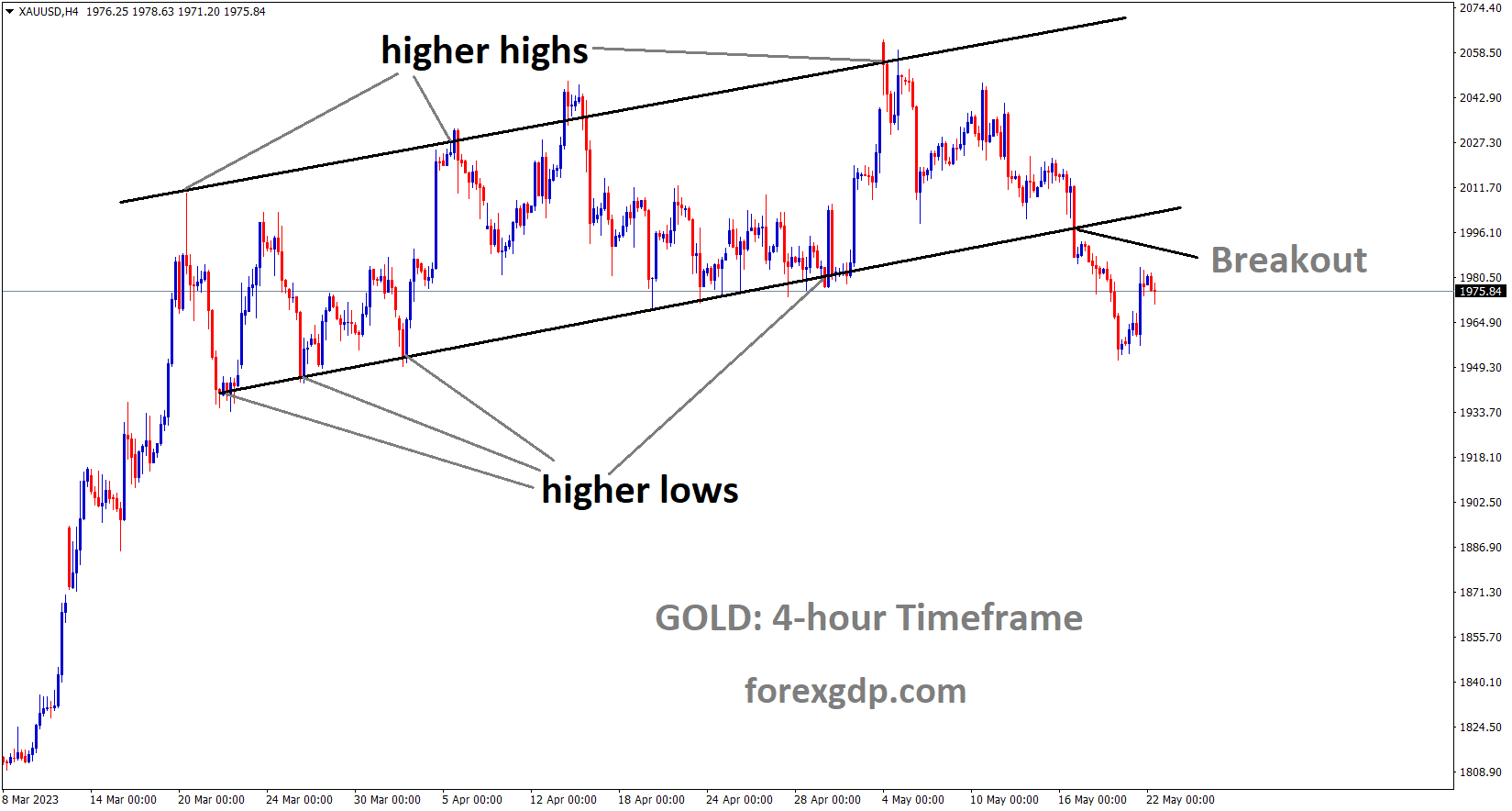

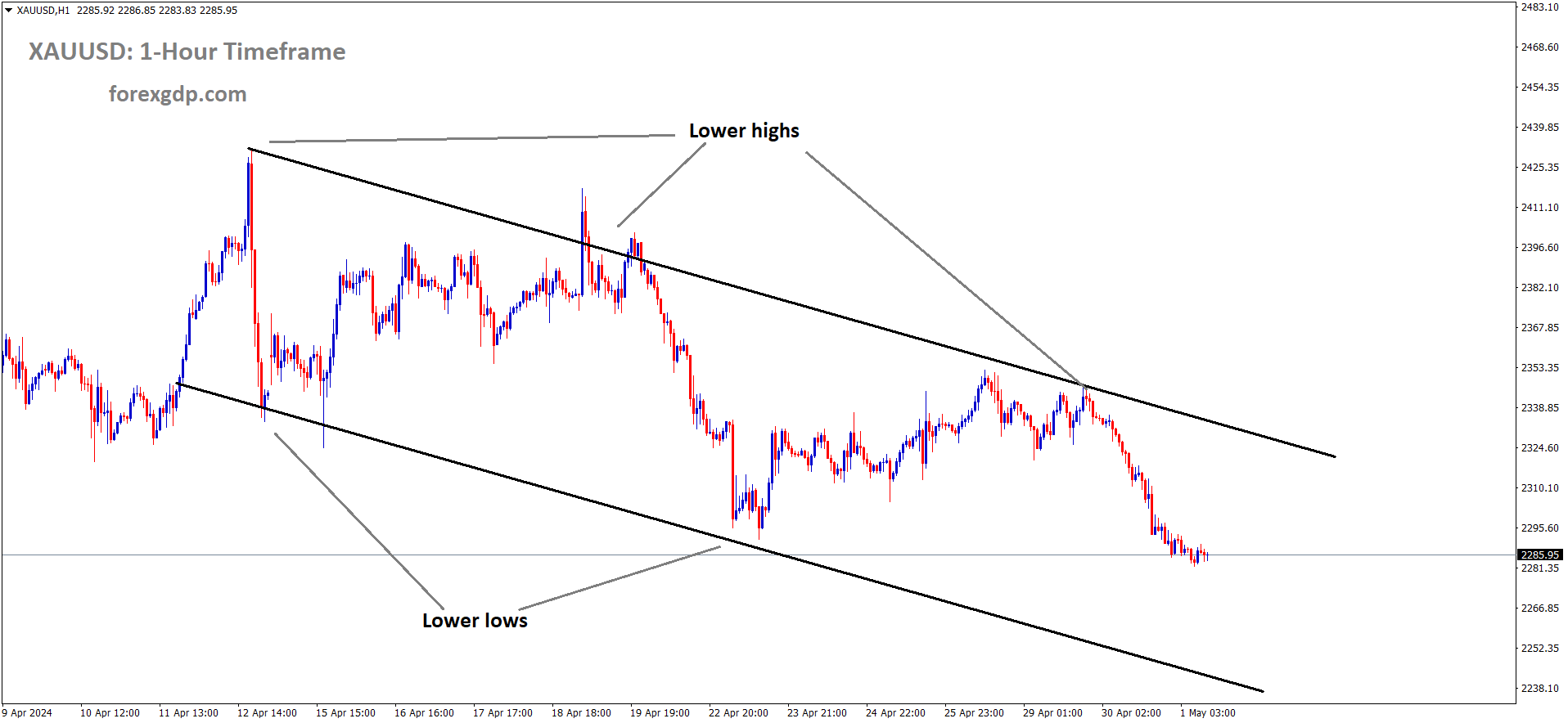

XAUUSD Gold price is moving in the Descending channel and the market has reached the lower low area of the channel

XAUUSD – Gold Price Dips Below $2,300 as US Employment Costs Increase

The gold prices are lifted down after the US Q1 Employment cost index rallied to 1.2% in Q1 and 0.90% printed in last quarter and 1.0% expected in this quarter. Due to Wage rising in the US Market, inflation also moving higher in the near term by consumer spending will be more if salary is increased from the companies. So FED hold or hike the rates this year inorder to control the inflation rates.

