AUD: China’s May CPI Inflation Steady at 0.3% YoY, Below 0.4% Forecast

China CPI inflation data for the month of May came at 0.30% YoY versus 0.40% is expected, -0.10% MoM came in the May month and 0.10% increase in the April month. China PPI index came at -1.4% versus -2.5% printed in the April month. Mixed bags of data moved higher for Australian Dollar against Counter pairs.

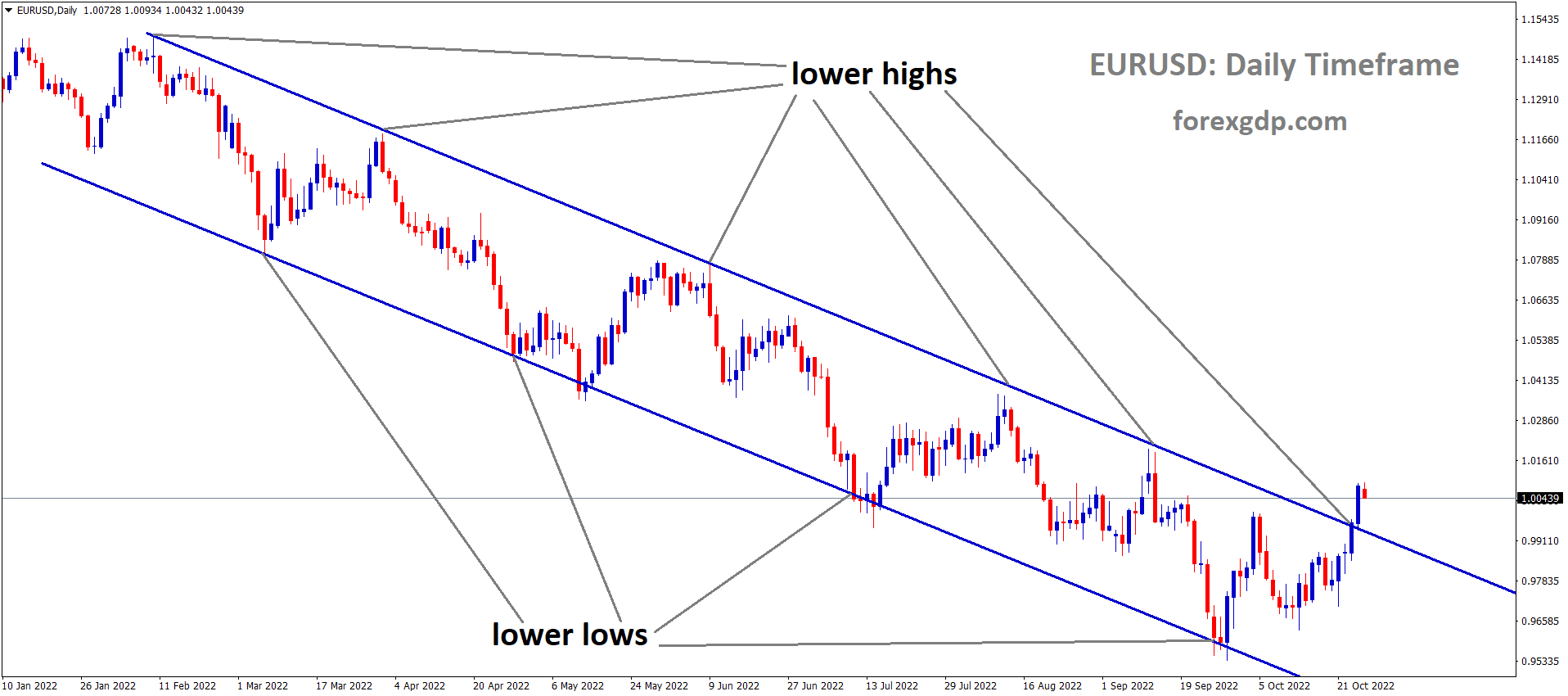

AUDUSD is moving in box pattern and market has reached support area of the pattern

In May, China’s Consumer Price Index (CPI) saw an annual increase of 0.3%, matching April’s growth rate but falling short of the anticipated 0.4%. On a month-to-month basis, the CPI registered a decline of 0.1%, contrary to the expected 0% change, and following a 0.1% increase in April.

In terms of the Producer Price Index (PPI), there was a 1.4% year-over-year drop in May, which is a smaller decline compared to the 2.5% decrease in April. This result was slightly better than the forecasted 1.5% decrease.

These figures suggest a continuing trend of weak inflation in China, which may reflect subdued domestic demand and other economic pressures. The lower-than-expected CPI growth and the smaller-than-expected decline in PPI could imply challenges for China’s economic policy aimed at stimulating growth.

AUD: China’s Steady Inflation Heightens Stimulus Pressure

Recent economic indicators from China revealed a Consumer Price Index (CPI) inflation rate for May that registered at 0.3% year-over-year, falling short of the anticipated 0.4%. On a month-to-month basis, the CPI declined by 0.1%, juxtaposed with a 0.1% increase in April. In a contrasting yet somewhat optimistic turn, the Producer Price Index (PPI) exhibited a year-over-year contraction of 1.4%, a marked improvement from the preceding month’s 2.5% decline.

