XAUUSD – Gold Price Holds Steady After Fed’s Decision Despite Upbeat US Inflation Report

The Gold prices are moving lower after the US FED makes no rate cuts in the June month meeting. FED Powell said still we have no confidence on inflation in the current reading to do rate cuts. Once 2% target reached we will do rate cuts from our side. Tight labour market, 2.4% GDP is forecasted this year. China paused Gold purchases after the 18 month buying , 72.80 Million Troy Ounces in the May month reported.

XAUUSD is moving in the Box pattern and the market has reached the support area of the pattern

Gold prices climbed on Wednesday, buoyed by a lower-than-expected inflation report in the United States (US), which increased the likelihood of a Federal Reserve (Fed) interest rate cut later in the year. However, the Fed’s cautious stance and Chairman Jerome Powell’s reluctance to commit to a specific timeline for rate cuts supported the US Dollar, tempering gains in the precious metal. As of now, XAU/USD is trading at $2,318, marking a modest increase of 0.13%.

During Wednesday’s press conference, Fed Chair Jerome Powell expressed reduced confidence in the need for immediate rate cuts, stating, “If job market conditions deteriorate unexpectedly, the Fed stands prepared to act.” Regarding the latest US inflation figures, Powell cautioned against overreacting to a single report, stressing the importance of observing the inflation trend aligning with the Fed’s target.

In the Federal Open Market Committee (FOMC) monetary policy statement, the Fed signaled a reluctance to adjust rates until it sees sustained progress towards its 2 percent inflation target. The committee emphasized readiness to adapt monetary policy as needed to mitigate risks that could hinder achieving its objectives.

In the updated ‘dot-plot,’ which reflects Fed officials’ rate projections, the median expectation for the federal funds rate by late 2024 was revised upward from 4.6% to 5.1%. This adjustment suggests a forecast for just one rate cut, contrasting with the current effective federal funds rate at 5.33%.

Looking ahead, the Fed’s Summary of Economic Projections (SEP) for 2024 remains optimistic, forecasting a 2.1% growth rate consistent with earlier estimates, and an unemployment rate holding steady at 4%. Projections also indicate a slight increase in PCE inflation from 2.4% to 2.6%, and Core PCE inflation rising from 2.6% to 2.8%.

Earlier data from the US Bureau of Labor Statistics (BLS) showed stagnant inflation in May compared to April, which supported gold prices as US Treasury bond yields declined. This downturn in yields contributed to a drop in the US Dollar Index (DXY) to a three-day low of 104.71, further bolstering gold’s appeal.

Meanwhile, the CME FedWatch Tool reflected increased market expectations for a Fed rate cut in September, rising from 46.7% to 61.3% following the latest inflation report.

Despite these positive factors for gold, news that the People’s Bank of China (PBOC) halted its 18-month buying spree of bullion weighed on the precious metal. PBOC’s gold holdings remained unchanged at 72.80 million troy ounces in May, influencing market sentiment towards gold prices.

In summary, gold prices exhibited resilience amid mixed economic signals and central bank policy expectations, finding support from subdued US inflation data and declining bond yields, while facing headwinds from a stronger US Dollar and international monetary policy developments.

EURUSD – ECB’s Vasle: More Rate Cuts Possible if Baseline Scenario Holds

The ECB Policy maker BostJan Vasle said there more rate cuts this year if inflation close to 2% target level. Next year more rate cuts seen if disinflation trend continues. Wage momentum reading is stronger in the Euro zone.

EURUSD is moving in the Descending channel and the market has reach the lower high area of the channel

European Central Bank (ECB) policymaker Bostjan Vasle indicated on Thursday that additional rate cuts are possible if the current baseline scenario persists. He emphasized the potential for further rate reductions next year if the disinflationary trend continues, although he cautioned that there is a risk this process could decelerate. Vasle also noted that wage momentum remains relatively robust at present.

USDJPY – Japanese Yen Weakens as BoJ Expected to Adopt Dovish Stance

The Japanese Yen is depreciated against counter pairs on the expectations of rate hold and tapering of Bond purchases announcement. The BoJ Governor Ueda said in this week, inflation is moving towards 2% target once reached we gradually dropped the purchases of bonds in the market. Japan PPI data came at 2.4% in the May month from 2.0% printed in the April month.

USDJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The Japanese Yen (JPY) retraced its recent gains on Thursday as the US Dollar (USD) strengthened following a hawkish stance from the US Federal Reserve (Fed), which bolstered the USD/JPY pair. In its latest policy meeting on Wednesday, the Federal Open Market Committee (FOMC) opted to keep its benchmark lending rate unchanged within the 5.25%–5.50% range, as widely expected.

Looking ahead, caution prevails in the market as investors await the Bank of Japan’s (BoJ) policy decision on Friday. While no interest rate changes are anticipated from the BoJ, traders will closely monitor any indications regarding potential adjustments to the central bank’s monthly bond purchases.

The US Dollar Index (DXY), which gauges the USD against a basket of major currencies, recovered from recent losses thanks to the Fed’s hawkish stance. The FOMC revised its projection to only one rate cut this year, down from the three forecasted in March.

According to the CME FedWatch Tool, the probability of a Fed rate cut in September by at least 25 basis points decreased to 61.5%, down from 69.4% a week earlier.

Investors are focusing on upcoming US economic data, including the weekly Initial Jobless Claims and Producer Prices Index (PPI) on Thursday, for further insights into the US economic health.

In a post-decision press conference, Fed Chair Jerome Powell noted that the current tight monetary policy stance is achieving the intended effects on inflation. The US Consumer Price Index (CPI) for May showed a 3.3% year-over-year increase, slightly below both the prior reading and the expected 3.4%. Meanwhile, the core CPI, which excludes volatile food and energy prices, rose by 3.4% year-over-year in May, down from April’s 3.6% and below the anticipated 3.5%.

In Japan, the Producer Price Index (PPI) data indicated a 2.4% year-on-year increase in May, surpassing market expectations of a 2.0% rise, raising concerns about potential consumer inflation.

Japanese Finance Minister Shunichi Suzuki emphasized the importance of sustaining economic growth and achieving fiscal health to maintain confidence in the country’s fiscal policy.

A Reuters poll revealed that nearly two-thirds of economists anticipate the BoJ initiating tapering of its monthly bond purchases at the upcoming policy meeting, marking an initial step toward gradually reducing the central bank’s expansive balance sheet.

Bank of Japan Governor Kazuo Ueda recently indicated that inflation expectations are gradually increasing but have yet to reach the 2% target. Ueda underscored the need to monitor market developments closely as the central bank progresses toward scaling back its massive monetary stimulus.

In summary, the USD/JPY pair’s movement reflects market reactions to the contrasting monetary policies of the Fed and the BoJ, amid ongoing economic data releases shaping investor sentiment.

USDCAD – BoC’s Macklem: No Close to Limit of Divergence with Fed

The Bank of Canada Governor Tiff Macklem said we are not close to the limit of Divergence rates from the FED. People suffering more inflation and buying hardly in the Canada. So Rate cuts are done this month. We are close to the people minds and we ready to free the people from higher rates of interest by lowering the inflation to the target of 2%.

USDCAD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

Bank of Canada (BoC) Governor Tiff Macklem emphasized on Wednesday the importance of aligning Canadian interest rates with those set by the Federal Reserve (Fed), although he noted they are not yet at a point where divergence would be limited.

Key points from Macklem’s statements include:

- Inflation Concerns: Macklem acknowledged that high inflation has been a significant challenge for many Canadians, particularly those experiencing it for the first time. He described it as a painful experience for households across the country.

- Communication and Transparency: He stressed the need for clear communication to the public about the central bank’s decisions and the rationale behind them. Ensuring that people understand the BoC’s actions is crucial amid ongoing economic uncertainties.

- Inflation as a Common Challenge: Macklem underscored that controlling inflation remains a primary goal for the central bank, highlighting that recent economic history has served as a stark reminder of the detrimental impacts of inflation on the economy.

