USDJPY is moving in the Descending channel and the market has reached the lower high area of the channel

USDJPY – BoJ’s Ueda: No Forex Rate Control in Monetary Policy

The BoJ Governor Ueda said in Parliament on Yesterday, Potential need for Policy changes in the economy, FX impact on our Yen prices and We must control by Policy settings. I am Focusing on inflation trend not on Yen price to control. Yen prices are impacted by huge Volatility by speculators and central bank interest rates divergence. We will not wait for 1.5-2 years for inflation to come to our target and then rise the rates. The Positive Wage cycle pushes the inflation cycle to higher in the economy. We are closely monitor the Yen Fluctuations in the economy. The Yen moved in Positive side after the Speech of Ueda on Parliament.

Bank of Japan (BoJ) Governor Kazuo Ueda addressed the Japanese parliament on Tuesday, expressing concern about the potential implications of foreign exchange movements and indicating readiness to take policy measures if necessary. He emphasized that the primary goal of monetary policy is to influence inflation rather than directly control the value of the yen. Ueda underscored the importance of monitoring the impact of yen fluctuations on the economy and prices, noting that such volatility could have a significant effect. He clarified that the BoJ does not intend to manage FX rates through monetary policy but recognizes the role of currency movements among various factors affecting the economy. Ueda highlighted the adverse effects of a weak yen, including increased import costs and potential impacts on demand. He affirmed the BoJ’s commitment to adjusting easing measures in response to changes in the inflationary trend, aiming for a gradual increase in trend inflation towards the target of 2%. However, he acknowledged the possibility of yen movements exerting a more substantial influence on inflation in the future. Ueda stated that the BoJ may not wait until inflation reaches the forecasted levels within the next 1.5 to 2 years before considering adjustments to interest rates, indicating a willingness to respond preemptively to evolving economic conditions. He also noted the strengthening of inflationary pressure driven by a positive wage-price cycle.

XAUUSD – Gold price shows slight upward trend despite stronger US Dollar

The Gold prices are trading flat in this week, China reported 60,000 troy ounces of Gold purchased in the April month due to fears of Stock market down and real estate down in the chinese economy. Another side Israel rejected the Hamas deal and expected more demands from Hamas by Israel, So invasion of Gaza is not stopped. FED Members staying positive on US Dollar due to inflation level might not come to target this year, So rate cuts applications will harm the US economy in the current situation.

XAUUSD Gold price is moving in the Descending channel and the market has reached the lower high area of the channel

XAUUSD Gold price is moving in the Descending channel and the market has reached the lower high area of the channel

Gold price (XAU/USD) is experiencing a slight uptick in Asian trading today. This uptrend is attributed to safe-haven demand amid geopolitical tensions and ongoing central bank purchases. However, hawkish comments from Federal Reserve (Fed) officials may dampen hopes for interest rate cuts in 2024, despite weaker-than-expected US employment reports in April, potentially dragging gold lower.

Later today, Fed policymakers Philip Jefferson, Susan Collins, and Lisa Cook are scheduled to speak. Their hawkish remarks could boost the Greenback and weigh on USD-denominated gold. Gold traders will closely watch the consumer sentiment reading from the University of Michigan on Friday.

In related news, Minneapolis Fed Bank President Neel Kashkari stated on Tuesday that it’s premature to declare inflation has stalled, hinting at potential interest rate cuts if price pressures ease. Meanwhile, Richmond Fed President Thomas Barkin believes current interest rates are restrictive enough to cool the economy and bring inflation back to the 2% target.

Financial markets are currently pricing in nearly 50 basis points (bps) of rate cuts from the Fed this year, with a 65.7% likelihood of a 25 bps rate cut in September, according to CME’s FedWatch Tool. Additionally, the preliminary University of Michigan Consumer Sentiment Index, expected to decline from 77.2 in April to 76.0 in May, will be released on Friday.

In other developments, Israeli troops launched strikes on Gaza’s southernmost city, despite Hamas agreeing to a ceasefire proposal on Monday, citing conditions that did not meet its demands, as reported by the New York Times. Additionally, the People’s Bank of China (PBoC) added 60,000 troy ounces of gold to its reserves in April, marking 18 consecutive months of purchases.

