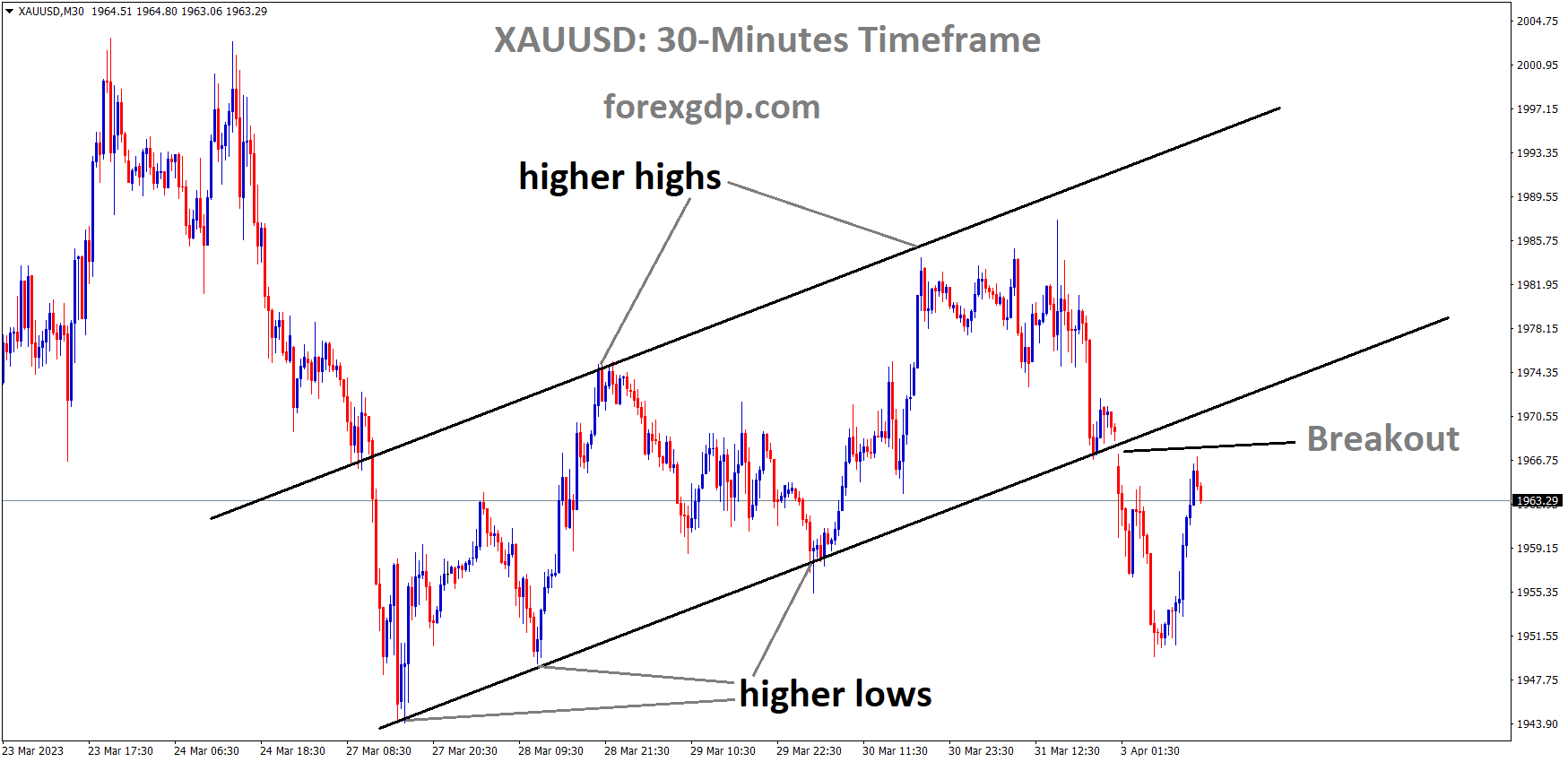

GOLD Analysis

XAUUSD Gold price has broken the Ascending channel in downside.