- Monetary Policy Outlook: While Macklem hinted at potential future interest rate cuts, he indicated that the BoC is approaching these decisions cautiously, evaluating the economic data and taking a step-by-step approach rather than committing to a specific timeline.

- Limits to Divergence: Regarding the alignment of Canadian rates with the Fed’s, Macklem acknowledged that there are limits to how far they can diverge before broader economic consequences arise. However, he clarified that Canada has not yet reached this threshold.

Overall, Macklem’s remarks underscore the BoC’s commitment to managing inflation while maintaining flexibility in monetary policy decisions to navigate economic uncertainties effectively.

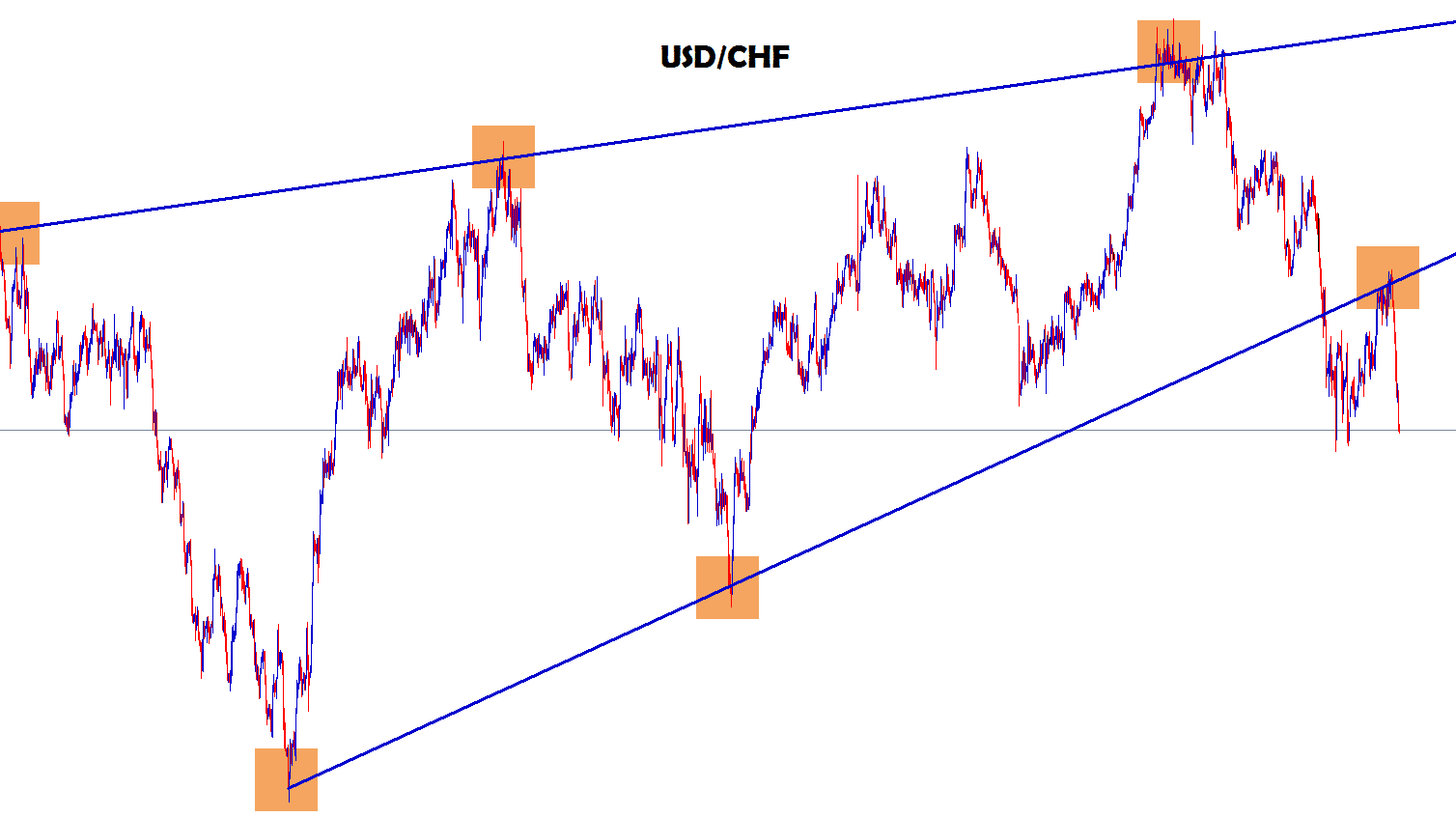

USDCHF – Approaches 0.8950 on Hawkish Fed Outlook; SNB Financial Stability Report in Focus

