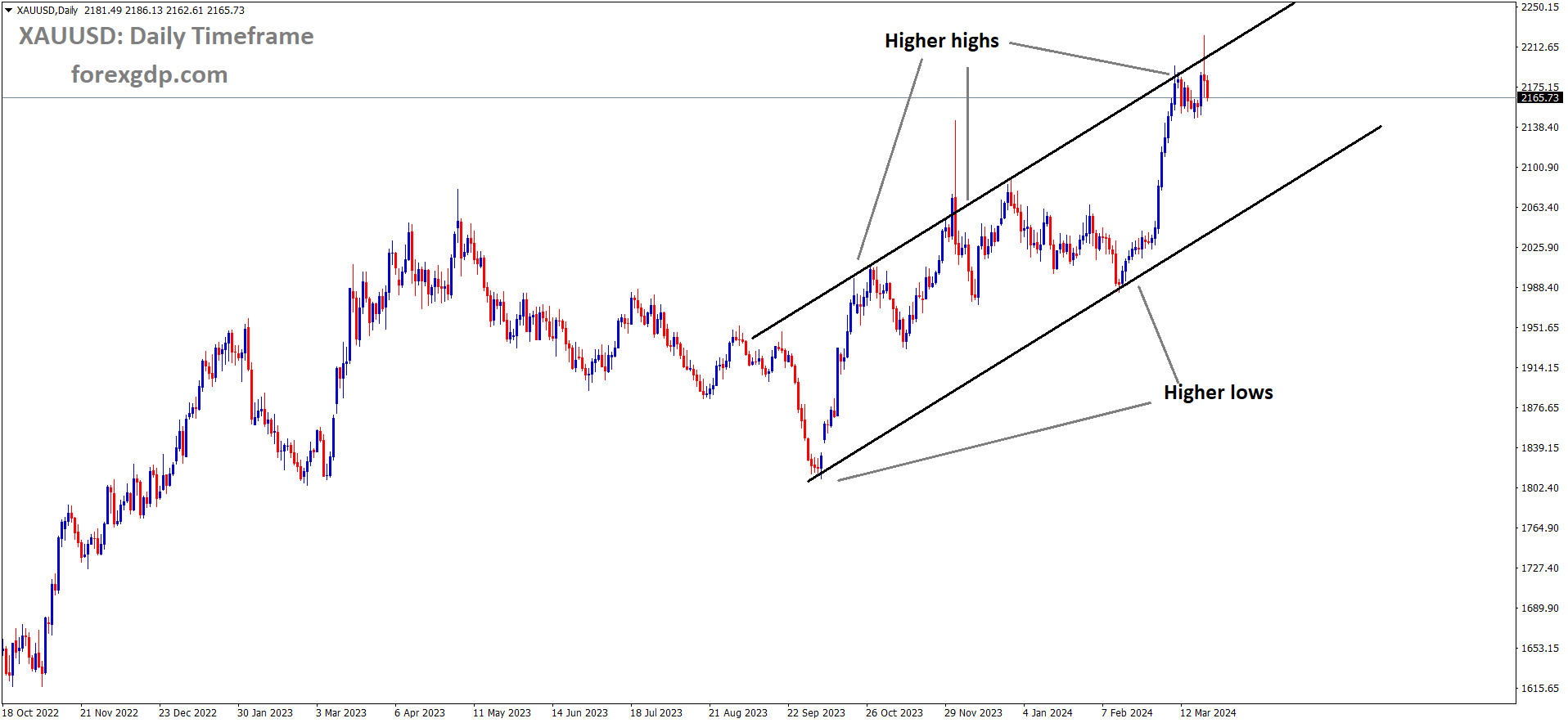

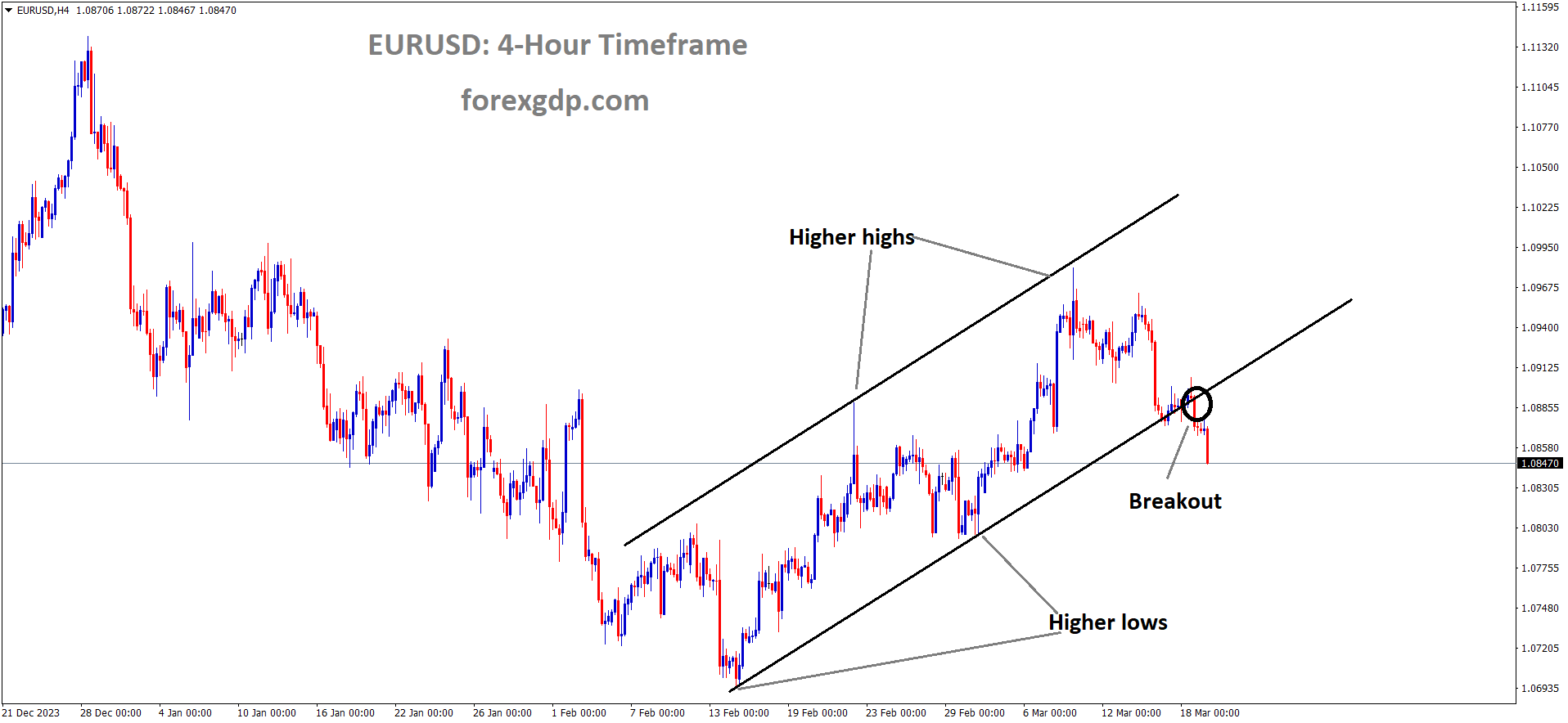

EURUSD has broken the Ascending channel in downside

EURUSD – ECB’s de Guindos: Patience Required as Services Inflation Persists

ECB Vice President Luis De Guindos said Service inflation is stickier in the Euro zone. So we wait until June month for rate cut. We do not dependent on FED rates move, we are solely decided on rates based on our Euro zone environment.

European Central Bank (ECB) Vice President Luis de Guindos remarked in a Tuesday interview, Services inflation is resistant. Therefore, patience is warranted.

Key points:

– The trajectory of wages remains pivotal, with further insights expected by June.

– While monitoring developments in the US economy, the ECB remains reliant on data, not influenced solely by the actions of the Federal Reserve.

