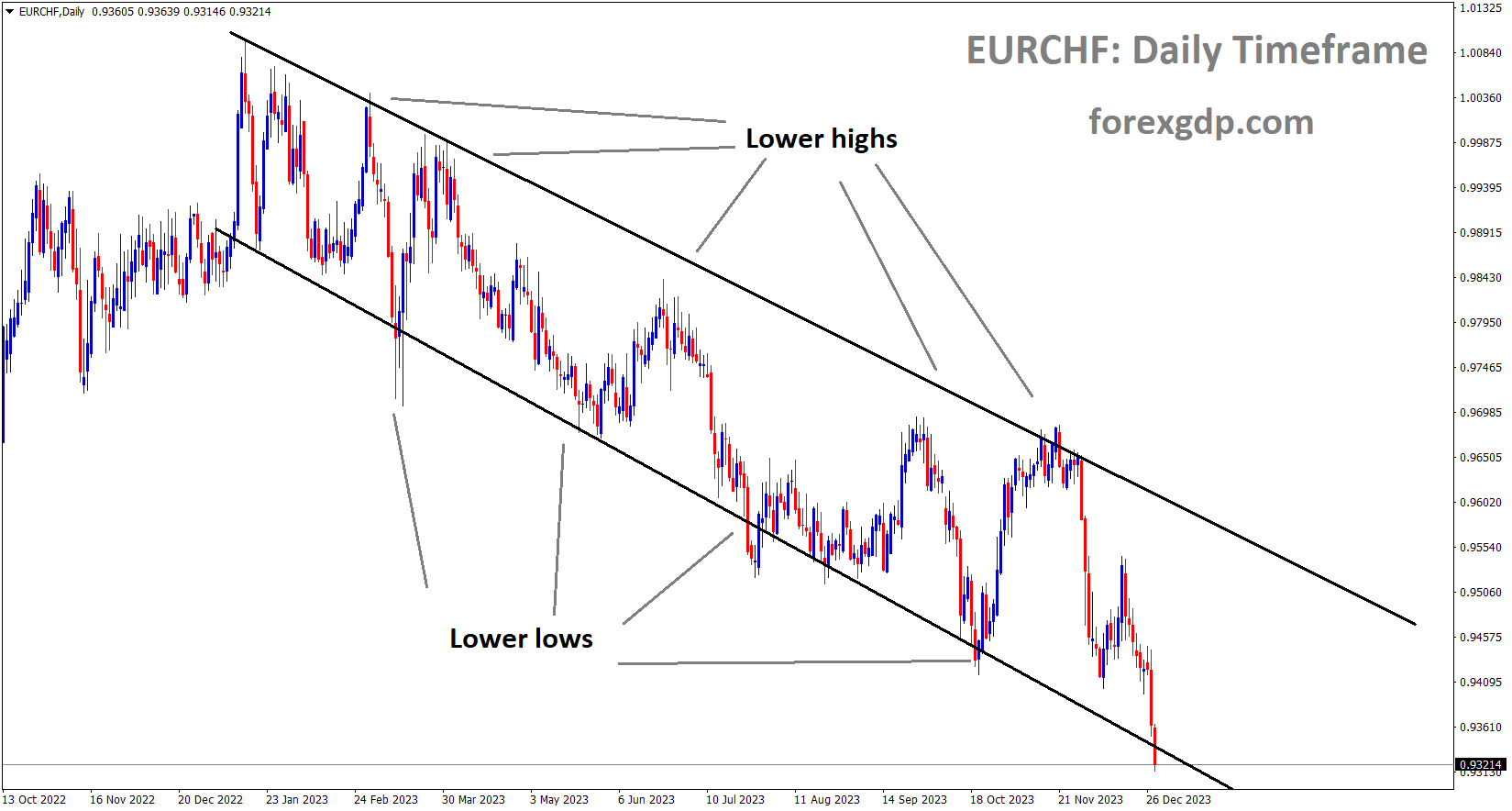

EURCHF Analysis:

EURCHF is moving in the Descending channel and the market has reached the lower low area of the channel

The Euro currency has strengthened against the USD as the European Central Bank (ECB) has announced that there will be no rate cuts in the first quarter of 2024. The ECB emphasized that their decision will be fully dependent on data.