The Gold price (XAU/USD) dipped slightly above the $2,300 mark during the US trading session on Tuesday, influenced by an upbeat market sentiment diminishing the appeal of safe-haven assets like Gold. Additionally, US data revealing an uptick in employment costs added pressure on Gold prices, raising concerns about inflation and future interest rate adjustments.

In the Asia-Pacific region, markets generally closed on a positive note, with the Nikkei surging by 1.24%, Australia’s ASX200 rising by 0.35%, and the Hang Seng edging up by 0.1% at the close. Notably, the Caixin Chinese Manufacturing PMI reached a 14-month high in April. In Europe, strong GDP growth figures from France and Spain hinted at a better-than-expected increase in Eurozone Q1 GDP.

The US Dollar (USD), which typically moves inversely to Gold, strengthened following the release of the US Employment Cost Index, which exhibited a 1.2% rise in Q1. This surpassed expectations of a 1.0% increase and the previous quarter’s 0.9% figure. The data underscored persistent inflationary pressures in the US economy, as higher employment costs often translate into increased wages and inflation. Consequently, it might prompt the Federal Reserve (Fed) to postpone interest rate cuts, bolstering the USD due to anticipated longer-term higher interest rates that attract more capital inflows.

The recent rally in Gold prices, particularly in Q1, was attributed to robust central bank purchases and over-the-counter (OTC) buying, according to a report by the World Gold Council (WGC). Total Gold demand during the period amounted to 1,238.3 tonnes, slightly lower than the previous quarter’s 1,269.7 tonnes. OTC buying, estimated at 136.4 tonnes, saw an increase from 126.9 tonnes in Q4. Central banks contributed significantly to the rally, purchasing 289.7 tonnes compared to 219.6 tonnes in the previous quarter.

The WGC report highlighted key insights:

– Gold mine production rose by 4.0% year-on-year (YoY) to 893 tonnes, marking a record first quarter.

– Gold recycling increased by 12% YoY to 351 tonnes, the highest quarter since Q3 of 2020.

– Eastern and Western investors displayed contrasting behaviors, with Eastern markets witnessing strong buying amidst price surges, while Western markets saw profit-taking amid healthy gold purchases.

– Global Gold ETF holdings experienced a decline of 114 tonnes, primarily driven by outflows in Europe and North America.

– Despite the price rally, demand from the jewelry sector remained robust, with global consumption decreasing by only 2.0%.

– Gold demand from the technology sector surged by 10.0% YoY, fueled by the AI boom, leading to increased buying from the tech industry.

EURUSD – De Cos of ECB proposes rate cuts in June if inflation slows

The ECB policy maker Pablo Hernandez de cos said inflation will cool down in this month then we do rate cuts in the June month, ECB is doing cautious approach on monetary policy settings and data dependent approach. Spanish central bank keep its rate at positive stance due to counter cyclical buffers.

EURUSD has broken the ascending channel in downside

During a statement on Tuesday, Pablo Hernandez de Cos, a policymaker at the European Central Bank (ECB), emphasized the necessity for the ECB to commence rate cuts in June should the anticipated deceleration in inflation persist, as reported by Reuters.

De Cos elaborated, stating, “Given the high uncertainty, the ECB will follow a data-dependent approach where decisions are taken at each meeting.” Additionally, he mentioned that the Spanish central bank was contemplating establishing a positive level for banks’ countercyclical buffer.

USDJPY – JPY’s intraday direction uncertain; awaiting Fed’s verdict

The Japanese Yen are weaker against counter pairs, Japan Jibun Bank Manufacturing PMI data came at 49.6 in the April month from 48.2 printed in the March month. This mark reduced the contraction in Manufacturing sector over 8 months history. The Japan Government may be provide the tax benefits to Firms for converting USD to JPY in the profits in order to the stablise the Domestic currency is possible.

