ACC: ACC Surpasses Q4 Earnings Expectations; Emkay Maintains ‘Buy’, Motilal Oswal Forecasts Upside

The ACC reported beat esimates Net profit in Q4 earnings as Rs.942 cr and consolidated revenue is Rs.5409 cr. EBITDA Operational performance increased to 79.5 percent as Rs.837 cr YoY and margin expanded by 15.5% from 9.8% in the last quarter. This volume of operations done by Ambuja cements joint venture by ACC.

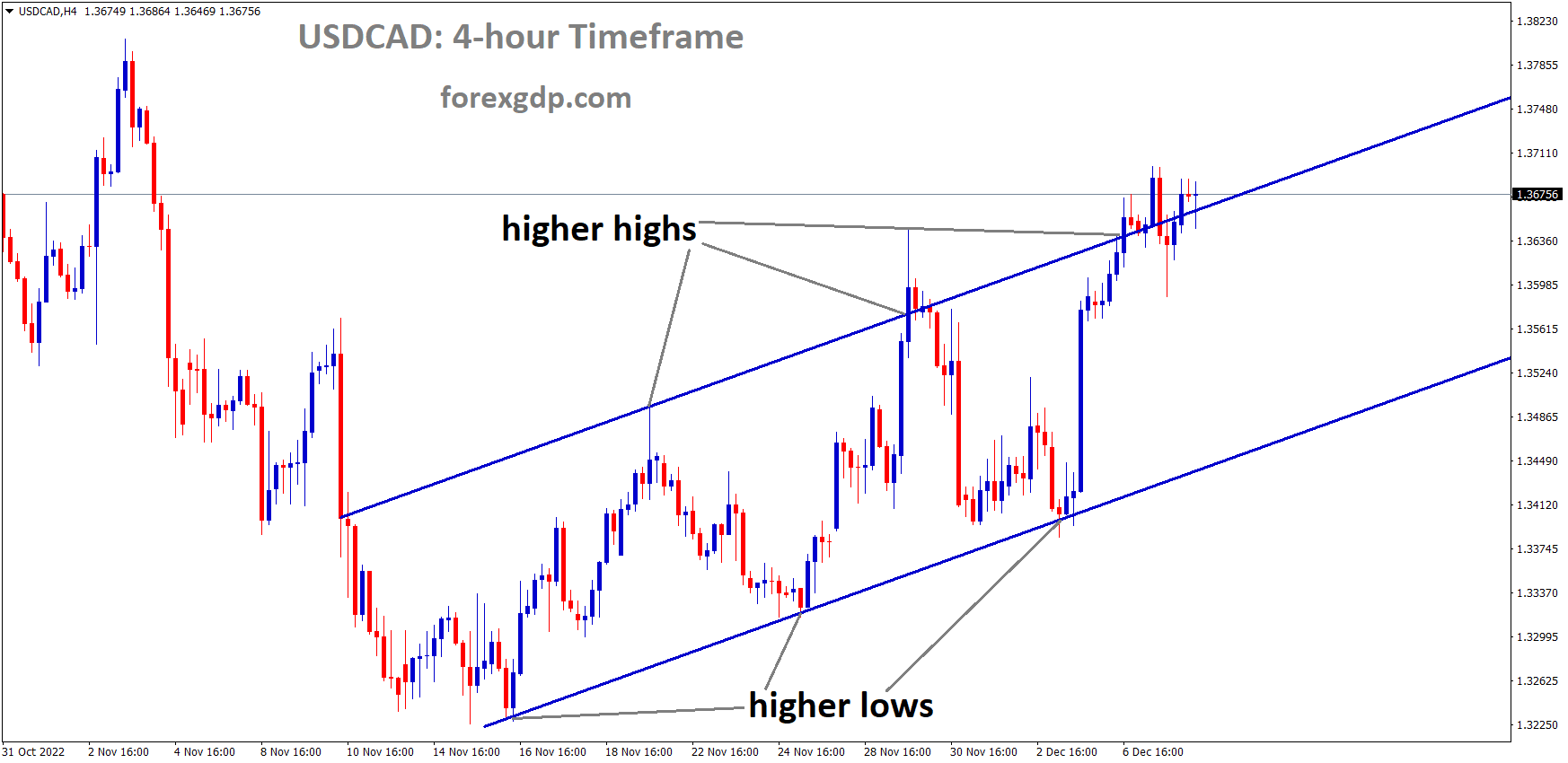

ACC Market Price is moving in Descending Triangle and market has reached lower high area of the pattern

