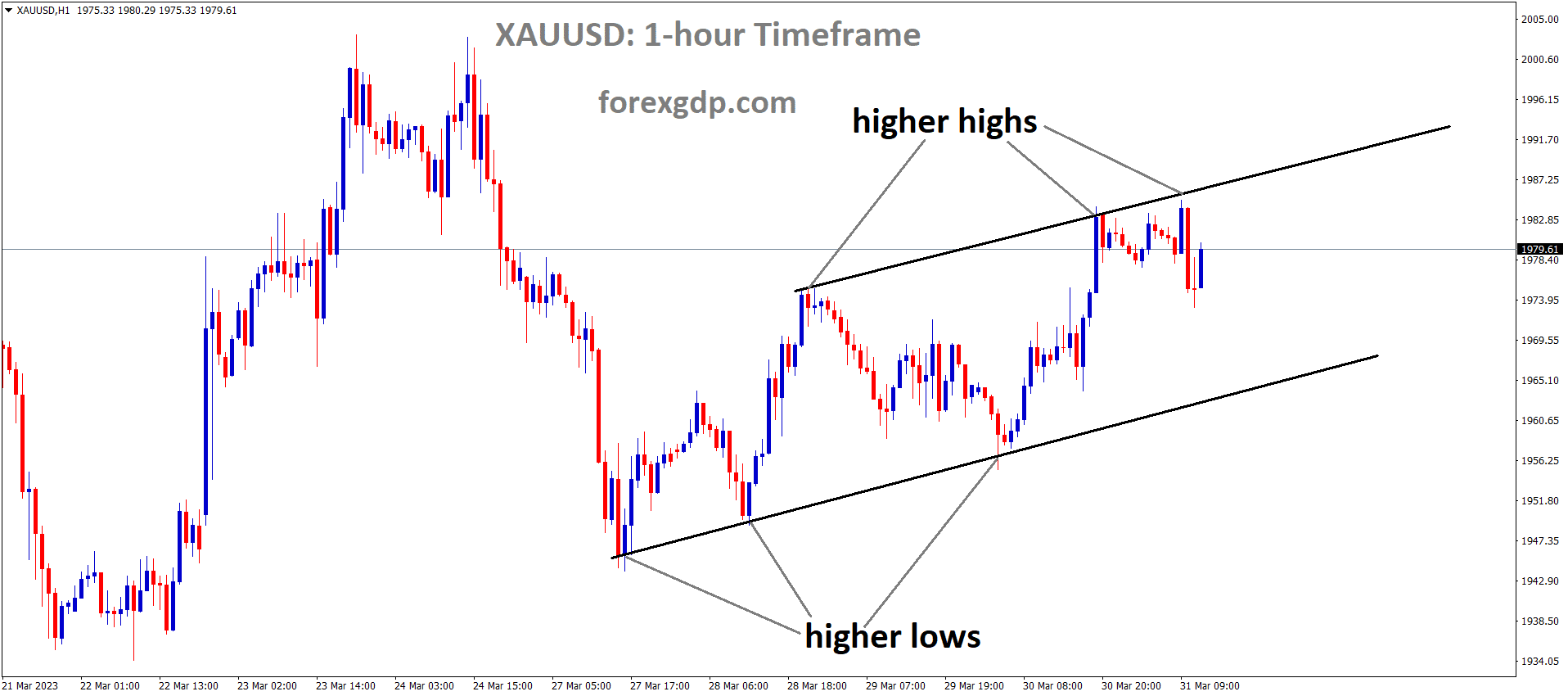

GOLD Analysis

XAUUSD Gold price is moving in an Ascending channel and the market has fallen from the higher high area of the channel.

In a private meeting with US Republican lawmakers, FED Chairman Jerome Powell discusses the possibility of a further rate rise. Gold prices increased the previous day after US GDP data came in lower than expected. As a result of FED-insured bank deposits, fears of bankruptcy have subsided on the markets. The FED requested an increase in funding for the Federal Insurance Corporation in order to raise the limits for insured bank deposits.