USDJPY is moving in an Ascending channel and the market has reached the higher high area of the channel

Japanese Yen (JPY) experienced notable declines against the US Dollar (USD) on Tuesday, erasing gains from potential intervention efforts by Japanese authorities. This reversal was primarily driven by the persisting interest rate gap between Japan and the United States (US), expected to remain significant in the foreseeable future. The USD garnered further strength amid a growing belief that the Federal Reserve (Fed) would maintain higher interest rates for an extended period, supported by ongoing signs of inflationary pressures in the US economy.

However, despite the USD’s strength, the risk-off sentiment prevailing in markets – evident from the decline in US and Asian equities – provided some buoyancy to the safe-haven JPY. This dynamic acted as a restraining force on the USD/JPY pair ahead of the crucial Federal Open Market Committee (FOMC) policy decision scheduled for later in the day.

In the Japanese economic landscape, the Bank of Japan’s (BoJ) cautious approach toward policy tightening and the uncertain rate outlook also weighed on the JPY. Moreover, reports indicating potential tax breaks for companies converting foreign profits into JPY failed to significantly uplift bullish sentiment or provide meaningful momentum to the USD/JPY pair, especially against the backdrop of a robust US Dollar.

On the data front, Japan’s Manufacturing PMI for April, finalized at 49.6, signaled a slower contraction compared to the previous month, yet failed to stimulate notable JPY recovery. Conversely, in the US, stronger-than-expected labor cost increases in the first quarter, alongside persistently high inflation as reflected in the Personal Consumption Expenditures (PCE) Price Index, reaffirmed market expectations of a delayed rate-cutting cycle by the Fed.

Looking ahead, market focus remains on the outcome of the FOMC policy decision, expected to impact the USD’s trajectory and offer fresh direction to the USD/JPY pair. Traders are also eyeing key US macroeconomic releases, including the ADP report on private-sector employment, JOLTS Job Openings, and ISM Manufacturing PMI, for further cues.

USDCAD – Climbs Over 1.3700 on Robust US Q1 Employment Cost Index, Soft Canadian GDP

The Canadian Dollar moved down against counter pairs after the Canadian GDP data came at 0.20%decline in the February month from 0.30% expected, 0.50% printed in the last month. The BoC have the chances to rate cuts in this year due to slowdown in the economy reveals from the data.

USDCAD has broken the Descending channel in upside

The USD/CAD pair has surpassed the significant resistance level of 1.3700 during the early American trading session on Tuesday. This rise is attributed to the strengthening of the US Dollar, propelled by robust Q1 Employment Cost Index data reported by the United States Bureau of Labor Statistics (BLS).

According to the BLS, the Labor Cost Index surged by 1.2%, surpassing market expectations of 1.0% and the previous reading of 0.9%. This notable increase indicates substantial wage growth, likely leading to heightened household spending, thereby reinforcing concerns about persistent inflationary pressures. Consequently, it is anticipated that the Federal Reserve (Fed) will maintain its current interest rate stance during its monetary policy announcement scheduled for Wednesday, with rates expected to remain within the range of 5.25%-5.50%.

Furthermore, the weak performance of the Canadian Dollar has also contributed to the upward pressure on the USD/CAD pair. This weakness is evidenced by the monthly Canadian Gross Domestic Product (GDP) report, which revealed a growth rate of 0.2%, falling short of both market expectations of 0.3% and the previous reading of 0.5%. This subdued growth underscores the potential impact of the Bank of Canada’s (BoC) recent interest rate hikes. Consequently, there is speculation that the BoC may contemplate earlier interest rate cuts in response to sluggish growth and diminishing inflationary pressures, with market participants eyeing the upcoming June meeting for potential policy shifts.

USDCHF – climbs above 0.9200 in overbought state

The FOMC meeting is scheduled today and is expected to hold the rates at 5.25%-5.50% is widely expected. The US Dollar playing higher against Swiss Franc after the Geopolitical tensions are calm down by Israel- Hamas ceasefire talks. Fears down in the market makes positive for USD and Negative for Swiss Franc.

