XAUUSD – Gold Gains Today, Ends Week Down 3%

The Gold prices are down 3% this week it is the biggest weekly loss since December 2023. The World Gold council announced Central banks bought 2200 tons of Gold Since Q22022. The FED is expected to delay rate cuts this year and may or may not be rate cut vision moved Gold down against USD. The US Consumer durable goods order for the month of April came at 0.70% MoM versus 0.80% in the March month. One Year inflation expectations in the US increased to 3.3% from 3.2% and 5 year inflation expectations stands at 3%.

XAUUSD is moving in Ascending Triangle and market has reached higher low area of the channel

Gold prices stabilized on Friday after experiencing consecutive days of losses, rising by 0.23%. Despite this recovery, gold was down more than 3% for the week, marking its largest weekly loss since December 2023. Better-than-expected US Durable Goods Orders data had a limited impact due to a downward revision to the previous month’s figures, which supported a rebound in gold prices.

Gold traders stepped in before the weekend, reacting to US economic data released on Thursday that showed increased business activity, reducing the likelihood of Federal Reserve (Fed) rate cuts. As of now, fed funds rate futures indicate just a 25 basis points cut in interest rates in 2024.

Friday’s data provided little optimism for a looser Fed policy. The US Department of Commerce reported positive Durable Goods Orders for April, but the impact was muted by a downward revision for March, which, along with a decline in US Treasury yields, aided gold’s recovery.

Additionally, the University of Michigan’s recent consumer sentiment survey showed slight improvement, though inflation expectations were mixed.

The US 10-year Treasury note yield fell to 4.461%, dropping one-and-a-half basis points, which weakened the US Dollar. The US Dollar Index (DXY), measuring the dollar’s performance against a basket of currencies, traded at 104.70, down 0.33%.

Market Movers:

– Gold prices climbed due to declining US Treasury yields, a weaker US Dollar, and improved risk appetite as Wall Street regained some ground.

– US Durable Goods Orders for April rose by 0.7% month-on-month, better than the expected -0.8% contraction, but lower than the downwardly revised 0.8% for March.

– The University of Michigan Consumer Sentiment Index for May was 69.1, down from April’s 77.2 but above the forecast of 67.5. One-year inflation expectations slightly increased to 3.3% from 3.2%, while five-year expectations remained at 3%.

– S&P Global’s final US PMI readings for May showed the Manufacturing PMI rose to 50.9, and the Services PMI increased to 54.8, both surpassing estimates.

XAUUSD is moving in Ascending channel and market has reached higher high area of the channel

– FOMC Minutes indicated uncertainty among Fed officials regarding the extent of policy restrictiveness, noting it might take longer to confidently achieve the 2% inflation target.

– Gold prices were supported by central bank purchases from emerging markets, driven by Western sanctions on Russia following its invasion of Ukraine.

– The World Gold Council reported that central banks added around 2,200 tons of gold since Q3 2022.

EURUSD – ECB’s Nagel: June Cut Likely, Next Move May Wait Until September

The ECB governing Council Member Dr. Joachim Nagel said rate cuts after the June month is not the route for consecutive rate cuts from the ECB. Currently Wage prices are not rise and Inflation is decreasing so we go for rate cuts expected in the June month meeting, we donot repeated rate cuts this year based on data dependent only. Euro pairs weakness in the market after the speech.

EURUSD is moving in Descending channel and Market has reached lower high area of the channel

European Central Bank (ECB) Governing Council Member Dr. Joachim Nagel commented on Friday that following an initial rate cut from the ECB, there would likely be a period of observation before considering another rate reduction.

Key Highlights:

– The increase in wages came as no surprise.

– The rise in wages is correlated with the high inflation rates observed in the past.

– Both core and headline inflation are showing signs of deceleration.

– The ECB is likely to be able to implement rate cuts in June.

– Dr. Nagel emphasized that there is no automatic process for rate cuts.

– Following any rate adjustments in June, it is anticipated that the next move may not occur until September.

USDJPY – Japanese Yen Stumbles Amid BoJ Rate-Hike Uncertainty

The JPY pairs are weakness in the market due to BoJ did not change the value of buying JGB Bonds operation market. One Year JGB Yields surpassed 1% on the expectations of BoJ do another rate hike in order to control the weakness of JPY in the market. CPI data for the April month came at 2.5%YoY versus 2.7% in the last month, Core CPI data came at 2.2% versus 2.6% in the last month.