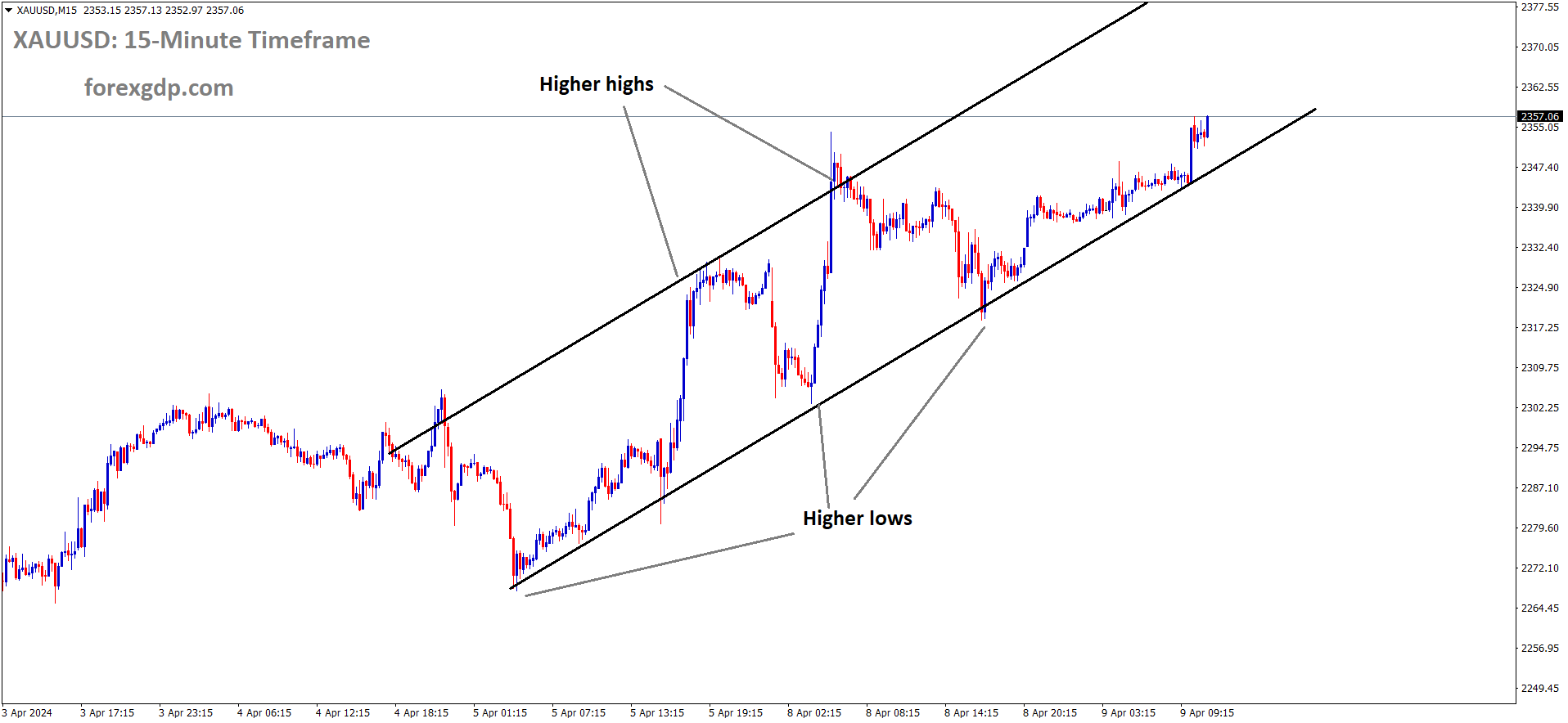

XAUUSD – GOLD Price Vulnerable Near One-Week Low Amid Fed Expectations

The Gold prices are trading lower against USD due to FED monetary policy meeting tomorrow. FED mostly do rate neutral at this meeting, June month rate cut is most probably do as per economists poll. Ukraine- Russia war existing and Israel and Gaza war extending makes safe deposits like Gold prices are increasing against USD.

XAUUSD Gold price is moving in the Descending triangle pattern and the market has reached the support area of the pattern

The price of gold continues to hover close to a one-week low, reflecting ongoing concerns driven by the prevailing hawkish sentiment regarding the Federal Reserve (Fed). This sentiment has contributed to the rise in US Treasury bond yields and bolstered the value of the US dollar (USD) to nearly two-week highs.

The anticipation surrounding the Fed’s stance on interest rates, particularly in terms of potential rate cuts, adds to the uncertainty in the market. Additionally, geopolitical tensions, such as the prolonged Russia-Ukraine conflict and unrest in the Middle East, serve as factors that could provide some level of support for gold prices.

Despite these potential sources of support, investors remain cautious and are awaiting guidance from the upcoming Federal Open Market Committee (FOMC) meeting. The outcomes and announcements from this meeting are expected to provide clearer indications regarding the Fed’s economic projections, including any adjustments to its rate-cutting plans. These insights will likely play a significant role in determining the short-term direction of gold prices.