USDCHF is moving in an Ascending channel and the market has reached the higher high area of the channel

During the early European session on Wednesday, the USD/CHF pair continues its upward movement, reaching 0.9210. This surge is primarily driven by renewed demand for the US Dollar (USD), which acts as a major catalyst for the pair. Additionally, market sentiment is influenced by the anticipation that the Federal Reserve (Fed) will maintain its current policy rate range of 5.25%–5.50% during its upcoming meeting. The Fed’s expected continuation of a hawkish stance further bolsters the USD.

From a technical perspective, the bullish trajectory of USD/CHF remains intact on the four-hour chart. The pair is positioned above the crucial 50- and 100-period Exponential Moving Averages (EMAs), indicating a bullish trend. Moreover, the Relative Strength Index (RSI) is situated in the bullish zone above the midline. However, it’s worth noting that the RSI is currently in the overbought territory, suggesting the possibility of some consolidation before any significant further appreciation in the USD/CHF pair in the near term.

USD INDEX – US Consumer Confidence Drops to 97.0 in April

The US Consumer confidence for the month of April came at 97.0 from 103.1 printed in the March month. This reading remarks lowest since 2022,Current Business and Labour market conditions are decreased to 142.9 in April month from 146.8 in the March month. 12 month inflation expecatations remained at 5.3%.

USD Index is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

In April, consumer sentiment in the United States took a hit, as reflected by the latest data from the Conference Board’s Consumer Confidence Index, which fell to 97.0. This marks the lowest reading since July 2022, down from the revised figure of 103.1 (initially reported as 104.7) recorded in March.

According to the Conference Board’s press release, the Present Situation Index, which measures consumers’ assessment of current business and labor market conditions, decreased to 142.9 in April from a revised 146.8 in March.

Moreover, the Expectations Index, which gauges consumers’ outlook for the future, declined to 66.4 from the previous month’s 74.0. Despite these declines, the 12-month inflation expectation remained steady at 5.3%.

GBPUSD – Sterling Pressured Ahead of Fed Policy Decision

The GBP is moving down against USD, BoE Governor Andrew Bailey said there will be June month rate cut due to inflation level is cooling down in the April month. BoE Deputy governor Dave Ramesdan also said inflation is stopped from rising levels and reached our Goal 2% in the next month.

GBPUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

The Pound Sterling (GBP) slightly retreats from its recent peak of 1.2570 against the US Dollar (USD), hovering above the key support level of 1.2500 in the early American trading session on Tuesday. The GBP/USD pair faces downward pressure as market participants await the upcoming monetary policy announcement from the US Federal Reserve (Fed) on Wednesday, seeking fresh insights into the central bank’s stance.

Amid a data-heavy schedule in the United States, the US Dollar remains on edge. Meanwhile, economic events in the United Kingdom are relatively sparse. Therefore, speculation surrounding the Bank of England’s (BoE) interest rate decision, scheduled for May 9, will guide the Pound Sterling’s trajectory. While the BoE is expected to maintain the status quo, the central bank’s guidance on interest rates is anticipated to lean slightly towards a dovish stance.

BoE Governor Andrew Bailey has expressed confidence in a significant decline in April’s headline inflation and views market expectations for two or three rate cuts this year as reasonable. Additionally, BoE Deputy Governor Dave Ramsden has suggested that the risks of persistent inflation have diminished. The BoE may provide further clarity on the timeline for potential interest rate reductions, with market sentiment split between the June or August meetings as potential pivot points for rate cuts.

In the currency markets, the Pound Sterling faces resistance near the immediate level of 1.2560 against the US Dollar. Meanwhile, the US Dollar gains strength following robust Q1 Employment Cost index data, which exceeded expectations, suggesting accelerated wage growth and potential inflationary pressures.

Looking ahead, investors are closely monitoring the Federal Reserve’s interest rate decision, scheduled for Wednesday. Expectations lean towards the Fed maintaining a hawkish stance, with policymakers likely to hold interest rates steady within the range of 5.25%-5.50%. Persistently higher inflation, driven by robust consumer spending and tight labor market conditions, could support the Fed’s argument for maintaining higher interest rates until sufficient evidence of sustained inflationary trends emerges.