On April 26, attention turned to shares of ACC following the company’s Q4 earnings report, which exceeded analysts’ expectations. For the quarter ending March 2024, ACC recorded a consolidated net profit of Rs 945 crore, marking a significant 300 percent increase compared to the same period last year. Consolidated revenue from operations also saw a notable uptick, rising by 12 percent to Rs 5,409 crore. This growth was attributed to higher sales volume and reduced operating expenses, compensating for lower-than-anticipated realization.

During the quarter, ACC’s consolidated sales volume surged to 10.4 million tonnes from 8.5 million tonnes a year ago. Moreover, for the full fiscal year 2024, sales volumes climbed to 36.9 million tonnes, up from 30.7 million tonnes in the previous fiscal.

Analysts at Motilal Oswal noted that ACC’s increased volume growth was propelled by a master supply agreement (MSA) with Ambuja Cements. They anticipate a clearer picture of ACC’s performance once Ambuja Cements’ consolidated numbers are available.

ACC’s operational performance also showed improvement, with Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) rising by 79.5 percent year-on-year to Rs 837 crore. Additionally, the EBITDA margin expanded by 570 basis points to 15.5 percent compared to 9.8 percent in the same period last year.

The management of ACC expressed optimism regarding the industry outlook, citing higher budgetary allocation to infrastructure, government initiatives for affordable housing, and an uptick in construction activities as factors expected to drive cement demand. The company aims to increase its green energy share to 60 percent by FY28, up from 9 percent in FY24.

Motilal Oswal maintained a ‘neutral’ rating on ACC, considering its reasonable valuations, and set a target price of Rs 2,600. Meanwhile, Emkay Global reiterated its bullish stance on the stock, factoring in the Q4FY24 performance and adjusting its EBITDA estimates. Emkay Global maintained a ‘buy’ rating with a target price of Rs 2,900 for March 2025.

In the previous trading session, ACC shares closed slightly higher at Rs 2,573.00 on the National Stock Exchange (NSE). Year-to-date, the stock has risen by 15 percent, outperforming the benchmark Nifty 50, which saw a 3.8 percent increase during the same period.

TECH MAHINDRA: Tech Mahindra’s Q4 Earnings Miss Leads to Brokerages Cutting Growth Targets

The Tech Mahindra reported Q4 earnings as Net profit rose to 29.5% as Rs.661 cr and Revenue fall down to 2% as Rs.12871 cr. Both values missed estimates by economists view. So Tech Mahindra has declining of order book in current stance due to higher rates sustaining in the US. IT Projects are lying down and more labour layoffs due to higher rates by the FED.

TECH MAHINDRA Market Price is moving in Ascending channel and market has rebounded from the higher low area of the channel

Tech Mahindra, an information services player, reported fiscal fourth-quarter earnings that fell short of estimates, prompting brokerages to revise down growth targets for the IT company.

The company’s net profit increased by 29.50 percent to Rs 661 crore, missing Moneycontrol’s estimate of Rs 709.47 crore. Meanwhile, revenue declined by 2 percent sequentially to Rs 12,871 crore, compared to estimates of Rs 12,926 crore.

A continued slowdown across key verticals, including telecom, communications, media, and entertainment, weighed on Tech Mahindra’s Q4 earnings.