EURUSD – Euro Zone Bond Yields Drop on Rate Cut Expectations

The Euro zone bond Yields are lowered in the Fourth Straight month after the hopes of interest rate cuts in the June month. The Euro policy makers have confident on June month rate cuts due to Euro zone faced 0.30% growth in Q1 2024 GDP data and 2.4% grew of Inflation rate in the March month.

EURUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

In the euro zone, bond yields witnessed a decline for the fourth consecutive session on Tuesday, as investors heightened their expectations for potential rate cuts from both the Federal Reserve and the European Central Bank (ECB) within the year. This shift in sentiment followed the release of disappointing U.S. jobs data on Friday.

Germany’s 10-year bond yield, serving as the benchmark for the euro zone, dropped by 4 basis points (bps) to 2.438%, touching its lowest level since April 18 at 2.431%. Notably, bond yields move inversely to prices.

The latest nonfarm payrolls report revealed that the U.S. labor market added 175,000 jobs in April, a significant decrease from the 315,000 jobs added in March and well below economists’ expectations of a 243,000 increase.

In response to this data, investors adjusted their positions to reflect the likelihood of two interest rate cuts by the Federal Reserve this year. This adjustment in expectations also bolstered speculations that the ECB could potentially lower rates three times, with the first cut anticipated as early as June.

Previously, a series of robust economic indicators in the United States had led investors to anticipate only one rate cut by the Federal Reserve this year, a notable reduction from around seven expected at the beginning of 2024. Given the substantial influence of the U.S. economy, this shift in expectations also impacted projections for other major central banks.

Christoph Rieger, head of rates and credit research at Commerzbank, commented on the prevailing sentiment, noting that minimal obstacles exist in the way of a gradual decline in yields. He attributed this trend to the thin data calendar, which is unlikely to alter the perception that the U.S. economy is gradually losing momentum.

Germany’s two-year bond yield, known for its sensitivity to ECB rate expectations, experienced a decline of 1 bp to 2.904%.

Meanwhile, recent data revealed that German exports rebounded in March, supported by robust demand from the United States and China. However, a disappointing performance in industrial orders for the month indicated lingering weaknesses in the economy.

ECB policymakers indicated on Monday that they were growing increasingly confident about the prospect of implementing interest rate cuts, especially as the economy displayed signs of modest growth and inflation remained manageable.

Recent GDP figures demonstrated a 0.3% growth in the euro zone economy during the first quarter, marking a recovery from a slight recession. Additionally, euro zone inflation decreased to 2.4% in April.

Italy’s 10-year yield witnessed a decline of 4 bps to 3.768%, while the spread between Italian and German bond yields widened by 1 bp to 132 bps.

USDCAD – Canada’s Ivey PMI Indicates April Acceleration

The Canada IVEY PMI Data for themonth of April came at 63.0 versus 57.5 printed in the March month. The Canada employment and inflation shows improvement in the recent months. The BoC May have chances to rate cut delays in the upcoming months due to data shows in improvement zone.

USDCAD is moving in the Descending channel and the market has reached the lower high area of the channel

According to the latest data from the Ivey Purchasing Managers Index (PMI) released on Tuesday, economic activity in Canada experienced a notable acceleration in April, with indicators for employment and inflationary pressures registering gains.

The seasonally adjusted index surged to 63.0 in April, up from 57.5 in March. A value above 50 signifies an expansion in economic activity. The Ivey PMI functions as a measure of the month-to-month fluctuations in economic activity, derived from insights provided by a panel of purchasing managers located across Canada.

In terms of specific components, the employment gauge saw a rise to a seasonally adjusted 56.4, climbing from 55.4 in March. Additionally, the prices index recorded a notable increase to 62.4, marking its highest level since December, compared to 57.9 in the previous month.

Furthermore, the unadjusted PMI, which is not adjusted for seasonal variations, exhibited a rise to 65.7 from 63.0, reflecting a robust expansion in economic activity.

