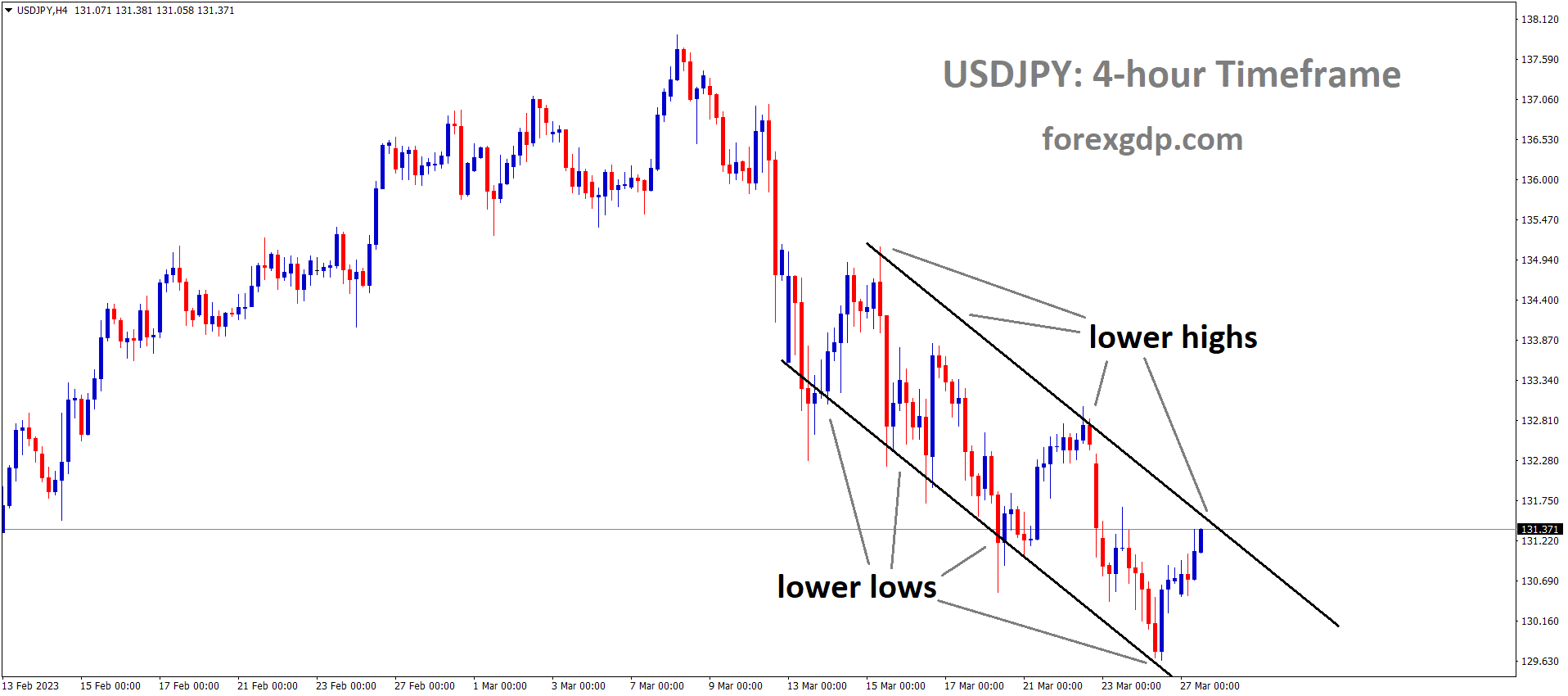

USDJPY Analysis

USDJPY is moving in the Descending channel and the market has reached the lower high area of the channel.

As a result of the US Dollar’s continued decline in the markets, the Japanese Yen is stronger. With the Japanese CPI coming in at a higher 3.3%, which is at a 40-year high, the incoming governor of the Bank of Japan, Ueda Kazuo, may decide to contain inflation in a different way.

This week’s scheduled data includes the US GDP, Japanese unemployment, retail sales, and industrial output.

