XAUUSD is moving in box pattern and market has fallen from the resistance area of the pattern

GOLD – US Inflation Trends, Market Responses, and Geopolitical Considerations

US CPI Inflation Trends: The Consumer Price Index inflation rate in the United States experienced a slight ease, dropping to 3.1% in January compared to 3.4% in December. This data, sourced from the U.S. Labor Department’s recent report, indicates a notable shift in inflationary pressures.

Monthly CPI Movement: On a monthly basis, the CPI saw a modest increase of 0.3% in January, up from the 0.2% rise observed in December. Similarly, the Core CPI, excluding volatile food and energy prices, exhibited a more substantial uptick of 0.4% in January, compared to 0.3% in the preceding month.

Core CPI Performance Over 12 Months: Over the course of the past year, the Core CPI surged by 3.9% year-over-year, surpassing market consensus expectations of 3.7%. This indicates a sustained inflationary trend that may have implications for monetary policy decisions.

Impact on Market Sentiment: The release of positive US CPI data prompted a reevaluation of market sentiment regarding potential interest rate adjustments. Traders adjusted their expectations for a rate cut, pushing back the anticipated timeline from May to June. This shift reflects a cautious approach by policymakers in responding to evolving economic conditions.

Treasury Yields Movement: Concurrently, there was an observed uptick in US Treasury yields, with the 10-year yield reaching 4.32% and the 2-year rate experiencing a notable jump to 4.654%. This surge marked the most significant single-day increase since May 5, 2023, signaling investor reactions to the inflationary landscape.

Gold Market Dynamics: The stronger-than-expected inflation data exerted selling pressure on gold prices, as it diminished expectations for an imminent rate cut by the Federal Reserve. This underscores the interplay between economic indicators and asset performance within financial markets.

Geopolitical Influences: Against the backdrop of economic developments, geopolitical tensions persisted, particularly in the Middle East and Eastern Europe. Ongoing conflicts, such as those involving Yemen’s Iran-aligned Houthis targeting vessels in the Red Sea, underscored the potential for geopolitical instability to impact market dynamics.

Safe-Haven Asset Considerations: Despite the economic implications of geopolitical tensions, traditional safe-haven assets like gold may experience increased demand in response to uncertainty. This underscores the complex interplay between geopolitical risk and investor behavior within global financial markets.

Upcoming Market Catalysts: Looking ahead, market participants are anticipated to closely monitor key events, including appearances by Federal Reserve officials and the release of additional economic data. Notably, attention will focus on US January Retail Sales figures and the Producer Price Index report, which are expected to provide further insights into economic trends and potential market movements.

EURUSD – USD Strengthens, EUR Reacts, Fed Rate Cut Speculation

EUR/USD Reacts to CPI Data:

Following the release of better-than-anticipated Consumer Price Index data, the EUR/USD currency pair experienced downward pressure. This movement reflected market reactions to the economic indicators shaping the currency pair’s dynamics.

EURUSD is moving in Descending channel and market has reached lower low area of the channel

US Dollar Strengthens on Rate Cut Speculations:

The US Dollar saw a notable strengthening as speculations surrounding a Federal Reserve interest rate cut in the upcoming March meeting subsided. This surge in the USD’s value was fueled by the unveiling of robust US inflation data for January, which dimmed expectations of an imminent rate adjustment by the Fed.

Market Anticipation of Fed Rate Cut:

Traders and analysts began recalibrating their expectations, with increasing consideration given to the possibility of a rate cut by the Federal Reserve, albeit likely deferred to June rather than March. This adjustment in market sentiment reflected evolving perceptions of the economic landscape and its implications for monetary policy decisions.

Euro Finds Support Amid Economic Indicators:

Despite the prevailing downward pressure on the EUR/USD, the Euro found a degree of support stemming from positive Economic Sentiment data originating from both the Eurozone and Germany, unveiled earlier in the week. This data release provided a brief respite for the Euro amidst broader market movements.

