republican faction warned this week that if the agreement does not contain ‘robust’ federal spending cuts, they could try to prevent any agreement to raise the $31.4 trillion debt ceiling from passing the House of Representatives.” In other news, the US Trade Representative (USTR) office reported on Thursday that the US and Taiwan had reached an agreement on the first component of their “21st Century” trade initiative, which deals with regulatory practises, small businesses, and customs and border procedures. This occurs before scheduled meetings between US Commerce Secretary Gina Raimondo, China’s Minister of Commerce Wang Wentao, and USTR Tai. These meetings have the potential to escalate Sino-American tension and spur the US Dollar’s gains. While these plays are going on, S&P 500 Futures are finding it difficult to follow Wall Street’s gains, and US Treasury bond yields are staying put despite reaching a multi-day high the day before. Now that Fed hawks are back at the table and US President Joe Biden has stated that a decision will be made to avoid a default by Sunday, the Federal Reserve’s (Fed) Jerome Powell’s speech and US debt ceiling negotiations will be crucial. The way China responds to the US-Taiwan trade agreement will be crucial.

GBPJPY Analysis

GBPJPY is moving in an Ascending channel and the market has reached the higher low area of the channel.

Kazuo Ueda, the governor of the Bank of Japan, has expressed his wish for a speedy resolution to the US debt ceiling issue. A US default, he continued, would have negative effects on the global economy, and the BoJ would work to keep markets stable and respond in a flexible manner while monitoring the state of the economy, market conditions, and financial developments.

GBPNZD Analysis

GBPNZD is moving in the Descending channel and the market has fallen from the lower high area of the channel.

According to large polls for the RBNZ conducted by Reuters, 80% of economists anticipate a 25 bps rate increase at the meeting on May 24 and a pause in the second half of 2022. Inflation may not reach the RBNZ’s target range of 1-2% until the second half of 2024, according to other economists.

According to a Reuters poll of 25 economists conducted between May 15 and 18, the Reserve Bank of New Zealand will raise interest rates by a final quarter point on Wednesday before ending its most aggressive tightening cycle since adopting the cash rate in 1999. The survey reveals that economists anticipate the RBNZ to adopt a pause until the end of the year. 21 out of 25 economists surveyed between May 15 and May 18 predicted that the RBNZ would increase its Official Cash Rate by 25 basis points to 5.50% at its May 24 meeting, matching the central bank’s anticipated peak rate. The other four respondents to the survey, which was done before the budget, anticipated no change. 14 out of 21 economists with a long-term outlook predicted that rates would remain at 5.50% in the upcoming quarter. The rates for the remaining six were 5.75% or higher for four, and 5.25% for three. By the end of 2023, rates were expected to be at 5.50% on average, but nearly 30% of respondents thought there would be at least one 25-bps reduction. According to a separate Reuters poll, the RBNZ’s target range of 1-3% for inflation was not anticipated to be reached until the second half of 2024.

AUDCAD Analysis

AUDCAD is moving in the Box pattern and the market has reached the horizontal support area of the pattern.

The RBA held the cash rate in June despite a 4.3K increase in employment and an increase in the unemployment rate to 3.8%. Rate increases by the RBA reduced consumer and business credit availability and decreased labour market demand.

The Australian asset has been able to prolong its recovery as the upward momentum for the US Dollar Index has run its course. Weak employment data that were released on Thursday are anticipated to encourage the Reserve Bank of Australia to resume maintaining a steady monetary policy stance. The number of workers in the Australian labour market fell by 4.3K in April. The unemployment rate for April has increased to 3.8%. Because higher interest rates have started to bite into firms’ production levels due to the gloomy economic outlook, RBA Governor Philip Lowe may decide to maintain interest rates at their current level of 3.85% at the June monetary policy meeting.

Today’s scheduled release of Canadian retail sales data was anticipated to show a 1.4% MoM decline and a 0.20 % decrease from the prior reading. After lower-than-expected retail sales data, the Canadian dollar increased. In the upcoming meeting, the Bank of Canada will attempt to hold interest rates steady. Following a string of positive domestic data points, the US dollar gains.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/