The US dollar has been broadly declining over the past week following the US Federal Reserve’s announcement of its monetary policy. The Japanese yen has benefited significantly from this decline, and the US currency is likely to continue to dominate the USDJPY exchange rate in the days ahead, despite the possibility of some additional domestic Japanese drivers. This indicates that further relative Yen strength is very possible, even if it isn’t as significant as it has been due to market exhaustion. After all, the pair has been consistently declining since October 2022 in reaction to the outlook for monetary policy, as is evident on its daily chart. On March 22, the Fed increased interest rates once more, but a clear modification to its forward-guidance language has markets increasing their bets that borrowing costs won’t rise significantly further in the largest economy in the world and that the terminal rate will top out considerably below the 5.7% market expectations from just a few weeks ago. Markets are confident that the Fed funds goal range of 4.75%-5% will rise in the future. The general opinion appears to be “not much higher.

The dollar has weakened overall as a result of this viewpoint, and while this may be a rational market reaction, it’s crucial to keep in mind that the Fed’s primary mandate is to fight inflation, so as long as pricing power is strong, further rate increases will likely still be in the cards regardless of what the markets may wish. Nobody at the Fed anticipates a decline in interest rates in 2023. Headline Official data show that Japanese inflation last month slightly decreased. The Consumer Price Index increased by 3.3%, which is 0.3% less than in January. The ‘core’ readings, which take out the volatile effects of food and fuel costs, offered policymakers much less solace. One measure of inflation reached fourty-year highs as it stayed obstinately strong. When he succeeds the long-serving Haruhiko Kuroda on April 8, Ueda Kazuo, the next Governor of the Bank of Japan, will have to deal with this. Even though the new Governor is only likely to tweak the long-standing and aggressive monetary easing policy of the central bank, that could still give the Japanese Yen more internal support than it has been accustomed to for many years.

But those are issues that are more immediate. The upcoming week will likely offer trading opportunities centred on important data points. The final analysis of the fourth-quarter US Gross Domestic Product figures for 2022 is the first probable candidate. On Thursday, that will be discussed, and the previously reported 3.2% increase will be scrutinised. Numbers for Japan’s retail sales, industrial output, and unemployment are released on the same day. China’s March manufacturing PMI will provide a snapshot of how the second-largest economy in the world is recovering from harsh Covid lockdowns, which is a major concern for Japan’s sizable export industry. The effect of all of these on USD/JPY is most likely to last only a brief time, though, as monetary policy differences continue to dominate the market.

GOLD Analysis

XAUUSD Gold price is moving in the Descending channel and the market has reached the lower high area of the channel.

Due to worries about liquidity and the need to prevent major default banks from providing liquidity measures, the US FED has put a stop to further rate hikes, but gold prices have not decreased.

Once global banks start to halt rate increases, non-yielding assets like gold continue to rise in value.

Although the metal is still near to one-year highs and the alluring $2000/ounce region, gold prices have slightly decreased in Friday’s European trading as this market, like all others, awaits the United States Federal Reserve’s announcement of its monetary policy for the coming week. On Wednesday, the US central bank increased interest rates once more while significantly reducing its “forward guidance.” Further interest rate rises would not likely surprise the financial markets, but the Fed has stoked expectations that the “terminal rate” may be very near. For gold bulls, a stable interest rate environment—or even the possibility that rates may decline—creates a much better climate because gold, of course, offers no yield. When yields elsewhere are lower, particularly in the bond market, such assets frequently prosper. It now appears probable that US interest rates will peak out much lower than the 5.7% level that markets were anticipating when this month started.

SILVER Analysis

XAGUSD Silver Price is moving in an Ascending channel and the market has reached the higher low area of the channel.

The Fed did make it clear that it won’t be considering a rate reduction in 2023, which may have helped to temper the gold market’s apparent post-hike enthusiasm. It’s important to note that inflation in the US and around the globe continues to be significantly higher than central bank targets. By increasing its own borrowing rates on Thursday, the Bank of England highlighted this point. Rate reduction discussions will always smack of optimistic thinking while prices are high. The requirements for central bank price regulation are very specific and stringent. However, the ongoing war in Ukraine and the increased pressures on the banking industry appear to guarantee that haven assets will continue to be in demand. The oldest safe haven of them all, gold, has experienced an impressive rise in price since November 2022 that has brought prices back to levels last seen in March of that same year.