The Swiss Franc gets depreciated after the FED holds the rates at 5.25%-5.50% last day. SNB is like to hold the rates at the June 20th meeting due to SNB chairperson Thomas Jordan said inflation is little higher when compared to last quarters. SNB Financial stability report is scheduled this week.

USDCHF is moving in the Descending channel and the market has rebounded from the lower low area of the channel

The USD/CHF pair retraced its losses from the prior session following the US Federal Reserve’s (Fed) hawkish stance. In its latest policy meeting on Wednesday, the Federal Open Market Committee (FOMC) kept its benchmark interest rate unchanged within the 5.25%–5.50% range, aligning with market expectations.

Despite the Fed’s decision, the US Dollar encountered challenges after softer-than-expected inflation data was released. The US Consumer Price Index (CPI) showed a 3.3% year-over-year increase in May, slightly below both the previous reading and the anticipated 3.4%. Meanwhile, the core CPI, which excludes volatile food and energy prices, rose by 3.4% year-over-year in May, down from 3.6% in April and below the expected 3.5%.

Following the Fed’s announcement, Fed Chair Jerome Powell emphasized in a press conference that the current tight monetary policy stance is achieving the desired impact on inflation. Powell indicated that despite economic progress, the Fed has not yet gained sufficient confidence in inflation trends to warrant a rate cut this year.

Turning to Switzerland, the Swiss National Bank (SNB) is not expected to implement an interest rate cut in June, which is likely to support the Swiss Franc (CHF). SNB Chairman Thomas J. Jordan previously highlighted minor upward risks to inflation expectations.

Market participants are awaiting the SNB Financial Stability Report scheduled for Thursday, which will provide insights into the stability of the banking sector and financial market infrastructure. Additionally, attention will be on the Producer and Import Prices data for further economic indicators.

USD INDEX – Powell Discusses Rate Outlook After Policy Hold

US FED meeting outcome is rate unchanged at 5.25%-5.50% yesterday, FED Powell said we still have no confidence on inflation to do rate cut in the US economy. Labour Market well tight like before the pandemic time, inflation in the housing market is higher, we have to bring down this inflation first, then only we get inflation back to 2%target. Not only seeing wages is the big picture for inflation reading contribution, but also Housing market pressures the inflation up in the market.

USD INDEX is moving in the Box pattern and the market has fallen from the resistance area of the pattern

Federal Reserve Chairman Jerome Powell explains the decision to leave the policy rate, known as the federal funds rate, unchanged within the range of 5.25% to 5.5%. He also responds to questions during the post-meeting press conference.

Follow our live coverage of the Federal Reserve’s policy announcements and the subsequent market reaction.

Key Takeaways from the Fed Meeting Press Conference:

- “A broad set of indicators suggest the labor market is back to where it was on the eve of the pandemic.”

- “Overall, the broad set of indicators in the labor market shows it is relatively tight but not overheated.”

- “We expect labor market strength to continue.”

- “More recent readings on inflation have shown easing.”

- “So far this year, we have not gained greater confidence in inflation to warrant a rate cut.”

- “We will need to see more positive data to bolster confidence in inflation.”

- “If the economy remains solid and inflation persists, we will keep rates at the current level for as long as needed.”

- “The opposite is also true in terms of potential rate cuts.”

- “Our policy is well-positioned, and we will continue to make decisions on a meeting-by-meeting basis.”

- “We need further confidence and more positive inflation readings, but we won’t specify how many are needed to start cutting rates.”

- “We will also be looking at the balance of risks and the overall outlook.”