USDJPY is moving in Ascending channel and market has reached higher low area of the channel

The Japanese Yen (JPY) continues to face downward pressure in Friday’s New York session following the release of softer National Consumer Price Index (CPI) data by the Statistics Bureau of Japan. April saw the annual inflation rate drop to 2.5% from 2.7% in the previous month, marking the second consecutive month of moderation while still staying above the Bank of Japan’s (BoJ) 2% target. This sustained inflation rate keeps pressure on the central bank to consider further tightening of monetary policy.

The Bank of Japan has emphasized the importance of achieving a virtuous cycle of sustained, stable attainment of its 2% price target, along with robust wage growth, for normalizing policy. Investors anticipate that the continued weakness of the JPY might prompt the BOJ to expedite its next interest rate hike to mitigate the impact on the cost of living, according to Reuters.

Meanwhile, the US Dollar (USD) experiences a sharp decline despite the hawkish sentiment surrounding the Federal Reserve (Fed), which aims to maintain higher policy rates for an extended period. This sentiment is supported by the release of higher-than-expected United States (US) Purchasing Managers Index (PMI) data on Thursday.

Daily Digest Market Movers: Japanese Yen Extends Losses Amid Soft CPI:

– Japan’s Core CPI (YoY), excluding fresh food but including fuel costs, rose 2.2% in April as expected, marking the second consecutive month of slowing from March’s reading of 2.6%.

– The S&P Global US Composite PMI surged to 54.4 in May from 51.3 in April, reaching its highest level since April 2022, surpassing market expectations of 51.1. The Service PMI recorded a growth of 54.8, indicating the largest output growth in a year, while the Manufacturing PMI edged up to 50.9.

– According to the CME FedWatch Tool, the probability of the Federal Reserve reducing interest rates in September decreased to 49% from 51% a day earlier.

– The Bank of Japan announced on Thursday that it maintained the amount of Japanese government bonds (JGB) unchanged compared to the previous operation. A month ago, the BoJ reduced the amount of 5-10 years it purchased in a scheduled operation.

– Tensions escalate following Lai Ching-te’s assumption of office as Taiwan’s new president, with Chinese state media reports indicating China’s deployment of numerous fighter jets and simulated strikes in the Taiwan Strait and around Taiwan-controlled islands, per Reuters.

– Japan’s Manufacturing Purchasing Managers Index (PMI), released by Jibun Bank and S&P Global, rose to 50.5 in May from April’s 49.6, surpassing market expectations of 49.7. This marks the first growth since May 2023. However, the Services PMI fell to 53.6 from the previous 54.3, still indicating the fastest expansion in eight months.

– Japan’s 10-year government bond yield surpassed 1% this week for the first time since May 2013, driven by traders’ increasing bets that the Bank of Japan would further tighten policy in 2024.

USDCHF – Nears 0.9150 as Traders Favor US Dollar

The Swiss Employment numbers came at Q1 is 5.488M versus 5.484M in the past quarter. The SNB has done rate cuts in the March month it is the nine year after rate cuts done. Still way to go for rate cuts from SNB if inflation sustained in the 0-2% target level.

USDCHF is moving in Ascending channel and market has reached higher low area of the channel

This upward movement comes after traders shifted their attention to the US Dollar (USD) following the release of higher-than-expected Purchasing Managers Index (PMI) data from the United States (US), which subdued risk appetite. The robust data further reinforced the hawkish sentiment surrounding the Federal Reserve (Fed), indicating a potential continuation of elevated policy rates.

The S&P Global US Composite PMI surged to 54.4 in May, up from 51.3 in April, marking its highest level since April 2022 and surpassing market expectations of 51.1. Notably, the Service PMI recorded a significant increase to 54.8, signaling the most substantial output growth in a year, while the Manufacturing PMI climbed to 50.9.

Meanwhile, Federal Reserve Bank of Atlanta President Raphael Bostic expressed on Thursday that the inflation outlook might not improve as rapidly as anticipated by market participants. According to the CME FedWatch Tool, the likelihood of the Federal Reserve implementing a 25 basis-point rate cut in September decreased to 46.6% from 49.4% the previous day.

In Switzerland, the Swiss Statistics Employment Level (QoQ) data revealed that the total number of employed workers stood at 5.484 million in the first quarter, slightly below the previous reading of 5.488 million.

The yield on the 10-year Swiss government bond remains around 0.76%, indicating the likelihood of the Swiss National Bank (SNB) maintaining current interest rates. This scenario could potentially strengthen the Swiss Franc (CHF) and weaken the USD/CHF pair.