USDJPY – BoJ Interest Rate Raised to 0%, YCC Abandoned

The Bank of Japan hiked 10 basis points to 0.0% from -0.10% rate first time rate hike since 2007. The negative rate era ended now since 2016 implemented. The Bank of Japan said they are continue to buy the JGB Bonds in the market whatever is needed, if inflation achieved 2% target with the sustainable wage hikes then we do rate hikes accordingly and we reduce the JGB Bonds purchases buying . JPY is Depreciated against counter pairs after the rate hike.

USDJPY is moving in an Ascending channel and the market has reached the higher high area of the channel

BoJ Raises Interest Rate to 0%, Ends Negative Era

After its two-day meeting, the Bank of Japan (BoJ) decided to increase the interest rate by 10 bps to 0%, marking the first rise since 2007. This move concludes the negative interest rate policy initiated in 2016, aligning with market expectations.

Summary of BoJ Policy Changes:

– Overnight call rate targeted at 0% to 0.1%.

– 0.1% interest applied to excess reserves with BoJ.

– Continuation of JGB purchases at current levels.

– Cessation of ETF and J-REIT buying.

– Gradual reduction in CP and corporate bond purchases.

– Discontinuation of CP and corporate bond purchases in approximately one year.

– Decision on long-term JGB buying made by 8-1 vote.

– Unanimous decision on asset buying other than long-term JGBs.

– Unanimous decision on treatment of new loan disbursements.

– BoJ to flexibly increase JGB buying regardless of monthly schedule.

– Change in monetary policy framework announced.

– Virtuous cycle between wages and prices assessed.

– Expectation of achieving 2% price stability target.

– QQE, YCC, and negative rate policy considered fulfilled.

– Short-term interest rate to be primary policy tool.

– Accommodative financial conditions expected to persist.

– Continued JGB buying at current levels anticipated.

– Commitment to inflation overshooting on monetary base fulfilled.

– Preparedness for rapid yield rise with nimble responses.

– Moderate recovery expected in Japan’s economy.

– CPI likely to exceed 2% through fiscal 2024.

– Underlying CPI inflation seen gradually increasing.

– High uncertainties in Japan’s economy and prices.

– Attention to market, FX developments, and economic impact.

– Continued announcement of JGB buying plans with flexibility based on market conditions.

USDCAD – Canada CPI Preview: February Inflation Expected to Edge Up to 3.1%

The Canada CPI inflation data for February month is expected at 3.1% it is up from 2.9% in January month printed. The Rising inflation costs Canadian Dollar more positive if came today.

USDCAD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

Canada to Release CPI Figures: Expected 3.1% Year-on-Year Increase in February

Canada is set to unveil its latest inflation data on Tuesday, with Statistics Canada releasing the Consumer Price Index (CPI) for February. Projections suggest a year-on-year uptick of 3.1% in the headline figure, slightly surpassing January’s 2.9% rise. Monthly forecasts anticipate a 0.6% increase compared to the previous month’s flat reading.

In addition to the CPI data, the Bank of Canada (BoC) will release its Core CPI gauge, excluding volatile elements like food and energy costs. January’s BoC Core CPI showed a monthly increase of 0.1% and a year-on-year rise of 2.4%.

These figures will be closely watched as they could impact the trajectory of the Canadian Dollar (CAD) and shape expectations regarding the Bank of Canada’s monetary policy. Currently, the CAD has exhibited weakness against the US Dollar (USD), hovering near multi-session lows beyond the 1.3500 level.

What to Expect from Canada’s Inflation Rate?

Analysts anticipate a pickup in price pressures across Canada in February, aligning with trends observed in many G10 countries, particularly the US. Despite a downward trend since reaching 4% in August, CPI remains well above the Bank of Canada’s 2% target.

")

Confirmation of increased inflationary pressures could lead investors to speculate on the central bank maintaining its current restrictive stance for a longer period. However, further tightening of monetary conditions appears unlikely, according to comments from bank officials.

During the latest BoC meeting, Governor Tiff Macklem expressed optimism about the fight against inflation, citing progress made and anticipating continued advancements. He emphasized the importance of core inflation measures, suggesting that unchanged levels could hinder efforts to reduce overall inflation. Macklem assessed risks to the inflation outlook as reasonably balanced and noted the supportive role of well-anchored inflation expectations.

USDCHF – Swiss Franc Stable Before SNB Meeting

The Swiss Franc traded lower ahead of SNB meeting is scheduled this week. The inflation is 1.2% in February month it is below target of 2%. So SNB has to do rate cuts before Euro zone is expected.

