The Cipla company posted Netprofit 93% up as Rs.939 cr and exceeded Rs.891 cr analysts estimate.The Revenue is grew by 13% as Rs.6163 Cr in the Jan- March Quarter 2024. This revenue is missed analysts expected of Rs.6224 cr.The Cipla US Revenue rose to 11% as $221 Million. The EBITA margin came at 21.4% versus 22% expected, R&D Development research funds allocated as 7.2% of its Revenue nearly Rs.444 cr.

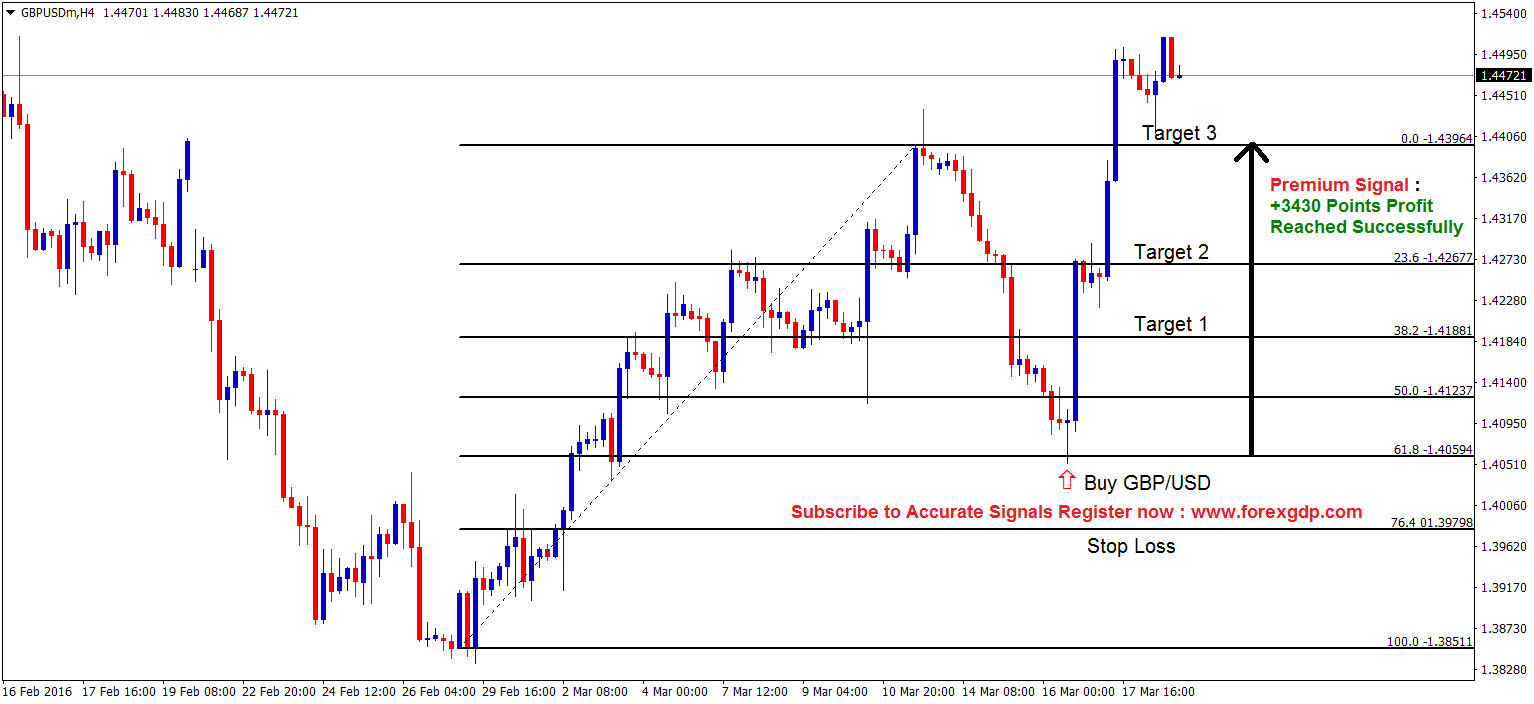

CIPLA Market price is moving in Ascending channel and market has reached higher low area of the channel