As markets speculate on how much further U.S. interest rates may have to increase, if at all, gold prices have remained stuck below the psychologically important $2000 per ounce level. When Republican members of Congress asked Fed Chair Jerome Powell behind closed doors on Wednesday about the probable rate path, Powell reportedly and understandably directed them to the central bank forecast of one more quarter-point rise this year. The present uncertainty in the gold market may be attributable to the markets’ lack of confidence in this. Gold and other non yielding investments become much less desirable as interest rates rise. Although the price increases have slowed since October, they are still above their levels from a year ago. The market has been buoyed by expectations of a pause in rate hikes and by the fact that inflation is still well above the 2% goal in many developed economies. Concerns about the global banking system have increased demand for haven assets like gold as lenders try to cope with rising interest rates, but the worst of these worries appear to be fading as markets become more confident that problems at a few banking names won’t cause another widespread financial catastrophe. In what is a week that is back loaded with important numbers, the gold market may also be looking for data cues. U.S. GDP and inflation numbers will be released by the end of the week, as will the closely monitored Purchasing Managers Index for the manufacturing sector and the University of Michigan’s time honored monthly survey of consumer sentiment. All of these factors could have an impact on future interest rate expectations and, by extension, gold prices. The metal is still in a short- and medium-term uptrend, even at the present high prices.

