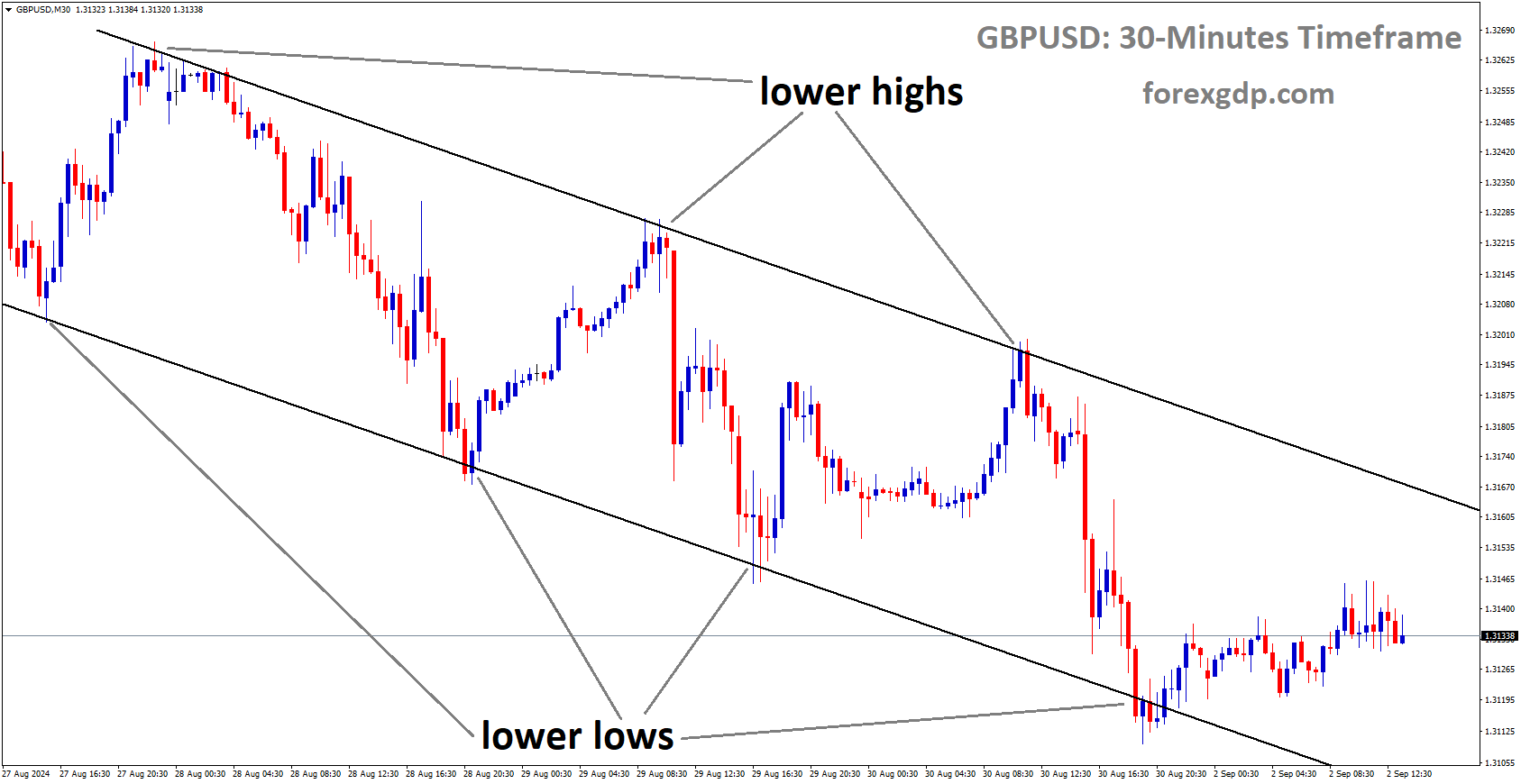

USDCAD has broken the Ascending channel in downside

The Bank of Canada is inclined to maintain the interest rates at 5.00% in the upcoming week. The Governor of the Bank of Canada has emphasized the need for stable rates to curb inflationary pressures in the economy. The decline in Canada’s GDP in Q3 suggests that the previous rate hike represents the peak in interest rates for the country. Peak interest rates tend to have a suppressing effect on both job demand and business activity.

The economic landscape of Canada is undergoing significant shifts, prompting a careful examination of interest rate trends. Economists polled by Reuters suggest that the Bank of Canada is on the brink of initiating interest rate cuts in response to slowing inflation and economic growth. This comprehensive analysis delves into the current economic scenario, economist consensus, predictions of rate cuts, and the far-reaching implications on sectors such as the housing market.

Current Economic Scenario:

The sentiments expressed by BoC Governor Tiff Macklem underscore the nuanced considerations shaping monetary policy. While acknowledging the absence of excess demand and anticipating weak growth, Macklem has yet to signal a readiness to consider interest rate cuts. In the last quarter, the Canadian economy was projected to grow at a modest 0.2% annualized rate, a rebound from a 0.2% contraction in April-June. However, the more notable development is the decrease in inflation, which has subsided from its peak of 8.1% in June 2022 to 3.1% in the last month.

These dynamics suggest a delicate balance between mitigating inflationary pressures and supporting economic growth. Macklem’s cautious approach reflects the uncertainties and challenges that lie ahead for the Canadian economy.

Economist Consensus:

A Reuters poll conducted from November 27-30 provides insights into the collective views of economists regarding the BoC’s future policy decisions. The consensus among 26 economists is that the BoC will likely maintain its main policy rate at 5.0% until at least the end of March, aligning with expectations from the U.S. Federal Reserve. Notably, only Barclays deviates from this consensus, anticipating a 25 basis point rate hike in January.