Speculation Surrounding ECB Rate Decisions:

Speculative discussions intensified regarding potential interest rate adjustments by the European Central Bank during the second quarter. Comments from ECB Executive Board member Piero Cipollone hinted at a potential pause in further tightening measures aimed at combating inflation, shaping market expectations for future ECB actions.

Shift in Market Sentiment:

Notably, there was a discernible shift in market sentiment, with expectations for an unchanged interest rate in the following month soaring to 93%. This marked a significant departure from prior forecasts, as investors pivoted towards considering the prospect of a Federal Reserve rate cut being postponed until June, reflecting evolving perceptions of economic conditions.

Reevaluation of Fed Rate Cut Expectations:

The unforeseen upside surprise in US inflation data prompted analysts at Commerzbank to reevaluate the likelihood of Federal Reserve interest rate cuts. As a result, there emerged speculation surrounding the previously anticipated rate cut slated for May, which now faced uncertainty amidst evolving economic indicators and shifting market dynamics.

USDJPY – USD/JPY Surges, Fed Rate Cut Expectations Shift

USD/JPY Reaches Three-Month Highs:

The USD/JPY pair surged to its highest levels in three months, driven by the release of US Consumer Price Index data which revealed inflation levels surpassing expectations. This movement underscored the significant influence of economic data on currency pair dynamics.

USDJPY is moving in Ascending channel and market has fallen from the higher high area of the channel

Strong January CPI Data:

January’s CPI figures exceeded forecasts, with the overall CPI reaching 3.1%, surpassing the anticipated 2.9%. Moreover, the Core CPI, which excludes volatile items, stood at 3.9%, outperforming expectations. These robust inflation figures dashed hopes for immediate rate cuts by the Federal Reserve, signaling ongoing inflationary pressures.

Wall Street Responds to Inflationary Data:

The release of the latest inflation data prompted losses on Wall Street as investors digested the news. January’s CPI figures, surpassing expectations, indicated a 3.1% year-on-year increase, albeit slightly below December’s 3.4%. Meanwhile, the Core CPI remained steady at 3.9%, contrasting with the forecasted 3.7% year-on-year figure.

Surge in 10-Year Benchmark Note Yields:

Yields on the 10-year benchmark note surged to 4.314%, marking an increase of over 13 basis points. This uptick reflected a shift in investor sentiment, as the possibility of Federal Reserve rate cuts diminished in response to the inflationary data, leading to adjustments in bond yields.

Market Sentiment via CME FedWatch Tool:

Analysis from the CME FedWatch Tool highlighted a notable shift in trader sentiment. Expectations for rate cuts in both March and May decreased, with increased probability seen for a rate cut in June. Consequently, the projected federal funds rate remained at 5.25%-5.50% for the initial months of 2024, according to market swaps.

Bank of Japan Policy Outlook:

The Bank of Japan presented a mixed stance on its future monetary policy. While data indicated a significant -14.1% year-on-year drop in Machinery Orders, suggesting economic weakness, the Producer Price Index remained stable at 0.2% year-on-year. Market participants anticipated a potential BoJ rate hike in June, but deliberations regarding the cessation of negative interest rates could be postponed pending sustained inflationary trends.

These developments underscore the intricate relationship between economic indicators, market reactions, and the shaping of monetary policy expectations, influencing both the USD/JPY currency pair and broader financial markets.

