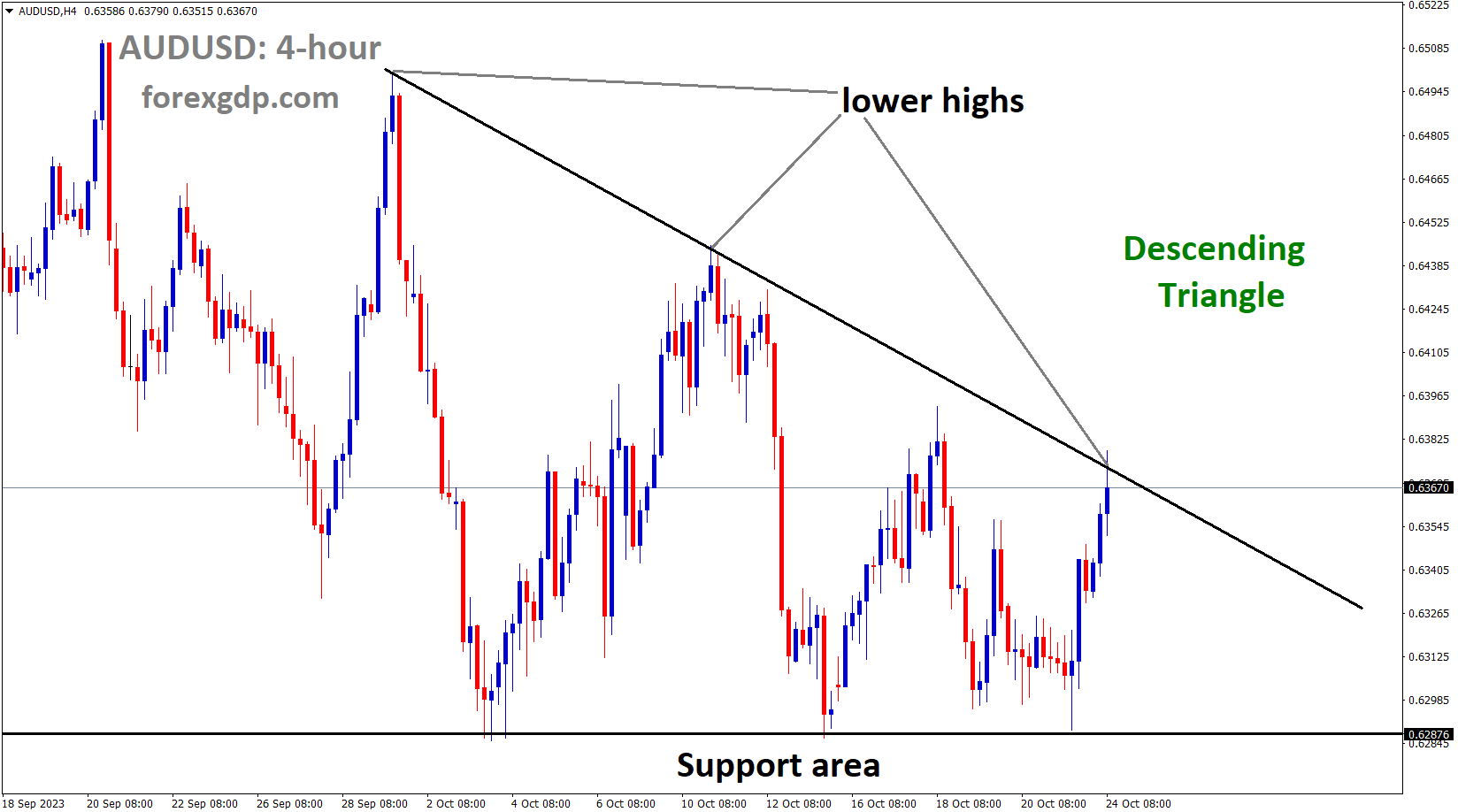

AUDUSD Analysis:

AUDUSD is moving in the Descending triangle pattern and the market has reached the lower high area of the pattern

In anticipation of tomorrow’s release of Q3 CPI data, the Australian Dollar has strengthened against its counterparts. Furthermore, there is positive news as the Chinese government is considering issuing 1 trillion Yuan worth of Sovereign debt to stimulate economic recovery from the impacts of COVID-19.