The Swiss Bank UBS reported $1.8 Billion profit in the First quarter after the lower estimate of analysts side, it shows stunning profits for the UBS Bank after the Credit Suisse take over. The Main reason for this profit is Employee reduction and continue this employees reduction process till the end of 2024. Too Big Too Fail concept from Swiss Government also reducing the rewards to Share holder of UBS.

USDCHF is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

UBS stunned investors with its impressive performance in the first quarter, reporting a profit of $1.8 billion on Tuesday. The bank also reassured shareholders by affirming its commitment to share buybacks, alleviating concerns surrounding Swiss plans to increase capital requirements.

Following the announcement, shares in Switzerland’s largest bank surged by as much as 10%, marking their most significant one-day gain since March 2023, when authorities orchestrated the rescue of Credit Suisse. Since acquiring Credit Suisse, UBS has witnessed its shares appreciate by over 50%, with investors optimistic about the combined entity’s prospects, given its low acquisition costs, substantial increase in assets, and relatively smooth integration process thus far.

UBS’s net income nearly tripled analyst forecasts, driven by cost-cutting measures and a boost from non-core aspects of the business inherited from Credit Suisse, which UBS aims to divest. CEO Sergio Ermotti attributed the strong performance to the robustness of the bank’s client franchises and progress in integration efforts.

Despite the positive momentum, UBS faces significant challenges in the integration process, including the consolidation of IT systems, client migration from Credit Suisse, and workforce reduction, with planned job cuts expected to commence towards the end of 2024 and continue through 2026.

Moreover, heightened regulatory and political scrutiny looms over UBS, as Switzerland seeks to enhance protections against systemic risks posed by banks deemed “too big to fail.” The Swiss government’s proposal to raise capital requirements for such banks has raised concerns about its potential impact on UBS’s ability to reward shareholders. However, Ermotti reaffirmed UBS’s commitment to share buybacks and dividend increases for the years 2024 to 2026.

Record buybacks and dividends have contributed to a rally in banking shares across Europe, with UBS bolstering its regulatory reserves by approximately $20 billion, regardless of the Swiss government’s plans. Analysts anticipate UBS to accelerate the winding down of legacy Credit Suisse trading positions, releasing substantial capital to meet potential regulatory capital increases.

In terms of business performance, UBS reported strong pre-provision profits in core operations, with wealth management attracting $27 billion in net new assets. However, asset management and investment banking revenues fell short of expectations.

UBS remains committed to cost-saving initiatives, achieving an additional $1 billion in gross cost savings in the first quarter, bringing total savings since the merger to $5 billion. The completion of the merger between the main parent companies is expected by the end of May, with the consolidation of their Swiss branches slated for the third quarter.

USD Index – Wells Fargo Predicts Dollar’s Reserve Currency Status Endurance

The Wells Fargo company predicted the US Dollar remained the dominance in the world market for transactions. US Seized $300 Billion worth of Russian Assets and now it is transferring to Ukraine for War aids. Russia Putin said US Citizens in the Russia may face US assets Freeze in the Russia, this is tit for tat communication happened between Two Giant country leaders. So US Dollar maintain as Dominant market against all currencies in the world.

USD INDEX is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

Recent actions by U.S. authorities to seize Russian assets could potentially contribute to ongoing efforts to diversify away from the dollar. However, despite these developments, Wells Fargo maintains that the greenback is likely to retain its position as the global reserve currency in the foreseeable future.

The prohibition of transactions with Russia’s central bank and finance ministry, along with the blocking of approximately $300 billion of sovereign Russian assets in Western countries, was a response to Russia’s invasion of Ukraine. Furthermore, the U.S. House of Representatives passed a bill allowing the confiscation of these Russian assets held in American banks, potentially transferring them to Ukraine. This move could trigger retaliatory measures from Russia, such as seizing the assets of U.S. citizens, including property and cash.