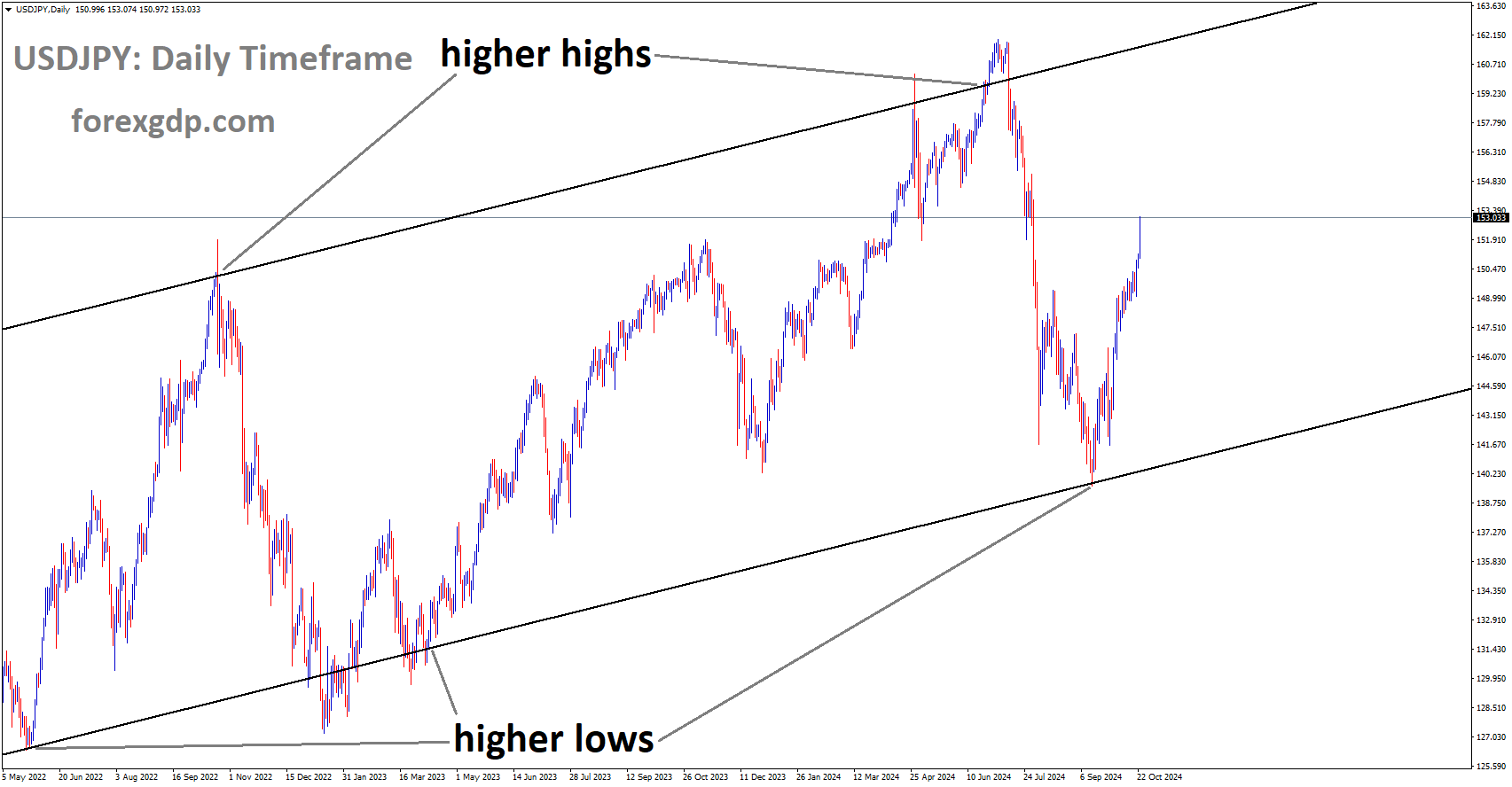

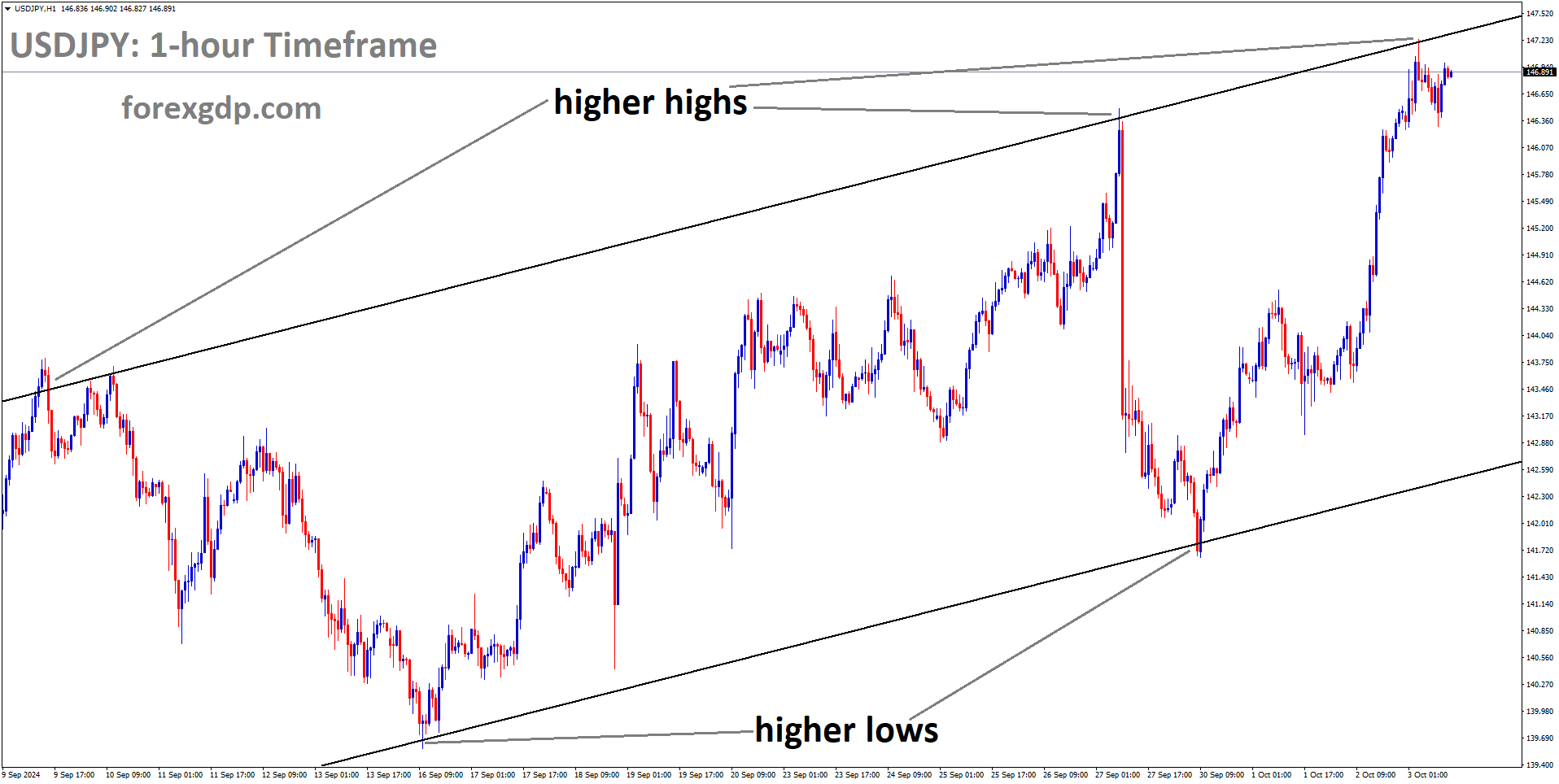

USDJPY Analysis

USDJPY is moving in an Ascending channel and the market has reached the higher high area of the channel.

Shunichi Suzuki, the minister of finance for Japan, stated that if market wage increases occur, Bank of Japan Governor Ueda will maintain the sound monetary policy and shortly revert to the previous monetary policy settings. The Japanese Yen received bad news when the jobless rate rose to 2.6% from 2.4% in February. According to Ranil Salgado, head of the IMF mission in Japan, there is more possibility for the long end of a curve under the Bank of Japan YCC policy.

After briefly touching a two-week high early Friday, the US dollar fell against the Japanese yen to a low of 132.90 as investors became nervous about upcoming important US inflation catalysts. The sluggish US Treasury bond yields, as well as the talk of the Bank of Japan and conflicting statistics from Japan, could be adding fuel to the fire of the retreat. The Tokyo consumer price index increased to 3.3% in March from 2.7% in February but slowed from 3.4% in February, while the Tokyo CPI excluding food and energy increased to 3.4% from 3.2% in the previous readings and 3.3% in the market opinion. In addition, the growth rate of Industrial Production in Japan jumped to 4.5% MoM in February from 2.7% in the month before and -5.3% in the month before that, and the growth rate of Retail Trade in Japan rose to 6.6% from 5.0% in the month before that and 5.8% in the month before that. On the other hand, the recent decline in the value of the Japanese yen can be traced back to Japan’s unemployment rate unexpectedly rising from 2.4% to 2.6% in February. After