The Euro continues to hold its ground at four-month highs, thanks to the weakening Dollar driven by expectations of Fed rate cuts. In the previous week, the US PCE Price Index saw a decline to 2.6% year-on-year, down from the revised 2.9% in October. Meanwhile, the Core PCE Prices Index, which excludes the influence of seasonal items like food and energy, also showed a more moderate decrease, settling at 3.2% from October’s 3.4%. However, it fell short of the expected 3.3% and remained well below the peak of 5.6% recorded in April 2022. The Core PCE Prices Index, excluding seasonal items, is expected to maintain a steady 0.2% growth rate, with a year-on-year decrease to 3.3% from 3.5%.

has announced that there will be no rate cuts in the first quarter of 2024")

These figures have solidified investors’ expectations of Fed rate cuts in early 2024. Futures markets are currently pricing in a probability of more than 70% for a quarter-point rate cut in March and a total of 150 basis points in cuts throughout 2024, as indicated by the CME Group FedWatch Tool. US Treasury yields continue to decline, with the benchmark 10-year yield at 3.85%, over 100 basis points below the peak reached in late October. This downward pressure on the US Dollar persists. Although this week’s economic calendar is relatively light, the positive sentiment may continue to bolster the Euro before the focus shifts to crucial Eurozone macroeconomic releases.

GOLD Analysis:

XAUUSD Gold price is moving in an Ascending channel and the market has fallen from the higher high area of the channel.

The price of gold surged to $2,080 as tensions escalated in the Red Sea due to a rebel attack. This increase was further fueled by the dovish stance of the United States, which raised hopes of a rate cut.

After the Christmas break, Gold prices resumed their upward trajectory, fueled by escalating geopolitical concerns. The precious metal saw a 0.7% increase in value on that day, driven by growing demand for safe haven assets. Geopolitical tensions have significantly boosted the appeal of safe havens among market participants, and the data from the United States leading up to the Christmas break did little to provide support for the US Dollar. The limited trading volume and liquidity during this week could serve as a relief for those bearish on Gold, potentially constraining its upward movement. The US Dollar’s recent weakness can be attributed to a series of disappointing data releases in the week before Christmas, causing market participants to maintain a cautious outlook on US interest rates for 2024, which has, in turn, weighed on the US Dollar.

Looking ahead, it is evident that there are few catalysts this week, and with subdued trading volume expected, the possibility of rangebound trading becomes prominent. The surprising post-Christmas development has been the continued rally of US Equities, in stark contrast to the increased demand for safe haven assets like Gold. However, this shouldn’t be entirely unexpected, as US Equities have been diverging from the consensus view of market participants for some time now. This divergence was most pronounced in 2023 when, despite numerous downside risks, US Equities defied expectations and continued their ascent. Meanwhile, US Treasury Yields continue to decline, as indicated in the chart below, with both the 2-year and 10-year yields following a downward trajectory due to rising expectations of interest rate cuts.

SILVER Analysis:

XAGUSD Silver price is moving in the Box pattern and the market has reached the resistance area of the pattern

The US Dollar experienced a decline in value following the Federal Reserve’s dovish stance on interest rates, with the possibility of rate cuts occurring in the first half of 2024. Additionally, disappointing domestic economic data, lower than previous figures, contributed to the US Dollar entering negative territory.

On Wednesday, the DXY index, which measures the strength of the U.S. dollar, experienced its lowest point in five months. This decline was primarily driven by a significant decrease in Treasury rates, particularly the 2-year yield, which dropped below 4.26%, marking its lowest level since late May. It’s worth noting that these market movements may have been exaggerated due to reduced trading activity during this time of year. However, the main factor contributing to the dollar’s bearish performance in recent weeks has been the belief among investors that the Federal Reserve will implement substantial interest rate cuts in 2024.