While such actions may have limited implications for the dollar’s reserve currency status, they could draw attention from China, given its significant exposure to the U.S. dollar. Concerns about the U.S. fiscal outlook and the frequent use of economic sanctions by Washington have already raised doubts about the dollar’s role as a global reserve currency in some quarters. The possibility of asset confiscation could further reinforce these concerns.

Despite efforts to diminish the dollar’s importance, such as bilateral clearing arrangements between countries like Brazil and China, as well as willingness among energy-exporting nations in the Middle East to accept renminbi as payment, Wells Fargo believes these moves are insufficient to significantly reduce dollar dominance. Factors such as the depth and liquidity of U.S. debt markets, as well as concerns about other currencies like the euro and the renminbi, contribute to the dollar’s enduring status.

For a currency to be considered a reserve currency, it must possess certain characteristics, including being freely convertible, widely accepted in trade and global transactions, and backed by large and liquid debt markets. The U.S. dollar meets these criteria, and Wells Fargo sees limited alternatives for foreign exchange reserve managers to allocate currency holdings away from U.S. government bonds. Therefore, the bank believes the dollar’s status as the global reserve currency will remain secure in the foreseeable future.

Morgan Stanley shares a similar view, noting that the dollar’s influence in the global economy remains strong across various economic and financial metrics. While China’s currency, the yuan, may see a modest increase in international usage, challenges such as debt, deflation, and demographics are expected to limit its appeal. Consequently, both Wells Fargo and Morgan Stanley anticipate only a gradual decline in the dollar’s international role, with the greenback maintaining its predominant position for the foreseeable future.