Prices are still in the wide uptrend channel that has helped the market recover from its lows in November of last year. However, the increase since the low of $1804.91 on March 8 has been very quick, and it appears probable that the psychologically significant $2000/ounce level will trigger a selloff. In light of this, it is fair to anticipate some consolidation into the week and month’s end before the bulls even consider preparing for a shot at the channel top. In any event, at $2045.19, that is still significantly above the current market and represents a very high point for the gold market. Keep in mind that the apogee was $2078 in 2022.

Support for the retracement is expected to be found at $1913.87, with additional minor support located above it in the $1965–$1975 range. Another support could come from the $1952 high from early February.

USDCAD Analysis

USDCAD has broken the Descending triangle pattern upside and retest the broken area of the pattern.

The Canadian economy’s retail sales data for the month of February came in at a strong reading of 1.4% higher than the 0.70% anticipated.

According to this reading, consumers are spending more money on goods in anticipation of the Bank of Canada’s tightening of financial circumstances.

The BoC may raise rates at its upcoming meeting in an effort to curb customer spending power and keep inflation under control.

In the Asian session, the USDCAD pair printed a new day bottom of 1.3725. The US Dollar Index’s muted performance and growing expectations for a restart of the Bank of Canada’s policy-tightening phase following the publication of strong Canadian Retail Sales data support the downward movement in the Loonie asset. S&P500 futures have made significant gains during the Asian session as market participants have grown more confident as US authorities contemplate expanding the emergency lending programme. The street is cheering the anticipated end to the Federal Reserve’s policy-tightening phase, but the US Dollar Index is failing to gain ground. (Fed). The USD Index is holding onto the 103.00 level, but it appears that the downside is more likely.

Expectations for a halt to the Fed’s rate-hiking cycle are intensifying as US banks’ lending standards tighten as a result of the unrest. Banks are taking more security measures when distributing loans. It appears that financial organisations have suffered greatly as a result of a bloody battle against persistent inflation. Positive Retail Sales statistics have increased the likelihood that the Bank of Canada will resume its policy-tightening rampage on the front of the Canadian Dollar. The BoC stopped raising rates at the beginning of the year because it believed the existing monetary policy was restrictive enough to keep inflation under control. In contrast to previously reported flat performance and the consensus estimate of 0.7%, monthly Canadian retail sales increased to 1.4%. Strong demand from Canadian consumers may compel businesses to raise their rates for the products and services they provide, necessitating further rate increases by the BoC. The price of oil is fluctuating in a constrained band above $69.00. The black gold is gaining traction for expanding the upside as more penalties against Russia become likely. Vladimir Putin, the president of Russia, has informed the Belarusian planning facilities for tactical nuclear weaponry of his intentions.