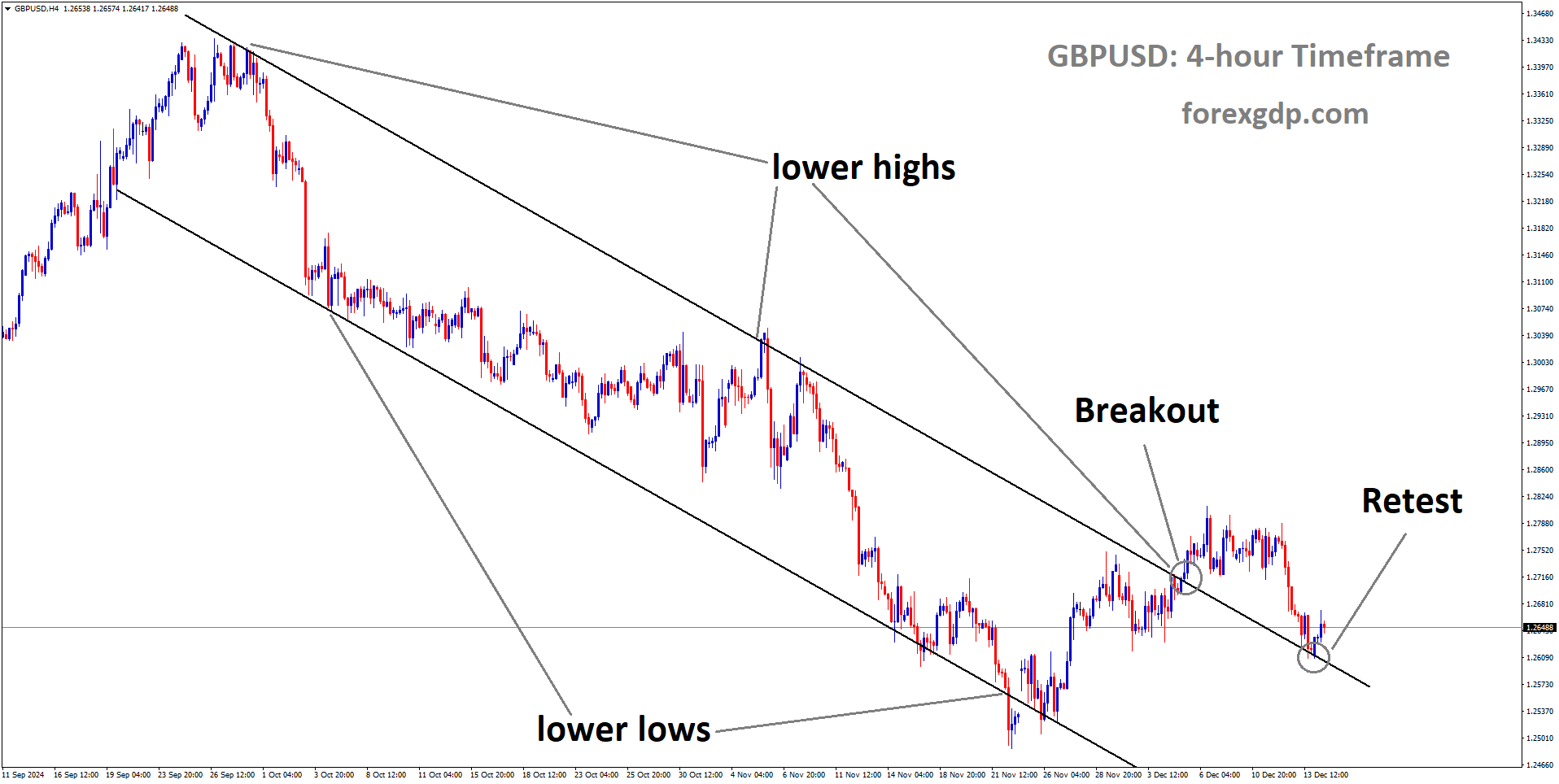

AUDCHF is moving in Ascending channel and market has reached higher low area of the channel

These disparate economic figures have had pronounced ramifications in the currency markets, notably propelling the Australian Dollar (AUD) upward against its peers. Several factors underpin this movement:

- Economic Interdependence: Australia’s economic fortunes are inextricably linked to China, particularly through the commodities trade. The enhanced industrial activity implied by the PPI data suggests a sustained demand for Australian exports, thereby bolstering the AUD.

- Market Sentiment: The juxtaposition of weak consumer inflation with robust industrial demand may have invigorated market sentiment towards risk. The AUD, being a currency that thrives on risk appetite, naturally benefited from this shift.

- Commodity Price Dynamics: An industrial resurgence in China presages increased demand for commodities, a significant portion of which are sourced from Australia. This anticipated upsurge in demand can drive commodity prices higher, providing further support to the AUD.

