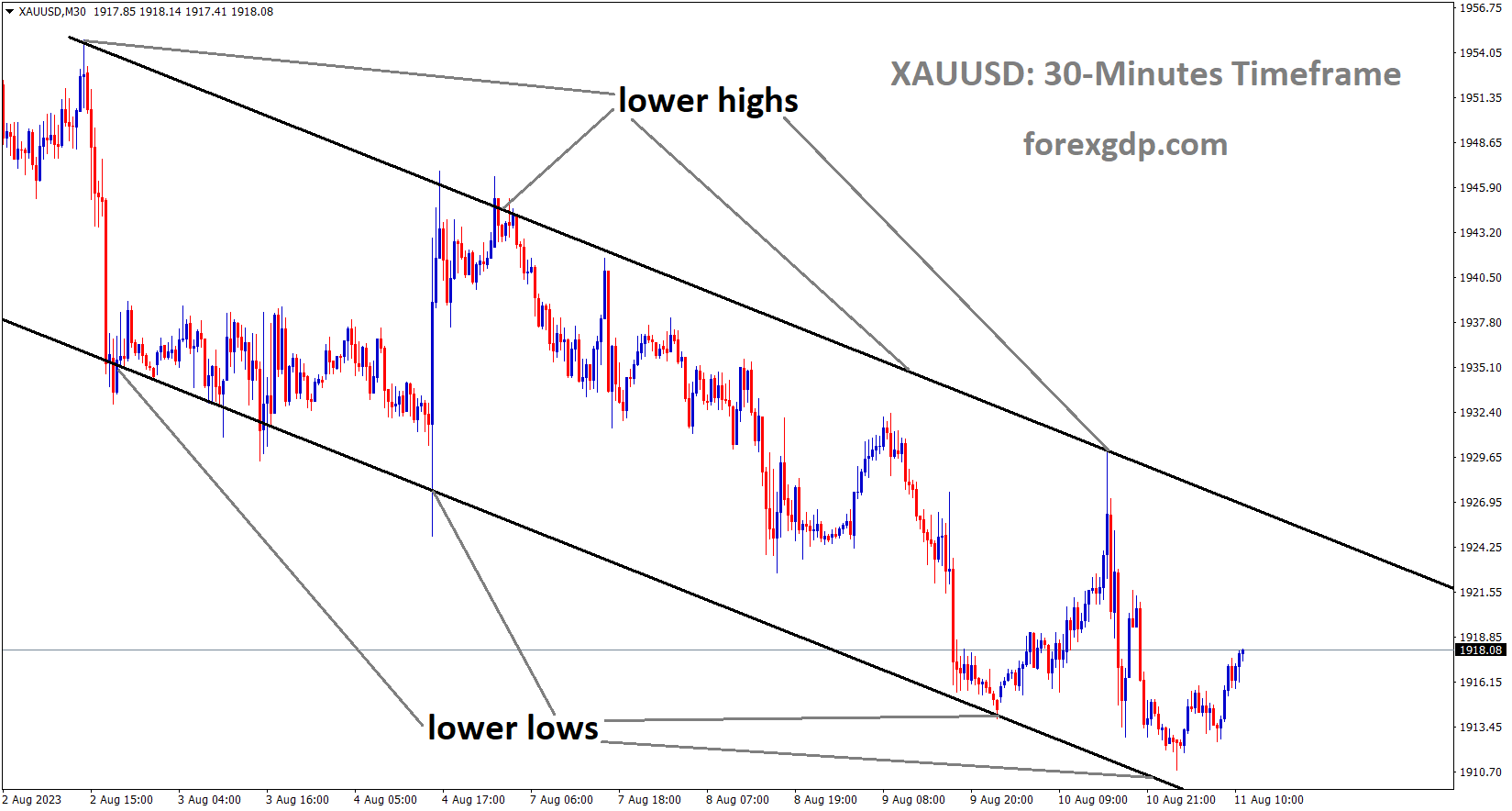

XAUUSD Analysis

XAUUSD Gold price is moving in the Descending channel and the market has rebounded from the lower low area of the channel

Gold prices saw a slight increase the previous day before declining when the US CPI for July came in at 3.2% instead of the 3.3% predicted, which was higher than the 3.0% reading. Because the FED has more room to raise the rate due to the three-plus year time horizon, gold will decline relative to the USD.