that, Japanese Finance Minister Shunichi Suzuki said he anticipates a strict implementation of monetary policy by the Bank of Japan and Ueda. The same boosts the independence of Japan’s central bank and will likely encourage it to press for exiting the easy money policies, particularly in light of the most recent wage increase. Still, it’s worth noting that IMF Japan Mission Chief Ranil Salgado was optimistic about the long end of the curve’s prospects in light of the Bank of Japan’s YCC policy.

But on Thursday, Federal Reserve Chairman Jerome Powell joined three other Fed Officials in supporting additional rate increases in order to tame inflation. Fed officials have been focusing on rejecting banking crisis worries, which has weighed on the US dollar and Fed bets, but recent mixed data from the US has cast question on their hawkish rhetoric. However, the CME’s FedWatch Tool indicates that there is a nearly 50% chance of a 0.25% rate increase at the May Fed meeting, down from 60% the day before. It’s worth noting that the Federal Reserve (Fed), European Central Bank, Bank of England, and Swiss National Bank have all lately taken steps to calm market concerns about the banking crisis. S&P 500 Futures, which track Wall Street’s optimism, have risen for three days in a row amid these maneuvers, to a level near 4,095. The yield on the 10-year US Treasury bond increased by two basis points to 3.57%, while the yield on the 2-year bond increased by the same amount over the course of five days to 4.13%. Next, markets will be looking to the Fed’s preferred inflation measure, the US Core Personal Consumption Expenditure Price Index for February, for guidance as they expect lower inflation will reduce the likelihood of hawkish Fed bets.

