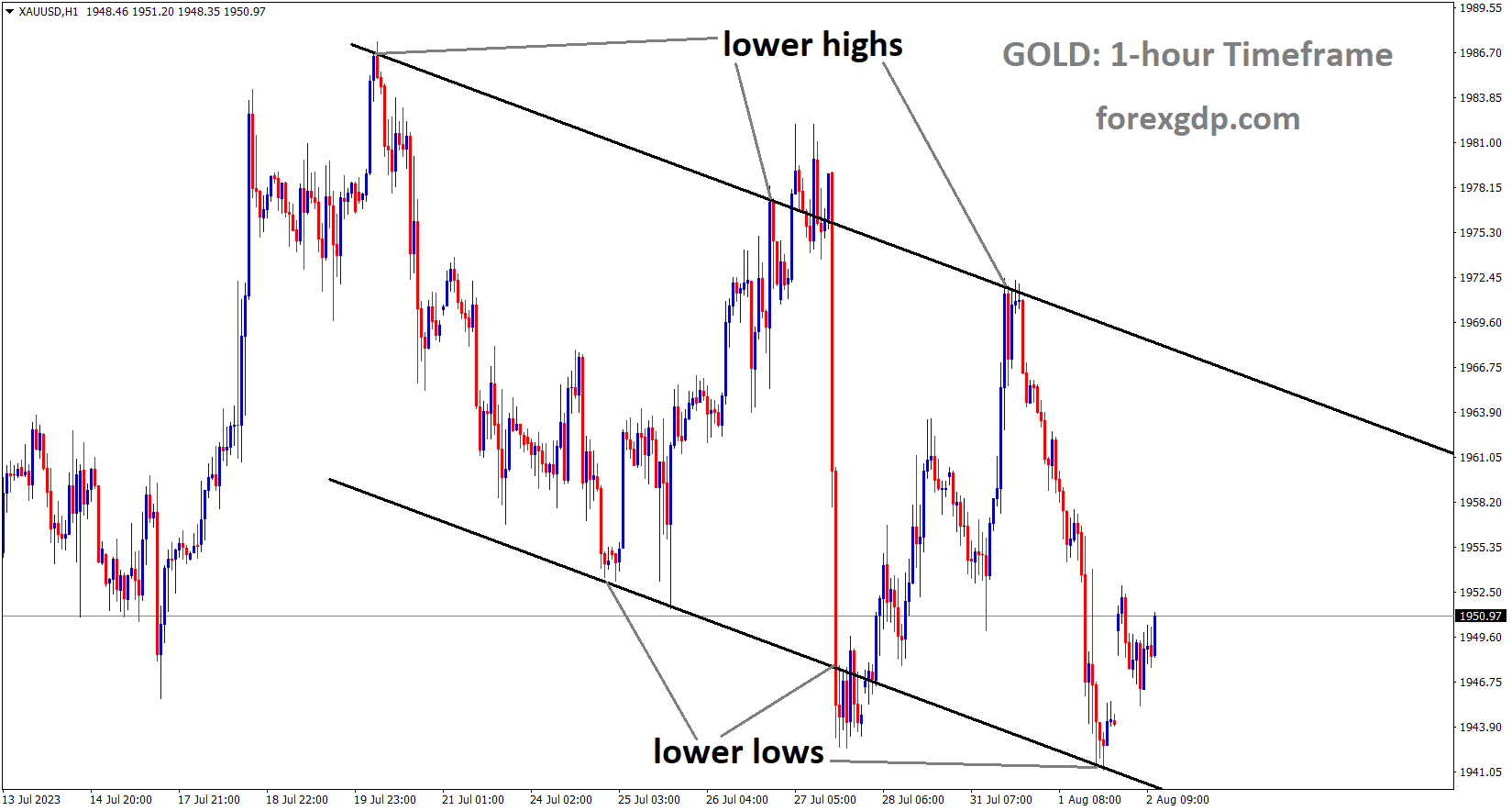

XAUUSD Analysis

XAUUSD Gold price is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

After yesterday’s mixed bag of US data readings, gold prices are marginally higher today. The US ISM Manufacturing PMI increased from 46.0 to 46.4, and the ISM Manufacturing Employment Index decreased from 48.1 to 44.4.