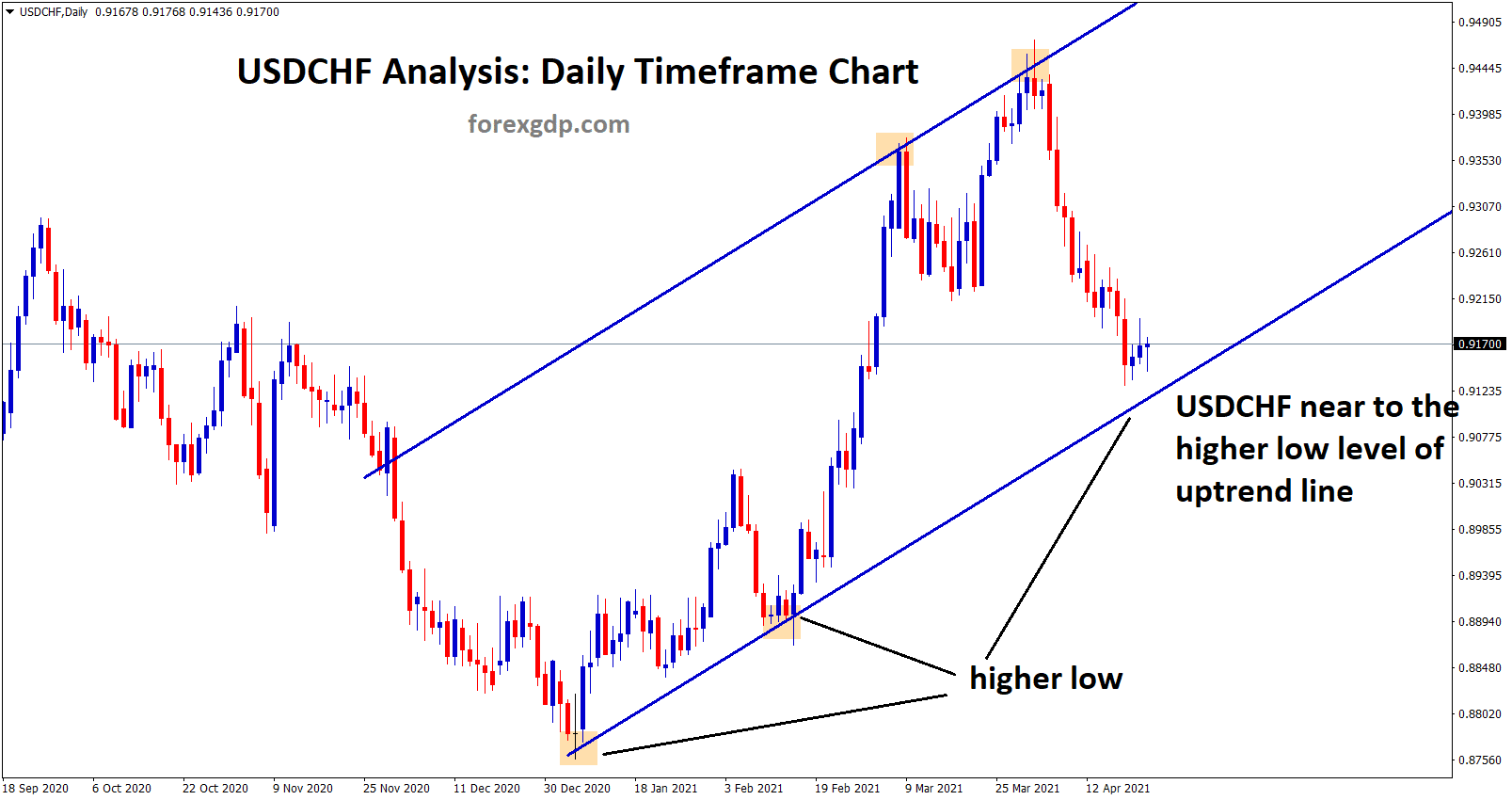

USDCHF Analysis

USDCHF is moving in the Symmetrical triangle pattern and the market has rebounded from the bottom area of the pattern.

The USDCHF found support and bounced back from the lower area as a result of quick actions taken by the US FED to contain the defaults of Major US Banks and SNB measures on Credit Suisse.

Following SVB, Swiss Credit Suisse, and now worries of a credit default swap-related bankruptcy at Deutsche Bank, Friday’s market volatility increased.

A series of banks have defaulted, starting with US banks, going on to Swiss banks, and now moving into the European region.

Finding support, the USDCHF’s decline to the downside was stopped at the 0.9125 mark. Due to the fallout from a regional bank and the contagion effect that spread to Europe, financial circumstances in the US started to ease. The market experienced a rollercoaster last week as a result of worries about Credit Suisse and an unexpected increase in Deutsche Bank’s credit default swap. However, prompt actions and a strong desire on the part of US authorities to save the banking sector helped USD/CHF end last Friday on the positive side.

Although this is the case, the pair’s downside bias is still present, and any convincing breach below the 0.9125 level will probably open the door for the multi-test support line at 0.9068 on the daily time frame. The 50-Day Moving Average (DMA), which is presently positioned near Wednesday’s high at the 0.9250 level, will probably continue to act as a ceiling on the upside. The pair will probably come up against the 21-DMA on a convincing break above this level, and breaching above both DMAs will take USD/CHF towards the two-week high at 0.9333. The 0.9446 level, which is also a multi-month high, is the last level of support for buyers. Lower lows are indicated by the Relative Strength Index, indicating that the combination has more downside potential. The US dollar will likely take its cues from these events, so attention will be focused on Russia’s placement of nuclear weapons in Belarus, this week’s Personal Consumption Expenditure (PCE) report from the US, and any additional developments regarding the liquidity of the world’s banks.