USDCAD Analysis

USDCAD has broken the Descending channel in Upside.

Positive numbers, if they arrive, will help the CAD against other currency pairs. Today Canadian GDP report is scheduled. The fact that Russia and OPEC+ entered talks but kept their production policies the same is another good development for oil prices.

In early Friday trading, the USDCAD recouped some of its previous day’s losses and was trading near 1.3520, its highest level in over a month. With the market on edge before the release of important inflation data from the US and Canada’s Monthly Gross Domestic Product data for January, the Loonie pair looks to the Dollar and Oil’s lack of movement for direction. After reviving a 13-day high earlier in the day, WTI crude oil is now modestly offered around $74.30. However, optimistic March official PMI prints from China and talk of no shift in OPEC+ production policies both favour Oil buyers. The US Dollar Index, meanwhile, fluctuates near 102.25 after having refreshed the weekly low with 102.05 earlier in the day. By measuring the dollar’s strength or weakness against a basket of six major currencies, DXY buyers can get a sense of the market’s general sentiment before important data is released.

It’s worth noting that the USDCAD pair’s recent corrective bounce seems to have been sparked by the hawkish rhetoric of Fed officials and robust US inflation expectations. Jerome Powell, president of the Federal Reserve System, has joined Susan Collins, president of the Federal Reserve Bank of Boston, Neel Kashkari, and Thomas Barkin, president of the Federal Reserve Bank of Richmond, in calling for a further rate increase to rein in inflation. The US dollar and Fed bets have taken a hit due to the Fed’s hawkish rhetoric and their rejection of banking crisis problems, but recent mixed data from the US has cast question on this. Traders expect a 47% probability of a 0.25% rate hike at the Federal Open Market Committee Monetary policy meeting in May, down from 60% the day before according to the CME’s FedWatch Tool. S&P 500 Futures, which track Wall Street’s optimism, hit a new three week high amid these manoeuvres. However, during a five day uptrend, yields on US 10-year Treasury bonds climbed two basis points to 3.57%, while those on 2-year bonds grind higher to 4.13%. Although the actual prints of the Core Personal Consumption Expenditure Price Index for February will be crucial for clear directions, the USDCAD may defend the recent corrective bounce before the key US inflation clues and Canadian GDP.

USDCHF Analysis

USDCHF is moving in the Box pattern and the market has rebounded from the horizontal support area of the pattern.

The release of Swiss retail sales data for February is scheduled, and it is anticipated to increase by 1.9% from the previous month’s contraction of 2.2%. This retail sales data will raise the Swiss zone’s inflation estimates. The SNB will then add more rate increases to the table to combat the inflation figures.

During the Asian session, the USDCHF pair has been stuck near 0.9140. After falling below 0.9120, the Swiss Franc is likely to hit a new low for the first time in two weeks. After a short pullback near 102.25, the US Dollar Index has gone down, which is making people bet more on the major going down. The USD Index is likely to drop below the immediate support level of 102.00 as the market moves against it. Bearish bets on the USD Index are getting stronger because investors think that Federal Reserve chair Jerome Powell will not raise rates again in 2023. This is based on the monetary policy meeting in May. No question, fears of a crisis in the US banking system have gone down a lot, but US banks will continue to make it hard to get credit in order to protect themselves from more losses. Also, the effects of US banking worries won’t be known for a while.