However, the poll reveals an interesting divergence between economist predictions and market expectations. Interest rate futures are pricing in the possibility of a rate cut as early as March, challenging the prevailing consensus. This disparity suggests a certain level of uncertainty and highlights the complexity of forecasting in an ever-changing economic landscape.

Rate Cut Predictions and Implications:

The crux of the matter lies in the forecasted interest rate cuts, with economists predicting a commencement in the second quarter. The median projection suggests a substantial 100 basis points of rate cuts in the coming year, surpassing the 75 basis points expected from the U.S. Federal Reserve. This prediction indicates a significant departure from the previously hawkish stance of the BoC.

EURCAD is moving in the Box pattern and the market has rebounded from the support area of the pattern

Approximately 70% of economists, numbering 18 out of 26, anticipate the policy rate to reach 4.0% or lower by the end of 2024. This stands in stark contrast to the expected fed funds rate, projected to be in the range of 4.50-4.75%. The consensus suggests that the BoC is gearing up to transition from its hiking cycle, indicating a belief among economists that the current policy has fulfilled its objectives and needs adjustment to align with a more normalized monetary policy setting.

Housing Market and Economic Impact:

The ripples of potential interest rate cuts extend to the housing market, a crucial component of the Canadian economy. A separate poll of 11 property analysts conducted from November 15-30 paints a nuanced picture of the future. The analysts forecast a stagnation in average home prices in 2024, following a decline of 3.3% in the current year. This projection is notably different from the optimism expressed in an August poll, which predicted a 2.0% rise in 2024.

Despite government measures announced in the latest Fall Economic Statement to boost housing supply and assist lenders dealing with homeowners at risk, concerns persist regarding the adequacy of new supply. The anticipation of interest rate cuts adds a layer of complexity to the housing market dynamics. With nearly 60% of mortgage holders yet to renew their home loans at higher rates, the market is poised for potential shifts.

Interest Rate Hike Cycle:

To comprehend the significance of the current discussions around interest rates, it is essential to revisit the recent past. The Bank of Canada commenced its interest rate hikes in April 2022. However, what makes this cycle particularly noteworthy is the aggressive nature of rate increases. Rates were propelled from 0.25% in March 2022 to 5% in July 2023, representing a considerable escalation over a relatively short timeframe.

GBPCAD is moving in the Box pattern and the market has rebounded from the support area of the pattern

This abrupt ascent in interest rates had substantial consequences. Mortgage interest payments soared, impacting all companies with large debts. The effect was not confined to financial statements; stock prices of these companies witnessed a decline as rising interest expenses became a financial burden. In response, some companies chose to prioritize mortgage payments over dividends, further influencing investor sentiments.

While higher interest rates resulted in increased income for banks, they also introduced elevated credit risk. The prevailing fear overshadowed optimism, leading to a downturn in bank and lending stocks throughout the rate hike cycle. The scenario played out as a cautionary tale, demonstrating how a significant portion of income diverted towards debt payments could have a cascading effect on consumer demand and various sectors, including discretionary items like automobiles.

Post-Hike Economic Shift:

The narrative took a turn as Canada’s inflation eased to 3.1% in October, prompting the Bank of Canada to pause further interest rate hikes since July. The rate remained unchanged at 5%, indicating a strategic reevaluation of monetary policy. With inflation showing signs of moderation, the central bank’s focus shifted from aggressive tightening to a more nuanced approach.

CADJPY is moving in the Descending triangle pattern and the market has rebounded from the support area of the pattern

The numbers and indicators hint at a potential shift towards interest rate cuts in early 2024. The upcoming Monetary Policy Committee meeting on December 6 is anticipated to provide further clarity on the central bank’s stance. Smart investors are eyeing this period for potential opportunities, expecting a positive momentum in early December.

Interest Rate Dynamics in Canada:

Understanding the current interest rate dynamics requires a closer look at the numbers. As of now, the Bank of Canada aims to maintain the interest rate at a neutral level. The current interest rate in Canada stands at 7.2%, a figure that significantly influences daily life and working individuals. The projection for 2024 is a rate of 4.5%, suggesting a deliberate move towards a more balanced monetary policy.

The expected rate cuts in early 2024 are viewed optimistically by investors, prompting strategic stock purchases. The prospect of a more accommodative monetary policy aligns with the broader economic narrative, signaling potential benefits for sectors that were adversely affected during the aggressive interest rate hike cycle.

Factors Influencing Canadian Interest Rates:

The intricacies of Canadian interest rates are shaped by a multitude of factors, each playing a role in the nuanced decisions made by the Bank of Canada. The central bank revises interest rates based on considerations such as inflation, prevailing market conditions, and changes in policies. The impact varies across different types of loans, including car loans, home loans, and mortgages, with lower interest rates proving advantageous for borrowers.

It is crucial to recognize the role of government regulations in shaping the final function of interest rates across banks and financial institutions in Canada. The regulatory framework provides a guiding structure, ensuring that interest rates align with broader economic goals while addressing the specific needs of borrowers and lenders.

Conclusion:

In conclusion, the economic landscape in Canada is undergoing a transformative phase, with the Bank of Canada poised to make pivotal decisions regarding interest rates. The delicate balance between controlling inflation and supporting economic growth is at the forefront of policy considerations. The consensus among economists points towards a shift from the aggressive interest rate hike cycle to a more accommodative stance, with predictions of rate cuts in early 2024.

AUDCAD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The implications of these potential rate cuts extend beyond the realm of monetary policy, touching sectors such as the housing market and influencing investor behavior. Understanding the factors shaping Canadian interest rates is essential for individuals, businesses, and policymakers alike. As the economic narrative unfolds, strategic insights into interest rate dynamics will play a crucial role in navigating the evolving landscape.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/