USD Index Analysis

US Dollar index has broken the Descending channel in Upside.

Due to concerns in the banking sector and tight financial circumstances, the US dollar is under pressure.

As a result of First Citizen Bank’s acquisition of SVB Financials, the markets are tranquil.

On March 27, 2023, 17 old SVB Branches will reportedly reopen as First Citizen Bank, according to the Federal Deposit Insurance Corporation.

After a selloff at the end of last week, the US dollar weakened once more today as markets continued to evaluate the banking sector’s uncertainty. According to reports, First Citizen Bank and SVB Financial have reached an agreement. The 17 former branches of Silicon Valley Bridge Bank, National Association will reopen as First-Citizens Bank & Trust Company on Monday, March 27, 2023, according to the statement on the Federal Deposit Insurance Corporation website. The market will be watching Deutsche Bank’s share price today after it took a beating on Friday amid worries that they, too, could be susceptible to tightening financial conditions. The news may help to allay some concerns.

The majority of the Treasury yield curve has seen little movement since Friday’s push downward. The benchmark 2-year note is currently yielding close to 3.80%, down from nearly 5.10% a few weeks back. It’s important to remember that at this time last year, it was below 2.40%. The 1-year bond was able to gain a few basis points today despite market uncertainty regarding the Fed’s rate course. The DXY index seems to have been weakened by the general decline in Treasury yields. Neel Kashkari, president of the Minneapolis Federal Reserve, stated over the weekend that the Fed is carefully monitoring the possibility of a credit crunch slowing the economy. After a few wild weeks, petroleum oil has had a calm start to the week, with the WTI futures contract hovering around US$ 69 bbl and the Brent contract hovering around US$ 75 bbl at the time of publication.

Early on, spot gold appeared below USD 1,970 per ounce but quickly rose back above it. Going into the European period, the Australian Dollar has been the best-performing major currency. Earnings and the general weakness in the housing sector are what cause Hong Kong’s Hang Seng Index to significantly underperform APAC stock benchmarks. Futures suggest that the European and North American equity sessions will get off to a strong start. Germany’s IFO figures will be the main event on today’s economic calendar. Numerous European CPI figures will be released later this week, and the US will receive GDP, Core PCE, and jobs statistics.

EURUSD Analysis

EURUSD is moving in an Ascending channel and the market has reached the higher low area of the channel.

According to ECB vice president Luis De Guidos, steps to tighten monetary policy in the Euro area are effective only in reducing economic inflation.

However, the US and Swiss banks’ fault steps will cause a liquidity crunch in the Euro area banks.

To prevent a shortage of liquidity in the banking industry, we must take action to tighten the rules.

According to an interview posted on the ECB website, Vice President of the European Central Bank Luis de Guindos stated over the weekend that the banking industry is “going through a period of very high uncertainty” that necessitates a meeting-by-meeting approach to interest rate policy.

It is appropriate to avoid committing in advance to monetary policy conference results. How the events in the US banking system and Credit Suisse will affect the economy of the euro-area is the issue at hand. We must determine whether they will result in a further tightening of funding conditions over the coming weeks and months.

Following rapid selling on the financial markets, which saw a 10% share price drop, German banking behemoth Deutsche Bank is under liquidity pressure.

This undermines the trust of European banks, and the ECB must act appropriately to safeguard the Deutsche Banks from this liquidity crisis.

As banking concerns return to the Eurozone, German banking behemoth Deutsche Bank is the most recent financial company to experience intense selling pressure. The stock of the business dropped more than 10% in early trading to a new multi-month low, and has lost more than 20% of its value this month. The credit default swap market showed significantly higher insurance costs as the cause of this recent sell-off, which also saw significant selling of the bank’s AT1 bonds. It is unclear if ECB President Lagarde will use the toolbox the central bank has at its disposal to provide the required liquidity if the current situation continues. She repeatedly stated it last week.