USDCHF is moving in the Box pattern and the market has reached the resistance area of the pattern

Swiss Franc Steady Ahead of SNB Meeting

The Swiss Franc (CHF) remains largely unchanged as the week begins, with minimal fluctuations observed in its major pairs. All eyes are on the upcoming Swiss National Bank (SNB) policy meeting scheduled for Thursday.

Market sentiment suggests a 29% probability of the SNB reducing its current 1.75% policy rate during this meeting. Such a rate cut would likely weaken the Swiss Franc, as lower interest rates tend to deter foreign capital inflows.

The Swiss Franc faces vulnerability due to subdued inflationary pressures. Recent data from the Federal Statistical Office indicated a decrease in the Consumer Price Index (CPI) to 1.2% year-on-year in February, below the SNB’s expectations outlined in its December meeting.

While the SNB projected an average inflation rate of 1.9% for 2024, the current inflation rate lags considerably behind this estimate, standing at 1.2%. However, there was a slight uptick in monthly CPI, rising from 0.2% to 0.6% in February.

Thursday’s SNB meeting will also see the release of new medium-term inflation forecasts, potentially influencing monetary policy outlooks. A downward revision in inflation forecasts could signal a higher likelihood of future interest rate cuts, exerting downward pressure on the Swiss Franc.

Although the SNB often aligns its policies with the European Central Bank (ECB), the faster decline in inflation within Switzerland compared to the Eurozone suggests the possibility of independent rate cuts by the SNB.

Thomas Jordan, Chairman of the SNB, expressed concerns in February that the Swiss Franc had become overvalued for Swiss businesses. This sentiment, coupled with indications of increased Swiss Forex reserve sales, suggests potential intervention by the SNB to manage the currency’s value.

USD INDEX – USD Sees Upside Ahead of FOMC Decision

The US Dollar index moving higher ahead of FED interest decision happening tomorrow. Strong inflation with weak labour data shows investors’ confidence on FED rate cut is Junemonth.

USD Index is moving in an Ascending channel and the market has reached the higher low area of the channel

USD Index Up at 103.55; Focus on Fed Decision

The US Dollar Index (DXY) shows minor gains at 103.55 on Monday, supported by rising US Treasury yields. Investors await the Federal Reserve (Fed) decision on Wednesday and updated economic projections.

With inflation persisting and labor market data weaker, the US economy faces a critical juncture, influencing expectations on the timing of Fed easing. Initial cuts are anticipated in June.

Market Movers: DXY Rises Amid Rising Treasury Yields

The Fed is expected to adopt a patient approach toward policy easing, assessing signs of slowing US inflation progress. June presents a 65% chance of a rate cut, with full cuts forecasted by July.

Despite recent dovish comments by Powell, Fed officials remain cautious about premature monetary easing.

US Treasury bond yields are up, with the 2-year yield at 4.75%, the 5-year yield at 4.35%, and the 10-year yield at 4.33%.

GBPUSD – Sees Selling Pressure Near Mid-1.2700s Ahead of Fed, BoE Decision

The UK Inflation reading is moderating in current situation, So BoE do rate cuts in the August month is more expected from economists side, The BoE keep rates as it is as 5.25% in this week meeting is most expected from Economists.

GBPUSD is moving in the Descending channel and the market has reached the lower low area of the channel

GBP/USD Faces Selling Pressure Amid USD Strength, Eyes Fed and BoE Decisions

The GBP/USD pair experiences downward pressure during the early Asian session, influenced by the USD’s rise above 103.50 and higher US yields. Market attention is focused on upcoming central bank meetings, notably the Federal Reserve (Fed) and Bank of England (BoE) interest rate decisions. As of now, GBP/USD trades at 1.2726, marking a marginal 0.02% decline.

The Fed is expected to maintain its interest rate for the fifth consecutive time at its March meeting on Wednesday. Fed Chair Jerome Powell recently hinted at potential future rate cuts but emphasized the need for sustained progress in achieving the 2% inflation target.

Attention will also be on the BoE, which is likely to keep rates unchanged at 5.25% on Thursday. Market expectations suggest potential rate cuts starting in August, with further cuts anticipated by year-end.

Today’s US economic calendar includes data on Building Permits and Housing Starts, with the focus primarily on the Fed’s monetary policy meeting and subsequent press conference on Wednesday. The BoE’s interest rate decision on Thursday will also be closely monitored, along with any insights provided by policymakers regarding inflation, economic growth, and labor market conditions.