The NFP and Private ADP data this week will boost gold prices.

Gold Price XAUUSD is off to a strong start in the Wednesday Asian session, rebounding from recent lows and the 200-SMA key support as it supports Fitch Ratings’ decision to lower the US government’s interest rate. As a result, the yellow metal modestly increases to around $1,950, reversing the previous day’s steep losses. The early signal for Friday’s Nonfarm Payrolls NFP, the United States Automatic Data Processing ADP Change Employment, comes today, but the bears are still optimistic. Although the Federal Reserve Fed is expected to raise interest rates in September, the gold price recovers on the news of the rate cut but remains weak. The US ISM Manufacturing PMI for July increased to 46.4 on Tuesday from 46.0 the previous day, beating the forecast of 46.8. Additional information reveals that the ISM Manufacturing Employment Index fell to 44.4 from 48.0 anticipated and 48.1 prior, while the ISM Manufacturing Price Paid for the aforementioned month increased to 42.6 from 41.8, exceeding 42.8 market expectations. Additionally, the US JOLT Job Openings for June decreased to 9.582M from 9.62M expected and 9.616M in earlier readings revised, which is a slight decrease. It should be noted that the CME’s FedWatch Tool suggests that the hawkish Fed bets for September will gradually increase.

As a result, the US Dollar Index DXY increased to its highest level in three weeks, placing downward pressure on the Gold Price and causing it to lose two straight days of gains. It is important to note that the recent decline in the DXY, caused by reports that Fitch ratings may have downgraded the US government from AAA to AA+, provides support for the Gold Price. The 200-SMA support and the consolidation in the quote prior to today’s important United States data present additional challenges for the XAUUSD bears. News stories that are unfavourable to China and India, the two countries that consume the most gold, put downward pressure on the XAUUSD price. The World Gold Council WGC reported a 2.0% annual decline in the demand for gold on Tuesday as the physical demand for the XAUUSD is harmed by major central banks’ higher interest rates. More importantly, according to Reuters’ Somasundaram PR, regional chief executive officer of WGC India, India’s gold demand in 2023 could fall 10% from a year ago to their lowest in three years, as record high prices are dampening retail purchases. Nevertheless, the WGC representative anticipates a decline in New Delhi’s XAUUSD demand to 700 metric tonnes in 2023 from 774.1 metric tonnes in 2018.

On the other hand, gloomy data from China and worries about Sino-US tension pose obstacles to the dragon nation’s economic recovery, even though Beijing has unveiled a number of stimulus measures to support the transition. Despite this, China’s Caixin Manufacturing PMI for July fell to 49.2 from 50.5 in June, below the 50.3 market expectations, and reached its lowest level since January. This is in contrast to its upbeat NBS counterpart. Additionally, in response to US tech and trade war tactics, China’s Commerce Ministry announced restrictions on drone exports, citing national security measures. It is important to note that the recent gains in Chinese and Indian equities, however, limit the potential decline in the price of gold. The US Dollar’s recent strength and worries about declining demand from the biggest buyers have pleased gold sellers, but the metal’s further decline is dependent on US employment statistics. The US Automatic Data Processing ADP Change Employment, however, is regarded as the early signal for Friday’s important Nonfarm Payrolls NFP and can prod the US Dollar bulls, which in turn may trigger the Gold Price rebound, if matching or declining below the pessimistic forecasts of 189K for July versus 497K prior.

USD index Analysis

USD index is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

Goolsbee, the president of the Chicago FED, stated that the economy needs an easing of inflation. The US’s easing inflation means that additional tightening is required to hit the country’s 2% inflation target. In 2023, no rate reduction is anticipated.