The Australian Dollar is trading positively for the second consecutive day, buoyed by a correction in the US Dollar, possibly due to weakening US Treasury yields. The US Purchasing Manager Index , US Gross Domestic Product , and US Personal Consumption Expenditure Index data scheduled for the upcoming week are expected to generate significant market activity involving the US Dollar . Meanwhile, in Australia, the preliminary S&P Global Manufacturing and Services PMI for October showed a decrease, indicating contraction in both the manufacturing and services sectors. Market expectations are leaning towards the Reserve Bank of Australia (RBA) adopting a more hawkish stance. RBA Governor Michele Bullock has suggested that if inflation persists above projected levels, the RBA is ready to implement appropriate policy measures.

In other news, the US Treasury Department has officially confirmed that the first meeting of the economic working group between the United States and China has taken place. This working group serves as a platform for discussions on bilateral economic policy matters. During the virtual meeting, both US and Chinese delegations engaged in productive and substantive discussions concerning domestic and global macroeconomic developments.

China is reportedly planning to approve an additional sovereign debt issuance of slightly over 1 trillion yuan, as part of the Chinese Communist Party’s efforts to boost infrastructure spending and stimulate economic growth. The National People’s Congress (NPC) is expected to approve this extra debt issuance during its meeting.

The US Dollar Index (DXY) is poised to extend its four-day losing streak, possibly influenced by declining US Treasury yields. After briefly reaching its highest level since 2007, the 10-year Treasury yield reversed course, resulting in some selling pressure on the US Dollar (USD). The markets currently do not perceive a likelihood of a November interest rate hike, but the odds for January 2024 remain above 30%.

In Australia, the S&P Global Composite PMI for October declined to 47.3 from the previous reading of 51.5. Manufacturing PMI eased to 48.0, down from the previous figure of 48.7, while the Services PMI dropped back into contraction territory, falling to 47.6 from the previous month’s reading of 51.8. Westpac’s Chief Economist, Luci Ellis, has stated that the Consumer Price Index (CPI) is expected to continue decreasing, returning to the RBA’s target band of 2-3% in 2025, aligning with the central bank’s expectations. Ellis has also highlighted several broader economic risks, including rising housing prices, global bond yield increases, and China’s slower-than-anticipated recovery from COVID-related lockdowns.

In the US, the weekly Initial Jobless Claims fell to 198K, below market expectations and reaching its lowest level since January. However, Existing Home Sales Change declined by 2.0% MoM in September, while Existing Home Sales improved to 3.96 million. The 10-year Treasury yield briefly surged to 5.02%, its first time at such levels since 2007, before reversing course and declining to 4.84%. Key data releases for the upcoming week include the US S&P Global PMI on Tuesday, Q3 Gross Domestic Product on Thursday, and the Core Personal Consumption Expenditures on Friday. Additionally, market participants will closely follow RBA Governor Bullock’s speech and the Consumer Price Index .