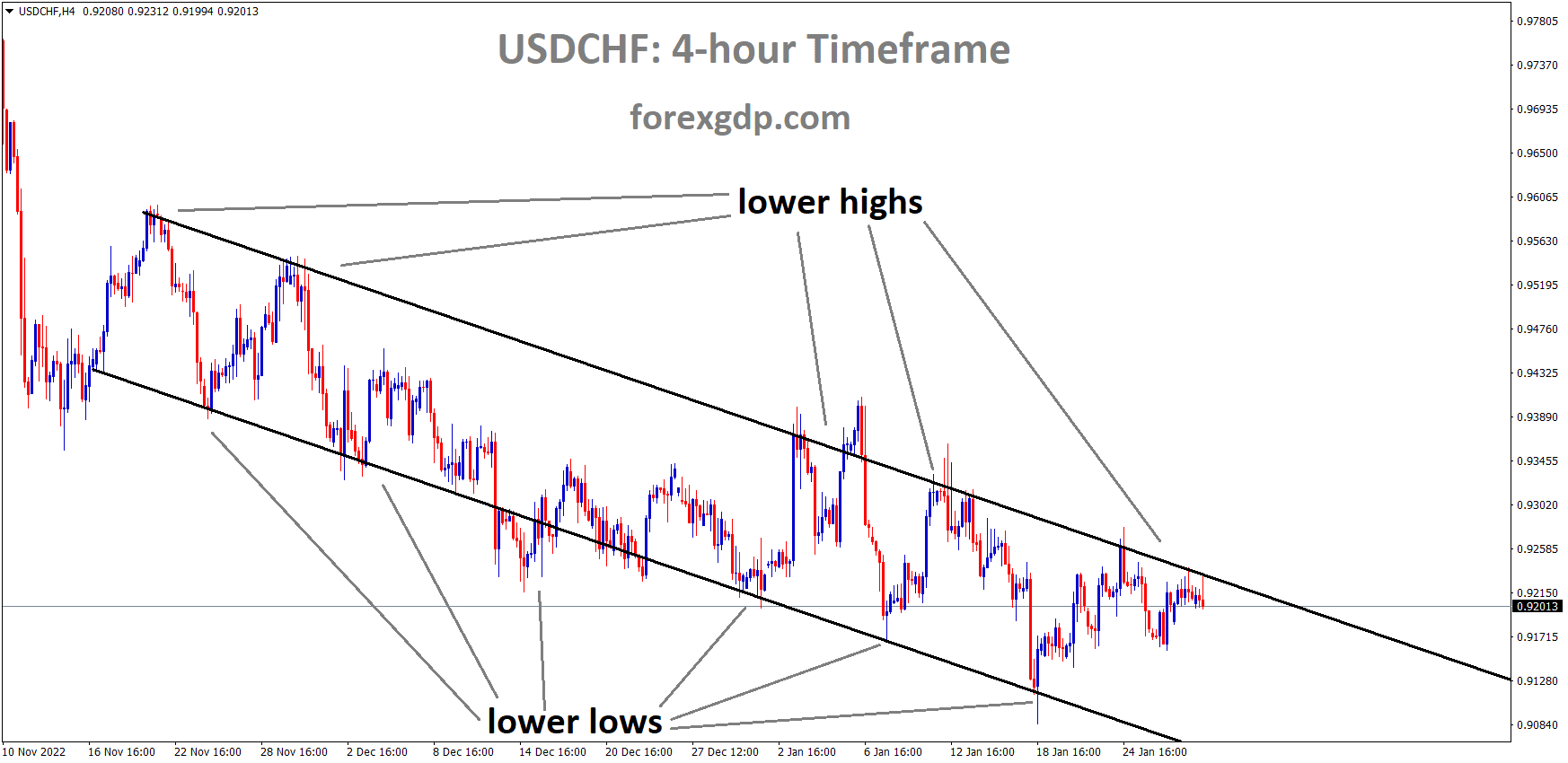

USDCHF – USD Outlook, SNB Policy, and Swiss Franc Trends

Upbeat Outlook for the US Dollar:

Investor sentiment towards the US Dollar remains positive, with expectations of the Federal Reserve implementing its first rate cut in July. This anticipation shapes the broader appeal for the USD amidst evolving market dynamics.

USDCHF is moving in Descending channel and market has reached lower high area of the channel

Potential Policy Shift by the SNB:

The Swiss National Bank may consider rolling back its restrictive interest rate stance sooner, driven by easing price pressures. This prospective policy adjustment reflects the SNB’s response to evolving economic conditions.