Investors are closely monitoring for signals on when the Fed will commence cutting interest rates. Meanwhile, the Swiss National Bank surprised markets by lowering interest rates for the first time in nine years in March, reducing the key interest rate by 25 basis points to 1.50%, making it the first major central bank to ease its monetary policy.

USDCAD – Canadian Dollar Rebounds Despite Retail Sales Miss

The Canada retail sales data for the month of March came at -0.20% MoM versus -0.10% MoM in the previous month. Excluding Automobiles retail sales printed at -0.60% MoM versus -0.20% in the last month. The BoC is giving way for rate cuts in the June month by the weak economic data in inflation and retail sales numbers in the past months.

USDCAD is moving in Ascending channel and market has reached higher low area of the channel

The Canadian Dollar (CAD) staged a recovery on Friday, driven by a shift in investor risk appetite. Despite weaker-than-expected Canadian economic data, broader market sentiment improved, pushing the US Dollar (USD) lower. This shift was prompted by positive developments such as higher-than-anticipated US Durable Goods Orders and slightly eased Consumer 5-year Inflation Expectations in May.

Daily Digest Market Movers:

– Canadian Retail Sales experienced a downturn of -0.2% month-on-month (MoM) in March, missing the forecasted recovery to 0.0% from the previous month’s -0.1%. Retail Sales excluding Automobiles dropped to a nine-month low of -0.6% MoM, significantly missing the forecast of 0.1%. However, the previous month’s figure was revised slightly upward to -0.2% from -0.3%.

– US Durable Goods Orders in April rose by 0.7%, surpassing the forecasted -0.8% decline, although the previous month’s print was revised sharply lower to 0.8% from 2.6%.

– The University of Michigan’s Consumer Sentiment Index showed a firm increase to 69.1 compared to the previous month’s 67.4. Median market forecasts had anticipated a slight uptick to 67.5.

– Consumer Inflation Expectations for the next five years, as measured by the University of Michigan, eased slightly to 3.0% in May, compared to the expected hold at 3.1%.

– Market sentiment rebounded on Friday following a midweek spike in risk aversion triggered by a significant adjustment in investor expectations for rate cuts. The CME’s FedWatch Tool indicates that rate markets are now pricing in nearly-even odds of a rate cut from the Federal Reserve (Fed) in September, down sharply from 70% at the beginning of the week.

USD INDEX – US Dollar Retreats Ahead of Upcoming PCE and GDP Data

The US Dollar moved up this week after the robust economic data printed this week. FED speakers believed the US economy is performing very well and no need of rate cuts this year. This news boosted US Dollar against counter pairs.

USD Index Market price is moving in Ascending channel and market has reached higher low area of the channel

This week, the US reported strong domestic economic data, including rising preliminary May PMIs from S&P Global, robust Durable Goods Orders, and favorable Jobless Claims figures, suggesting a potential continuation of the US Dollar’s recovery.

The Federal Reserve’s (Fed) cautious stance on premature easing will likely limit any significant downward movement in the DXY. Next week, the release of April’s Personal Consumption Expenditures (PCE), the Fed’s preferred inflation gauge, could influence the central bank’s messaging and policy direction.

Daily Digest Market Movers:

– Despite signs of economic resilience, the DXY is seeing losses.

– US Durable Goods Orders increased by 0.7% in April, exceeding market expectations of a 0.8% decline, although March’s figures were revised down to 0.8%.

– Excluding transportation, new orders rose by 0.4%. Without defense orders, new orders remained almost unchanged.

– The Fed remains cautious about premature easing, with members indicating that the current policy rate may persist for an extended period. Market probabilities for a rate cut are around 50% in September and 85% in November, with a cut expected by December.

GBPUSD – Pound Sterling Rebounds Despite Weak UK Retail Sales, Thanks to Decline in US Dollar

The UK retail sales for the month of April came at -2.3% MoM versus -0.40% decline expected and -0.20% decline in the last month, Core Retail sales came at -2.0% MoM versus -0.60% in the March. YoY decline to -2.7% in the April month versus 0.40% increase in the March month and Core YoY data declined to -3.0%. GBP Down after the Retail sales figures tremendous sharp fall in the market. The rate cut bets is higher in the June month from BoE by the economists view. Continuous falling in the inflation reading, consumer spending and Manufacturing data.