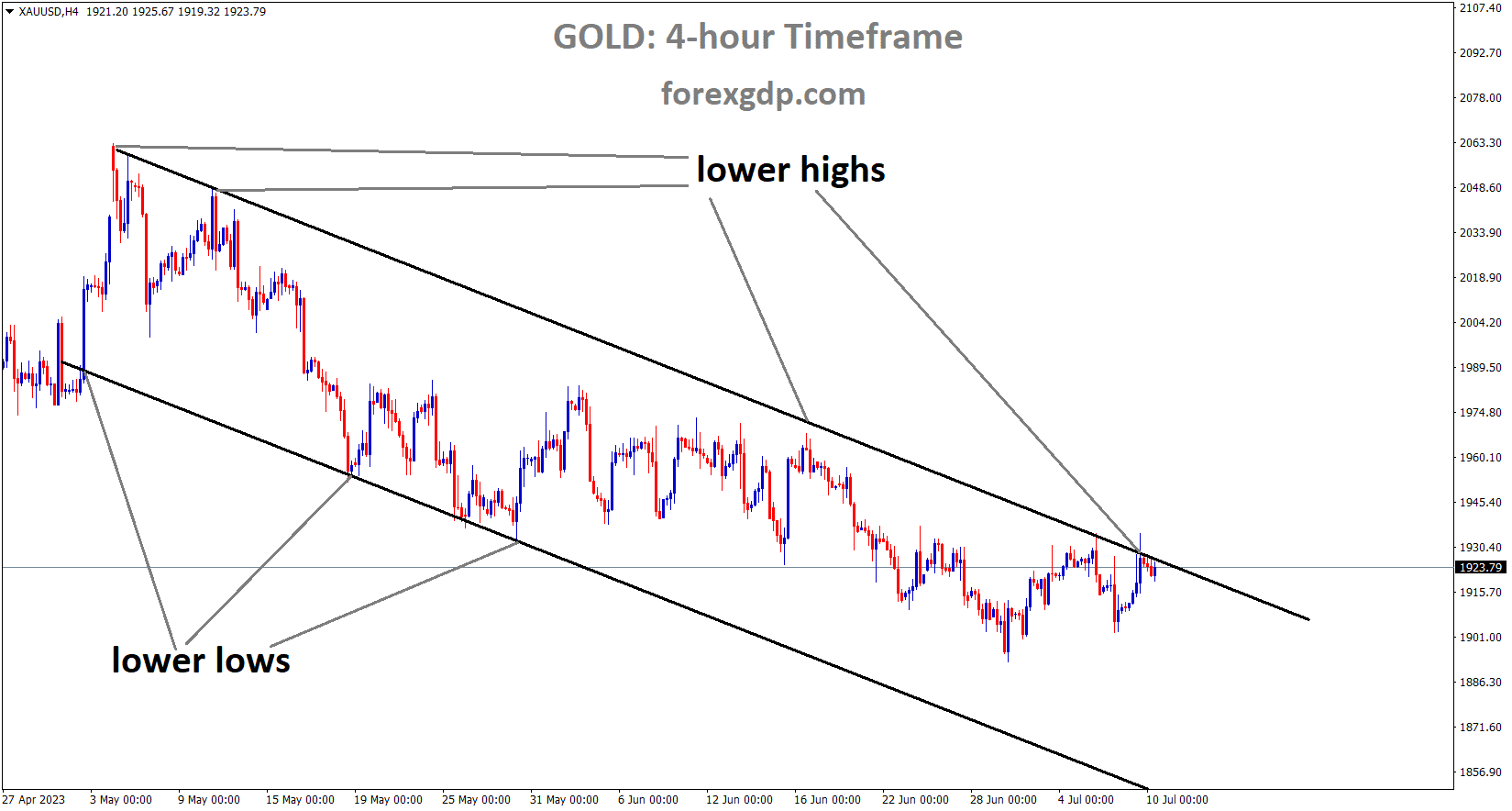

Gold Analysis:

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel.

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel.

The Israel-Hamas conflict temporarily halted the usual fluctuations in gold prices in the market. Whenever the threat of war arises, it tends to support gold prices at elevated levels.

The price of the precious metal is on the rise, thanks to a correction in the US Dollar (USD), which can be attributed to the less optimistic US Treasury yields. The US Dollar Index (DXY) continues its four-day losing streak, with a hovering value around 105.50. After hitting a peak of 5.02%, the 10-year Treasury yield has quickly reversed course, dropping to 4.84% in the latest update. Should US bond yields continue to decline, it would likely keep the US Dollar weaker, offering support for Gold prices to potentially reach the $2,000 mark. Geopolitical tensions in Israel usually boost the demand for gold as a safe-haven asset. Nevertheless, the current risk-on sentiment might pose a challenge to Gold prices, following diplomatic efforts aimed at reducing tensions in the Gaza Strip. These efforts have reduced market risk aversion, although there is a growing call within Israel to reassess the potential scope of a ground invasion of Gaza, which had been expected in the near term.

")

The disclosure of China’s plan to authorize slightly over 1 trillion yuan in additional sovereign debt issuance has potentially improved market sentiment. Furthermore, positive discussions between the US and China during their initial meeting of the economic working group have contributed to an enhanced market sentiment. This, in turn, has put pressure on the safe-haven US Dollar, resulting in an increase in the price of Gold. Market observers are gearing up for a week filled with economic data. Tuesday will see a close examination of the US S&P Global PMI, followed by a keen focus on Thursday for Q3 Gross Domestic Product figures. The week will conclude with a spotlight on Core Personal Consumption Expenditures on Friday.