- “Unexpected weakness in the labor market could also prompt a response.”

- “We will be monitoring the labor market for signs of weakness, but we are not seeing that right now.”

- “We do not see ourselves as having the confidence that would warrant policy loosening at this time.”

- “I like to look at 3-month and 6-month series on payroll reports given differences between the establishment and household surveys.”

- “The overall picture is one of a strong and gradually cooling labor market.”

- “People are coming to the view that rates are less likely to return to pre-pandemic levels.”

- “We are making policy with the economy we have and the distortions we face.”

- “The question of whether the policy is restrictive enough will be answered over time.”

- “We are prepared to adjust policy as appropriate.”

- “The housing situation is complicated.”

- “Ultimately, the best thing we can do for the housing market is to bring inflation down.”

- “The banking system has been solid, strong, and well-capitalized.”

- “Wages are still running above a sustainable path.”

- “Wages are not the principal cause of inflation, but they need to come down for overall inflation to return to 2%.”

The US Federal Reserve announced on Wednesday that it left the policy rate, the federal funds rate, unchanged within the range of 5.25% to 5.5% following the June policy meeting. This decision was in line with market expectations.

Key Takeaways from the Federal Reserve’s Policy Statement and the Dot Plot:

- The revised Summary of Economic Projections, also known as the dot plot, published alongside the policy statement, showed that:

4 out of 19 officials saw no rate cuts in 2024,

7 projected a 25 basis points (bps) rate reduction,

8 marked down a 50 bps cut in the policy rate.

- “Fed officials’ median view of the federal funds rate at the end of 2024 is 5.1% (previously 4.6%).”

- “Fed officials’ median view of the federal funds rate at the end of 2025 is 4.1% (previously 3.9%).”

- “Fed officials’ median view of the federal funds rate at the end of 2026 is 3.1% (unchanged from previous projection).”

- “Fed officials’ median view of the federal funds rate in the longer run is 2.8% (previously 2.6%).”

- “Fed projections imply 25 bps of rate cuts in 2024 from the current level, and another 100 bps in 2025.”

- “Fed policymakers see end-2024 PCE inflation at 2.6% versus 2.4% in the March projection; core inflation is seen at 2.8% versus 2.6%.”

- “Fed policymakers see 2.1% GDP growth in 2024, with the unemployment rate at 4%; both unchanged from the March projection.”

- “Forecasts show 2025 PCE and core PCE inflation at 2.3% versus 2.2% in the March projection.”

- “There has been modest further progress toward the 2% inflation objective.”

- “The Fed does not expect it will be appropriate to reduce the policy target range until gaining greater confidence that inflation is moving sustainably toward 2%.”

- “The economy continues to expand at a solid pace, job gains remain strong, and the unemployment rate remains low.”

- “Inflation has eased over the past year but remains elevated.”

- “Risks to achieving policy goals have moved toward a better balance.”

- “The Fed will continue to reduce its holdings of Treasuries and mortgage-backed securities.”

- “The vote in favor of the policy was unanimous.”

GBPUSD – Trades with Mild Losses Below 1.2800 as Fed Holds Rates Steady

The GBP is moving down after the US FED holds the rates at steady last night. GBP GDP came at 0% in the April month from 0.40% printed in the March month. Stagnated growth in the GDP makes BoE have the chances to rate cut in June 20.

GBPUSD is moving in the symmetrical triangle pattern and the market has reached the top area of the pattern

This pullback followed a mixed impact on the US Dollar (USD): while the negative surprise in the US Consumer Price Index (CPI) inflation report for May initially weighed on the Greenback, the Federal Reserve’s (Fed) hawkish stance tempered its decline.

In May, US CPI inflation remained unchanged on a monthly basis, and the yearly rate eased to 3.3% from 3.4% in April, falling below market expectations of 3.4%. Excluding volatile food and energy prices, core CPI inflation increased by 0.2% in May and 3.4% year-on-year, down from April’s 3.6%.