The appeal of safe-haven assets in the Euro Area increased as a result of this most recent wave of banking fear, with the yield on the German 2-year government bond dropping precipitously. The first glimpse at German inflation on March 30 and Euro Area flash inflation on March 31 are the two noteworthy data releases on the Euro Area calendar for the following week. Manufacturing and service sectors in the Eurozone are moving in distinct directions, according to recent economic data. According to data provider S&P Global, while the services sector kept growing, the manufacturing sector lost more new orders while total input costs and selling price inflation rates remained high.

A safety buy for the US dollar and Eurozone contagion both contributed to the Euro’s decline against the US dollar. The dollar continues to be the default coin of choice in tough financial times, despite the fact that the US banking system is also under scrutiny. On the daily chart, the EUR/USD pair reached a peak of 1.0930 yesterday. Today’s price is 1.0740, nearly two full points lower. The pair is now susceptible to further losses if the Eurozone banking crisis persists as a result of the move over the past 24 hours, which has broken a string of higher highs and higher lows.

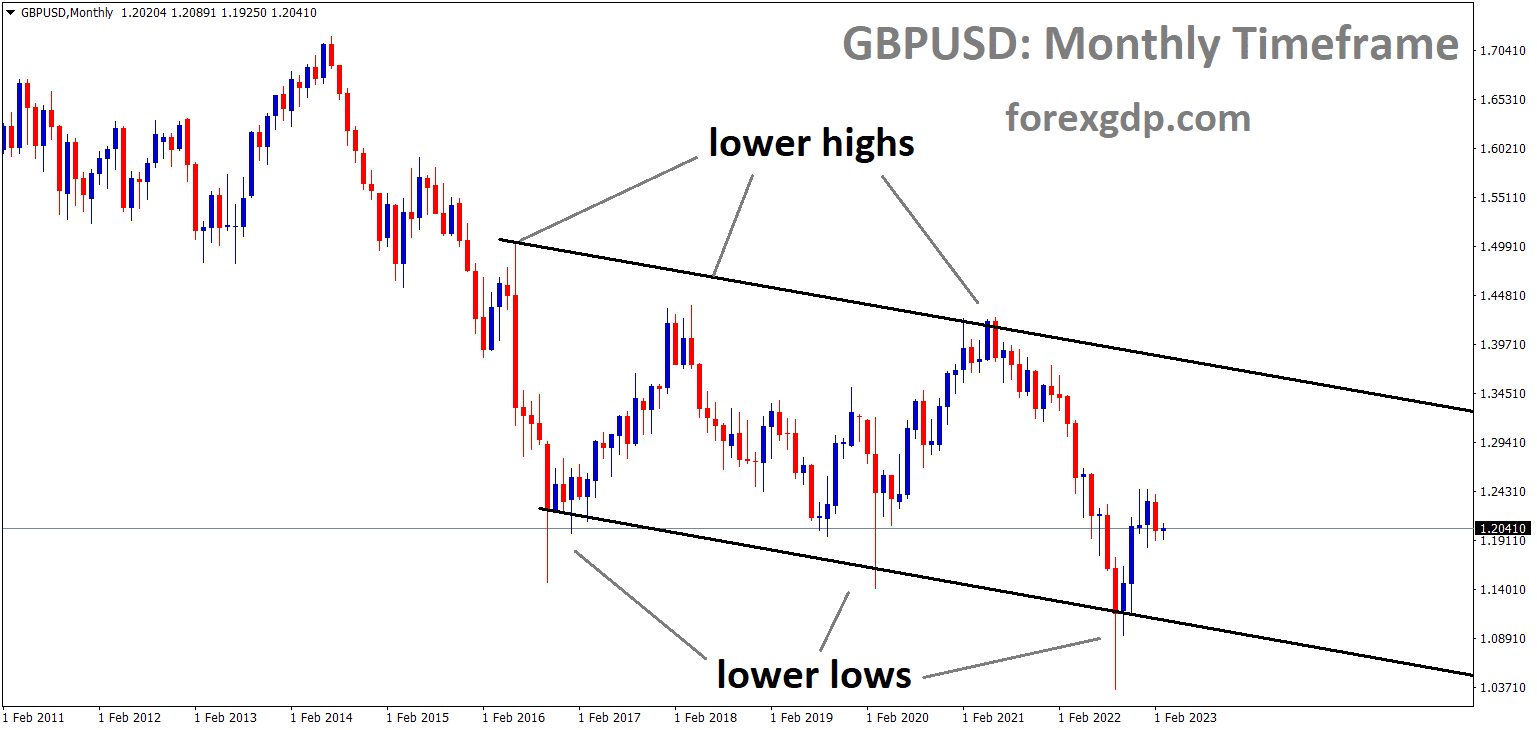

GBPUSD Analysis

GBPUSD has broken the Rising wedge pattern in downside.

Last Friday, strong figures for UK retail sales were released, printing 1.2% higher than the 0.20% forecast. Compared to the predicted 4.7% loss, the annual contraction is 3.5%. This information increases trust that the Bank of England will continue to raise interest rates.

In the Asian session, the GBPUSD pair has given up its early gains and is trading close to 1.2230. The US Dollar Index (DXY), which has shown some rebound following a gradual correction, caused the Cable to experience some heat after failing to rise above the immediate resistance of 1.2250. The US administration’s pledge to give mid-size banks more financial support has given market players more confidence, and the USD Index has tried to recover from its recent low of 103.00. According to Bloomberg, US authorities are contemplating expanding the emergency lending facility to give banks more support and more time to strengthen their balance sheets. This move would also give First Republic Bank more time to do so.

After a strong week, S&P500 futures have added some respectable gains on expectations that mid-size banks will be able to attract more customers thanks to emergency loan support. Additionally, more financial assistance for tiny US banks would help them regain the trust of consumers after declining deposits following the banking crisis. The decision-making is being influenced by the Federal Reserve’s (Fed) opposing views on the US crisis. Neel Kashkari, president of the Minneapolis Fed, stated on Sunday that recent stress in the banking industry and the potential for a secondary credit crisis “brings the US closer to recession.”