Silver Analysis:

XAGUSD Silver price is moving in an Ascending channel and the market has reached the higher low area of the channel

The US Dollar is currently in a consolidation phase leading up to the release of Q3 GDP data and Fed Chair Powell’s upcoming speech this week. The conflict between Israel and Hamas escalated briefly after a period of ongoing tensions. As a result, market activity has cooled off in anticipation of any potential talks between the two sides.

The US Treasury Department officially announced on Tuesday that the United States and China convened their inaugural session of the economic working group. This group serves as a platform for engaging in discussions pertaining to bilateral economic policy issues. The Treasury Department reported that the meeting between the US and Chinese delegations took place virtually and proved to be both productive and substantive, covering topics related to domestic and global macroeconomic developments.

USDJPY Analysis:

USDJPY is moving in the Box pattern and the market has fallen from the resistance area of the pattern

The Bank of Japan announced its plan to purchase Japanese Government Bonds (JGB) with a total value of 300 billion JPY in the 5-10 year maturity range and an additional 100 billion JPY in the 10-25 year maturity range.

The US Treasury Department disclosed that virtual meetings between the United States and China have effectively facilitated discussions on macroeconomic developments, resulting in productive and valuable exchanges.

The Bank of Japan made an announcement on Tuesday, revealing plans for an unscheduled bond operation to take place on Wednesday. During this operation, the BoJ intends to purchase Japanese government bonds with a total value of 300 billion yen. These bonds will have maturities ranging from five to 10 years. Additionally, the BoJ plans to acquire 100 billion yen worth of bonds with maturities falling in the range of 10 to 25 years.

The US Dollar (USD), as measured by the US Dollar Index (DXY), has dipped to the 105.55 range. The decline in US Treasury yields is leading the market to speculate on a reduced likelihood of a Federal Reserve (Fed) interest rate hike, resulting in waning interest in the US Dollar. Recent data from the US economy indicates robust economic activity. This week, Thursday will bring the preliminary estimate of Q3 Gross Domestic Product (GDP), followed by the release of September’s headline and core measures of the Personal Consumption Expenditures (PCE) on Friday. The core PCE is the Fed’s preferred indicator of inflation. Both of these data points will provide a clearer picture of the US economy and could significantly influence expectations for the Fed’s upcoming decisions on November 1 and in December.

At the time of writing, the US Dollar Index has slid to 105.60, marking a nearly 0.50% decrease. Monday’s economic calendar doesn’t hold any significant highlights, so attention is shifting to the high-impact economic figures scheduled for release later in the week. It is anticipated that Q3 Gross Domestic Product will show acceleration. Meanwhile, on Friday, the Core PCE Price Index is expected to register at 3.7% year-on-year, down from the previous 3.9%. Simultaneously, US Treasury yields are declining, with rates for the 2-year, 5-year, and 10-year bonds standing at 5.07%, 4.80%, and 4.84%, respectively. According to the CME FedWatch Tool, the probability of a 25 basis points hike at the December meeting remains low, hovering near 30%.

USDCHF Analysis:

USDCHF is moving in the Descending channel and the market has fallen from the lower high area of the channel

The conflict between Israel and Gaza has generated concerns in the Middle East, leading to daily appreciation of safe-haven currencies such as the Swiss Franc due to increased demand. If the Swiss ZEW economic survey prints at -27.6 in September, indicating further declining numbers, Switzerland may potentially encounter more challenging labor and business conditions.

The Swiss Franc is facing challenges due to the decline in the US Dollar (USD), which can be attributed to the dovish remarks made by US Federal Reserve (Fed) officials. The Swiss Franc is typically considered a safe haven, and it may have found support amid geopolitical tensions between Israel and Hamas. However, diplomatic efforts to ease tensions in the Israel-Hamas Gaza Strip have reduced market risk aversion, which, in turn, has boosted investors’ risk appetite. Investors will likely keep an eye on the ZEW Survey Expectations for October, scheduled for Wednesday. In September, the sentiment data stood at -27.6. If the upcoming data shows a further decline, it could signal worsening business conditions and labor market conditions in Switzerland.

The US Dollar Index (DXY) is continuing its four-day losing streak, possibly influenced by subdued US Treasury yields. The spot price of the US Dollar is hovering around 105.50. Although the 10-year Treasury yield briefly reached its highest point since 2007 at 5.02%, it swiftly reversed course, dropping to 4.85% in the latest update.