The FOMC, in its June meeting, opted to maintain the benchmark lending rate within the 5.25%-5.50% range for the seventh consecutive time. The committee revised its economic projections, signaling only one rate cut for this year, down from three forecasted in March. The ‘dot-plot’ revealed a median expectation among FOMC officials for the federal funds rate to rise from 4.6% to 5.1% by late 2024.

Market sentiment adjusted swiftly, with futures traders now pricing in a 73% probability of a Fed rate cut in September, up from 53% before the CPI release, according to the CME FedWatch tool. Later on Thursday, investors awaited further US economic data, including the weekly Initial Jobless Claims, Producer Prices Index (PPI), and a speech by Fed’s John Williams.

On the UK front, economic growth stagnated in April, as reported by the Office for National Statistics (ONS), with GDP remaining flat after a 0.4% expansion in March, aligning with market forecasts. Attention turned to the upcoming Bank of England (BoE) meeting on June 20, where expectations of a rate cut in June have diminished, shifting towards potential moves in August or September.

In summary, the GBP/USD pair faced pressure after reaching recent highs, influenced by mixed US economic indicators and cautious positioning ahead of central bank actions on both sides of the Atlantic.

AUDUSD – Australian Dollar Fails to Gain Support Despite Robust Employment Data

The Australian Employment change came at 39.7K in the May month from 38.5K in the April month and 30.0 is expected. Unemployment rate came at 4.0% in the May month from 4.1% in the last month. The Australian Dollar loses even better employment data printed in the May month.

AUDUSD is moving in the Box pattern and the market has fallen from the resistance area of the pattern

The Australian Dollar (AUD) experienced slight depreciation despite positive employment data released on Thursday. Australia reported an increase of 39.7K employed individuals in May, surpassing expectations of a 30.0K rise and April’s 38.5K increase. Concurrently, the Unemployment Rate decreased to 4.0%, slightly lower than April’s 4.1% as forecasted.

However, the US Dollar (USD) regained strength following the US Federal Reserve’s (Fed) hawkish stance, which weighed on the AUD/USD pair. Market participants are now awaiting the US weekly Initial Jobless Claims and Producer Prices Index (PPI) on Thursday for further insights into the US economic landscape.

In its June meeting, the Federal Open Market Committee (FOMC) kept its benchmark lending rate unchanged within the 5.25%–5.50% range for the seventh consecutive time, aligning with market expectations.

Key highlights from the market movement include:

Fed Chair Jerome Powell affirmed in a post-decision press conference that the Fed’s current restrictive monetary policy stance is yielding the anticipated effects on inflation. The FOMC now anticipates only one rate cut this year, down from the three previously projected in March.

The US Consumer Price Index (CPI) for May rose by 3.3% year-over-year, slightly below both the prior reading and expectations of 3.4%. Meanwhile, the core CPI, which excludes volatile food and energy prices, increased by 3.4% year-over-year in May, down from April’s 3.6% and below the anticipated 3.5%.

China’s CPI data for May showed a 0.3% year-over-year increase, missing expectations of a 0.4% rise. Month-over-month (MoM), inflation declined by 0.1%, contrasting with April’s 0.1% increase.

Australian Treasurer Jim Chalmers emphasized the significance of China Premier Li Qiang’s visit to Australia, acknowledging underlying economic challenges in China and suggesting caution regarding immediate economic recovery expectations.

Australia’s NAB Business Confidence index dropped to -3 index points in May, the lowest in six months, turning negative for the first time since November last year. Concurrently, Business Conditions slipped to 6 index points, slightly below the long-term average.

National Australia Bank (NAB) Chief Economist Alan Oster highlighted concerns about growth prospects alongside cautious optimism regarding inflation. Oster expects the Reserve Bank of Australia (RBA) to maintain its current interest rates as it navigates these economic dynamics.

RBA Governor Michele Bullock recently indicated readiness to adjust interest rates should the Consumer Price Index (CPI) fail to return to the target range of 1%-3%.

Overall, the AUD’s movement reflects a combination of domestic economic data releases, global market sentiment influenced by the Fed’s monetary policy stance, and international developments impacting Australia’s economic outlook.