According to the CME Fedwatch tool, there are more than 52% chances that the Fed will leave its monetary policy stance the same at its policy meeting in May. In the meantime, Thursday’s confidence about the S&P500 futures has been carried over. During the Asian session, the futures on 500 US stocks have made more gains, which shows that market players are still willing to take risks. Lack of confidence about the future of monetary policy is making less people want to buy US government bonds. In terms of the Swiss Franc, investors are waiting for the Real Retail Sales statistics to come out. The annual retail sales data is predicted to grow by 1.9% instead of shrinking by 2.2%, which would make inflationary pressures even stronger and more likely to grow. Also, the Swiss National Bank is set on raising rates in the future to bring down inflation.

USD index Analysis

US Dollar index is moving in the Descending channel and the market has reached the lower high area of the channel.

The US Dollar fell after the publication of the data, but other fundamental data, such as ISM Manufacturing services, US Consumer confidence and NFP, and the unemployment rate, are extremely encouraging. The 75 basis point forecast is reduced to 40 basis points as a result of FED Chairman Powell’s statement that a further rate increase will be implemented in 2023. In accordance with these terms, interest rates will increase in 2023 and decrease in 2024.

EURUSD Analysis

EURUSD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

The anticipated Eurozone inflation rate is 7.1%, down from 8.5% in the previous release. Energy prices are decreasing, which helps to reduce inflation. The labour scarcity is the primary reason why the ECB raises interest rates at its meetings. The labour cost index is currently between 5% and 6%, the greatest level in decades; the likelihood of more workers entering the workforce is increasing as a result. Households have adequate funds for expenditure, and rate increases cannot affect their spending.

After failing to exceed Thursday’s high around 1.0926 in the early European session, the EURUSD has gradually declined to near 1.0900. The main currency pair has experienced selling pressure as a result of investors’ increased caution prior to the release of data for the US core Personal Consumption Expenditure Price Index and the Eurozone preliminary Harmonized Index of Consumer Prices. The US Dollar Index is improving, establishing support above 102.10. Investors have reduced their bets on the downside for the USD Index because they believe the Federal Reserve will raise interest rates at its monetary policy conference in May. The Federal Reserve’s plan for May’s policy has quickly changed as waning concerns about further damage to the US banking system have made space for the Fed to keep tightening policy. As investors grow anxious before the release of the Federal Reserve’s favoured inflation tool, gains made by the S&P500 futures during the Asian session have been cut in half. However, the general tenor of the market is quite upbeat. As investors ignore the US banking collapse incident, demand for US government bonds has decreased. The rates on US 10-year Treasury bonds fluctuate around 3.55%. Market players now feel very confident as worries about further US banking turmoil are fading. With baking jitters subsiding, investors do not expect any recession warnings, which has boosted demand for US stocks. Federal Reserve policymakers’ faith that the rate-hiking cycle can be maintained to contain persistent US inflation has also been restored by waning banking jitters. Jerome Powell, the head of the Federal Reserve, said he expects one more rate hike in 2023 during a private discussion with US lawmakers. According to the CME Fedwatch tool, there is a 53% possibility of a 25 basis point (bp) rate hike, which would raise interest rates to 5.00–5.25%.

Additionally, Thomas Barkin, president of the Richmond Federal Reserve, stated on Thursday that he is happy with the FOMC’s present trajectory of determining whether a 25 bps interest rate hike is necessary at each meeting. According to Barkin, households have a lot of money that is accessible for spending. He continued, It’s possible that tighter credit standards and the lag effect from our rate changes will cause inflation to decline fairly rapidly. But I still believe it might take some time before inflation reaches its intended level. Investors will monitor US core PCE Price Index data for more clarification. The PCE deflator is expected to increase by 0.4% more than nominal expenditure (+0.3%), according to Wells Fargo analysts. It is highly likely that the Eurozone’s headline inflation rate would sharply decline, driven by lower energy prices, taking cues from the German HICP report that was published on Thursday. The consensus predicts that the headline HICP for the Eurozone will decline from its previous report of 8.5% to 7.1%. The severe labour scarcity in the Eurozone is the economic indicator that may drive the need for additional rate increases from the European Central Bank. Due to a lack of job seekers, talent now has more negotiating power, which has also enabled wage growth to accelerate. According to Reuters, the labour cost indicator in the Eurozone is fluctuating between 5% and 6%, which is the highest level in decades. Therefore, as households have enough money for disposal, core Eurozone inflation statistics could become even more sticky. The public anticipates that Christine Lagarde, president of the European Central Bank, will raise rates in the future.