Regarding US Federal Reserve officials’ views, Atlanta Federal Reserve President Raphael Bostic expressed skepticism about a US central bank rate cut before the middle of next year. Fed Philadelphia President Patrick Harker favored maintaining existing interest rates, while Fed Cleveland President Loretta Mester suggested that the US central bank is either at or very close to the peak of the rate hike cycle.

Market watchers are preparing for a week filled with economic data. Tuesday will involve scrutiny of the US S&P Global PMI, followed by a close watch on Thursday for Q3 Gross Domestic Product (GDP) figures. The week will conclude with a focus on the Core Personal Consumption Expenditures (PCE) on Friday.

EURUSD Analysis:

EURUSD has broken the Descending channel in upside

Today, Eurozone PMI data is on the calendar, and economists will assess whether the Eurozone economy is poised for a second-half recovery based on the results.

Let’s shift our focus back to the Euro. Analysts at Commerzbank have assessed the outlook for the single currency. Today, the publication of Eurozone PMIs is anticipated, and these figures are expected to further dampen any prospects of an economic recovery. These indicators are likely to validate the forecasts of our experts, who anticipate a contraction in the Eurozone economy during the latter part of this year. Consequently, if the PMIs fail to stabilize and perhaps even surprise on the downside, it could exert downward pressure on the Euro.

The actions taken by the European Central Bank (ECB) this week may not necessarily be determinative. The real question appears to revolve around the duration for which key interest rates will remain at their current levels before potentially undergoing further easing. The market perceives the likelihood of this occurring as early as the spring. Should the PMIs corroborate this expectation, it might lead to downward pressure on the Euro today. Furthermore, if the ECB adopts a cautious tone on Thursday regarding the future economic outlook, the Euro could face even more challenges. Conversely, our experts do not anticipate the ECB to reduce its key interest rates in 2024. This expectation is likely to bolster the Euro if the market must subsequently adjust its projections. However, this adjustment may still be some time away, and in the interim, the Euro could face downward pressure due to growing expectations of interest rate cuts stemming from weaker economic data.