GBPUSD is moving in Symmetrical Triangle and market has reached lower high area of the channel

Earlier, the GBP/USD pair had faced significant pressure following the release of weak Retail Sales data for April by the United Kingdom (UK) Office for National Statistics (ONS), combined with the US Dollar’s extended recovery.

According to the ONS, monthly Retail Sales experienced a sharper decline than anticipated, contracting by 2.3%. Economists had forecasted a decrease of 0.4% from the prior reading of -0.2%, which had been revised downward from a previously stagnant performance. Additionally, annual Retail Sales saw a contraction of 2.7% after expanding by 0.4% in March, a downward revision from 0.8%. Economists had expected a decline of 0.2%.

Retail Sales data serves as an indicator of current consumer spending patterns, which significantly contribute to economic growth. The substantial decrease in sales at retail establishments suggests that the impact of the Bank of England’s (BoE) higher interest rates has deeply affected consumer spending. Weak Retail Sales data also serves as a leading indicator of the inflation outlook, with low figures suggesting a potential easing of price pressures. This scenario could prompt the BoE to consider shifting towards policy normalization sooner than previously anticipated.

Daily Digest Market Movers: Pound Sterling Rises Amid US Dollar Pressure:

– Despite weak economic indicators such as Retail Sales and the preliminary S&P Global/CIPS UK Purchasing Managers Index (PMI) data for May, released on Thursday, the Pound Sterling rebounded to 1.2700.

– The Composite PMI dropped to a two-month low at 52.8, below estimates of 54.0 and the prior reading of 54.1, driven by a significant decline in the Services PMI to a six-month low at 52.9 from the consensus of 54.7.

– While the Manufacturing PMI showed growth above the 50.0 threshold, economists had forecasted a smaller increase to 49.5 from April’s 49.1.

– The weak economic indicators have raised concerns about the UK economic outlook, potentially reigniting speculation about a rate cut by the BoE from its June meeting.

– Meanwhile, the US Dollar experienced a slight decline but maintained gains. The US Dollar Index (DXY) hovered near the crucial resistance level of 105.00 amid uncertainty about the timing of potential interest rate reductions by the Federal Reserve (Fed).

– According to the CME FedWatch tool, traders perceive a 49% probability of interest rates being lower than the current level at the September meeting, down from 64% recorded a week earlier due to the Fed’s hawkish guidance on interest rates and strong preliminary PMI data for May.

AUDUSD – AUD Slips on Strengthening USD, Focus on Consumer Sentiment

The Australian Dollar moved down against counterpairs after the China increased the Mock of Fighter jets in the Taiwan Border. The inflation expectations for 12 month decreased to 4.1% in the may month from 4.6% in the April month. Manufacturing PMI data came at 49.6 it is the 4th consecutive decline in the reading, Services PMI came at 53.1 from 53.6 in the past month.

AUDUSD has broken Ascending channel in downside

AUD Declines Amid USD Strength, RBA Minutes and US Economic Data Awaited

The Australian Dollar (AUD) extends its downward trajectory for the fourth consecutive session on Friday, facing pressure possibly due to increased risk aversion. The AUD/USD pair dips as the US Dollar (USD) gains ground, fueled by hawkish sentiments surrounding the Federal Reserve (Fed) and expectations of prolonged higher policy rates.

The Australian Dollar weakens further as Consumer Inflation Expectations for future inflation over the next 12 months drop to 4.1% in May, down from April’s 4.6%, hitting its lowest level since October 2021. This decline raises concerns about inflation persisting above the target for an extended duration. The latest Reserve Bank of Australia (RBA) meeting minutes reveal policymakers’ agreement on the challenge of predicting future changes in the cash rate.

Meanwhile, the US Dollar continues its ascent following the release of upbeat Purchasing Managers Index (PMI) data from the United States (US) on Thursday. The data prompts fears that interest rates may remain elevated for a longer period, leading to a surge in Treasury yields. Moreover, concerns about inflation persisting longer than anticipated, as highlighted in the recent Federal Open Market Committee (FOMC) Minutes, contribute to the USD’s strength.

Market watchers eagerly await the release of US Durable Goods Orders, which provide insights into manufacturers’ orders for durable goods intended to last three years or more. Additionally, the Michigan Consumer Sentiment Index will offer valuable perspectives on US consumers’ financial and income outlook.

In other developments, the ASX 200 Index rebounds, hovering around 7,740 on Friday, despite pressure from lower commodity prices. Australian equities face headwinds amid concerns that the Federal Reserve might prolong higher interest rates, prompted by stronger-than-expected US PMI data.