Cipla’s Shares Dip by Nearly 3% After Q4 Results Fall Below Expectations

On May 10, shares of Cipla witnessed a downturn of almost 3% following the announcement of its fiscal year 2024 Q4 results, which failed to meet market expectations. By 2:56 pm, Cipla’s shares were trading at Rs 1,342.25 on the NSE.

Despite a notable 79% increase in net profit to Rs 939 crore compared to the previous year, exceeding Moneycontrol’s estimated Rs 891 crore, the company’s revenue and margin figures fell short. This substantial profit surge was primarily attributed to a low base effect, with the previous year’s net profit being impacted by one-time impairment charges of Rs 182.42 crore.

However, revenue only grew by 13% year-on-year to Rs 6,163 crore, missing the expected Rs 6,224 crore mark. This was partly due to the divestment of Cipla’s Uganda-based subsidiary QCIL in the preceding quarter. Additionally, the company’s India business experienced slower growth than anticipated, with sales reporting a modest 7% year-on-year increase, attributed to soft seasonal demand in the consumer segment, contrary to analyst projections of double-digit growth.

On the positive side, Cipla’s US business continued to demonstrate robust growth, with sales climbing by 11% to $226 million, driven by sustained expansion in key differentiated assets and the base portfolio.

While the EBITDA margin expanded marginally by 54 basis points to 21.4%, it fell short of the 22% target set by management due to increased research and development expenditures. Research and development spending during the quarter rose by 11% year-on-year to Rs 444 crore, equivalent to 7.2% of total revenue.

Cipla is actively pursuing innovation in the respiratory segment, having filed for five assets, including generics of Symbicort and Qvar, with anticipated launches over the next three years. Additionally, the company aims to submit two more respiratory assets within the next 12-15 months.

In the peptides and complex generics category, Cipla has filed for 12 assets, aiming for launches within a timeline of 2-4 years. Furthermore, the company plans to introduce four peptide assets during fiscal year 2025.

Hindustan Zinc: “Hindustan Zinc Stock Jumps 19% to 52-Week High on Upbeat China Data Boosting Zinc Prices”

The China Government has increased the prices of Zinc, it was impacted in Hindustan Zinc company revenue to Rs.7549 cr and surpassed the estimates of 48.3%. Dividend Rs.10 per share announced by Board worth Rs.4225.32 cr. The Company net debt Rs.370 cr is fully covered by Rs.1700 cr positive cash flow in the Company. The Company capital expenditure now fall to $270-$350 Million in the coming quarter.

HINDUSTAN ZINC Market price has broken Ascending channel in upside

Hindustan Zinc Shares Skyrocket by Almost 19% to Reach 52-Week High Amid Surge in Zinc Prices

On May 10, Hindustan Zinc shares experienced a remarkable surge of nearly 19%, hitting a peak of Rs 540.95 per share, marking a 52-week high. This substantial increase was propelled by a notable upswing in zinc prices. The price of zinc on the London Metal Exchange witnessed a surge of over 2%, reaching $2,955, primarily driven by positive trade data from China. The data showcased growth in both imports and exports for the month of April.

By the closing bell, shares of Hindustan Zinc had soared by 16% to settle at Rs 529 apiece on the NSE. The optimistic trade figures from China not only indicated a revival in domestic and international demand but also signaled a favorable environment for zinc prices. Given that China is a significant consumer and producer of zinc, any positive indications from its economy tend to impact zinc prices positively.

The surge in zinc prices augurs well for Hindustan Zinc, as the company is actively involved in the mining and refining of the metal. Additionally, in a move to reward its shareholders, the company announced an interim dividend of Rs 10 per equity share, amounting to a total payout of Rs 4,225.32 crore.

