BEML: BEML Soars with Strong Q4 Net Profit Growth; Stock Surges 130% in 12 Months

BEML Shows Q4 Robust results as 62.9% percent up in the Net profit and Revenue increased to 9% as Rs.1513.7 Cr and EBITA Soared by 29.2% to Rs.370.4 cr. Margins improved to 24.5% from 20.7% YoY.

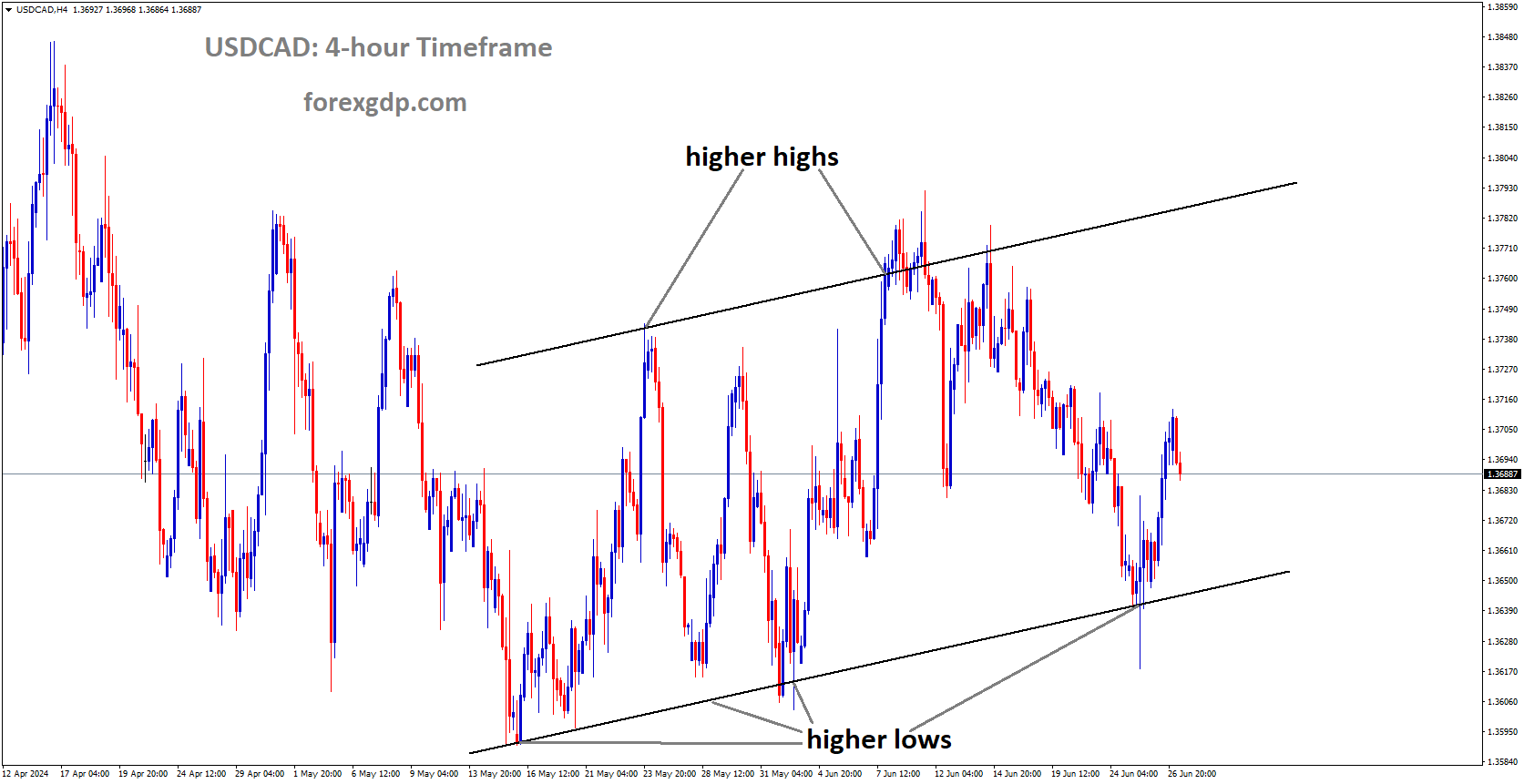

BEML Market price is moving in Ascending channel and market has rebounded from the higher low area of the channel

BEML Ltd’s shares witnessed a surge of over 2 percent on May 13, buoyed by the company’s impressive financial performance in the fourth quarter of the fiscal year ending March 2024. The company reported a remarkable 62.9 percent year-on-year growth in consolidated net profit, reaching Rs 256.8 crore for the quarter, driven by robust operating metrics. Additionally, its revenue from operations saw a 9 percent year-on-year increase, totaling Rs 1,513.7 crore.

Notably, BEML’s EBITDA soared by 29.2 percent to Rs 370.4 crore, accompanied by a substantial improvement in margins from 20.7 percent to 24.5 percent year-on-year.

BEML, a public sector undertaking operating under the Ministry of Defence, caters to various sectors including defence, power, and infrastructure. The company specializes in manufacturing a diverse range of heavy equipment utilized in earthmoving, railways, transportation, and mining.

![]()

For the full fiscal year 2023-24, BEML witnessed a significant surge in net profit, which rose by 78.46 percent year-on-year to Rs 281.77 crore, compared to Rs 157.89 crore recorded in the previous fiscal year. Sales for the fiscal year increased by 3.98 percent year-on-year, reaching Rs 4,054.32 crore compared to Rs 3,898.95 crore in the preceding year.