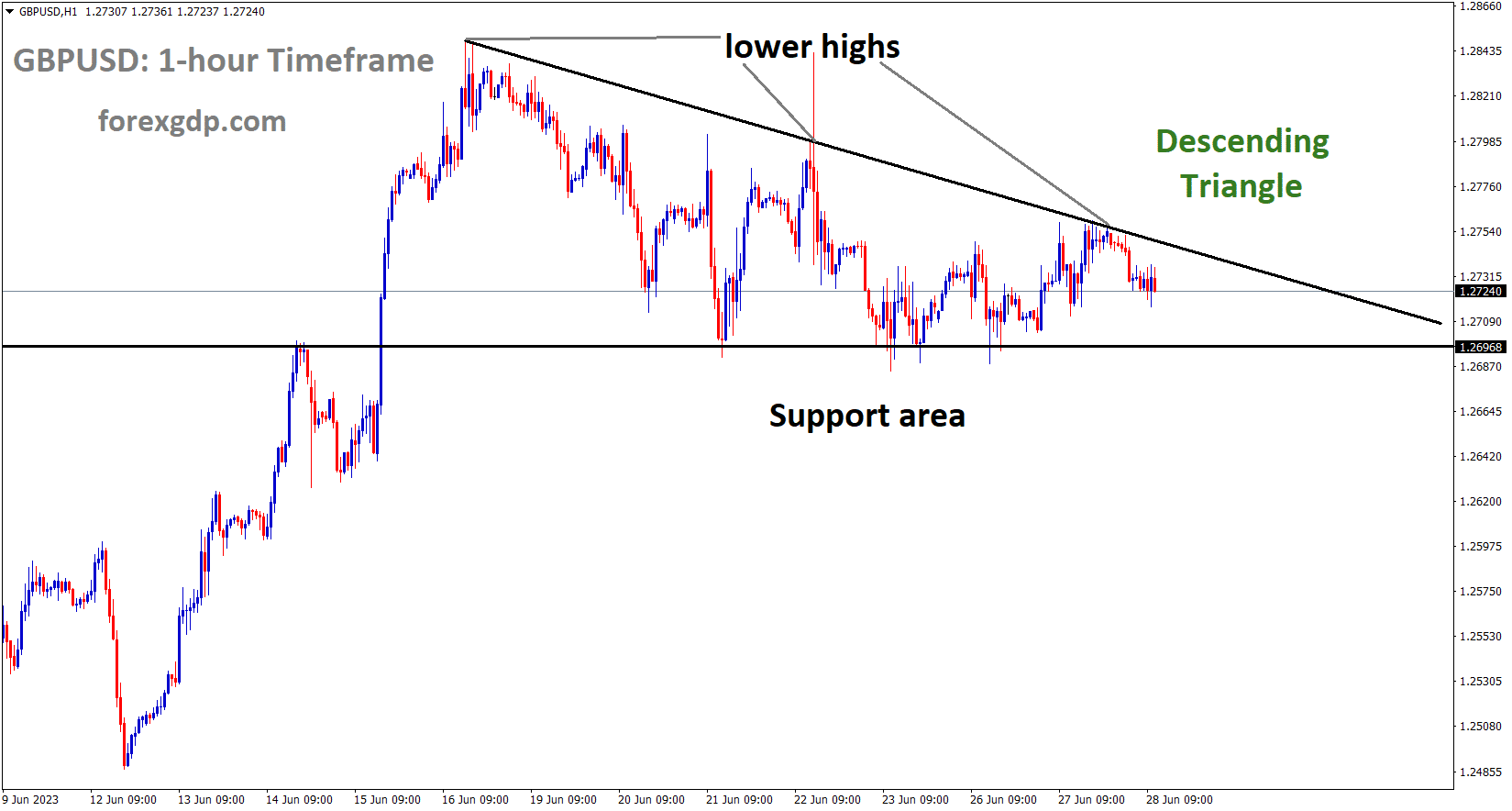

GBPUSD – GBP Falls as Market Eyes Bank of England

The Bank of England is expected to keep the rates at 5.25% Tomorrow, inflation in the March month came at 3.2% it is well above 2% target level. UK Industrial sector reading is weakness and Services sector shows weakness in the market. So August or September month have the chances to rate cuts in the England is possible.

GBPUSD has broken the Ascending channel in downside

On Tuesday, the British Pound experienced a partial reversal against the United States Dollar, following a return to normal trading activity in local markets after a holiday on Monday. As a result, Sterling cross rates are anticipated to exhibit a slight drift leading into Thursday’s session, which marks the Bank of England’s May monetary policy announcement.

Expectations suggest that interest rates will remain unchanged this month, with the pivotal Bank Rate forecasted to hold steady at 5.25%. Consequently, market attention will focus on the voting distribution among the nine-member Monetary Policy Committee (MPC) influencing the decision, alongside its accompanying analysis. Historically, the BoE has occasionally demonstrated a three-way split in voting preferences, encompassing rate hikes, cuts, and maintaining the status quo.

However, the upcoming announcement is likely to feature at most a two-way split, with no members advocating for rate hikes. Despite inflation in the United Kingdom surpassing the BoE’s government-set 2% target, it is showing a downward trajectory. The most recent data, from March, indicated inflation at 3.2%, marking a significant decrease over two years. The current monetary tightening measures, albeit gradual, appear to be effective, and further constraints on monetary policy could prove detrimental to the UK’s sluggish economy.

Presently, futures markets indicate the possibility of the first UK rate cut occurring in September, coinciding with expectations for a similar move by the US Federal Reserve. However, these forecasts are highly contingent on incoming data. Recent disappointing US labor figures have accelerated expectations for Fed action, with prior estimations suggesting a November adjustment.

Amidst these factors, the British Pound is expected to maintain its current trading range leading up to the monetary policy decision, potentially encountering challenges in advancing if the BoE sustains existing expectations regarding rate cuts.

AUDUSD – RBA No Rate Hikes Planned, Aussie Dollar Weakens

The RBA Left interest rate unchanged in the monetary policy settings makes Australian Dollar weakness in the market against counter pairs. The Inflation rate will come to 2-3% target in 2025.

Until rate cuts or hikes is not possible and mostly data dependent approach.

AUDUSD is moving in the Box pattern and the market has fallen from the resistance area of the pattern

The Reserve Bank of Australia (RBA) opted to maintain the cash rate at 4.35%, marking the sixth consecutive meeting without a change. The RBA’s statement highlighted persistent concerns regarding inflation, noting that although inflation remained elevated, its decline was slower than anticipated. This was attributed largely to sustained upward pressure on underlying inflation, particularly stemming from services.