Furthermore, preliminary data indicates that Australian private sector activity remains expansionary for the fourth consecutive month in May. However, any geopolitical tensions, such as reported deployments of Chinese fighter jets near Taiwan-controlled islands, may impact the Australian market, given the close trade ties between China and Australia.

NZDUSD – NZ Confidence Up, Rate Cuts Unlikely; US PMI Impact

The ANZ Roy Morgan Consumer confidence up by 84.9 in May month from 82.1 in the past month. The RBNZ Assistant governor Karen Silk said there is no chances for rate cuts in this year due to higher inflation persists in the NZ economy. The NZ Dollar boosted by the comments from RBNZ Governors against counter pairs.

NZDUSD is moving in Ascending channel and market has rebounded from the higher low area of the channel

NZD/USD faced downward pressure amid rising risk aversion sentiment triggered by the release of higher-than-expected Purchasing Managers Index (PMI) data from the United States (US) on Thursday. This data bolstered the already hawkish sentiment surrounding the Federal Reserve (Fed), suggesting that the central bank may maintain higher policy rates for an extended period. As a result, the NZD/USD pair hovered around 0.6100 during the Asian trading session on Friday.

The S&P Global US Composite PMI climbed to 54.4 in May from April’s 51.3, marking its highest level since April 2022 and surpassing market expectations of 51.1. Both the Service PMI and the Manufacturing PMI showed significant growth, reaching 54.8 and 50.9, respectively.

Furthermore, the latest Federal Open Market Committee (FOMC) Minutes revealed that Fed policymakers expressed concerns about the persistent lack of progress on inflation, which has been more enduring than initially anticipated at the beginning of 2024.

Investors are anticipated to closely monitor US Durable Goods Orders data on Friday, which provides insight into orders received by manufacturers for durable goods expected to last three years or more. Additionally, the Michigan Consumer Sentiment Index will offer valuable information on consumer sentiments regarding financial and income situations in the US.

In New Zealand, the ANZ – Roy Morgan Consumer Confidence index rose to 84.9 in May from April’s 82.1, although it remains relatively subdued compared to pre-pandemic levels. While this increase may have provided some support for the New Zealand Dollar (NZD), it helped limit the downside of the NZD/USD pair.

Deputy Governor Christian Hawkesby of the Reserve Bank of New Zealand (RBNZ) stated on Friday that “cutting interest rates is not part of the near-term discussion.” Additionally, RBNZ Assistant Governor Karen Silk expressed concerns about near-term inflation risks, indicating that the bank has adjusted its modeling after underestimating domestic inflation strength.

In an interview with Bloomberg on Thursday, Governor Adrian Orr downplayed the likelihood of another interest rate hike, suggesting that the central bank would only tighten policy further if necessary to contain inflation expectations. Orr also mentioned that the RBNZ could consider easing before inflation reaches 2%.