Due to the OPEC+ production cuts of 1 million barrels per day and the US FED’s probability of a 25 basis point rate hike in May, gold values are volatile relative to the US dollar. After the bank crisis calms down, the US dollar is relieved, and gold becomes a safe haven for buyers after their fears have subsided.

The gold price has recovered some of its early morning European declines to hover around $1,955 so far today. In doing so, the precious metal recovers from an intraday low not seen in a week as investors reevaluate the threats to the sentiment that originally favoured the US Dollar strength. After opening at 103.05, the US Dollar Index has fallen to 102.90 as early day risk aversion subsides and hawkish wagers on the Federal Reserve decrease. Concerns that China and Brazil will stop using the US Dollar in international trade have also thrown off the greenback’s gauge against the six main currencies. It’s worth mentioning that earlier today, OPEC and its allies led by Russia, known as OPEC+, declared a 1.16 million bpd output cut, which has renewed inflation fears.

As a result, they place downward weight on the Gold price due to a stronger US Dollar. Gold’s price has been recovering as investors have stopped betting on a sharp rate increase from the Federal Reserve. According to data from CME Group FedWatch Tool, the likelihood of a rate hike of 0.25% by the Fed in May has fallen to 42% from 52% last Friday. On the other hand, the XAUUSD traders face challenges from a weaker China Caixin Manufacturing PMI, heightened Sino-American conflict, and the market’s pre-NFP caution. Ahead of Friday’s US jobs data, Gold traders may be interested in Thursday’s US ISM Manufacturing and Wednesday S&P Global Manufacturing PMI.

USDJPY Analysis

USDJPY is moving in an Ascending channel and the market has reached the higher high area of the channel.

According to Japanese Prime Minister Fumio Kishida, unlike Western nations, Japan’s financial system is secure and does not fear panic. We keep a close eye on both domestic and international markets, and we implement the necessary laws to safeguard investor funds.

Japanese Prime Minister Fumio Kishida said Monday that the country financial infrastructure is secure. Foreign and domestic markets, as stated by the Prime Minister Kishida, require our full focus. The U.S. dollar strengthened against the Japanese yen to a day-end price of 133.67.

USDCAD Analysis

USDCAD is moving in the Descending channel and the market has reached the lower high area of the channel.

In January, Canadian GDP grew by 0.50% rather than the predicted 0.30%. Additionally, the announcement by OPEC+ to reduce its production by 1 million barrels helped the Canadian Dollar when compared to other currencies. The Ivey PMI and Canadian Employment Change are planned for this week, and the Canadian Dollar is in positive territory relative to other currency pairs.

Although the US dollar remained near its highest level in more than five weeks as Friday came to a close, the Canadian dollar edged lower against it. Canadian economic development in the first quarter was stronger than expected, lending support to the Canadian dollar and sending the pair lower from a high of 1.3564 to a low of 1.3507. The Canadian economy grew by 0.5% in January, which was more than the 0.3% rise predicted by economists, and GDP grew by another 0.3% in February, according to preliminary data. Meanwhile, expectations that the Federal Reserve would be less aggressive in hiking interest rates were bolstered by slower rise in US consumer spending. Inflation in the United States is showing signs of abating, according to the most recent PCE price indicator.

From January to February, the increase in the basic price index was a meagre 0.3%. The annual rate of core inflation is now 4.6%, while the overall rate of inflation is 5.0%. The rise in personal income was 0.3% (from 0.6% in January), while the decrease in personal expenditures was 0.2%. Oil is a significant export for Canada, and the price of this commodity hit a three-week high on Friday, reaching $75.68 on the spot market. Oil prices are expected to rise on the weekend news that OPEC producers have announced voluntary oil production cutbacks, which should be good for the Canadian dollar.

USDCHF Analysis

USDCHF has broken the Descending channel in Upside.

This week’s schedule for Swiss CPI statistics calls for more readings than the prior reading. In order to manage inflation readings, the SNB has already stated that they are prepared to raise interest rates. This week, the US ISM Manufacturing PMI is predicted to increase to 47.5 from its prior reading of 47.7. only the last four straight US ISM manufacturing PMI readings below 50.0.