Following the release of US inflation data on Thursday, gold prices declined, undoing upward momentum that had built up over the previous twelve hours. July’s headline CPI came in at 3.2% y/y, slightly below the slightly softer 3.3% consensus. However, it was an improvement over the 3% result from last month. Concurrently, as anticipated, the core gauge declined marginally to 4.7% y/y from 4.8%.

XAGUSD Analysis

XAGUSD Silver price is moving in the Descending channel and the market has rebounded from the horizontal support area of the minor Box pattern

Treasury yields increased as well; the chart below illustrates this. Examining Federal Reserve monetary policy expectations in more detail shows that although the report had little effect on short-term interest rate bets, it did change the outlook slightly for the longer term. With a longer-term hawkish outlook, the most tightening was added to the horizon of three years or more. The president of the San Francisco Fed, Mary Daly, stated that the bank still has more work to do during the previous day. Because of this, it is not surprising that longer-term Treasury rates have rallied the most, as financial markets are beginning to view a central bank that may postpone the next round of rate cuts. Not surprisingly, gold, the anti-fiat instrument, did not perform well.

USDCHF Analysis

USDCHF is moving in the Box pattern and the market has reached the resistance area of the pattern

Following the significant collapse of Credit Suisse, the Swiss Government stated that there is no financial guarantee for deposits made by investors to banks. UBS vigorously terminated the loss protection contract.

UBS’s voluntary termination of its loss protection agreement, the Swiss government announced on Friday that Switzerland and its taxpayers are no longer at risk from guarantees made to maintain financial stability in the wake of Credit Suisse’s collapse. The Swiss Federal Council also stated that it is continuing its thorough review of the too-big-to-fail regulatory framework and that it still plans to present a bill to parliament to establish a public liquidity backstop under ordinary law.