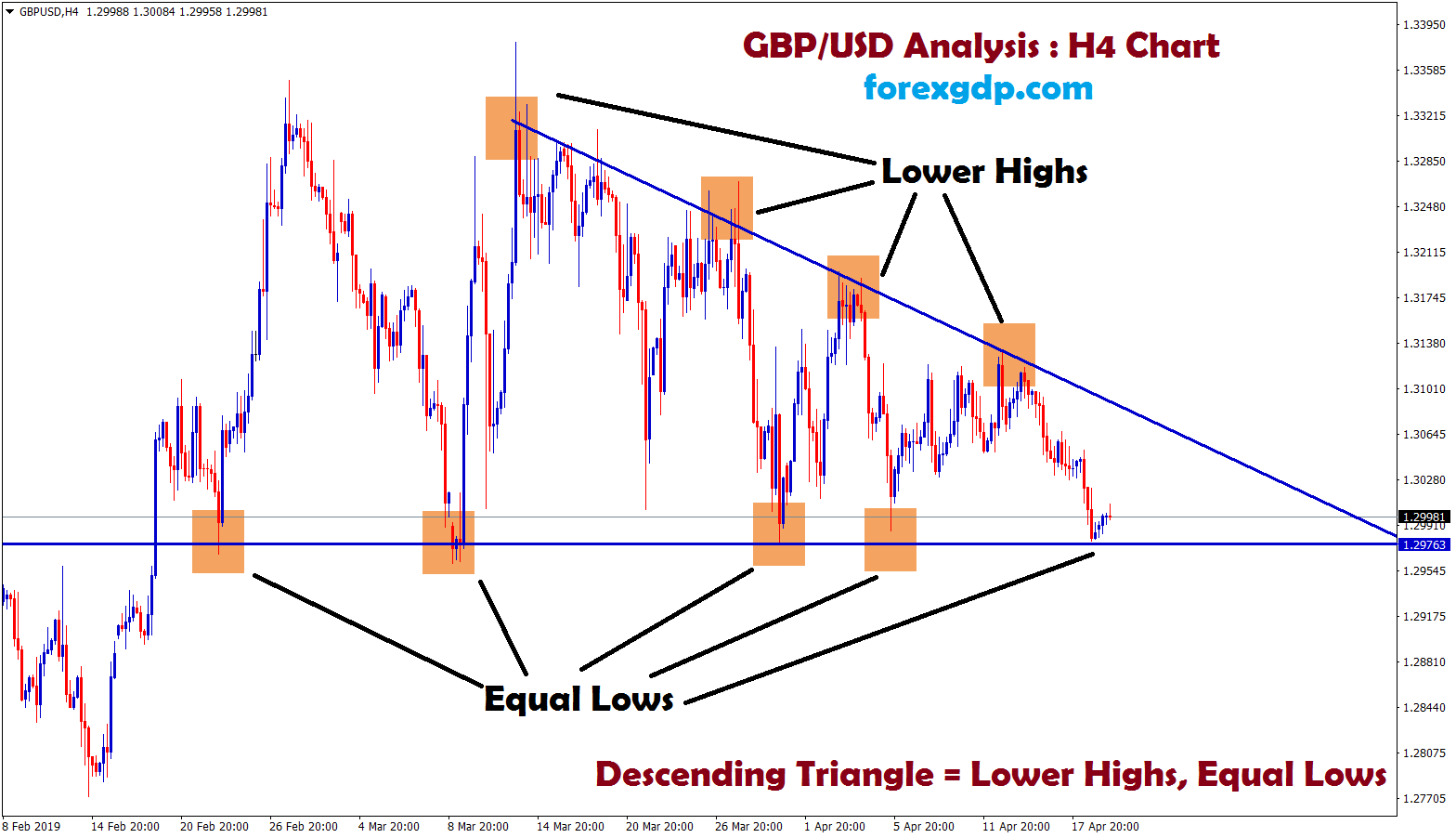

GBPUSD Analysis:

GBPUSD is moving in the Descending channel and the market has reached the lower high area of the channel

The UK’s Q3 employment data delivered a surprise with only -82,000 job losses, compared to the anticipated -198,000 layoffs. Additionally, the unemployment rate declined to 4.2% in the June-August period, surpassing the expected 4.3%. This decrease in job demand within the UK may pave the way for future inflation to recede.

The Pound Sterling (GBP) is gaining strength and making strides towards the critical resistance level of 1.2300. This upward momentum is fueled by improved market sentiment and better-than-expected employment data. According to the UK Office for National Statistics (ONS), the labor market recorded its third consecutive quarter of job losses in the period up to August. However, the number of job losses was lower than initially anticipated. Additionally, the Unemployment Rate decreased and remained below expectations, suggesting a stable labor market situation. The demand for labor in the UK has significantly slowed down due to an increasingly challenging demand environment, partly driven by the Bank of England’s (BoE) efforts to combat consumer inflation by raising interest rates. The BoE’s next interest rate decision, scheduled for November 2, has become a focal point for investors. The BoE is widely expected to maintain its interest rates at the current level of 5.25%, given the growing signs of economic weakness. In the short term, the Pound Sterling is poised for further gains due to improved market sentiment and favorable UK labor market data.

The UK ONS reported a decrease of 82,000 jobs in the June-August period, significantly lower than the expected 198,000 layoffs. Over the three-month period ending in July, employment declined by 207,000. This sustained reduction in employment over three consecutive months suggests that businesses have been cutting their workforce due to weak demand. Notably, the Unemployment Rate fell to 4.2% for the three months ending in August, surpassing expectations and the previous reading of 4.3%. In September, the Claimant Count Change increased by 20,400, well above the economists’ projection of a marginal increase of 2,300. In August, only 900 individuals claimed jobless benefits. It’s worth noting that the labor market data was initially expected last week, but the Labour Force Survey (LFS) reported inconsistencies in comparison with tax data and employer surveys. Investors should be aware that the Employment Change and Unemployment data are experimental adjusted estimates due to low response rates affecting the usual data collected by the LFS.

GBPCHF Analysis:

GBPCHF has broken the Descending channel in upside

A Reuters poll indicates that the Bank of England is likely to keep interest rates unchanged at 5.25% on November 2. This decision is influenced by the absence of supportive economic indicators and the confidence expressed by BoE Governor Andrew Bailey that inflation will significantly decrease in the coming month. Key economic indicators such as UK Manufacturing and Services PMI are currently below the 50.0 threshold, signaling weak economic activity. Additionally, labor demand has slowed, and Retail Sales have contracted, which may dampen consumer inflation expectations. The overall market sentiment remains subdued, primarily due to ongoing tensions in the Middle East, where Israeli military troops are considering a ground assault in Gaza. Gaza health authorities have reported 5,000 deaths and over 15,000 civilian injuries.