In the Asian session, the USDCHF pair is encountering resistance near 0.9170 after a slight rebound. The US Dollar index appears poised to retest its weekly peak above 102.95, which bodes poorly for the Swiss franc. The USD Index received a shot in the arm recently as hopes rose for a global inflation rebound driven by higher oil prices following the news of oil production cuts by OPEC+. The S&P 500 futures have continued their losses from the Asian session as buyers look to reduce their equity exposure in light of the recent sharp increase in the price of oil. U.S. stocks are faltering, reflecting a general trend towards risk fear. As further rate increases from the Federal Reserve are widely anticipated, interest in US government assets has been lacklustre. As a result, the yields on 10 year US Treasury notes have increased to 3.51 percent. The release of US ISM Manufacturing PMI data on Monday is anticipated to keep the USD Index extremely volatile. The latest estimate is slightly lower than the previous one. In addition to the PMI number, the New Orders Index will receive close attention. It is anticipated that the forward-looking economic index for Manufacturing PMI will drop sharply to 44.6 from the previous release of 47.0. It appears that households are feeling the pinch of higher inflation, which may be having an effect on retail consumption. Prior to the release of CPI statistics, the Swiss Franc will continue to be traded. The Swiss National Bank has already left the door open for further rate hikes as inflationary pressures in the Swiss zone have stayed elevated.

USD Index Analysis

US Dollar index is moving in the Descending channel and the market has reached the lower high area of the channel.

Due to the OPEC+ and Russian-announced cuts in oil output, the US dollar is rising. US oil exports and output gain from this. Due to the Russia-Ukraine war problem, the regions of Europe benefited the most from US Oil and OPEC+. In light of the supply cutbacks by OPEC and others, the US dollar may rise in the days ahead.

Oil prices have increased as a result of the OPEC+ countries’ decision to reduce oil production. Within the G10 universe, the US Dollar benefited the most. Why? Commerzbank’s Head of FX and Commodity Research, Ulrich Leuchtmann, explains the USD reaction. If US energy production becomes more valuable as a result of a decline in production elsewhere, oil production in the United States becomes more profitable and attracts capital and labour. In this sense, the value of everything else produced in the United States increases. The burger in New York is more valuable because it must be produced, despite the fact that those frying it could get more lucrative employment on the Oil fields and those providing the capital to open the restaurant could just as easily invest in shale Oil companies. This makes the New York burger more valuable than its counterparts in Hamburg, Milan, or Tokyo. If this change is not reflected solely by a rise in the USD price of burgers in New York, the USD must appreciate in order to bring the relative value of Japanese, American, Italian, and German burgers in accordance with these new fundamentals. This is the reason why the dollar is presently appreciating, not the fact that the oil price displayed on your screen is in US dollars.

EURUSD Analysis

EURUSD has broken the Ascending channel in Downside.

When compared to February’s 8.5% YoY reading and forecasts of 7.1%, March’s 6.5% YoY reading for Eurozone CPI was lower than anticipated. The ECB’s hawkish tone on interest rates is called into question by this CPI figure. Additional rate hikes may be necessary to bring inflation under control, according to ECB Vice President Luis De Guindos.

As traders prepare for Monday’s crucial US Nonfarm Payrolls report, the euro/dollar has trimmed its advances from the previous two weeks around 1.0800. Recent worries of escalating pressure on prices and softer Eurozone inflation numbers compared to firmer prints of the Federal Reserve favourite inflation measure may be adding fuel to the fire of the pullback moves. Resurgent inflation worries and concerns of higher rates underpinned demand for the US Dollar after the Organization of the Petroleum Exporting Countries and allies headed by Russia, known as OPEC+, recently announced a surprise supply cut. Recent firmer inflation signals may be bolstering the US dollar, as the Fed’s favoured measure of inflation, the US Core Personal Consumption Expenditures Price Index, fell to 4.6% YoY in February from 4.7% in January and January. The 0.3% monthly increase in Core PCE was less than the 0.4% expected by the market and the 0.5% previously reported, which was amended down. In contrast, the European Central Bank’s favoured measure of inflation—the Harmonized Index of Consumer Prices—declined to 6.5% YoY in March from 8.5% YoY in February and 7.1% YoY in market forecasts.