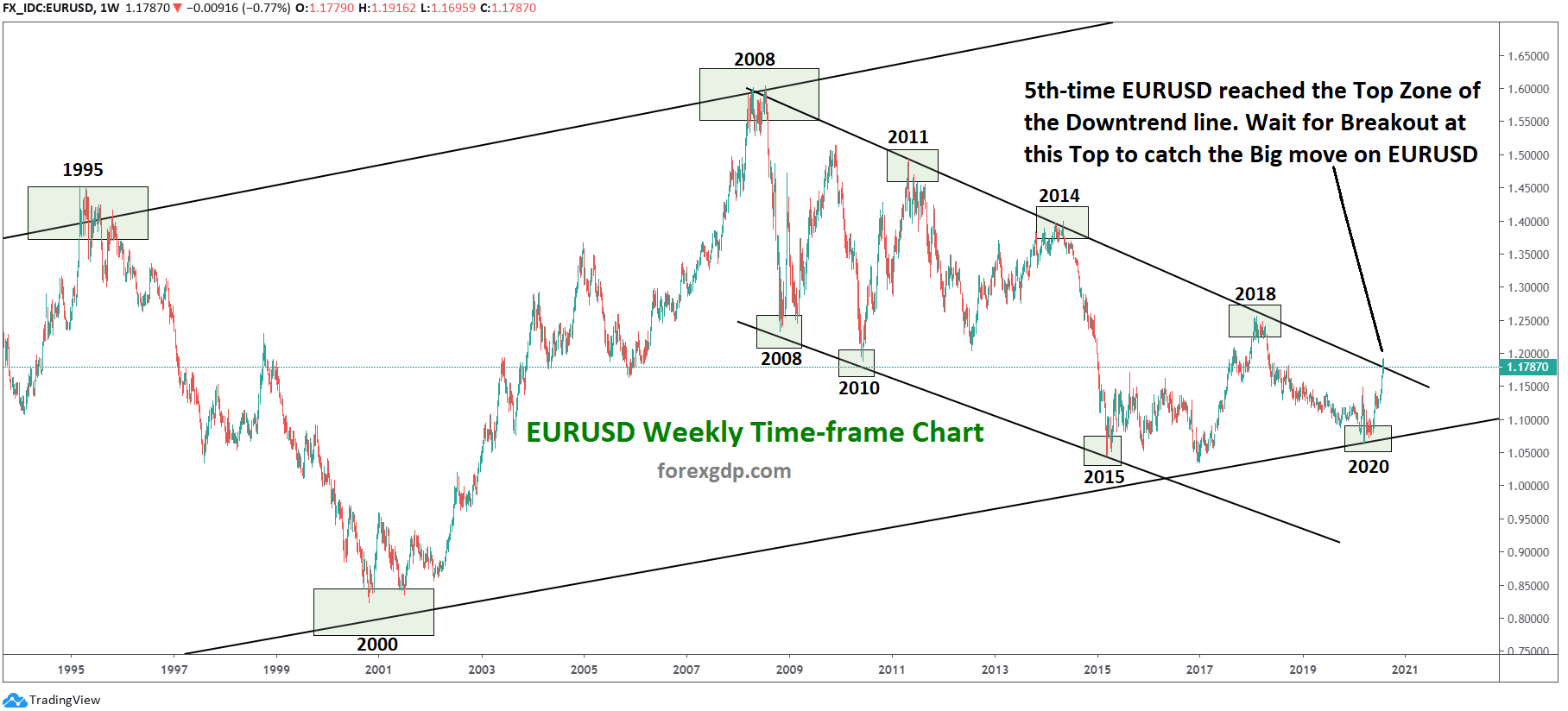

EURUSD Analysis

EURUSD is moving in the Box pattern and the market has fallen from the resistance area of the pattern

90% of polls indicated that interest rates would rise by year’s end, but the ECB was forced to halt rate increases in September due to a decline in polling data. After rate reductions in 2024’s second and third quarters, inflation did not return to 2% until 2025.It was stated by 53% of economists that the 4.00% level will be reached this year, and by 33% in September.

A slim majority of respondents to the most recent Reuters poll regarding the European Central Bank (ECB) anticipate a pause in the rate-hike trajectory in September, but some economists are also inclined to predict a rate increase by year’s end due to the high rate of inflation. It is noteworthy that while traders are split on whether ECB rates should rise to 4.0%, the interest rate futures indicate that inaction in September garners 60% acceptance. The target inflation rate was not reached until 2025, and over 90% of economists surveyed predict no rate reductions before 2024’s second quarter. Additionally, 53% of respondents said they expected the deposit rate to increase to 4.00% at some point this year; 33 economists predicted September, and four predicted October or December.

EURJPY Analysis

EURJPY has broken the Box pattern in upside

Since last September 2022, when the USDJPY hit the 151.00 level, there has been no expectation of BoJ intervention in the FX market due to the further depreciation of the Japanese yen. The YCC level has recently changed to 0.50–1.00%. JGB’s are therefore increasing to 0.65%, which is higher than it was in 2014.