Ahead of the Fed’s decision, market participants are eyeing key economic indicators such as the ADP Employment Change and the ISM Manufacturing Purchasing Managers Index (PMI) data for April. Additionally, the upcoming Nonfarm Payrolls (NFP) report for April, scheduled for release later in the week, will also influence US Dollar dynamics.

AUDUSD – AUD advances ahead of Fed rate call

The Australian industry index came at 3.6 points down to -8.9 in the April month from -5.6 in the march month. This is contraction trend of past two years in the industry index since rate hikes from RBA side. ANZ analysts expected RBA to cut the rates in the November month is possible.

AUDUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

AUD gains ground as market sentiment improves, despite pressure from AiG Industry Index data indicating a contraction in Australian private business activity. The Reserve Bank of Australia (RBA) is expected to maintain its current interest rate of 4.35% at its upcoming meeting.

The Australian Dollar faced setbacks following lower-than-expected Aussie Retail Sales data, potentially impacting the RBA’s hawkish stance on interest rates. However, stronger-than-expected domestic inflation data last week has raised expectations of a delay in interest rate cuts.

The US Dollar Index (DXY) continues its rally ahead of the US Federal Reserve (Fed) policy meeting, supported by higher-than-expected Employment Cost Index data and hawkish remarks from Fed officials suggesting no immediate rate cuts. Traders await US economic indicators such as ADP Employment Change and ISM Manufacturing PMI for further insights into the US economy.

The AiG Australian Industry Index decreased to -8.9 points in April, reflecting continued contractionary trends. The ASX 200 opened lower on Wednesday following robust US employment data. ANZ predicts the RBA may start reducing interest rates in November, while Commonwealth Bank revises its forecast for the first interest rate cut to November.

In the US, the Employment Cost Index surged by 1.2% in the first quarter, exceeding expectations and highlighting wage pressures. Australian Retail Sales experienced a decline in March. The likelihood of the Fed maintaining interest rates at current levels during the June meeting has increased, according to the CME FedWatch Tool.

Fed Chair Jerome Powell suggested a longer timeline to address inflation concerns, while Fed Governor Michelle Bowman and Minneapolis Fed President Neel Kashkari hinted at potential inflation risks and no rate cuts this year, respectively.

NZDUSD – RBNZ’s Hawkesby: Global inflation poses financial stability risk

The RBNZ Deputy Governor Christian Hawkesby said employment trend is cooling down after the RBNZ rate hikes are done, inflation is still in higher levels due to Global uncertainty.

NZDUSD is moving in the Symmetrical triangle pattern and the market has reached the higher low area of the pattern

During his remarks on Wednesday, Christian Hawkesby, the Deputy Governor of the Reserve Bank of New Zealand (RBNZ), emphasized that the recent uptick in interest rates signifies a potential slowdown in the job market. He highlighted that the persistence of elevated global inflation continues to pose a significant risk to financial stability.

Hawkesby’s statements included the following key points:

– The employment data reaffirms the anticipated trend.

– The implementation of higher interest rates is anticipated to temper the vigor of the labor market.

– Despite other factors, such as ongoing monetary policies, the prevailing high global inflation rate remains a critical concern for maintaining financial stability.

CRUDE OIL – WTI pressured below $81.00 due to unexpected oil stockpile build

The US Crudeoil inventories rose by 4.906 million barrels for week ending April 26 and 3.23 million barrels drawback in the last week, 1.5 million Barrels shortage is expected in this week. Oil stocks piled up makes Oil prices to slowdown against USD in the market.

XTIUSD Crude oil Price is moving in an Ascending channel and the market has reached the higher low area of the channel

WTI, the US crude oil benchmark, is currently trading around $80.80. Its value is declining due to a surprising increase in crude inventories in the United States. This unexpected build in stockpiles contrasts with previous expectations of a decrease.

Additionally, tensions in the Middle East seem to be easing, contributing to the downward pressure on oil prices. However, concerns about potential supply disruptions persist, keeping the market on edge.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!