Austan Goolsbee, president of the Chicago Federal Reserve Bank, stated on Tuesday that he needs more evidence that inflation is decreasing before considering raising interest rates. He will not commit in advance to a vote for September. While extending a warm welcome to attendees of Chicago’s Business Smart Week, he made these comments. According to Goolsbee, the need for additional tightening of monetary policy will depend on how prices develop. He mentioned that any rate reductions would be far in the future when speaking of them. Goolsbee stated that the JOLTS report appears consistent with a strong market transitioning towards a more balanced phase.

EURCAD Analysis

EURCAD is moving in the Descending channel and the market has reached the lower high area of the channel.

Due to more positive remarks about the US economy than the Canadian economy, the Canadian Dollar has continuously fallen against the USD. The Bank of Canada’s July rate increase helped the Canadian dollar, but the reduction in crude oil production has put some pressure on it.

Crude Oil Analysis

Crude Oil Price is moving in the Box pattern and the market has reached the resistance area of the pattern.

Despite a rise in crude oil prices, the Canadian dollar has been steadily falling against the US dollar since mid-July. Since the Bank of Canada’s (BoC) Summary of Deliberations last week revealed the central banks reluctance to tighten monetary policy further going forward after raising interest rates by 25bps in July, the increase in the price of crude oil has largely offset some of the dollar’s gains. Money market pricing (see table below) currently shows no additional increases priced in, but there is room for increases if economic data deems them necessary. The BoC should be at the peak of its rate hike cycle if Canadian inflation follows a similar trend as global inflationary pressures decline. The next point of contention will be rate reductions, but for the time being, markets will be focusing on Canadian fundamental data to first rule out any further rate increases.

EURCHF Analysis

EURCHF is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

Consumer spending in the Eurozone and a 0.10 percent decline in inflation during the month of July allow the ECB to keep raising interest rates in upcoming meetings. The ECB is becoming more confident about raising rates in the coming months as Q2 GDP increases.

GBPUSD Analysis

GBPUSD is moving in an Ascending channel and the market has reached the higher low area of the channel.

According to economists at Danske Bank, the Bank of England may raise interest rates by 25 basis points tomorrow as a result of surrounding higher inflation rates.

Danske Bank economists anticipate that the Bank of England BoE will increase the Bank Rate key policy rate by 25 basis points on Thursday, Governor Bailey is likely to reiterate the BoE’s data-dependent approach, effectively kicking the issue down the road. In general, we anticipate the BoE to emphasise how tight the labour market is still and leave room for more tightening. Overall, we continue to believe that relative rates are favourable for the EURGBP, which is one of several factors influencing our fundamental propensity to purchase EURGBP dips.

GBPCHF Analysis

GBPCHF is moving in an Ascending channel and the market has reached the higher high area of the channel.

The Swiss ZEW Survey expectations data increased from the previous reading of -30.8 to -32.6. Swiss retail sales decreased by 0.90% in May but increased by 1.8% in June.

According to the Swiss ZEW Survey Expectations data by the Centre for European Economic Research, the result was worse than expected, coming in at -32.6 instead of -30.8 previously. Swiss Retail Sales YoY for June were 1.8% as opposed to a 0.9% decline in May. The Manufacturing PMI, Consumer Price Index (CPI), and Swiss SECO Consumer Climate could provide information about the movement of the Swiss franc. Prior to the US ISM Service PMI and Nonfarm Payrolls, market participants will also be watching the release of the US ADP employment report later in the day. Trading opportunities will be found around the USD/CHF pair as traders take cues from the data.

AUDUSD Analysis

AUDUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel.

Lower than anticipated, the June month AIG Industry index came in at -14.7 from -11.9. The governor of the RBA stated yesterday that rate increases are appropriate and based on news.