Raphael Bostic, president of the Atlanta Fed, told NPR on Friday that there are undeniable indications that the financial system is secure and robust. also Fed Bostic states that he “does not anticipate a recession in the industry. Following strong Retail Sales figures, the Pound Sterling was still trading on Friday in the United Kingdom. Compared to the prior release of 0.9% and the consensus estimate of 0.2%, the monthly retail sales figures saw a strong acceleration of 1.2%. The UK’s annual Retail Sales figures fell short of expectations by 3.5%, falling short of a 4.7% decline. This suggests that the Bank of England’s (BoE) rate-hiking cycle will last longer.

AUDUSD Analysis

AUDUSD is moving in the descending channel and the market has reached the lower high area of the channel.

As the US FED and Swiss Central Banks concentrate on liquidity measures that banks discovered to be ineffective, the Australian Dollar is under pressure. RBA The next meeting is anticipated to be a rate pause to address liquidity issues across the globe after only a few rate increases in the 25–50 bps range over the previous 10 meetings.

Last week, the Australian Dollar held steady, fluctuating by about one cent around the 67 mark. This occurs despite the RBA indicating a break in their pattern of rate increases in the meeting minutes that were made public last week. It appears that the battle against inflation is over, and that the need to halt the economy is no longer necessary. However, it seems that the current administration can see further down the road with expectations of price pressures rolling over. Previous RBA boards have usually avoided joining the forecasting game. To determine whether the posture is supported, the quarterly CPI figure in late April will be closely observed. The US Dollar’s gyrations continue to dominate the currency market, so the RBA’s relatively dovish attitude hasn’t hurt the Aussie Dollar.

Federal Reserve Chair Jerome Powell made a point of emphasising a few days ago that they can only manage what is in front of them when it comes to handling monetary policy across the Pacific. Despite several US banks failing just before the Fed’s conference, rates were increased by 25 basis points. There may be more financial institution failures in the US, but this unpredictability was unable to outweigh the bank’s inflation-fighting principles. Treasury yields are still higher than Australian Commonwealth Government bonds across the curve, which has typically undermined the Australian dollar in the interest rate environment.