The Core HICP, on the other hand, coincided with 5.7% expert projections and 5.6% previously. In March, the overall HICP increased by 0.9%, which was higher than both the 0.8% increase forecast and the 0.8% increase seen in February. Meanwhile, the Core HICP increased by 1.2%, which was higher than both the 0.6% increase forecast and the 0.8% increase seen in February. It is worth noting that the most recent remarks from European Central Bank officials, namely Vice-President Luis de Guindos and policymaker Fabio Panetta, suggest a reduction in inflationary pressure while defending the bank’s hawkish monetary policy stance. While Federal Reserve Bank of Boston President Susan Collins has emphasised the significance of higher rates to tame inflation, Federal Reserve Chairman Jerome Powell has pushed for one more rate hike. In the same vein, Federal Reserve Bank of New York President John C. Williams predicted that inflation would drop to around 3.15% this year and 3.25% in the coming year, bringing us closer to our longer-term objective. S&P 500 Futures print slight losses against this background despite Wall Street’s optimistic closing, while yields grind higher following a three-day decline. After that, the focus should be on the US employment report and headlines indicating inflation woes this coming Friday rather than the US ISM Manufacturing PMI or S&P Global Manufacturing PMI for March, which can direct intraday movements.

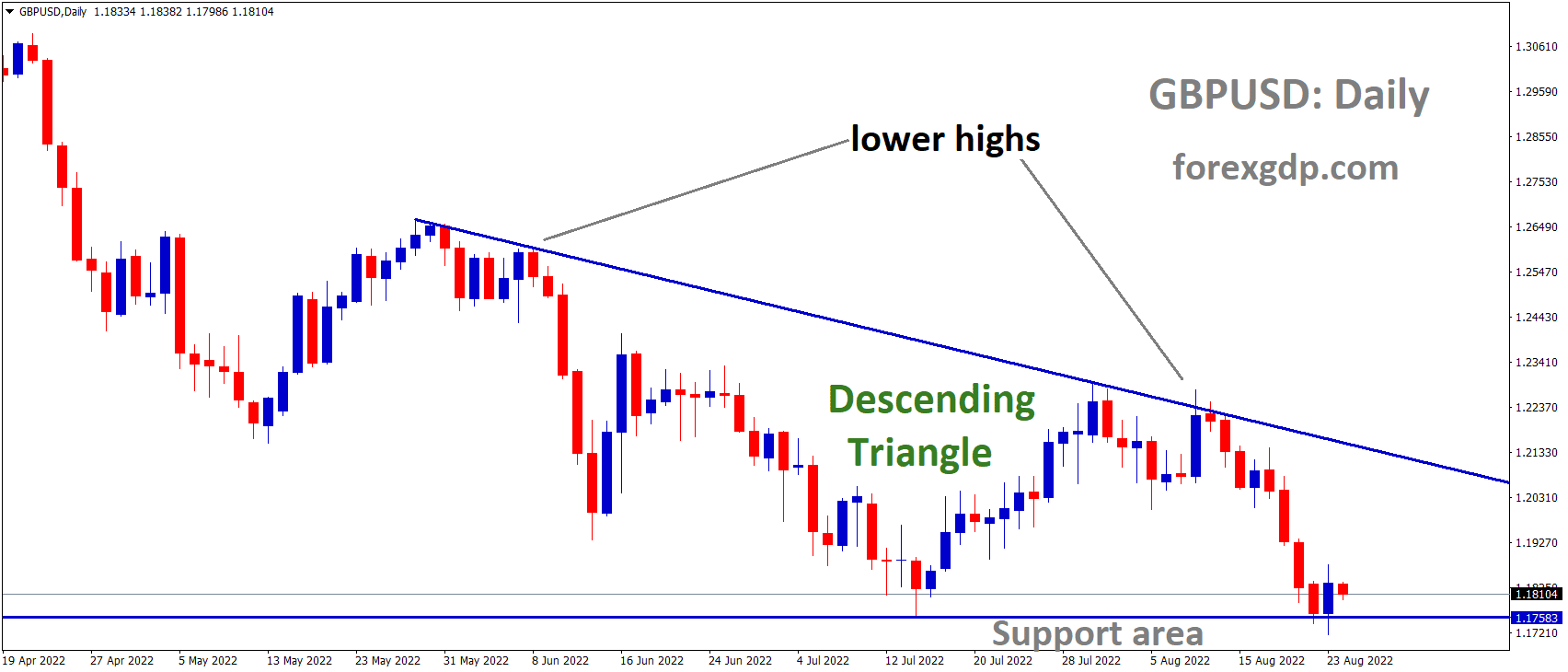

GBPUSD Analysis

GBPUSD has broken the Rising wedge pattern in downside.

Citi and YouGov conducted a survey of the public’s inflation predictions in the UK, and the results indicate that these expectations were lower in March than in February. Public hopes in the UK for the next five to ten years decreased to 3.7% in March from 3.8% in February. However, the range is still higher than the pre-pandemic limit of 3.4% to 3.4%. Expectations for the next year are 5.4% in March, down from 5.6% in February.

A monthly survey conducted by Citi and YouGov revealed on Monday that the British public’s inflation expectations decreased in March after nudging up in February. The British public’s expectations for the next five to ten years decreased to 3.7% in March from 3.8% in February, but remain above the range of 3.0% to 3.4% observed prior to the COVID-19 pandemic. March inflation expectations in the United Kingdom decreased to 5.4% from 5.5% in February. GBPUSD is off its lows but remains under pressure below 1.2300 on the back of encouraging survey results that support the case for a Bank of England rate hold. As of this writing, the pair is trading at 1.2290, down 0.34 percent on the day.