The Federal Reserve’s shift in stance at its December FOMC meeting has further supported the existing market trends. During that meeting, the central bank adopted a more accommodative approach, signaling its willingness to discuss potential reductions in interest rates. This move is likely part of a strategy aimed at prioritizing economic growth over concerns about inflation. The chart below illustrates the ongoing decline of the DXY index, which has coincided with increasing expectations of monetary easing in the coming year.

USDJPY Analysis:

USDJPY is moving in the Descending channel and the market has fallen from the lower high area of the channel

The Bank of Japan’s summary of opinions indicates a negative impact on the Yen in the market. However, the fundamental backdrop of the USD provides support for the JPY’s strength in the market.

And Bank of Japan Governor Ueda conveyed in an interview with NHK that a rate change is anticipated in 2024, and it may occur even before smaller firms initiate discussions about wage increases. The BoJ’s primary objective is to achieve sustained wage hikes in conjunction with inflation. Monetary policy tightening in 2024 will only be considered once this goal has been achieved.

The Japanese Yen had a weak start to the post-Christmas trading day, largely due to the Bank of Japan’s Summary of Opinions, which revealed a divided panel leaning towards caution regarding a tighter monetary policy. While all members agreed to maintain the current ultra-loose policy for the time being, discussions about potential future changes and their timing are now underway. Some key statements from the panel include the need to ensure a sustainable and stable achievement of the price target before ending negative rates and Yield Curve Control.

Furthermore, the panel emphasized the importance of closely monitoring wage and price movements under YCC, considering that the strong upward pressure on prices appears to have stabilized. They also mentioned that they are not in a situation where they would be caught off guard by raising rates, even if they decide to wait until after assessing wage negotiations next Spring. One member expressed the view that the Bank of Japan should seize the opportunity to normalize its policy to prevent the risk of high prices negatively impacting consumption and hindering the achievement of the price target. They stressed the importance of continued in-depth discussions on issues such as the timing of exiting the current policy and the appropriate pace of rate hikes thereafter.

Overall, this news was received less favorably for the Yen and was further compounded by disappointing Japanese housing start data that fell short of forecasts. The decline in new construction projects has reached its lowest level since August, highlighting the challenges facing the Japanese economy. These data points will play a crucial role in determining the path toward a more normalized monetary policy in the context of heightened inflation.

In an interview with NHK, Bank of Japan Governor Kazuo Ueda stressed the absence of any immediate need to unwind the central bank’s highly accommodative monetary policy. He pointed out that the likelihood of inflation exceeding 2% and showing a significant upward trend was currently quite remote, stating, Currently, I do not perceive a substantial probability of such a scenario materializing. Ueda went on to explain that it would require a significant amount of time before data related to smaller firms becomes accessible, and he expressed doubts about Japan’s consistent ability to achieve the BOJ’s 2% inflation target.

As for the potential of raising short-term interest rates from negative territory in the upcoming year, Ueda indicated that it was not entirely implausible. He emphasized that a critical factor in this decision would depend on whether wage increases extended to smaller firms during the annual spring wage negotiations in 2024. However, Ueda also alluded to the possibility that the BOJ might choose to make a decision even before the outcomes of these negotiations are revealed, particularly if smaller firms demonstrate exceptionally robust profits.