Swiss Franc Asset Sees Upside Potential:

The corrective move witnessed in the Swiss Franc asset is attributed to profit-booking following a strong rally spurred by January’s resilient United States inflation data. This suggests anticipated further upside for the Swiss Franc asset amidst prevailing market trends.

Market Sentiment and S&P500 Futures:

S&P500 futures record nominal gains in the Asian session, indicating a degree of alleviation in the prevailing risk-aversion sentiment. However, broader market sentiment remains negative, influenced by persistent US Consumer Price Index data postponing expectations of Federal Reserve rate cuts in the March monetary policy meeting.

Impact of Core CPI Data:

Core CPI data, excluding volatile food and oil prices, demonstrates steady growth at 3.9%, contrasting investor forecasts of a decline to the same rate. Fed policymakers typically consider core inflation data when formulating monetary policy remarks, with stubborn core inflation reinforcing arguments for maintaining interest rates at restrictive levels for an extended period.

Pressure on the Swiss Franc:

The Swiss Franc faces downward pressure as price pressures within the Swiss economy decelerate significantly. January’s monthly CPI growth of 0.2% follows stagnation in December, diverging from investor expectations of a 0.6% increase. Additionally, annual inflation decelerates to 1.3% from prior readings, prompting consideration for a shift in the SNB’s monetary policy stance.

Significance of Inflation Trends:

The deceleration in Swiss inflationary pressures highlights the evolving economic landscape, influencing the SNB’s policy decisions. As inflationary trends deviate from expectations, policymakers may adjust their approach to ensure economic stability and growth.

Implications for SNB Policy:

The moderation in Swiss inflation rates provides leeway for the SNB to recalibrate its monetary policy stance. This potential policy shift reflects the central bank’s commitment to maintaining price stability and supporting economic recovery amidst changing global economic conditions.

Market Response and Expectations:

Investor reactions to evolving inflationary trends and central bank policy shifts will shape market dynamics in the coming months. As market participants adjust their expectations and positions, currency valuations and asset prices may experience fluctuations.

The market outlook is influenced by expectations regarding US Dollar dynamics, potential shifts in SNB policy, and Swiss Franc performance. Evolving inflation trends and central bank responses underscore the importance of monitoring economic indicators and policy developments for informed decision-making in financial markets.

USDCAD – Impact of Inflation, Oil Prices, and Rate Expectations

USDCAD Soars Amid Surprising US Inflation:

USDCAD witnessed a significant 0.85% surge following unexpected upside in US inflation data on Tuesday. This unexpected development had notable implications for currency market dynamics, particularly affecting the US Dollar against the Canadian Dollar.

USDCAD is moving in box pattern and market has rebounded from the support area of the pattern

Crude Oil Prices Bolster Canadian Dollar:

The Canadian Dollar found support, partly due to higher crude oil prices. Notably, West Texas Intermediate crude oil prices traded around $77.50 per barrel, contributing to the CAD’s strength. Despite facing challenges, the resilience of crude oil prices aided in buoying the Canadian Dollar.

Fed Rate Adjustment Probability Reaches 93%:

Market sentiment shifted notably, with the probability of the Federal Reserve avoiding a rate adjustment in March surging to 93%. Investors began considering the potential for a rate cut by the Federal Reserve in June, reflecting changing expectations in response to economic data.

USD Decline and Weakening USD/CAD Pair:

The decline in the US Dollar was attributed to decreased US Treasury yields, subsequently weakening the USD/CAD pair. This weakening of the pair highlighted the intricate relationship between economic indicators, market sentiment, and currency valuations.

US Inflation Exceeds Expectations:

US headline Consumer Price Index data surpassed expectations, registering at 3.1%, albeit slightly lower than the previous rate of 3.4%. Similarly, the US Core CPI remained unchanged at 3.9%, defying market forecasts of a decline to 3.7% in January. These figures had immediate repercussions on currency markets, particularly impacting USDCAD.