AUDUSD – RBA Governor’s Speech: Insights on Interest Rate Direction Post-Hold

The RBA kept interest rates at 4.35% unchanged today on Monetary policy meeting, RBA Governor Michelle Bullock said we are still under war against inflation rate, we doing necessary steps for controlling inflation rates, labor market is tightened, we see both sides of the economy, whenever inflation gets cooler we do changes in the monetary policy settings. Now we are going on the right track with our monetary policy settings asper RBA Governor said in the meeting.

AUDUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

RBA Governor Michele Bullock addresses press post March policy hold, highlighting cautious stance and employment focus.

Key points:

– Emphasis on employment data monitoring.

– Balanced outlook risks.

– Inflation battle ongoing.

– Statement language subject to data response.

– Policy risks acknowledged.

– Confidence needed for rate adjustment.

– Flexible policy approach.

– Data responsiveness paramount.

– Uncertain NAIRU range: 4.0-4.5%.

NZDUSD – Faces Selling Pressure Above 0.6050, Watches Fed Rate Decision

The Chine Foreign Minister Wang Yi said They are ready to implement free trade agreement with New Zealand, this news failed to impress the NZ Dollar in the market. Ahead of NZ Q4 GDP data and Consumer survey data, FED Interest rate decision tomorrow, NZ Dollar is waiting for move.

NZDUSD is moving in the Descending triangle pattern and the market has fallen from the lower high area of the pattern

NZD/USD Faces Selling Pressure Amid Stronger US Dollar, Eyes Fed Rate Decision

The NZD/USD pair experiences selling pressure during the early European session on Tuesday, influenced by the uptick in the US Dollar Index (DXY) reaching two-week highs above 103.80. Market sentiment remains cautious ahead of the Federal Reserve’s (Fed) monetary policy meeting scheduled for Wednesday. Currently, the pair trades around 0.6053, down 0.53% for the day.

Recent US economic data suggests a robust economy with elevated inflation, potentially delaying interest rate cuts by the Fed and bolstering the US Dollar broadly. Fed Chairman Jerome Powell remains unconcerned about persistent inflation above the bank’s target, emphasizing the need for sustainable inflation decline before rate adjustments.

Market expectations anticipate the Fed to maintain unchanged interest rates for the fifth consecutive time at the conclusion of its two-day meeting. Powell hints at potential rate cuts later in the year, contingent upon evidence of inflation subsiding to the 2% target. Financial markets reflect a 73% likelihood of rate cuts in July, according to the CME FedWatch Tools.

On the Kiwi front, despite positive remarks from Chinese Foreign Minister Wang Yi regarding collaboration on an upgraded China-New Zealand free trade agreement, the New Zealand Dollar (NZD) fails to rally as a China-proxy.

Looking forward, traders await New Zealand’s Westpac Consumer Survey for Q1 and the Current Account data on Wednesday. The Fed interest rate decision and subsequent press conference will dominate market focus this week. Thursday will bring attention to New Zealand’s Q4 Gross Domestic Product (GDP), expected to grow by 0.1% QoQ.

XTIUSD – Crude Oil Rally Continues: WTI Surpasses $82.00

The Crude Oil prices reached $82.00 after the fears of supplies constraint from OPEC+nations and US side. The US Oil supply constraint shows the increase of cost of Oil Barrels.

Crude Oil price is moving in the Descending triangle pattern and the market has reached the lower high area of the pattern.

WTI Crude Oil Surpasses $82.00, Hits 16-Week High:

West Texas Intermediate (WTI) crude oil surged above $82.00 per barrel on Monday, marking a near-term bullish trend. This climb saw US crude oil reaching its highest prices since November, peaking at $82.46 to commence the new trading week.

Concerns are mounting in energy markets over the continued decline in crude oil supplies in the near future. Despite record oil production levels from non-OPEC countries, particularly the US, the crude oil market is widely anticipated to face medium to long-term supply constraints, driving up barrel prices.

Weekly crude oil stock data from the American Petroleum Institute (API) for the week ending March 15 is set for release on Tuesday, with the last report showing a significant drawdown of -5.5 million barrels. Additionally, the Energy Information Administration (EIA) will release its own crude oil stocks change report on Wednesday, with expectations of a further modest drawdown of 25,000 barrels following the previous week’s decline of -1.5 million barrels.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/