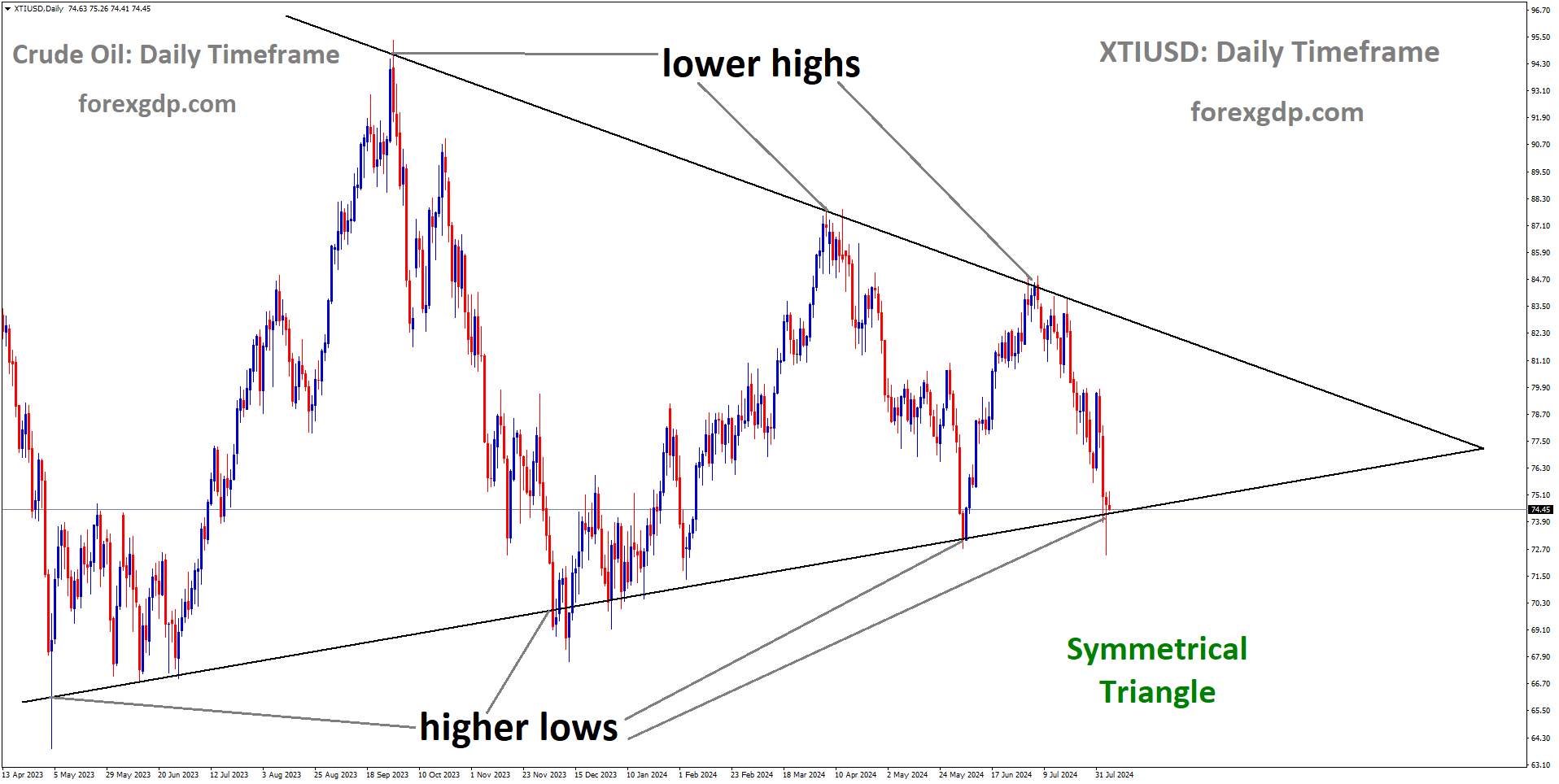

CRUDE OIL – Crude Oil Rebounds, WTI Enters Congestion on Friday

The Crudeoil prices are dipped after the US Core Durable goods order data came at positive yesterday. EIA reported supply of Oil in the week ended May 17 also another cause for this dip of Oil. June 01 OPEC+ meeting is conducted and expected output cuts 2.2MBPD with no change.

XTIUSD is moving in Ascending channel and market has reached higher low area of the channel

The Crude Oil market received a boost from a recovery in broad market risk appetite, particularly after investor expectations for a rate cut from the Federal Reserve (Fed) in September diminished further during the week. According to the CME’s FedWatch Tool, traders are now pricing in slightly worse-than-even odds of at least a quarter-point rate cut from the Federal Open Market Committee (FOMC) in September, a significant decrease from the 70% odds at the beginning of the trading week.

Key Economic Indicators:

– US Durable Goods Orders rebounded in April, increasing by 0.7% month-on-month (MoM) compared to the forecasted -0.8% decline. However, March’s figure was revised downward to 0.8% from the initial print of 2.6%.

– The University of Michigan’s 5-year Consumer Inflation Expectations eased slightly to 3.0% for May, falling slightly below the forecasted hold at 3.1%. The moderation in inflation expectations has provided some relief to investor sentiment, particularly among commodity traders.

Forecast for the Coming Week: Fedspeak and PCE in Focus:

– Comments from policymakers at the Fed dominated financial headlines during the week, with officials emphasizing caution regarding rate cut expectations. The Fed continues to stress the need for more evidence that inflation will eventually decrease to the Fed’s target of 2% annual price growth.

– US Crude Oil production remains a concern for market participants, as supply counts defied forecasted declines, showing another buildup in US Crude Oil supply lines. Energy traders had anticipated a continued decline in US supply stocks, but unexpected increases in barrel counts reported by both the American Petroleum Institute (API) and the Energy Information Administration (EIA) have left Crude Oil speculators awaiting a potential increase in demand to alleviate pressure on US pumping capacity.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!