In essence, while the economic data from China presented a convoluted tableau, the favorable elements pertaining to industrial demand and recovery have collectively contributed to the Australian Dollar’s appreciation vis-à-vis other currencies.

China’s consumer inflation remained stable in May, with the CPI increasing by 0.3% year-over-year, consistent with April’s rate but below the anticipated 0.4% rise. The month-on-month CPI dipped by 0.1%, contrasting with a 0.1% increase in April and missing the zero growth expected by economists. The Producer Price Index (PPI) decline moderated to 1.4% year-over-year from April’s 2.5% drop, slightly better than the forecasted 1.5% decrease.

Despite these numbers, underlying trends suggest that China’s economic recovery is uneven and domestic demand remains weak. This is largely attributed to low consumer confidence and the ongoing property sector crisis. Multiple rounds of support measures have not significantly bolstered consumption, indicating the need for stronger and more coordinated fiscal and monetary interventions.

Economists, including Zhiwei Zhang of Pinpoint Asset Management, emphasize that the modest improvement in PPI is driven more by rising commodity prices, such as copper and gold, rather than robust domestic demand. The weak month-on-month CPI and persistent deflationary pressures reflect ongoing challenges.

Investment sentiments were tepid, with Asian shares and China’s blue-chip index seeing slight declines following the release of the inflation data. Zhou Hao, chief economist at Guotai Junan International, noted that while a moderate reflation is ongoing, low inflation remains the base scenario.

China’s economy has struggled to gain momentum despite the easing of stringent COVID-19 measures at the end of 2022, primarily due to the prolonged property sector crisis impacting overall confidence. Beijing has implemented measures to stimulate demand, including incentives for the housing sector and consumer goods, as well as job creation linked to major projects.

Core inflation, which excludes food and energy prices, slowed to 0.6% in May from 0.7% in April, highlighting the difficulty in boosting domestic demand. Economists like Zichun Huang from Capital Economics predict consumer inflation will remain modest, averaging around 0.5% for the year due to persistent industrial overcapacity.

To achieve its GDP growth target of around 5% for the year and ensure a sustainable rebound, many economists argue that Beijing will need to introduce a comprehensive fiscal and monetary policy package. This would help restore confidence and stimulate spending among households and businesses. Recent measures to stabilize the property sector have been perceived as insufficient, underscoring the necessity for a more proactive and comprehensive policy approach .

AUD: China’s May CPI Inflation Disappoints, PPI Decline Slows

The recent economic data from China showed that the Consumer Price Index (CPI) inflation for May increased by 0.3% year-over-year, which was below the expected 0.4%. Month-over-month, the CPI saw a decrease of 0.1%, following a 0.1% increase in April. In contrast, the Producer Price Index (PPI) showed a decline of 1.4% year-over-year, which was an improvement from the 2.5% drop in April.

AUDCAD is moving in box pattern and market has rebounded from the support area of the pattern

This mixed economic data from China has had notable effects on the currency markets. Specifically, the Australian Dollar (AUD) gained strength against its counterparts. This movement can be attributed to several factors:

- China’s Economic Health: Australia is highly dependent on trade with China, particularly in commodities. Improved industrial activity, as indicated by the better-than-expected PPI data, suggests continued demand for Australian exports, which supports the AUD.

- Risk Sentiment: The mixed economic signals from China, showing some improvement in industrial demand despite weak consumer inflation, could have boosted risk sentiment. The AUD often benefits in such scenarios due to its status as a risk-sensitive currency.

- Commodity Prices: A recovery in China’s industrial sector can lead to higher demand for commodities, many of which are exported by Australia. This prospect can drive up the prices of these commodities, further supporting the AUD.

Overall, while China’s economic data presented a mixed picture, the positive aspects regarding industrial recovery and demand have contributed to the Australian Dollar’s appreciation against other currencies.

In May, China’s Consumer Price Index (CPI) increased by 0.3% year-over-year, falling short of the anticipated 0.4% rise and maintaining the same pace as April. Month-on-month, the CPI experienced a 0.1% decline, contrary to expectations of no change. This subdued performance in consumer inflation reflects ongoing weak consumer spending amid an uncertain economic recovery, as consumers have significantly reduced discretionary spending due to persistent economic concerns.

However, the Producer Price Index (PPI) showed signs of improvement, contracting by 1.4% year-over-year, which was better than the expected 1.5% decline and a marked improvement from the 2.5% decrease in April. This indicates a slower pace of deflation and suggests a sustained recovery in the industrial sector, driven by robust overseas demand and consistent policy support from Beijing.

China’s industrial sector has shown steady improvement in recent months, which is reflected in the better-than-expected PPI figures. This sector’s recovery is attributed to continued stimulus measures and strong foreign demand, despite broader economic challenges.

The overall economic outlook remains mixed due to the contrasting performance between the industrial sector and consumer spending. While the industrial sector’s recovery is encouraging, the ongoing weakness in consumer spending highlights the challenges facing the world’s second-largest economy. Sustained policy efforts from Beijing will be crucial to boosting domestic demand and ensuring a balanced economic recovery.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!