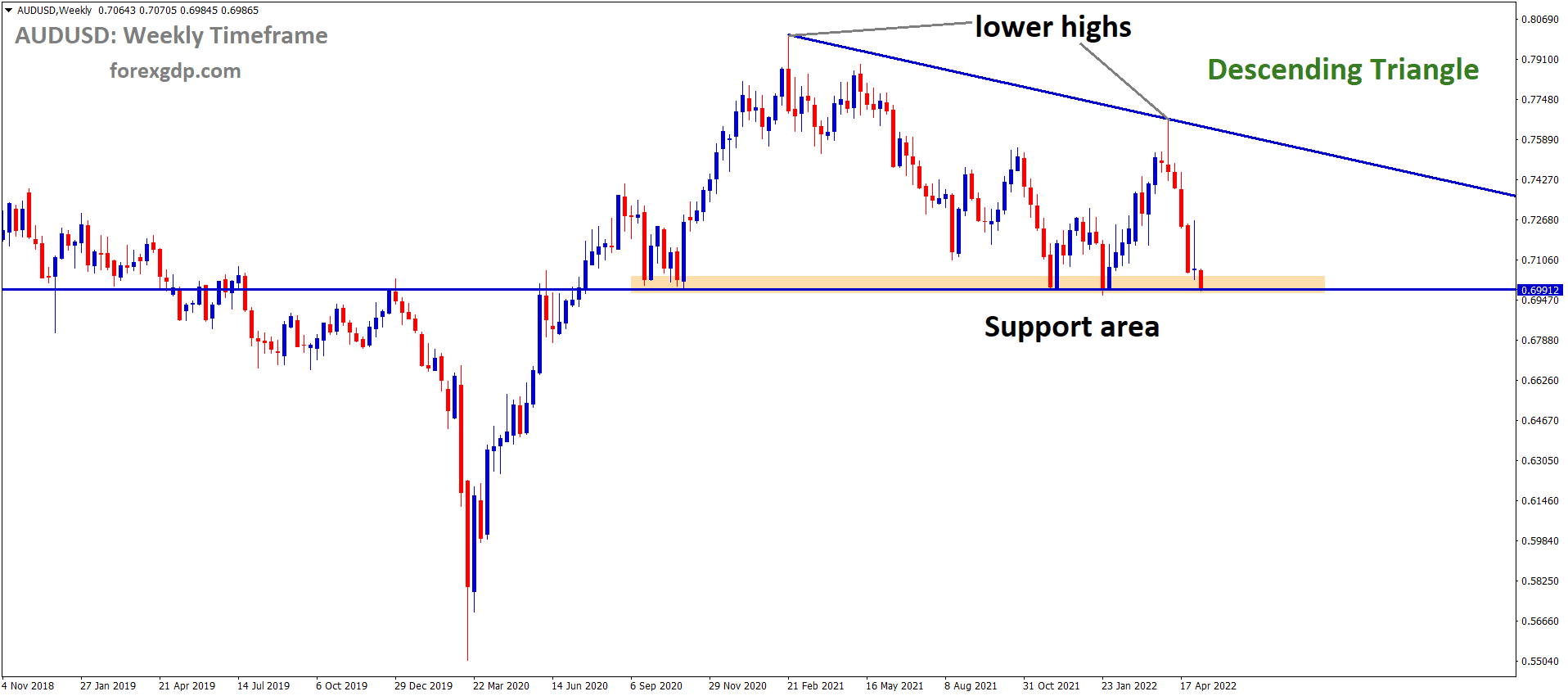

AUDUSD Analysis

AUDUSD is moving in an Ascending triangle pattern and the market has rebounded from the higher low area of the pattern.

Tomorrow RBA Policy Meeting is anticipated to result in a 25 bps rate increase. Data on month-over-month inflation decreased from 8.4% in December to 6.8% in February. Manufacturing data from Caixin came in at 50.0 compared to 51.7 expected and 51.5 in the prior reading. Due to the decline in the volume of manufacturing activity in the Chinese economy, this reading had an effect on the Australian Dollar.

After a decline during the Asian trading period, the AUDUSD has found some support around 0.6660. Investors are waiting for the release of United States ISM Manufacturing PMI data to provide new impetus, so the Australian asset has attempted a decent recovery but is likely to stay on the tenterhooks. Investors’ anticipation of Tuesday’s interest rate decision from the Reserve Bank of Australia would cause significant swings in the Australian dollar. In the early European session, S&P500 futures are auctioning in a negative trajectory, reflecting a risk-averse theme, as oil prices have risen on concerns that OPEC+ will reduce oil output further. Producers will be forced to pass on the cost of higher oil costs by charging customers more for goods and services when they leave the factory. In the long run, families would suffer the most, which could reduce demand at stores.

As a result of renewed worries about a resurgence in global inflation spurred by higher energy prices, demand for US government bonds has plummeted. Yields on 10-year US Treasuries are currently close to 3.52 percent. With rising oil prices expected to have far-reaching consequences, the US dollar has been on a tear recently. Inflation had been stubborn for a year, and many countries were having trouble getting back on track. And now, with oil costs rising, the already-weak efforts to rein in inflation are likely to falter. The fact that the Federal Reserve is likely to maintain its policy tightening programme in order to counteract oil-inspired price pressures has boosted the value of the US dollar. The CME Fedwatch tool indicates that the probability of a 25 basis point hike to 5.00-5.25% at the monetary policy conference in May is now greater than 61%. The US ISM Manufacturing PMI data is expected to keep investors occupied going forward. The previous Manufacturing PMI reading was 47.7, and the average forecast calls for a slight drop to 47.5. The US Manufacturing PMI has been below 50.0 for the past four months in a row, a trend that investors should be mindful of. The New Orders Index is the most attention-grabbing component of the US industrial PMI suite because it indicates future industrial activity. Manufacturing forward demand is forecast to drop sharply to 44.6 from the previous report of 47.00.