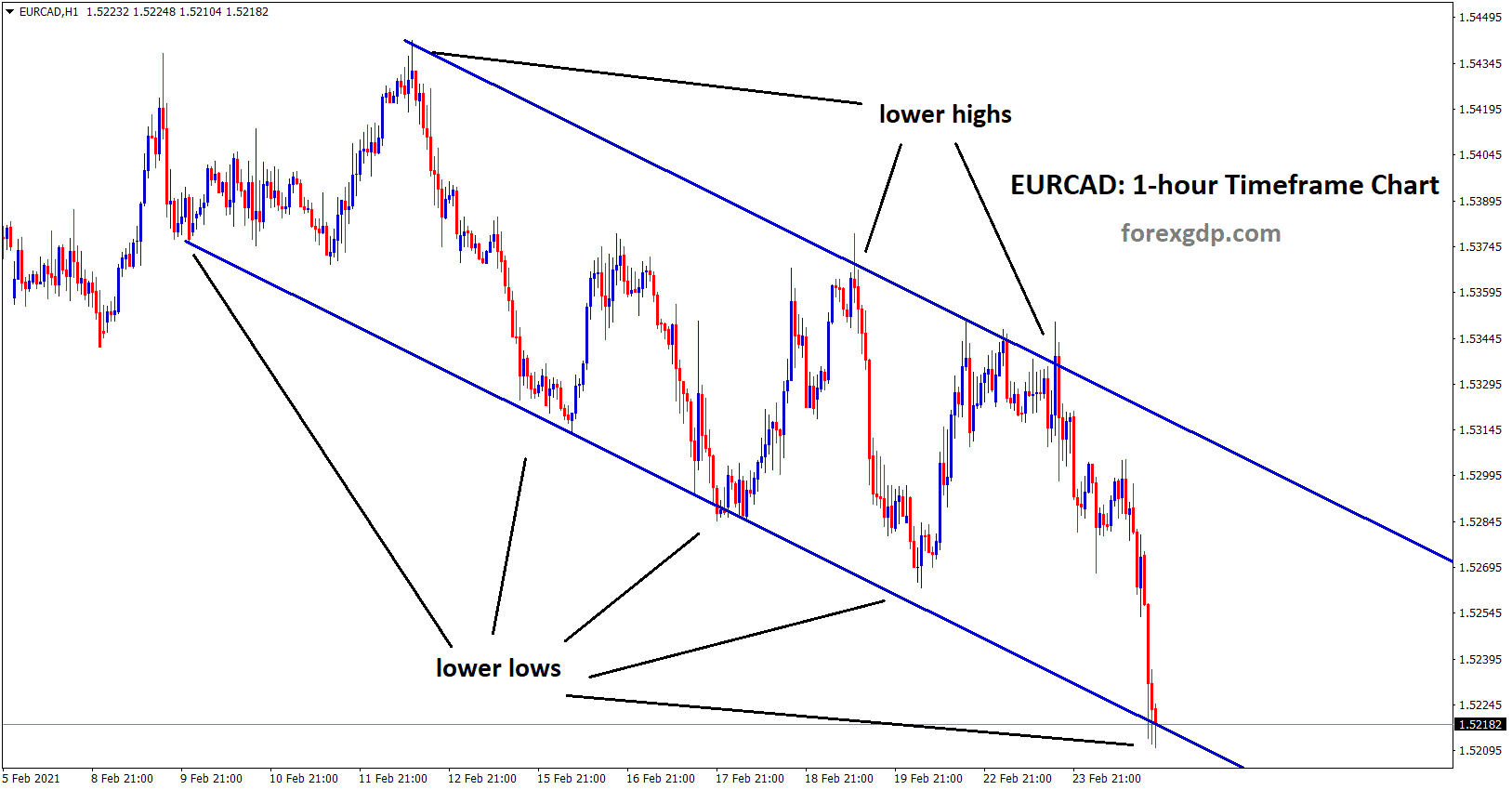

USDCHF Analysis:

USDCHF is moving in the Descending channel and the market has reached the lower low area of the channel

Today, the US Dollar has reached a historical low against the Swiss Franc, reminiscent of levels last seen in 2015. This decline is attributed to the potential closure of the Gibraltar Strait by Iran, a move that could severely disrupt maritime trade routes. This geopolitical tension is driving the Swiss Franc to strengthen in comparison to other currency pairs.

The USDCHF is encountering difficulties primarily due to the weakened US Dollar. Geopolitical tensions in the Middle East have intensified, prompting a surge in demand for the safe-haven Swiss Franc as investors adopt a risk-averse stance. During periods of heightened geopolitical uncertainty, assets like the CHF become sought after as havens of safety. One of the focal concerns revolves around the possibility of Iran closing the Gibraltar Strait, adding to the geopolitical complexities. Nevertheless, there are signs of a gradual return to normalcy in the region, as major shipping companies have started resuming operations in the Red Sea.