In the aftermath of the banking crisis, US yields plunged, but they have since stabilised. Following the US notes’ example, ACGBs’ returns decreased along with them. While the 3-year portion of the curve is close to 75 basis points in support of the “big dollar,” the benchmark 10-year bonds have a yield differential of about 16 basis points in favour of the dollar. The disparity between the RBA and the Fed is highlighted by the wider spread at the short end. In general, industrial commodities are maintaining high levels, but soft commodities like maize are still struggling.

NZDUSD Analysis

NZDUSD is moving in an Ascending channel and the market has reached the higher low area of the channel.

Chris Hawkes, the deputy governor of the RBNZ, stated that despite the flooding in New Zealand, the bank’s capital levels have held up well. We do have a lot of strict regulations on the banking industry, and this remark allayed concerns about selling pressure on the New Zealand Dollar from its lows.

The New Zealand Dollar is supported by the market lows of the US Dollar.

After a depressing weekly ending, the NZDUSD shows the market’s inaction by making rounds to 0.6200 early on Monday. Thus, the Kiwi pair falls short of defending the Reserve Bank of New Zealand’s cautious optimism and mildly positive sentiment in the face of a light schedule, conflicting news, and apprehension regarding the most important data coming out of the US and China. Even though the Pacific island nation of New Zealand (NZ) is expected to experience more flooding, Reserve Bank of New Zealand Deputy Governor Christian Hawkesby downplayed concerns about banking fallouts in NZ earlier in the day. Although more research is required to understand how they might possibly compound with other risks to the financial system, RBNZ’s Hawkesby stated that the capital ratios of the nation’s banks will remain resilient during the majority of severe weather events. On the other hand, the momentum traders of the NZDUSD pair face difficulties due to a light calendar and a dearth of significant macros. In terms of advantages, Bloomberg’s reporting on the Silicon Valley Bank appeared to have boosted the risk-taking attitude. According to individuals familiar with the situation, First Citizens BancShares Inc. is in advanced talks to acquire Silicon Valley Bank following its collapse earlier this month. Neel Kashkari, president of the Minneapolis Fed, made remarks along the same lines in which he raised concerns about a potential US recession and restrained demands for further rate increases by the US central bank.

The majority-positive US data, the earlier hawkish Fed speech, and the report that Russia has moved its nuclear weapons closer to Belarus all weigh on the Kiwi pair in the meantime. The North Atlantic Treaty Organization criticised Vladimir Putin on Sunday for his ‘dangerous and irresponsible’ nuclear rhetoric, according to Reuters, a day after the Russian leader declared his intention to deploy tactical nuclear weapons in Belarus. Durable goods orders for February fell by 1.0% on Friday, compared to a decline of 5% in January (revised from -4.5%) and a rise of 0.6% expected by the market. Details indicated that although the number for Nondefense Capital Goods Orders ex Aircraft came in firmer-than-expected 0.0% to 0.2%, compared to 0.3% previously, it was also negative for Durable Goods Orders ex Defense and ex Transportation. The US S&P Global PMIs for March showed preliminary readings that were firmer than anticipated. The manufacturing gauge increased to 49.3 from 47.3 in February, versus an expectation of 47.0, while the services PMI increased to 53.8 from 50.6 in February, versus an expectation of 50.5. As a result, the S&P Global Composite PMI rose to 53.3 from 50.1 in February, beating the market expectation of 50.1.

Following the release of the US data, Raphael Bostic, president of the Atlanta Fed, told NPR that while raising the policy rate was not a simple choice, he did not anticipate a recession. In addition, policy hawk James Bullard, president of the St. Louis Federal Reserve, said on Friday that the response to the bank stress was prompt and appropriate, enabling the monetary policy to concentrate on inflation. The policymaker also mentioned that the forecasts call for one more rate increase, which might occur at the upcoming FOMC meeting or shortly thereafter. Moving forward, traders of the NZDUSD pair must keep an eye on the Fed’s favoured inflation indicator, the Core Personal Consumption Expenditure Price Index, in advance of China’s official activity data for March.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/