Jefferies, a brokerage firm, anticipates weak near-term growth for Tech Mahindra due to the company’s weak order book and declines in headcount. Consequently, Jefferies lowered its growth estimates by 4-9 percent and margins for FY26/27. The brokerage also reduced its price target for the stock to Rs 1,065 while maintaining an “underperform” rating.

CLSA, another brokerage, noted weaknesses in Tech Mahindra’s earnings and adjusted its EBIT margin and EPS targets downward by 13 percent and 12 percent, respectively, for FY25 and FY26. Despite this, CLSA maintained a “buy” rating with a price target of Rs 1,589.

In response to the challenges, Tech Mahindra’s CEO and MD Mohit Joshi unveiled a three-year roadmap aimed at achieving better revenue growth than peer average and optimizing margin improvement by FY27. Joshi’s strategy for FY27 targets surpassing peers’ average growth and achieving a 15 percent EBIT margin.

HSBC, a brokerage, views the turnaround plan as sensible but highlights challenges in execution, particularly given the current macroeconomic backdrop. The brokerage emphasizes that margin expansion for Tech Mahindra is heavily dependent on pyramid improvement while maintaining average pricing, given the lackluster outlook for the sector. HSBC maintained a “hold” rating with a price target of Rs 1,300.

Nuvama, another brokerage, expresses caution regarding Tech Mahindra’s ambitious targets. While acknowledging that the targets are achievable, Nuvama warns of significant near-term challenges in implementing the necessary steps. The brokerage reduced its FY25/26 target by 2 percent/1.5 percent and maintains a “reduce” rating on the stock with a target of Rs 1,000.

UTI AMC: UTI AMC Jumps 6% to 52-Week High on Strong Q4 Results; InCred Raises Target Price

The UTI AMC reported Q4 earnings as robust growth as 90% increase in the Net profit to Rs.163cr and 38% increase in the Revenue as Rs.416cr. UTI did lower operational costs in this quarter made increases in the revenue of Q4.

UTI ASSET MNGMT Market Price has broken box pattern in upside

On the morning of April 26, shares of UTI Asset Management Company (AMC) experienced a notable surge of over 6 percent, reaching a fresh 52-week high of Rs 1,005.15. This surge followed the company’s release of robust financial results for the March quarter.

UTI AMC reported a substantial 90 percent year-on-year increase in profit, amounting to Rs 163 crore, alongside a significant 38 percent rise in revenue, totaling Rs 416 crore.

InCred Equities highlighted that the improving performance of UTI AMC schemes contributed to steady inflows and healthy Assets Under Management (AUM). Furthermore, the rationalization of operating expenses bolstered the company’s operating performance, creating a favorable risk-reward scenario.

In light of these developments, the brokerage retained its “add” rating on the stock and revised the target price upward to Rs 1,100 from Rs 1,050.

Nuvama Institutional Equities, however, offered a contrasting view, characterizing the quarter as weak for UTI AMC despite the strong Profit After Tax (PAT) and revenue figures. Notably, the company’s Equity Assets Under Management (AUM) grew by a mere 0.2 percent sequentially, lagging behind the industry’s robust equity inflows of Rs 94,200 crore.

Persistent weak fund performance led to net outflows from equity schemes during the reviewed quarter.

UTI AMC’s core operating earnings for the March quarter stood at Rs 130 crore, marking a notable 43.4 percent year-on-year increase. This growth was attributed to elevated employee and other expenses, driven by increased investments in personnel, subsidiaries, and expansion into foreign markets. Additionally, other expenses remained high due to larger payments to the Pension Fund Regulatory and Development Authority (PFRDA) and index service providers as ETF AUM increased.

Despite these challenges, UTI AMC maintains a 3.7 percent market share in equity AUM. Analysts at Nuvama anticipate that the company’s investments in international and retirement solutions businesses will provide further momentum.

However, UTI AMC faces the highest costs as a percentage of AUM compared to listed peers, primarily due to steep expenses in the non-officer category of employees. Nuvama emphasized that controlling costs is crucial for the realization of operating leverage.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!