After IHS Markit reported poor Caixin Manufacturing PMI data, the Australian dollar stayed volatile throughout the Asian session. The economy statistics came in at 50.0, which is below both the expected 51.7 and the previously released 51.5. As China’s most important trading partner, the Australian dollar felt the effects of a slowdown in China’s industrial sector. The Reserve Bank of Australia’s interest rate decision, set to be revealed on Tuesday, is currently the centre of attention. Rate hikes of 25 basis points by Reserve Bank of Australia Governor Philip Lowe to a total of 3.80% are widely anticipated. In February, Australia’s monthly inflation index fell to 6.8% from December’s 8.4% high. RBA policymakers will not be persuaded to maintain current interest rate levels even in the presence of evidence indicating a sharp decline in Australian inflation.

NZDUSD Analysis

NZDUSD is moving in an Ascending triangle pattern and the market has rebounded from the higher low area of the pattern.

According to the article from the New Zealand Institute of Economic Research, the Shadow Board members expect the RBNZ to raise the official cash rate by a smaller amount at their meeting on Wednesday. After the initial round of rate increases put pressure on businesses and the economy, one of the shadow members suggested pausing the official cash rate. The formal cash rate for this year is expected to range from 4.25% to 5.50%, according to other Shadow members. Some of the group held the view that New Zealand’s economy might enter a recession if interest rates continued to rise at their current pace or were raised even further this month.

According to the most recent report from the New Zealand Institute of Economic Research, shadow board members advocate for a more modest increase in the Official Cash Rate during the Reserve Bank’s forthcoming April Monetary Policy Review. Given that inflation pressures are still high and inflation expectations are still above the Reserve Bank’s 1-3 percent inflation goal band, the NZIER report notes that the consensus opinion was for an OCR increase of 25 basis points. Nonetheless, two Shadow Board members suggested the Reserve Bank maintain the OCR at 4.75%. One of them thought the OCR had reached its zenith already, while the other warned of an impending economic downturn. The Shadow Board’s consensus on where the OCR should be in twelve months was between 4.25 and 5.50 percent. In order to drive inflation down, some members of the Reserve Bank have suggested keeping the OCR high for some time after April. Since businesses’ profits and finances have been struck so hard by interest rate increases so far, one business community Shadow Board member believes the OCR should be lower in a year.

Crude Oil Analysis

Crude Oil is moving in the Descending channel and the market has reached the lower high area of the channel.

To address supply issues, OPEC+nations declared a reduction of 1 million barrels per day. Russia has declared a daily reduction of 500k barrels. Due to an unanticipated reduction in production by OPEC+ countries, crude oil prices rose 8% on Monday morning. In light of the current state of the economy, rate cutbacks are not advised, according to the US Spokesperson for the National Security Council.

After OPEC+ unexpectedly announced a production cut over the weekend, crude oil prices surged more than 8% on Monday morning. The explosive increase comes after the price of black gold increased by over 9 percent last week. Since the opening price spike, prices have decreased, and market liquidity at the time may have exacerbated the initial move. Several OPEC+ officials reportedly implied last week that there would not be a production cut in the immediate future. The reduction of more than 1 million barrels per day follows last week’s announcement that Turkey will no longer be able to obtain oil from Kurdistan due to a ruling by an international court of arbitration. It is estimated that global markets will receive 400-450 thousand fewer barrels per day from this source. In addition, Russia has stated that it will maintain its production reduction of 500,000 barrels per day through the end of the year.

Saudi Arabia will perform the majority of the heavy lifting within OPEC+ by reducing production by 500,000 barrels per day. It appears that the syndicate views the Fed’s rate-hike cycle as having slowed down economic activity in the largest economy in the globe. Ironically, the tightening oil supply could contribute to inflationary pressures, prompting the Fed to reconsider its tightening policies. In response to the cut, a spokesperson for the US National Security Council stated, Given the current market uncertainty, we do not believe that cuts are prudent at this time. China’s removal of pandemic restrictions has not resulted in the anticipated increase in global economic activity, which may have played a role in the decision. The cartel made the unconventional announcement a day before the OPEC+ monitoring committee meeting. In early trading, the WTI futures contract peaked at US$ 81.69 bbl, while the Brent contract reached US$ 86.44. Since reaching those peaks, each contract has retraced lower.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/