GBPUSD Analysis

GBPUSD is moving in the Box pattern and the market has reached the resistance area of the pattern.

The UK’s Q4 GDP was announced today and came in at 0.60%, which is significantly higher than anticipated and below the level seen before CVID-19. The UK economy grew by 0.10% in the fourth quarter of 2022, beating predictions for the quarter’s GDP of 4.0% by 4.1%. Following the announcement of the news, GBP gains.

According to data published by the Office for National Statistics, the UK economy grew by 0.1% in Q4 2022, which was 0.1% above forecasts. The Q3 statistics were also updated to -0.1% by the same amount. The level of quarterly GDP in Quarter 4 2022 has been revised up from the prior estimate of 0.8% below to 0.6% below its pre-coronavirus level. The prior estimate of 4.0% for 2022’s GDP growth has now been revised up to 4.1%. Real GDP rose by 0.6% when compared to the same quarter last year.

On the basis of the ONS release, cable made a small increase and returned to above 1.2400 for the first time in a month. Over the past few weeks, the price of sterling relative to the US dollar has been marginally higher. The continuing market speculation that the Fed may have finally completed its aggressive rate hike cycle and growing speculation that the US central bank may begin cutting rates at the end of Q3/beginning of Q4 continue to put pressure on the dollar. With the release of the closely watched US core PCE data this afternoon, we get the most recent glimpse at price pressures in the US. These rate-cut expectations will be dashed if US inflation stays stubbornly high and sticky, which will increase the value of the US currency. The remainder of the setup is still favourable when looking at the daily GBPUSD chart, even though the pair may begin to appear expensive when using the CCI indicator. The three moving averages are currently in a positive sequence, and cable is trading above all three of them as recent resistance turned support near the 1.2292 level continues to hold. Any upward movement appears to be vulnerable to the recent double top around 1.2448, and a verified break above this level would leave 1.2667 as the next area of resistance.

AUDUSD Analysis

AUDUSD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

According to Australian Prime Minister Albanese, the government should increase the minimum salary to keep pace with inflation rates. People with lower salaries do not adjust their inflation readings downward. The Australian Chamber of Commerce and Industry requested that the government increase the minimum salary by up to 4%.

Anthony Albanese, the prime minister of Australia, said on Friday that he supports increasing the minimum salary to keep up with inflation. The government report suggested that low-income employees’ real wages not decrease, but clarified that it was not arguing that wages should generally increase in tandem with inflation.

I would be pleased if the Fair Work Commission made such a determination, but ultimately it is up to the administration. They get to pick what kind of considerations they give weight to. My morals have remained the same. Meanwhile, in a Friday submission, the Australian Chamber of Commerce and Industry advocated for a raise of up to 4% in minimum and award pay.

NZDUSD Analysis

NZDUSD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

NBS Manufacturing PMI for China came in at 51.9, beating expectations of 51.5 and the previous figure of 52.6. After the statistics was made public today, the New Zealand Dollar increased. The non-manufacturing PMI increased from prior readings of 56.3 to 58.2. On Wednesday this week, Taiwan president Tsai Ing-wen visited the US, raising concerns about the trade ties between the US and China.

On Friday morning, optimistic data on China’s economic activity in March was released, sending the New Zealand dollar soaring to fresh weekly highs. Broad US Dollar weakness on dwindling hawkish Federal Reserve bets and mixed US data, as well as the market’s cautious confidence, have all contributed to the Kiwi pair’s upside. The main NBS Manufacturing PMI for China increased to 51.9 from 51.5 and 52.6 previously, while the Non Manufacturing PMI increased to 58.2 from 56.3.