RBA Governor Bullock underscored the risks of inflation, emphasizing a bias towards upward pressure. She openly discussed the prospect of raising interest rates, expressing a hope that the economy would not need to endure such increases.

During the meeting, there was deliberation on the possibility of rate hikes. However, the Board ultimately concluded that existing monetary policy measures were sufficiently restrictive to guide inflation back within the 2-3% target range by late 2025. While Bullock acknowledged that a rate hike remained plausible, she suggested it was currently unnecessary.

Market expectations seemed to anticipate a more hawkish stance regarding potential rate hikes, leading to a decline in the Australian dollar, dropping by as much as 0.5% following the RBA announcement.

In contrast, the Federal Reserve in the United States has signaled a reluctance to consider rate cuts at present, citing ongoing concerns about inflation. Richmond Fed President Barkin characterized first-quarter inflation data as “disappointing” but expressed optimism that the current policy stance would temper demand and facilitate a return to the 2% target. Similarly, New York Fed President Williams described current policy as “in a very good place,” indicating that any decision to cut rates would hinge on forthcoming data.

NZDUSD – NZ Dollar Weakens Due to Strong Greenback

The NZ Dollar moved down after the FED President Neel kashkari said FED will keep the Borrowing costs at higher until the inflation has to come down. The RBNZ delay rate cuts until 2025 the inflation rate has to come down.

NZDUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

The New Zealand dollar experienced a decline to approximately $0.59, influenced by the strengthening of the US dollar following hawkish remarks from Minneapolis Fed President Kashkari.

On Tuesday, Kashkari articulated that the persistently sluggish inflation trajectory implies that the Federal Reserve will likely maintain current borrowing costs for an extended duration, possibly throughout the year.

Market participants are eagerly awaiting updated guidance from Federal Reserve officials later this week to gain further insight into the potential timeline for any adjustments to interest rates.

On the domestic front, the Reserve Bank of New Zealand (RBNZ) signaled a deliberate approach towards delaying any shifts towards monetary easing until 2025, citing persistent inflationary pressures observed in the first quarter.

However, market sentiment indicates full anticipation of a rate cut by October, particularly in light of recent underwhelming employment data.

CRUDE OIL – Oil Prices Steady Amid U.S. Reserve Refill, Gaza Cease-fire Uncertainty

The Crudeoil prices are moving in the flat after the US energy reserves announced 300 million barrels per day is decreased every day from strategic reserves and we will survive if any uncertain conditions came. OPEC+ announced 4 million Barrels perday going to reserves for uncertainity conditions. So Oil prices did not move in Volatility in the market due to strategic reserves followed by OPEC+ and US Side.

XTIUSD Oil price is moving in an Ascending channel and the market has reached the higher low area of the channel

The situation in the Middle East and oil markets has been somewhat uncertain lately. Crude oil futures experienced minimal change on Tuesday amidst developments such as the U.S. decision to replenish the strategic petroleum reserve and ongoing uncertainty regarding a potential cease-fire in Gaza.

The U.S. Energy Department initiated a bid for the purchase of 3.3 million barrels to bolster the strategic petroleum reserve, initially driving oil prices higher before they ultimately closed lower. Global oil inventories have been dwindling by 300,000 barrels per day in 2024, partly due to OPEC+ adhering to production cuts.

Despite these trends, significant uncertainty persists regarding developments in the Middle East, which could potentially lead to a sharp increase in oil prices. Israeli Prime Minister Benjamin Netanyahu expressed skepticism about a cease-fire proposal accepted by Hamas, further complicating the situation.

Although oil prices have reacted to geopolitical risks in the region in the past, no major disruptions to supplies have occurred. OPEC+ currently holds 4 million barrels per day of spare capacity, which could mitigate short-term supply disruptions.

The possibility of a cease-fire in the ongoing conflict in Gaza remains uncertain, with cease-fire negotiations ongoing in Cairo. However, achieving a truce continues to be challenging, and risks to oil supply remain, particularly concerning Houthi militant attacks on shipping in the Red Sea.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!