Delhivery: Delhivery Stock Falls 5% After Q4 Loss; Emkay Reiterates ‘Buy’

The Delhivery Logistics Company reported the Loss of Rs.68.5 cr in the Q4FY24 and 11.5 cr profit in the last quarter. This loss is narrowed down 57% from Rs.159 cr in the Q4FY23. The Revenue is up by 12% YoY to Rs.2076 cr. EBITA increased by Rs.46 cr from Rs.13 cr printedin the last quarter, Margin are at 2.2%it is lower than 2.6% street estimates.

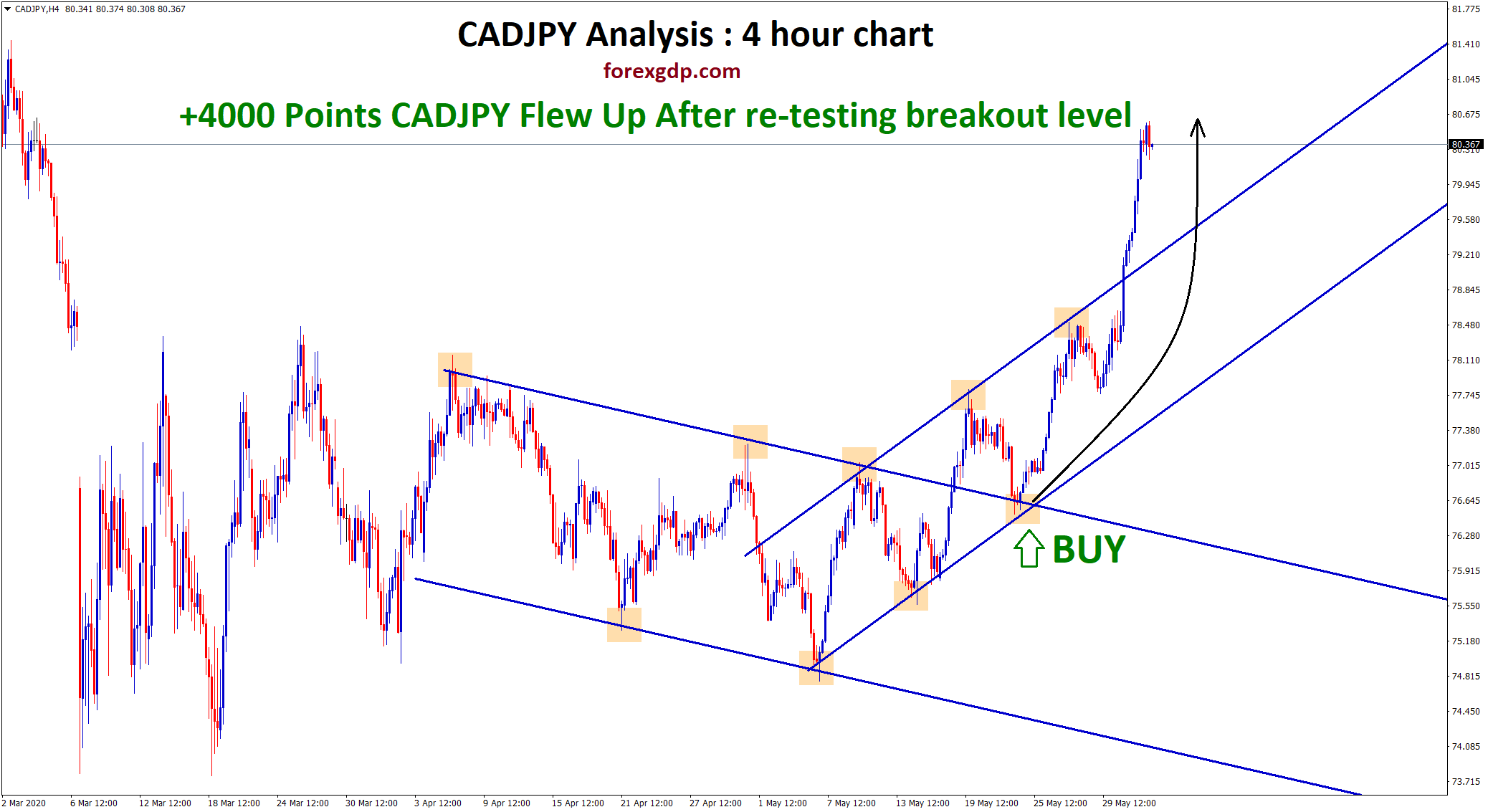

DELHIVERY is moving in Ascending channel and market has fallen from the higher high area of the channel

Shares of Delhivery slumped 5 percent on May 18 after the logistics solutions company reported a loss of Rs 68.5 crore for the March quarter (Q4FY24), compared to a profit of Rs 11.7 crore in the December quarter. However, the year-on-year (YoY) loss narrowed by 57 percent from Rs 159 crore in Q4FY23.