Implications of Canadian Employment Data:

Recent Canadian employment data portrayed a healthier labor market picture, potentially leading the Bank of Canada to reconsider forecasts of rate cuts initially projected for April. BoC Governor Tiff Macklem’s remarks indicated a shift in the central bank’s focus towards discussing the duration of interest rates at current levels rather than deliberating on their adequacy.

Market Sentiment and Rate Expectations:

Overall, evolving market sentiment, coupled with shifting rate expectations and economic data releases, played significant roles in shaping the movement of USDCAD. The interplay of these factors underscores the complexities inherent in currency market dynamics and the importance of monitoring various indicators for informed decision-making.

Outlook for Crude Oil Prices:

Looking ahead, the trajectory of crude oil prices remains a key factor influencing the performance of the Canadian Dollar. Continued resilience or fluctuations in oil prices could have continued implications for USDCAD and broader market sentiment.

Fed Policy and Economic Indicators:

Furthermore, market participants will closely monitor future Federal Reserve policy decisions and economic indicators, as they continue to assess the impact on currency valuations and anticipate potential shifts in market dynamics.

The surge in USDCAD following unexpected inflation data, coupled with the impact of crude oil prices and shifting rate expectations, highlights the multifaceted nature of currency market movements. Investors and traders must remain vigilant in assessing various factors to navigate the evolving landscape of currency markets effectively.

EURJPY – Japanese Intervention and ECB Speculation

EUR/JPY Dips Amidst Japanese Intervention:

During the early European trading session on Wednesday, the EUR/JPY pair experiences a decline, shedding momentum as Japanese authorities intervene verbally in the foreign exchange market. Their statements prompt a boost in demand for the Japanese Yen, thereby exerting downward pressure on the EUR/JPY cross.

EURJPY is moving in Ascending channel and market has rebounded from the higher low area of the channel

Verbal Intervention by Japanese Authorities:

Masato Kanda, Japan’s top currency diplomat, issues a cautionary statement regarding recent FX market movements, emphasizing that authorities stand ready to take necessary steps to address any disruptive volatility. Similarly, Finance Minister Shunichi Suzuki underscores the undesirability of rapid FX fluctuations, signaling heightened vigilance and potential intervention measures to stabilize the market.

ECB’s Policy Speculations Drive Market Sentiment:

Speculation surrounding potential rate cuts by the European Central Bank amplifies market uncertainty. Despite maintaining benchmark rates at record highs since September 2023, concerns regarding sluggish economic growth and easing price pressures fuel expectations of rate adjustments. Investors anticipate the likelihood of the first rate cut occurring in either April or June, closely monitoring ECB officials’ statements for insights into the timing and extent of potential rate cuts.

Impact of ECB’s March Economic Outlook:

The ECB’s forthcoming outlook for inflation and economic growth in March assumes critical importance in shaping future monetary policy decisions. ECB Governing Council member Pablo Hernandez de Cos underscores the pivotal role of this outlook in determining the timing of interest rate adjustments. Market participants await these insights for clarity on the ECB’s stance and potential policy shifts.

Anticipation of Eurozone GDP Data:

Traders eagerly await the release of Eurozone Gross Domestic Product figures for the fourth quarter, scheduled for Wednesday. Additionally, December Industrial Production data is poised to provide further insights into economic performance. A stronger-than-expected economic performance could bolster the Euro, potentially mitigating downside risks for the EUR/JPY cross.

Potential Market Reaction to Lagarde’s Speech:

ECB President Christine Lagarde’s upcoming speech on Thursday holds significance for market participants, offering insights into the central bank’s policy direction and economic outlook. Traders scrutinize her remarks for indications of future ECB actions, which may influence trading decisions around the EUR/JPY cross.

Adaptation to Market Dynamics:

Investors closely monitor economic data releases, central bank communications, and intervention measures for trading opportunities. As events unfold, they adjust their strategies in response to evolving market conditions, seeking to capitalize on emerging trends and mitigate risks associated with volatility in the EUR/JPY cross.