Market sentiment, as reflected by the CME Fedwatch tool, indicates a probability of over 88% for a rate cut by the Federal Reserve in March, with complete pricing in of a rate cut by May. These statistics underscore the prevailing expectations among investors that the Fed may consider implementing monetary policy easing measures. Furthermore, the softer inflation figures in the US Core Personal Consumption Expenditures provide additional support for the belief that the Federal Reserve might contemplate adjusting its monetary policy to address prevailing economic conditions. In terms of economic indicators, the US Richmond Fed Manufacturing Index recorded a significant decline of 11 points in December, contrary to the anticipated 7-point decrease and following a 5-point drop in November. Market attention is now turning towards Thursday’s releases of Initial Jobless Claims and Pending Home Sales in the United States, which are expected to offer further insights into the labor market and the state of the real estate sector.

GBPCHF Analysis:

GBPCHF is moving in the Descending channel and the market has reached the lower low area of the channel

The most recent domestic data for GBP has shown positive figures, leading to reduced expectations of a rate cut by the Bank of England when compared to other central banks. As a result, the GBP is maintaining a positive stance against the USD.

The US Dollar remains under pressure as investors speculate about potential interest rate cuts by the Federal Reserve. According to the CME Fedwatch tool, markets are currently pricing in a likelihood of more than 88% for a rate cut starting in March 2024, with expectations of more than 150 basis points in rate reductions for the upcoming year. Conversely, in the United Kingdom, the Bank of England (BoE) has signaled that rate cuts are not imminent.