Additionally, Federal Reserve Chairman Jerome Powell sided with three other Fed Officials on Thursday to support additional rate increases, citing the need to tame inflation woes. However, inconsistent US data casts question on Fed hawkish rhetoric, with policymakers instead focusing on their rejection of banking crisis problems, which has weighed on the US dollar and Fed bets. Consequently, the CME FedWatch Tool now predicts a nearly 50% rather than 60% chance of a 0.25% rate increase at the May Fed meeting. The market’s bets of future rate increases are weighed down by the Fed talks and the mixed US data, which helps to propel the Kiwi pair. However, the Real Gross Domestic Product for the fourth quarter in the United States came in at an effortless 2.6% Annualized Growth Rate, compared to the 2.7% Growth Rate that had been predicted. The Q4 PCE price index was in line with expectations and prior readings of 3.7% QoQ, while the Core PCE number increased to 4.4% QoQ, compared to 4.3% expected and prior readings of 4.2%. Next, the 198K figure for the week ending March 25 in Weekly Initial Jobless Claims was higher than the 191K figure reported the week before and the 196K figure predicted by the market. However, it should be mentioned that the NZDUSD bulls are encouraged by the Sino-American problems. The Taiwan Affairs Office in China has warned retaliation because of Wednesday’s visit by Taiwan’s president, Tsai Ing-wen, to the United States. As of March, the fiscal situation is even better than it was in January and February, according to China’s Premier Li Qiang. However, by opposing trade protectionism and decoupling, the policymaker has implicitly targeted the United States, heightening geopolitical tensions. Looking ahead, the US Core Personal Consumption Expenditure Price Index for February will be crucial as it represents the Fed’s favoured inflation gauge.

Crude oil Analysis

Crude oil price is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

The price of crude oil increased from the three-month lows and surpassed $74 per barrel. The primary causes are that China is recovering from the COVID-19 disaster and that demand for fuel increased in China as a result of the release of the lockdown. No change in output cuts, according to OPEC+ and Russia, helped crude oil prices rise even higher on the markets.

With the WTI futures contract up over 7% heading into the weekend, crude oil has maintained gains gained earlier today. This follows a 3.5% increase the previous week as it works its way back up from the three-month low hit earlier this month. While the Brent contract is just over US$ 79 barrel, the WTI contract is close to that price. The Chinese manufacturing PMI came in at 51.9 versus 51.6 forecasts for March, barely below the 52.6 figure from February, which helped the market somewhat. The non-manufacturing PMI increased from 56.3 to 58.2 against the forecast of 55. While APAC equities followed Wall Street’s example into the green today with an upbeat mood overall, gold is stable near USD 1,980. The best winner so far has been Japan Nikkei 225, which once increased by more than 1%. The USDJPY peaked earlier in the day at 133.50, suggesting that a weakened Yen is helping. At this point last week, the price had fallen to a low of 129.64, almost by four big digits. Today’s statistics on the number of jobs in Japan, the Tokyo CPI, retail sales, and industrial production all exceeded expectations. Here, you can see all the specifics. The North American stock session is expected to get off to a good start, according to futures. There hasn’t been much activity on other exchange markets today. The Federal Reserve’s Neel Kashkari and Susan Collins’ remarks from yesterday seem to have slightly increased the likelihood that the Federal Open Market Committee will decide to raise interest rates by 25 basis points in January. They both emphasised the necessity of containing inflation. The US core PCE printing hotter than anticipated, coming in at 4.4% year-over-year to the end of December instead of 4.3%, added to their remarks. Although the 1 year note is back to 4.70% and the majority of the curve is higher over the past week, Treasury yields have scarcely changed today. Looking ahead, a plethora of European inflation indicators will follow the UK GDP before the release of Canadian GDP statistics.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/