The EUR/JPY pair reacts to Japanese intervention measures and ECB rate cut speculations, navigating through market uncertainties and economic data releases. Traders remain vigilant, adjusting their strategies based on central bank guidance and economic indicators to navigate the fluctuating landscape of the EUR/JPY cross.

EURGBP – GBP Weakens on UK CPI, EUR/GBP Reacts to ECB Outlook

UK CPI Data Disappoints Expectations:

The UK Consumer Price Index for January registers a year-on-year increase of 4.0%, falling short of the expected 4.2%. This weaker-than-anticipated economic data prompts reactions in currency markets, particularly affecting the Pound Sterling against other currencies.

EURGBP is moving in Descending channel and market has reached lower high area of the channel

Revised Rate Cut Expectations for 2024:

Traders adjust their expectations for rate cuts in 2024, anticipating a reduction of 118 basis points, down from the previously expected 145 bps at the beginning of February. This revision reflects evolving market sentiment and economic projections.

Eurozone GDP and Industrial Production Key Focus:

Traders closely monitor Eurozone GDP growth figures for the fourth quarter and December Industrial Production data, scheduled for release on Wednesday. These data points are anticipated to influence market sentiment and trading dynamics, particularly in currency pairs like EUR/GBP.

GBP Under Pressure, EUR/GBP Supported:

Weaker-than-expected UK economic data, as evidenced by the drop in UK CPI and slower-than-forecasted annual headline CPI growth, exerts selling pressure on the Pound Sterling. Consequently, EUR/GBP receives a tailwind, reflecting the relative strength of the Euro against the Pound.

UK CPI Highlights:

Recent data from the Office for National Statistics indicates a month-on-month decline of 0.6% in UK CPI for January, contrasting with a 0.4% rise in December. Annual headline CPI growth stands at 4.0% YoY, below the consensus expectation of 4.2%. Core CPI, excluding volatile food and energy prices, rises 5.1% YoY in January, slightly below the estimated 5.2%.

ECB Officials’ Statements:

European Central Bank chief economist Philip Lane and Governing Council member Pablo Hernandez de Cos provide insights into the ECB’s monetary policy outlook. Lane emphasizes that the timing and extent of rate cuts will hinge on the ECB’s progress towards its inflation target. De Cos underscores the significance of the ECB’s March outlook for inflation and economic growth in shaping monetary policy decisions.

Market Expectations for ECB Rate Cuts:

Despite initial expectations, the ECB maintains benchmark rates at a record high of 4% following its January meeting. Traders adjust their forecasts for the timing of rate cuts, with expectations now leaning towards April or June. This adjustment reflects evolving economic conditions and central bank guidance.

Volatility Ahead: Eurozone and UK GDP Figures:

Market participants await Eurozone GDP growth numbers for Q4 and December Industrial Production data, along with UK GDP growth figures for Q4, scheduled for release. These events have the potential to trigger market volatility and offer clarity on the direction of the EUR/GBP cross and broader currency markets.

Market Reaction and Trading Dynamics:

The release of economic data and statements from central bank officials are expected to shape market sentiment and influence trading decisions. Traders remain vigilant, analyzing developments to navigate currency market fluctuations effectively.

The impact of UK CPI data and ECB outlook statements underscores the interconnectedness of global economic factors in currency markets. As market participants digest incoming data and central bank guidance, currency pairs like EUR/GBP are likely to experience heightened volatility, presenting opportunities and challenges for traders.

GBPJPY – Pullback, JPY Demand, and BoE Speculation

Pullback from Multi-Year Peak:

GBP/JPY experiences a retracement during the Asian trading session on Wednesday, stepping back from the multi-year peak achieved in the prior session. The currency pair retreats from the significant level of 190.00, marking its highest point since August 2015.

GBPJPY is moving in Ascending channel and market has reached higher low area of the channel

Demand for Japanese Yen:

A surge in demand for the Japanese Yen is notable, driven by prevailing market sentiment favoring safe-haven assets. This uptick in demand contributes to the pullback in GBP/JPY, exerting downward pressure on the currency pair.