On Monday, the GBPUSD pair staged a strong recovery, largely in response to a sell-off in the US Dollar Index (DXY), which retreated sharply to around 105.50. This drop in the USD Index was driven by a decline in long-term US Bond yields from their multi-year highs above 5%. The 10-year US Treasury yields have retreated in anticipation of upcoming key US economic data scheduled for release later in the week. Investors are closely monitoring data such as Q3 Gross Domestic Product (GDP), the Federal Reserve’s preferred inflation gauge, and Durable Goods Orders. Concerns are mounting among investors about deteriorating financial conditions, driven by higher yields and Middle East tensions, which could potentially lead to a slowdown in the US economy.

CADCHF Anlaysis

CADCHF is moving in the Descending channel and the market has rebounded from the lower low area of the channel

The Bank of Canada’s decision to keep interest rates unchanged this week is widely anticipated, primarily due to concerns about persistently low inflation and declining retail sales over the past three months.

The Canadian Dollar is experiencing a lift as the new trading week begins, primarily driven by a resurgence in investor risk appetite during early trading. The upcoming week will witness significant data releases, including the US Purchasing Manager Index , US Gross Domestic Product , and US Personal Consumption Expenditure Index, which are expected to generate substantial market activity around the US Dollar . On Wednesday, the Bank of Canada is scheduled to announce its latest rate decision, followed by a press conference. It is widely expected that the BoC will maintain its reference rate at 5%, but market participants will closely scrutinize any hints regarding the central bank’s future considerations regarding rate cuts. The CAD’s strength is further supported by the prevailing broad-market dynamics that are exerting downward pressure on the USD.

However, the CAD faces some limitations due to declines in Crude Oil prices on Monday, which can curtail the potential upside in the currency, given its close ties to the oil market. Tuesday will bring the release of US PMI figures, potentially overshadowing the low-impact Canadian housing price data. The Canadian New Housing Price Index is anticipated to show a 0.1% increase in September. Meanwhile, US PMI components are expected to decline slightly, with Manufacturing forecasted at 49.5 and Services projected at 49.9. The BoC’s upcoming rate decision is widely anticipated to keep the rate at 5%, but investors are eagerly watching for any indications that the Canadian central bank may start considering rate cuts in the near future. Additionally, the easing of potential supply constraints arising from the Gaza Strip conflict, as diplomatic efforts aim to reduce Middle East tensions, has contributed to a decline in oil prices, thereby affecting the CAD’s performance.

AUDNZD Analysis:

AUDNZD is moving in the Descending channel and the market has reached the lower high area of the channel

The New Zealand Dollar has depreciated against the US Dollar in anticipation of this week’s scheduled release of US Q3 GDP data and a speech by Federal Reserve Chair Powell.

The economic calendar lacks significant New Zealand-specific data, leaving the NZD vulnerable to shifts driven by market reactions to US growth and inflation figures. On Tuesday, attention turns to the US Purchasing Manager Index (PMI) data for October. Both components of the PMI are expected to show slight declines: the Manufacturing PMI is forecasted to drop from 49.8 to 49.5, while the Services PMI is anticipated to fall from 50.1 to 49.9, indicating a potential return to contraction territory for the services sector.

Wednesday brings a speech by Federal Reserve (Fed) Chairman Jerome Powell, followed by US Gross Domestic Product figures on Thursday. US GDP is expected to show an acceleration in the third quarter, rising from 2.1% to 4.2% on an annualized basis for the third quarter. The week concludes with another important US inflation indicator: the Personal Consumption Expenditure Index data for September. It is expected to increase from 0.1% to 0.3%. Rising underlying inflation figures pose a challenge for overall market sentiment, as investors hope for a shift in Fed interest rate expectations. However, stubborn inflation is likely to be a significant hurdle for the US central bank to overcome before considering rate cuts. The current “dot plot” from the Fed doesn’t indicate any rate cuts until the latter half of 2024 as it stands.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/