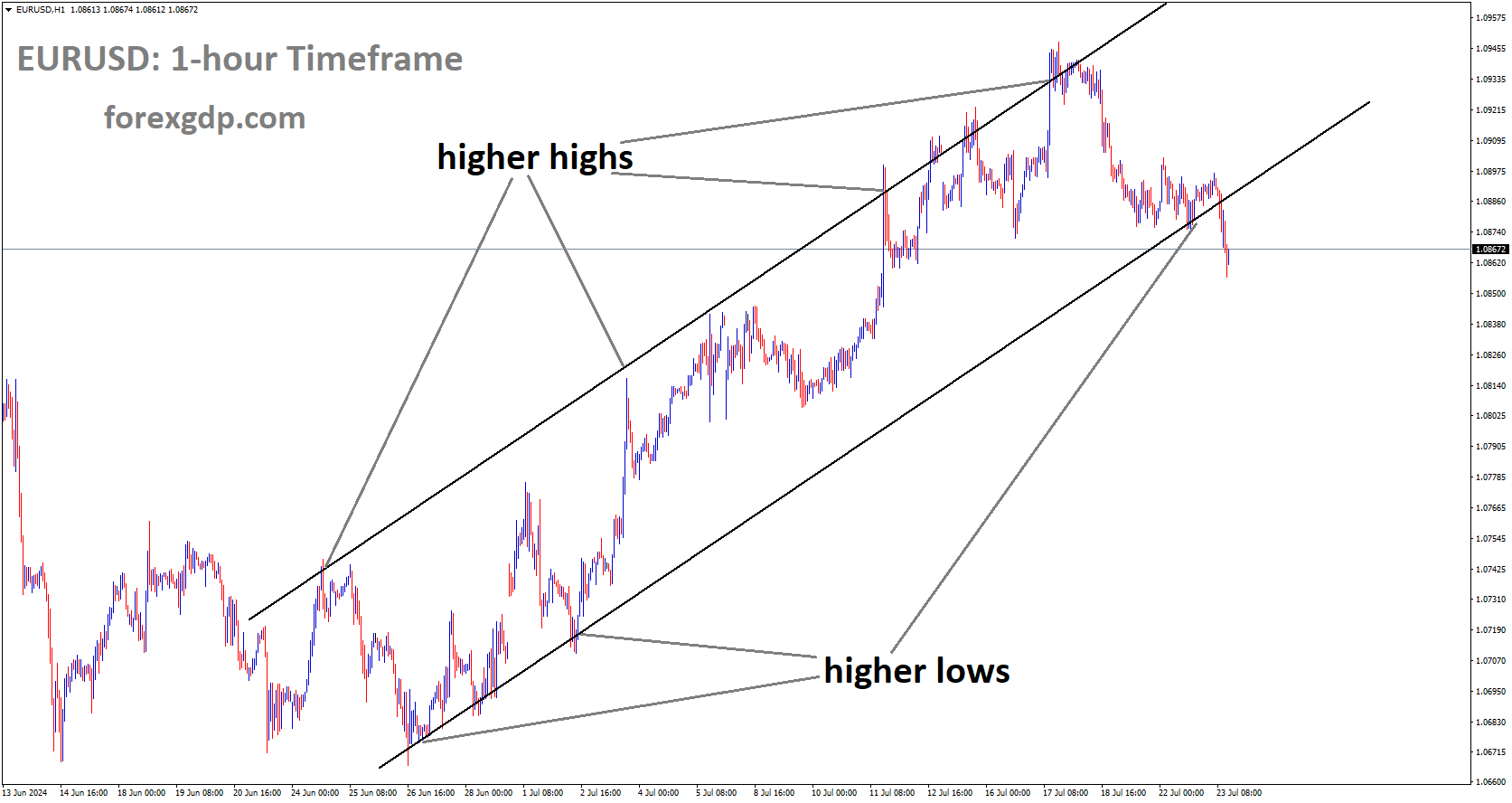

GBPUSD Analysis:

GBPUSD is moving in an Ascending channel and the market has reached the higher high area of the channel

The BoE has maintained its interest rates for the third consecutive meeting, affirming its commitment to keeping borrowing costs at the current level of 5.25% for an extended period. Policymakers at the central bank have previously stated that it is premature to discuss rate cuts. However, money markets anticipate interest rate cuts next year, with the first potential cut anticipated in May.

Amid the holiday season’s thin trading conditions, market sentiment is expected to continue influencing the movements of GBPUSD until the New Year. Later on Thursday, the United States will release data including Initial Weekly Jobless Claims, Trade Balance figures, and November’s Pending Home Sales. Additionally, the UK Nationwide Housing Prices and the US Chicago Purchasing Managers’ Index are scheduled for release on Friday.

CADCHF Analysis:

CADCHF has broken the Box pattern in downside

In December, the US Richmond Federal Reserve Manufacturing Index reported a reading of -11, a decrease from the -5 recorded in November. Consequently, the US Dollar depreciated against the Canadian Dollar on the previous day.

In Wednesday’s report, the US Richmond Fed Manufacturing Index for December plummeted to 11, a sharp decline compared to November’s reading of -5, and it fell short of expectations for a 7-point drop. This coincided with a dip in the value of the US Dollar, which reached its lowest point since July, hovering near 100.80. The drop in November’s US Core Personal Consumption Expenditure Price Index sparked expectations of early rate cuts by the Federal Reserve in 2024. As per the CME Fed Watch tool, the market is now pricing in a probability of over 88% for a rate cut to begin in March 2024, with more than 150 basis points of cuts priced in for the coming year.

Turning to the Canadian Dollar, it has gained strength thanks to the rebound in oil prices, acting as a headwind for the USDCAD pair. In addition, the Bank of Canada, in a recent meeting, did not rule out the possibility of an additional rate hike. However, market sentiment suggests that the likelihood of another rate increase has diminished, with investors widely anticipating that the next move by the central bank will be to lower interest rates at some point in the next year. Looking ahead, market participants will closely monitor the release of US Initial Weekly Jobless Claims, the Trade Balance for November, and Pending Home Sales on Thursday. It’s worth noting that these figures may not exert a significant impact on the market due to the current light trading volume.

AUDUSD Analysis:

AUDUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel

The inflation and housing data have revealed elevated levels, creating an opportunity for the Reserve Bank of Australia to consider another interest rate hike in February. Meanwhile, the Chairman of China’s NDRC has expressed a commitment to expanding domestic demand, facilitating a rapid economic recovery, and maintaining stable growth.