Verbal Intervention by Japanese Authorities:

Japanese authorities, including top currency diplomat Masato Kanda and Finance Minister Shunichi Suzuki, issue statements emphasizing vigilance over foreign exchange market movements. Their remarks signal a willingness to take appropriate measures, including intervention, to address rapid fluctuations in currency values.

Speculations Surrounding BoE Rate Cuts:

Market sentiment regarding potential rate cuts by the Bank of England influences GBP/JPY dynamics. Speculations have surfaced suggesting reduced likelihood of early rate cuts by the BoE, supported by favorable UK economic indicators such as lower-than-expected unemployment rates and resilient wage growth.

Anticipation of UK CPI Data Release:

Traders shift their focus towards the impending release of UK consumer price index data. This data release is expected to provide insights into inflationary trends within the UK economy, influencing market sentiment and GBP/JPY movement.

Impact of UK Economic Calendar:

The UK’s economic calendar for the week includes significant events such as the release of preliminary Q4 GDP figures and monthly retail sales data. These data points are anticipated to shape market expectations regarding the BoE’s future monetary policy decisions, impacting GBP/JPY dynamics.

Market Sentiment and Intervention Speculations:

Speculations regarding potential intervention by Japanese authorities and expectations of a shift in the Bank of Japan’s policy stance contribute to market sentiment. Traders remain cautious amidst uncertainties surrounding such intervention possibilities.

BoE Governor’s Testimony:

BoE Governor Andrew Bailey’s scheduled testimony later in the day garners attention from market participants. His remarks are anticipated to provide insights into the BoE’s policy outlook, potentially impacting GBP/JPY movement and trading decisions.

Expectations of Increased Volatility:

Traders brace for heightened volatility surrounding the GBP/JPY pair in response to upcoming economic data releases and central bank communications. This anticipation underscores the importance of monitoring developments closely to capitalize on trading opportunities.

The retreat in GBP/JPY, coupled with factors such as JPY demand, BoE rate cut speculations, and upcoming data releases, underscores the dynamic nature of currency markets. Market participants remain vigilant, adjusting their strategies in response to evolving market conditions and central bank policies.

AUDUSD – AUD/USD Rebounds on Weaker USD

AUD/USD Recovery Amid USD Softening:

The AUD/USD pair exhibits positive momentum on Wednesday, marking a partial reversal of recent losses attributed to a softer USD. This rebound sees AUD/USD climbing from its recent lows, following a downturn prompted by robust US consumer inflation data.

AUDUSD is moving in Descending channel and market has fallen from the lower high area of the channel

US CPI Data Boosts USD Bulls:

The release of US Consumer Price Index data, surpassing expectations with a 0.3% increase in January and a year-on-year rate of 3.1%, strengthens the position of USD bulls. Despite a slight easing from December’s figures, the CPI readings exceeded consensus estimates, reinforcing the likelihood of delayed Fed rate cuts.

Market Eyes Australian Employment Data:

Traders shift their focus towards upcoming Australian employment details slated for release on Thursday, seeking potential catalysts for market movements. This data holds significance for AUD/USD dynamics, with expectations of meaningful insights shaping trading sentiment.

Technical Recovery in AUD/USD:

AUD/USD attracts buyer interest, initiating a technical rebound from recent lows. This recovery follows the pair’s descent to its lowest level since November 14, propelled by the impact of robust US inflation data on currency markets.

US CPI Exceeds Expectations:

According to the US Bureau of Labor Statistics, the headline CPI surged by 0.3% in January, marking the highest increase in four months, while the yearly rate moderated to 3.1% from December’s 3.4%. These figures outpaced consensus forecasts, reinforcing market expectations regarding Fed rate adjustments.