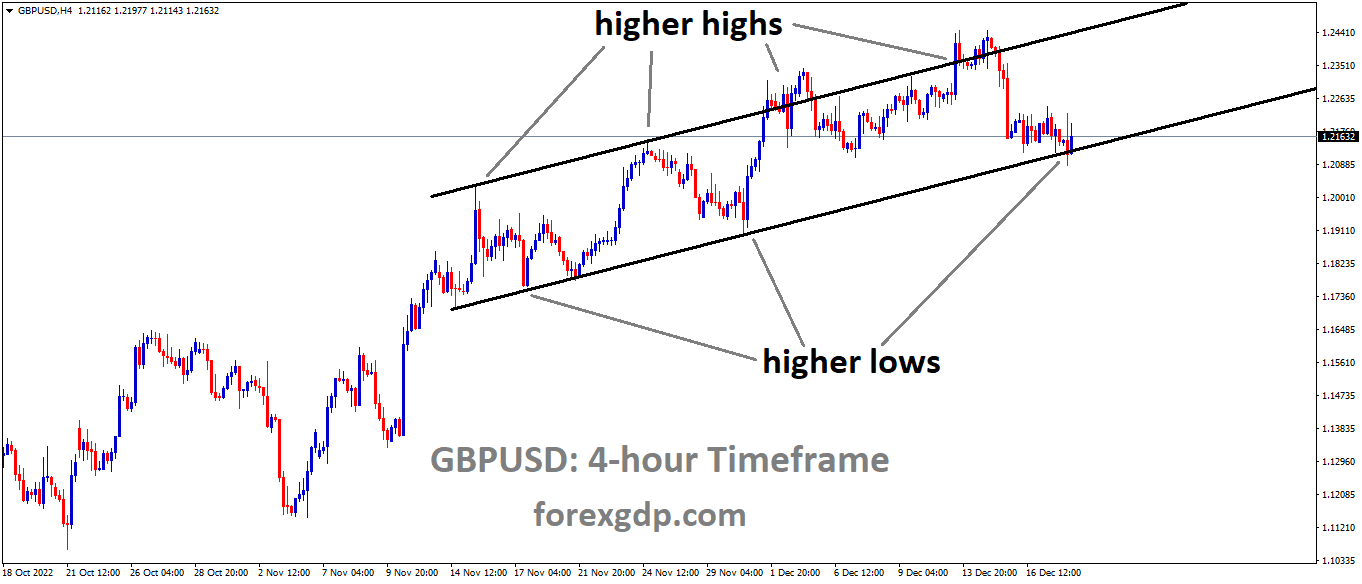

GBPUSD Analysis

GBPUSD is moving in the Descending channel and the market has rebounded from the minor box pattern of the channel

According to the UK GDP Q2 report, the country’s GDP expanded by 0.20% from the previous quarter to June.According to UK Chancellor Jeremy Hunt, sustained economic growth requires a solid foundation. In June, the UK GDP MoM was 0.50%, as opposed to the predicted 0.20%.

GBPCHF Analysis

GBPCHF is moving in the Box pattern and the market has reached the horizontal support area of the pattern

In contrast to the 0.1% growth recorded in the first quarter of 2023, the UK economy grew by 0.2% QoQ in the three months leading up to June. There was no growth predicted by the market for the reported period. In Q2, the UK GDP grew by 0.4% annually, exceeding both the 0.2% forecast and the 0.2% increase from the previous quarter. In June, the UK GDP grew by 0.5% MoM, compared to 0.2% predicted and -0.1% the month before. In the meantime, the June Index of Services came in at 0.1% 3M/3M, 0% predicted, and 0% prior. Jeremy Hunt, the finance minister of the United Kingdom, commented on the GDP report, saying, “We are laying strong foundations needed to grow economy. The measures we are implementing to combat inflation are beginning to show results. We will grow faster than Germany, France, and Italy if we follow our plan.

AUDUSD Analysis

AUDUSD is moving in the Descending channel and the market has reached the support area of the minor Box pattern

TDS Forecast predicts that the RBA will keep the cash rate at 4.10% in November. Increased labour costs will result in higher oil and real estate prices, which will cause an RBA rate hike at that point. This year, we have already missed our forecast rate by 4.85%. In 2024, rate reductions occur in Q2 and Q3.

Economists at TD Securities report that the RBA indicated it believes it is at or very close to a peak in the target cash rate in both its August Statement and its Statement on Monetary Policy. The foundation for an RBA hike in November is created if the labour market stays stable and there is proof that increased labour costs are being passed through. Time will tell, though. Although there is a chance this estimate could change, for the time being we believe the RBA cash rate will peak at its current level of 4.10%. Increased oil prices and rising property values that stimulate consumption (via the wealth channel) are the sources of the upside risks. The RBA is therefore anticipated to hold the cash rate in place for a longer period of time given our assessment that the cash rate peaks earlier and lower than our previous 4.85% forecast. We are now projecting rate reductions for Q2 2024 to Q3 2024.

AUDCAD Analysis

AUDCAD is moving in an Ascending channel and the market has reached the higher low area of the channel

Speaking before the House of Representatives, Governor Philip Lowe of the Reserve Bank of Australia expressed concern about rising unemployment rates in addition to the fear of inflation, which has led to rate hikes thus far. Therefore, rate hikes are currently at or very near their peak range.

Philip Lowe, the governor of the Reserve Bank of Australia (RBA), continues his remarks in front of the House of Representatives Standing Committee on Economics. The policymaker defended the most recent status quo by citing concerns about raising rates too quickly to bring inflation closer to the target after first citing fears of higher inflation and readiness to raise the rates. The decision-makers claimed that doing so would have increased unemployment. According to Reuters, RBA’s Lowe added that it would not be in the country’s best interests to require significantly higher rates in order to bring inflation to target by 2024. The policymaker continues by saying that it makes sense that the community believes the rate’s peak is at or near its current location.

While 3.5% was anticipated in July, Canadian building permits came in at 6.1% MoM, and the country’s trade deficit increased to C$3.73 billion in June. Imports decreased to 0.50% and exports to 2.2%.