In the early hours of Wednesday in the Asia-Pacific region, AUDUSD remains defensive around 0.6615-20 while licking its wounds at the lowest level in a month. In doing so, the Aussie pair struggles to support the US Dollar’s decline from a multi-day high while maintaining the anxieties caused by the Reserve Bank of Australia RBA. However, the recent decline in the US Dollar may be related to a surprise downgrade of the country’s credit rating, recent dismal Federal Reserve Fed talks, and mixed US data. It is important to note that Australia’s AiG Manufacturing PMI for the same month plunged to -25.6 from -19.8 previous readings and exerts downward pressure on the AUDUSD price lately. Australia’s AiG Industry Index for the same month fell to -14.7 from -11.9. Late on Tuesday, Fitch Ratings lowered the US government’s credit rating from AAA to AA+, citing concerns about the debt crisis as the primary drivers. The White House and US Treasury Secretary Janet Yellen hurried to denounce the decision and defend the US Dollar after the announcements, but they ultimately fell short. Prior to that, the AUDUSD pair’s recovery is supported by pessimistic remarks made by Raphael Bostic, president of the Atlanta Federal Reserve Bank. Despite this, Fed’s Bostic dismisses the need for a rate hike in September and expresses concern about the danger of overtightening.

However, it should be noted that the RBA’s second consecutive inaction contrasts with expectations of a Fed rate hike in September, which would give AUDUSD bears hope, particularly in light of unfavourable catalysts from China. After challenging the two hawkish surprises at the previous monetary policy meeting in July, the Reserve Bank of Australia RBA defied market expectations on Tuesday by maintaining the benchmark rates at 4.1% for a second straight meeting. However, Governor Phillip Lowe of the Australian central bank stated in his Monetary Policy Statement that Some further tightening of monetary policy may be required to ensure that inflation returns to target in a reasonable timeframe, but that will depend upon the data and the evolving assessment of risks. However, in response to US tech and trade war tactics, China announced restrictions on drone exports, citing national security measures. The China Caixin Manufacturing PMI for July dropped to 49.2 from 50.5 the month before, missing market expectations of 50.3 and marking the lowest level since January. It also failed to match its upbeat NBS counterpart.

In other news, the US ISM Manufacturing PMI for July rose to 46.4 from 46.0 the month before, beating expectations of 46.8. Additional information reveals that the ISM Manufacturing Employment Index fell to 44.4 from 48.0 anticipated and 48.1 prior, while the ISM Manufacturing Price Paid for the aforementioned month increased to 42.6 from 41.8, exceeding 42.8 market expectations. Additionally, the US JOLT Job Openings for June decreased to 9.582M from 9.62M expected and 9.616M in earlier readings revised, which is a slight decrease. In light of this, Wall Street ended the day with a mixed performance, and although US Treasury bond yields increased, the S&P500 Futures had already fallen by the time of press by 0.34%.Looking ahead, the AUDUSD movements may be influenced by the market’s response to the US rating cut and its cautious attitude in the lead-up to the US ADP Employment Change. However, if the ADP data match or fall short of the pessimistic forecasts—189K for July versus 497K earlier—the US Dollar bulls may be prompted.

AUDJPY Analysis

AUDJPY is moving in the Descending channel and the market has fallen from the lower high area of the channel.

In order for the BoJ to make any changes, according to Bank of Japan Deputy Governor Shinichi Uchida, the Government policy settings must be changed whenever the economy and price conditions change. The BoJ’s deflationary outlook keeps Japan’s inflation target of 2% from being met any time soon.

According to Deputy Governor of the Bank of Japan (BoJ) Shinichi Uchida, the BoJ will step in before the 10-year yield hits 1.0%, depending on the speed of moves. There is a chance that the BoJ’s response could alter if the price and economic conditions change in the future. Long-term rates will not rise much if economic and price conditions do not change much, so the current policy will probably be fairly stable. By fostering the shift in Japan’s deflationary mindset, we can achieve 2% inflation.

AUDNZD Analysis

AUDNZD is moving in the Descending triangle pattern and the market has rebounded from the horizontal support area of the pattern.

NZD Q2 employment rate was 3.6%, up from the previous reading of 3.5%. Employment changed at a 1.0% higher rate than it did previously (0.80%). After the data reading is printed, the Labour Cost index decreased to 1.1% from 1.2% NZD.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/