In the March FY24 quarter, Delhivery’s revenue rose 12 percent YoY to Rs 2,076 crore, driven by significant growth in the partial truckload (PTL) and full truckload (FTL) segments, which increased by 27 percent and 60 percent YoY, respectively.

Despite Q4 being seasonally weaker for the PTL industry, Delhivery saw a 21 percent YoY improvement in PTL volumes due to enhanced service levels and a stronger sales force in tier 2+ cities. Conversely, its express business faced challenges from seasonal factors and the insourcing of volumes by a key customer.

The company’s EBITDA increased to Rs 46 crore from Rs 13 crore a year ago. However, margins came in at 2.2 percent, below the street estimates of 2.6 percent, despite a 58 basis points expansion in gross margin. Delhivery’s integrated offerings, tech investments, and scale advantages have helped it gain market share in the PTL segment and strengthen its leadership in the 3PL Express market.

Emkay Global remains optimistic about Delhivery’s future, maintaining a ‘buy’ rating with a target price of Rs 500. The brokerage expects the company to turn PAT positive in FY25, supported by reduced capex intensity and a net cash balance sheet, which should mitigate short-term volume pressures.

ASTRAL: Astral Stock Dips 5% After Disappointing Q4 Results; Profit and Margins Decline

The Astral Bathware segment company reported 12% YoY dipped Net profit to Rs.181.6 cr, Revenue is up by 8% and reached Rs.1625 cr in Q4FY2024. EBITA declined 5.7% to Rs.291.4 cr from Rs.309cr in the last quarter. The company has opened 1000 showrooms and Net sales at 24.2 cr so far this quarter.

ASTRAL Market price is moving in Ascending channel and market has reached higher high area of the channel

Shares of Astral experienced a decline of up to 5 percent in the special trading session on May 18, following the company’s report of a 12 percent year-on-year drop in its net profit to Rs 181.6 crore for the January-March quarter of FY24.

Despite this decline in profit, the building materials and equipment firm witnessed an 8 percent rise in revenue from operations, reaching Rs 1,625 crore in Q4FY24.

Operationally, Astral’s earnings before interest, tax, depreciation, and amortization (EBITDA) saw a decline of 5.7 percent to Rs 291.4 crore in the same period, down from Rs 309 crore in the corresponding quarter of the previous fiscal year. The company’s EBITDA margin stood at 17.9 percent in the March quarter, down from 20.5 percent in the corresponding period in FY23.

During the quarter under review, Astral’s bathware segment recorded sales of Rs 24.2 crore. With the company surpassing 1,000 showrooms or dealers, it anticipates significant growth in the bathware division in FY25.

The company’s board has proposed a final dividend of Rs 2.25 per equity share of Rs 1 each (face value) for FY2024, subject to approval by members at the upcoming annual general meeting (AGM).

Over the last three years, Astral’s stock has delivered returns of approximately 64 percent, surpassing Nifty returns of around 48 percent during this period.

JSW STEEL: JSW Steel Stock Rises Despite 64.5% YoY Profit Decline

The JSW Steel company reported 64.5% Net profit decreased results as Rs.1299 cr in Q4FY24. The revenue declined to 1.5% as Rs.46296 cr from Rs.46962 cr in the last quarter. The main reason for dipping net profit is higher coking coal prices and domestic steel demand is reducing by china steel imports.

JSW STEEL Market price is moving in Ascending channel and market has rebounded from the higher low area of the channel

JSW Steel saw a modest increase of nearly 0.8 percent during early morning trade on the NSE despite reporting a weak performance in Q4FY24, as disclosed on May 17.

In its regulatory filing, JSW Steel revealed a notable 64.5 percent year-on-year decrease in net profit to Rs 1,299 crore for the quarter ended March 31, 2024. This decline was primarily attributed to higher coking coal prices and reduced realizations amid challenging conditions in the domestic steel market. Revenue for Q4FY24 also experienced a slight dip of 1.5 percent, amounting to Rs 46,269 crore compared to Rs 46,962 crore in the previous fiscal period.

During the quarter, consolidated crude steel production stood at 6.79 million tonnes, while the company invested Rs 3,503 crore in consolidated capital expenditures.

Furthermore, JSW Steel’s board approved a plan to raise funds up to Rs 7,000 crore through non-convertible debentures (NCDs) with warrants, equity, or convertible shares. The company’s regulatory filing specified that the board endorsed the issuance of NCDs with warrants, convertible into or exchangeable with equity shares of the Company with a face value of Rs 1 each at a later date.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!