The company’s board also proposed a final dividend of Rs 15.5 per equity share. As of 9:23 am, BEML shares were trading 1.5 percent higher at Rs 3,258.45 apiece on the National Stock Exchange (NSE).

Over the last six months, BEML’s stock has witnessed a substantial climb of around 48 percent. Year-to-date, BEML’s share price has surged over 14 percent, surpassing the benchmark Nifty 50 index, which has seen a modest increase of around 1.5 percent during the same period.

Remarkably, over the past year, BEML shares have generated significant returns of 130 percent, providing investors with substantial gains.

Bank of Baroda: Brokerages Bullish on Bank of Baroda After Solid Q4 Performance

The Bank of Baroda reported 2.3% increased in the Net Interest income, and Net NPA Decreased to 2.92% from 3.79% in the previous quarter. Overall Q4 results beat the street estimated rate makes BoB Shares gain in the market.

BANK OF BARODA Market price is moving in box pattern and market has rebounded from the support area of the pattern

Following a performance in line with expectations for the January-March quarter (Q4FY24), brokerages maintained their optimistic outlook on Bank of Baroda (BoB). The bank saw both its profit and net interest income (NII) grow by 2.3 percent year-on-year (YoY) during Q4, leading analysts to perceive the stock’s valuations as appealing for potential re-rating.

Year-to-date, BoB’s shares have surged over 10 percent, outperforming the modest 1.5 percent rise observed in the benchmark Nifty 50 index.

Despite encountering certain one-off events, BoB’s Q4 performance was deemed stable by analysts. JPMorgan analysts, maintaining an ‘overweight’ rating, raised the target price to Rs 340 per share, indicating a 33 percent upside from current levels. They highlighted that BoB’s Q4 profit surpassed estimates despite the additional impact of wage revisions, with net slippages remaining low at 45 basis points for the March-ended quarter.

Motilal Oswal analysts reiterated a ‘buy’ recommendation on BoB, maintaining a target price of Rs 300 per share. They remarked that the bank reported a steady quarter and adjusted their earnings per share (EPS) estimates for FY25/FY26 by 1.9 percent/2.8 percent to reflect stable margins and controlled provisions. They forecast a return on assets (RoA) and return on equity (RoE) of 1.22 percent and 17.3 percent, respectively, for FY26.

BoB’s asset quality remained resilient, with gross non-performing assets (NPAs) at 2.92 percent in Q4FY24, down from 3.79 percent a year ago. Kotak Institutional Equities analysts noted that the bank’s asset quality continued to fare well, with FY24 slippages at 1.4 percent, alleviating concerns about portfolio stress. They maintained an ‘add’ rating with a target price of Rs 280 per share.

However, BoB’s net interest margin contracted to 3.18 percent in Q4FY24 from 3.31 percent in the year-ago period due to a higher cost of funds. Conversely, it expanded by 17 basis points sequentially. Management has maintained margin guidance at 3.15 percent for FY25, attributing it to slower growth in overseas loans and a lower impact of deposit repricing.

Operationally, BoB witnessed a 7.7 percent YoY growth in total domestic deposits and a 12 percent YoY climb in domestic advances during Q4FY24. Management has projected a 12-14 percent growth in loans and a 10-12 percent growth in deposits going forward.

In terms of valuation, Morgan Stanley analysts anticipate the stock’s recovery to persist owing to improved valuations. They maintained an ‘equal-weight’ rating and raised the target price to Rs 280 per share. Additionally, analysts at Nuvama believe that BoB’s current trading discount relative to SBI is warranted. They share a ‘hold’ rating on the stock with a target price of Rs 255 per share.

ABB: ABB Stock Surges 7% on Strong Q1 Results; Motilal Oswal Recommends ‘Buy’

ABB Company report strong Q4 Result in 2024, Net Profit rises to 83% as Rs.467 Cr and Revenue increased to 29% YoY as Rs.3080 cr and EBITA came at 18.3%, This contribution comes from Efficient utilisation in the Electrification segment.

ABB INDIA Market price is moving in Ascending channel and market has reached higher high area of the channel

This surge came on the heels of the company’s March quarter earnings report, which exceeded market expectations.

Analysts remained bullish on ABB India as the major player in electrification and automation disclosed an impressive 82 percent year-on-year increase in net profit, totaling Rs 467 crore, attributed to higher revenue. The company’s total income also saw a substantial 29 percent year-on-year growth, reaching Rs 3,080 crore for the period.

According to analysts at Nomura, ABB India’s EBITDA margin of 18.3 percent in the March quarter surpassed expectations, largely driven by the execution of higher margin orders and efficient capacity utilization in the electrification segment. They also noted pricing advantages in select products and a favorable job mix in the Motion segment.

Nomura highlighted ABB’s structural change over the past three years, with a margin trajectory of 14-15 percent, supported by strong industry tailwinds, enhanced penetration, and localization efforts. They anticipate sustained growth, projecting revenue, EBITDA, and PAT CAGR of 18 percent, 21 percent, and 22 percent, respectively, over CY23-26.

Despite acknowledging ABB’s strong performance, Nomura maintained a ‘Neutral’ rating due to expensive valuations, with a target price of Rs 6,660 based on sum-of-the-parts (SOTP) analysis.

Motilal Oswal sees further potential for margin improvement for ABB, attributing its success to being among the top players in critical segments like electrification, automation, and data centers. They anticipate favorable margins driven by factors such as improved product mix, higher services share, better operating leverage, and group management fees.

Jefferies also reiterated a ‘buy’ rating on ABB, raising the target price to Rs 8,845 per share, expecting the company’s order flows to increase post-elections in the second half of CY24.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!