The Australian Dollar continues its ascent, driven by several factors. Subdued US Treasury yields have provided a favorable environment for the AUDUSD pair. Additionally, improved risk appetite among investors has lent support to the Australian Dollar, as they anticipate a dovish stance from the Federal Reserve in early 2024 regarding interest rates. Australia’s economic indicators, such as inflation and housing prices, are displaying resilience, potentially influencing the Reserve Bank of Australia to maintain its hawkish stance. Recent RBA forecasts suggest that inflation is nearing the upper boundary of the 2-3% target by the end of 2025. In their Meeting Minutes, the RBA emphasized the need to carefully assess additional data to gauge the balance of risks before making future interest rate decisions. It is widely anticipated that the RBA will refrain from cutting rates in its February policy meeting.

Meanwhile, China’s National Development and Reform Commission Chairman, Zheng Shanjie, has reaffirmed the country’s commitment to implementing familiar policy measures. During a meeting held on Tuesday, Zheng highlighted China’s dedication to expanding domestic demand, promoting a swift economic recovery, and ensuring stable growth. The US Dollar Index continues to weaken as the market anticipates potential rate cuts by the Federal Reserve in the first quarter of the upcoming year. This expectation is rooted in the Fed’s policy pivot in December, where rate expectations, as indicated by the dot plot, suggested the possibility of up to three cuts, totaling 75 basis points in rate reductions by the end of 2024. Notably, the US Richmond Fed Manufacturing Index recorded a significant decline of 11 points in December, surpassing market expectations of a 7-point drop. This follows a 5-point decrease in November and may influence market perceptions of economic conditions. Investors are likely to focus on Thursday’s releases of Initial Jobless Claims and Pending Home Sales for further insights.

RBA Private Sector Credit showed a 0.4% increase in November, exceeding the previous 0.3% rise. However, the Year-over-Year data indicated a decrease of 4.7%, compared to the previous 4.8% rise, underlining the RBA’s cautious approach in evaluating future interest rate decisions. In China, Industrial Profits for January to November year-on-year registered a decline of 4.4%, signaling a slowdown and indicating the need for additional policy support from Beijing to bolster the growth of the world’s second-largest economy. Former Dallas Federal Reserve President Robert Kaplan emphasized the Fed’s caution to avoid a scenario where monetary tightening becomes overly restrictive. In the US, the Housing Price Index contracted to 0.3% from the previous 0.7% in October, falling short of the expected 0.5%. The US Bureau of Economic Analysis reported that the Core Personal Consumption Expenditures – Price Index grew at 3.2% in November, slightly below the expected 3.3% and the prior 3.4%. Meanwhile, the month-on-month data remained consistent at 0.1%, falling short of the market’s 0.2% expectation. Lastly, the US Gross Domestic Product Annualized grew at a rate of 4.9% in Q3, slightly below the expected 5.2%.

NZDUSD Analysis:

NZDUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel

Positive business and consumer confidence data in New Zealand have bolstered the NZD, leading to its appreciation against the USD. Additionally, the Reserve Bank of New Zealand’s hawkish stance on policy settings is contributing to the NZD’s strength relative to the USD.

The New Zealand Dollar is benefiting from the improved consumer and business confidence in New Zealand. Additionally, the Reserve Bank of New Zealand’s hawkish stance has been a factor supporting the NZD. Analysts at ANZ are predicting that a global resurgence in risk appetite, coupled with the NZD’s advantageous carry trade position, will continue to drive its strength into 2024. In contrast, the US Richmond Fed Manufacturing Index for December came in at -11, a decline from the previous month’s -5 and falling short of market expectations of -7, as reported on Wednesday. On Thursday, the US is set to release the Initial Weekly Jobless Claims report, which is expected to show a rise of 210,000 for the week ending December 23.

The US Dollar has slipped to its lowest level since July, hovering around 100.85, largely due to the drop in the US Core Personal Consumption Expenditure Price Index for November. This has prompted speculation about early rate cuts by the Federal Reserve in 2024. Investors are anticipating that the Fed will maintain interest rates at its upcoming January meeting but may consider rate cuts as early as March next year. Looking ahead, market participants will closely monitor the US Weekly Jobless Claims, Trade Balance, and the November Pending Home Sales report, all scheduled for release on Thursday. Additionally, the Chicago Purchasing Managers’ Index for December will be published on Friday. However, it’s worth noting that these figures may not have a significant impact on the market as traders transition into holiday mode heading into 2024.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/