Market Sentiment and USD Performance:

Despite a modest recovery in US equity futures and a retreat in US Treasury bond yields, the USD remains resilient. Market sentiment reflects increasing acceptance of the Fed’s stance on maintaining higher rates for an extended duration, limiting downward pressure on the USD.

Expectations for Fed Rate Decisions:

Investor sentiment has shifted, with the likelihood of a Fed rate cut in March being priced out entirely. Odds for such a move in April stand at approximately 35%, while speculation mounts that the Fed may defer rate adjustments until the June policy meeting. These expectations support US bond yields and curb potential USD downside.

Impact of RBA Governor’s Speech:

Attention turns towards an upcoming speech by Reserve Bank of Australia Governor Michele Bullock during the early Asian session on Thursday. Alongside this event, the release of key Australian monthly employment data is anticipated to inject volatility into AUD/USD trading, offering opportunities for market participants.

Bearish Undercurrent in AUD/USD:

Despite potential volatility surrounding upcoming economic releases, the prevailing fundamental backdrop suggests a bias favoring bearish traders. This assessment aligns with prevailing market conditions and indicates a continued downward trajectory for AUD/USD, given the prevailing sentiment.

The rebound in AUD/USD amidst USD softening, coupled with anticipation of Australian employment data, underscores the fluidity of currency markets. Traders are advised to remain vigilant, closely monitoring evolving factors shaping AUD/USD dynamics for informed decision-making.

SILVER – Bearish Outlook Signals Near-Term Losses

Silver Extends Losses, Approaches Two-Month Low:

Silver prices continue to decline, nearing a two-month low established in December. This persistent downward trend reflects ongoing selling pressure in the market, exacerbating losses from the previous session.

XAGUSD is moving in Descending channel and market has fallen from the lower high area of the channel

Bearish Technical Setup Supports Near-Term Losses:

The technical setup for silver favors bearish traders, reinforcing the potential for further near-term declines. The repeated failures near the critical 200-day Simple Moving Average and subsequent downward movement validate the negative outlook for XAG/USD.

Selling Pressure Persists in European Session:

During the first half of the European trading session on Wednesday, silver experiences continued selling pressure for the second consecutive day. This downward momentum contributes to the metal’s retreat toward the year-to-date low, signaling investor sentiment towards the precious metal.

Repetitive Failures Near Key SMA:

The repeated inability of silver prices to breach the crucial 200-day SMA underscores the significance of this resistance level. Each failed attempt reinforces the bearish sentiment and adds weight to the negative outlook for XAG/USD.

Oscillators Indicate Strong Bearish Momentum:

Technical oscillators on the daily chart depict a strong bearish momentum, as they remain deep in negative territory. Despite the downward movement, these indicators have yet to reach oversold levels, suggesting potential for further downside in the near term.

Analysis of Daily Chart Patterns:

A comprehensive analysis of the daily chart patterns reveals the persistent downward trajectory of silver prices. The failure to break above the 200-day SMA, combined with sustained selling pressure, reinforces the prevailing bearish sentiment in the market.

Market Sentiment and Investor Behavior:

Investor sentiment towards silver remains cautious, as evidenced by the ongoing selling pressure and reluctance to establish long positions. The lack of bullish momentum and the presence of technical indicators favoring bears contribute to a subdued market sentiment.

Impact of External Factors:

External factors, such as macroeconomic trends and geopolitical developments, may further influence silver prices in the near term. Investors closely monitor these factors for potential shifts in market dynamics that could either exacerbate or alleviate the current downward pressure on silver.

Potential Catalysts for Market Reversal:

While the current outlook for silver remains bearish, certain catalysts could trigger a reversal in market sentiment. These catalysts may include unexpected shifts in global economic indicators, geopolitical tensions, or changes in monetary policy stances by major central banks.

In summary, silver prices continue to decline, nearing a two-month low amid persistent selling pressure. The bearish technical setup, coupled with strong negative momentum indicators, suggests the potential for further near-term losses. However, market dynamics remain fluid, and investors should closely monitor developments for any signs of a potential reversal in sentiment.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/