Canadian building permits for July came in at 6.1% MoM, which was higher than the 3.5% decline that the market had predicted. Furthermore, in June, Canada’s trade deficit reached a record high of C$3.73 billion, the highest in almost three years. imports decreased by 0.5% and exports by 2.2%. Since Canada is the top oil exporter to the US, the decline in oil prices is detrimental to the Canadian dollar.

NZDUSD Analysis

NZDUSD is moving in the Descending channel and the market has reached the lower low area of the channel

A Reuter’s poll indicates that the RBNZ will not raise interest rates on August 16 and that none are anticipated until March 2024. The NZ Business PMI reading was 46.3, above the previous reading of 47.5 and the expected 49.4. The food price index fell below expectations, by -0.50% MoM, from 2.1%.

The NZDUSD pair is still unsure of itself despite pulling back from a 2.5-month low. It faded over the course of several days and was close to 0.6015 at early Friday press time in Auckland. In doing so, the Kiwi duo finds it difficult to defend their dovish views of the Federal Reserve Fed in the face of worries about the Reserve Bank of New Zealand’s RBNZ passivity. According to the most recent Reuters Poll on RBNZ, the central bank of New Zealand should keep the benchmark interest rate at its current level on August 16 and continue to do so until at least the end of March 2024. Conversely, negative data for July came from New Zealand NZ. The Business NZ PMI fell to 46.3 in July, below 47.5 in June and 49.4 in the forecast, while the Food Price Index fell to -0.5% MoM, below 2.1% in June and 2.1% in the market. Speaking of US data, the Consumer Price Index CPI for July’s headline inflation rate of 0.2% MoM was in line with market expectations. Nonetheless, the annual CPI increased from 3.0% in prior readings to 3.2% YoY for the mentioned month, a slower improvement than anticipated. This represents the first acceleration of the annual rate in 13 months. In addition, the Core CPI, or CPI ex Food & Energy, showed unchanged MoM data of 0.20% while still meeting market expectations. However, YoY data eased to 4.7% from June’s 4.8% mark and the anticipated figures. Interestingly, US Initial Jobless Claims increased to 248K for the week ended August 4, compared to 227K the previous week and 230K expected. Meanwhile, Continuing Jobless Claims decreased to 1.684M from 1.692M revised, compared to 1.71M market estimates.

A number of Federal Reserve Fed policymakers crossed wires to communicate the hard-won victory over inflation that the US central bank has achieved despite the generally negative US data. Nevertheless, their tones seemed less persuasive to doves, and they added to the risk-averse worries about China that were driving up the yields on US Treasury bonds. Nevertheless, to celebrate the weaker US CPI, Philadelphia Federal Reserve Bank President Patrick Harker raised a toast to the Fed’s victories in the war on inflation. He was joined by Presidents Susan Collins of the Boston Federal Reserve and Raphael Bostic of the Atlanta Federal Reserve Bank. President Daly of the San Francisco Fed, however, declined the congratulations for their win, stating that “there is still more work to be done.”Other concerns included the expectation of more geopolitical confrontations between the US and China, primarily as a result of the US ban on investment in Chinese technology companies and the likelihood that the UK and EU would follow suit. The US Dollar bears were also pushed back by talk of slower economic growth in developed nations and the difficulties associated with the recession in China, Germany, and the UK. The country is also aware of intelligence activity connected to China in and against the island nation and the Pacific region, according to the New Zealand Security Intelligence Service NZSIS annual report. This information raised geopolitical concerns about the Kiwi nation and depreciated the New Zealand Dollar NZD.

Because of this, even with the S&P 500 Futures being modestly bid and the US Dollar and US Treasury bond yields declining, the NZDUSD pair lacks recovery momentum.In order to influence immediate movements in the NZDUSD exchange rate, the US Producer Price Index PPI for July will be released ahead of the University of Michigan’s UoM Consumer Sentiment Index CSI for August first readings. The UoM 5-Year Consumer Inflation Expectations for that month will also be significant. Above all, the RBNZ and China news of the upcoming week will be critical in determining the quote’s future trajectory.

After the US CPI data came in at 3.2% instead of the expected 3.3%, the USD dropped. The core CPI decreased marginally from 4.8% to 4.7%.President of the San Francisco Fed Mary Daly stated that more interest rate hikes are planned for this year, which will raise the US dollar from its lows.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/