NZDUSD – Slips to Around 0.6150 After Ending Winning Streak; US PPI Data Awaited

The NZD Dollar moved down after the Electronic Card retail sales spending down to -1.1% MoM versus -0.40% MoM in the April month. Annual data came at -1.6% drop in the May month from -3.8% drop in the April month. FED meeting outcome also dragged the NZ Dollar against USD.

NZDUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel

The decline in the NZD/USD pair can be attributed to the strengthening of the US Dollar (USD) following the hawkish stance maintained by the US Federal Reserve (Fed) during its Wednesday meeting. Investors are now focused on upcoming US economic data releases, particularly the weekly Initial Jobless Claims and Producer Prices Index (PPI), for further insights into the US economic conditions.

During its June meeting, the Federal Open Market Committee (FOMC) opted to keep its benchmark lending rate unchanged in the range of 5.25%–5.50%, in line with market expectations. Fed Chair Jerome Powell emphasized in a post-decision press conference that the Fed’s current restrictive monetary policy stance is achieving the anticipated impact on inflation. Powell stated that despite economic progress, the Fed has not yet gained sufficient confidence in inflation trends to warrant a rate cut this year.

The US Dollar Index (DXY), which measures the USD against a basket of major currencies, edged higher towards 104.80, potentially supported by a rebound in US Treasury yields. As of the latest update, the 2-year and 10-year US Treasury bond yields stood at 4.76% and 4.32%, respectively.

In New Zealand, Electronic Card Retail Sales decreased by 1.1% month-over-month in May, a sharper decline compared to April’s 0.4% decrease. However, on an annual basis, the decline moderated to 1.6%, a significant improvement from the previous year’s 3.8% drop.

Looking ahead, the Reserve Bank of New Zealand (RBNZ) has signaled its intention to maintain current interest rates throughout 2024, with no anticipated rate cuts until mid-2025. Despite acknowledging economic challenges, RBNZ policymakers have cautioned about potential upward risks to inflation. Market sentiment, reflected in bond futures, suggests a 44% probability that the RBNZ could consider easing monetary policy as early as October 2024, according to Reuters.

Overall, the NZD/USD pair’s movement reflects a combination of USD strength driven by Fed policy expectations and local economic data releases impacting New Zealand’s economic outlook and monetary policy stance.

CRUDE OIL – Crude Oil Rally Falters as Fed Signals Less Likelihood of Rate Cuts; WTI Drops Below $78

The Crudeoil prices are lowered after the FED makes no changes in the rates in this meeting. EIA reported 3.73 Million Barrels for the week end June 03 it is more than last week 1.53 Million Barrels stockpiles. US CPI data came at lower than expected as 3.4% from 3.6% in the April month.

XTIUSD Crude oil price is moving in the Descending channel and the market has reached the lower high area of the channel

Federal Reserve (Fed) Chairman Jerome Powell adopted a cautious stance on potential rate cuts, citing the ongoing need for substantial progress in inflation control before considering any adjustments. The Fed’s latest economic projections, known as the Summary of Economic Projections (SEP) or “dot plot,” scaled back expectations for rate cuts, forecasting only a modest quarter-point reduction in 2024 as per the median estimate.

Earlier in the day, the broader market sentiment turned bullish after the US Consumer Price Index (CPI) for May revealed a faster-than-expected cooling. Monthly headline CPI inflation stagnated at 0.0%, contrary to the anticipated decline to 0.1% from the prior 0.3%. Year-on-year Core CPI inflation also moderated to 3.4%, lower than the expected 3.5% and the previous month’s 3.6%. These figures initially fueled hopes of a September rate cut of at least 25 basis points, pushing market expectations above 70% during early US trading hours.

However, optimism was short-lived as the Energy Information Administration (EIA) reported an unexpected increase in US Crude Oil Stocks Change for the week ending June 7. Crude oil inventories rose by 3.73 million barrels, contrasting with forecasts of a 1.55 million-barrel decrease and adding to the previous week’s build of 1.233 million barrels.

The conflicting data points contributed to the fluctuating oil prices, highlighting the market’s sensitivity to economic indicators and central bank policies amid ongoing inflation concerns and supply dynamics.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!