In its financial performance for the March quarter, Hindustan Zinc reported robust revenue of Rs 7,549 crore, with margins surpassing estimates at 48.3%. Notably, the company achieved a significant financial milestone by transitioning from a net debt position of Rs 370 crore in the December quarter to a net cash position of Rs 1,700 crore by the end of the March quarter.

Looking ahead, the management of Hindustan Zinc outlined ambitious projections for increased production of both mined metal and refined metal in fiscal year 2025 compared to fiscal year 2024. Furthermore, the company anticipates project capital expenditure for the year to fall within the range of $270 million to $325 million, signaling its commitment to further growth and expansion initiatives.

SBIN: “SBI’s Strong Q4 Performance Applauded by Brokerages Despite Valuation Concerns”

The SBI reported Q4 net profit as 24% up and Rs.20698 cr, Net interest rose to 3% as Rs.41656 cr and Net NPA decreased to 0.57% from 0.67%, Gross NPA Stood at 2.24% from 2.72% last quarter. The wage for workers revision to Rs.670 cr from the Rs.5400 cr expenses, this is the bigger impact for increasing the profit Rs.10000-14000 cr to Rs.20698 cr.

SBIN Market price is moving in Ascending channel and market has reached higher high area of the channel

Brokerages Maintain Positive Outlook on SBI’s Strong Q4 Performance

India’s leading lender, State Bank of India (SBI), pleasantly surprised investors with its exceptional performance in the January-March quarter (Q4FY24), driven by lower staff costs and increased treasury gains. Despite this commendable showing, analysts are divided on the potential for a re-rating of the stock due to its premium valuations.

Kotak Institutional Equities reiterated a ‘buy’ recommendation on SBI and revised its target price upwards to Rs 950 from Rs 850, implying a significant upside of 16% from the current levels. However, they caution against expecting strong outperformance as the stock is currently trading at rich valuations.

“SBI has consistently exceeded expectations each quarter. In Q4, robust revenue growth and lower provisions contributed to impressive earnings,” noted analysts in a post-result review.

Nomura also maintained a ‘buy’ rating on SBI and raised its target price to Rs 1,000 per share from Rs 825. The brokerage firm attributed the lower-than-expected operating expenses to reduced provisions for wage revisions.

SBI’s Q4 witnessed a wage revision provision of only Rs 670 crore, substantially lower than the management’s guidance of Rs 5,400 crore.

Meanwhile, the lender reported a 24% year-on-year increase in net profit to Rs 20,698 crore in Q4FY24, surpassing analysts’ estimates by a wide margin. Similarly, its net interest income (NII) rose by 3% year-on-year to Rs 41,656 crore.

Despite a 37 basis points (bps) contraction in net interest margin (NIM) to 3.47% year-on-year due to rising cost of funds, the bank’s margin expanded by 8 bps sequentially.

Emkay Global analysts anticipate a gradual improvement in margins, supported by a healthy Loan-Deposit Ratio (LDR), a better portfolio mix, and controlled cost of funds. They reaffirmed a ‘buy’ rating on SBI and raised the target price to Rs 950 per share from Rs 750.

The management expressed confidence in maintaining stable margins in the coming quarters, citing the plateauing of deposit repricing.

SBI’s asset quality remained robust in the March quarter, with gross non-performing assets (GNPA) at 2.24% and net NPA at 0.57%, down from 2.78% and 0.67%, respectively, in the previous year.

With a favorable Loan-Deposit Ratio (LDR) and stable asset quality, Nuvama analysts anticipate SBI to outperform in the future. “Given the solid asset quality and potential upside from new investment norms and strategic divestments, we reiterate a ‘buy’ rating on SBI and raise the target price to Rs 950,” the brokerage stated.

Year-to-date, SBI shares have surged by over 27%, outperforming the benchmark Nifty 50 index’s modest 1% increase during the same period.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!