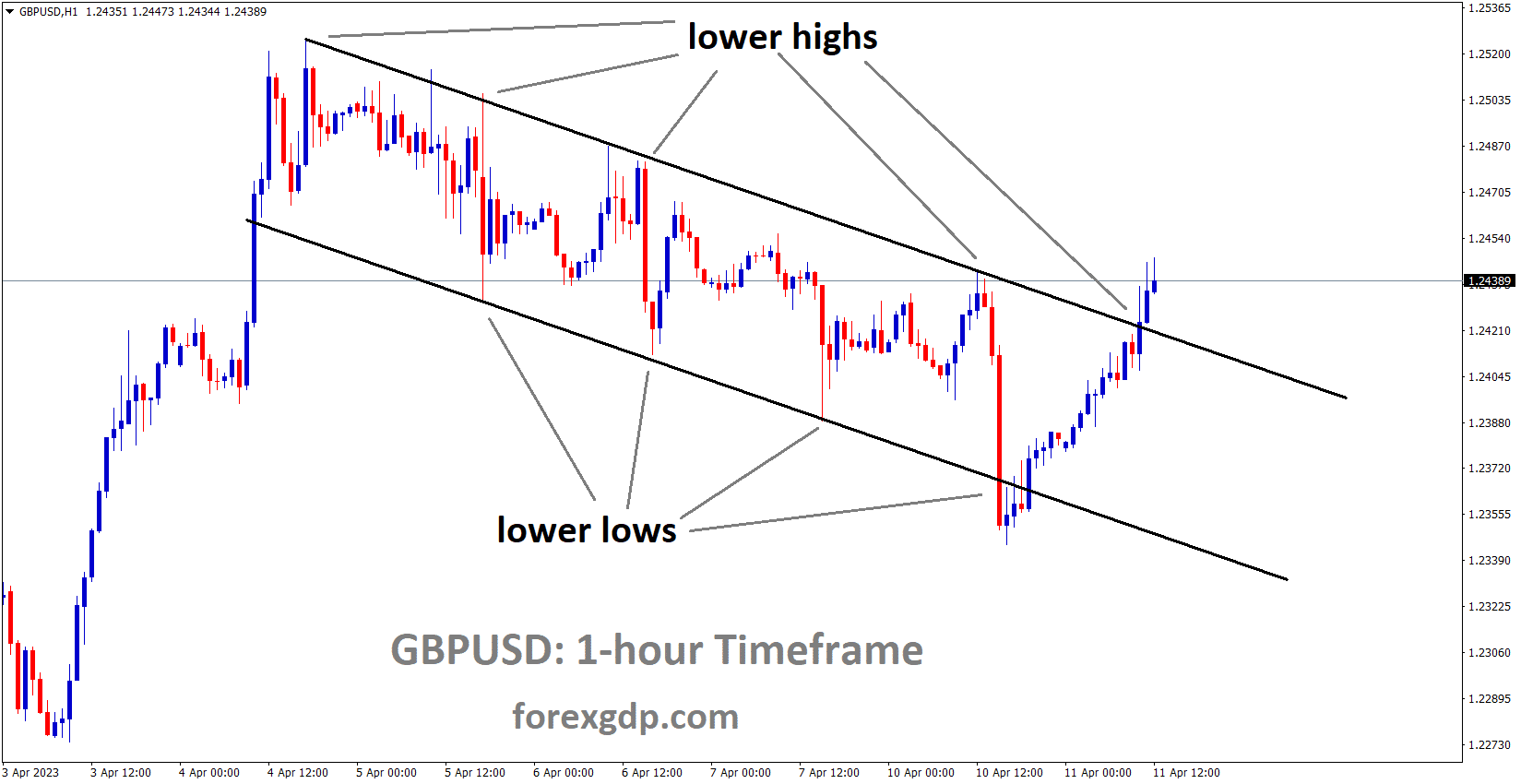

GBPUSD Analysis

GBPUSD is moving in the Descending channel and the market has reached the lower high area of the channel.

Although rate increases have not prevented inflation from rising in the UK economy, it has. The continued strength of retail sales has kept inflation high. Another factor driving up the UK’s CPI is the demand for oil and gas, primarily as a result of the wars in Russia and Ukraine.

In the early European session, the GBPUSD auction rose above the 1.2400 round level of resistance. Bids have been placed on the Cable as investors react more responsibly to the growing likelihood of further rate hikes from the Federal Reserve. Fears among investors ahead of the release of the US Consumer Price Index have subsided, but that hasn’t helped the US Dollar’s downward trend in the Asian session. With the market sentiment so optimistic, the US Dollar Index appears susceptible above the near-term support level of 102.30. Futures on the S&P 500 are showing slight advances in Asia. After opening lower than expected on Monday, US stocks recovered, suggesting further losses are likely limited. Investors continue to back the US equity market, despite a reduced consensus for profits to be delivered on the S&P500. Profits for the S&P 500 are predicted to decrease by 5.2%, according to Refinitiv, compared to the 1.4% growth forecast made at the beginning of the year. The Federal Reserve’s decision to raise interest rates and tighten credit conditions among US commercial banks have contributed to a reduced projection for the S&P 500. Market optimism has also acted as a barrier to further gains in US yields. Below 3.41 percent, rates on 10-year US Treasuries appear slow. Investors have begun pouring money into risky assets despite increased odds of a fourth consecutive rate hike by the Federal Reserve of 25 basis points. Since the US labour market has exhibited no discernible indications of slowing down despite higher rates and tighter lending conditions, investors appear confident that the Federal Reserve will continue raising interest rates. After less hawkish comments from New York Fed Bank president John C. Williams, the US dollar continued its downward trend in the Asian session. U.S. Central Bank Williams predicted that this year’s inflation rate would be around 3.75 percent, growth would be under one percent, and the unemployment rate would rise to 4.5 percent. This bodes well for future rate cut expectations as it suggests inflation will ease. According to Fed Chairman Jerome Williams, the recent banking upheaval was not caused by the Federal Reserve’s decision to raise interest rates. If the Federal Reserve’s hawkish monetary policy is not to blame for the banking crisis, this has calmed nerves.

As the final inflation figures before the Federal Reserve’s interest rate decision, which will be revealed in the first week of May, the release of the US CPI data has generated considerable attention among investors. As a result, the US inflation report on Wednesday will be more significant. TD Securities forecasts an increase of 0.1% in headline inflation and 0.4% in core CPI for March. They anticipate a 3.6% CPI slowdown by the end of the year. Consistently reduced oil prices, which have eventually supplied petrol to end consumers at more affordable costs, are projected to lessen March’s headline inflation in the United States. While households have more disposable income than ever before, core inflation may be accelerated by the rising labour cost index. The United Kingdom is one of the countries that is having extreme difficulty taming runaway inflation. The Bank of England’s interest rates have hit decade highs, and the UK government has offered financial incentives to delay retirement, but the price index still shows no signs of easing. The British Retail Consortium’s monthly report on same-store sales held unchanged at 4.9%. Inflationary pressures are predicted to remain high as a result of persistently strong retail demand.

GOLD Analysis

XAUUSD Gold price has broken the Descending channel in upside.

Since last Friday, when the US Jobs data showed high confidence in the US Economy, the gold price has corrected. In May, the US FED will raise rates by 25 basis points before pausing further rate hikes.

As a result of widespread U.S. dollar strength and greater odds of future Fed tightening in the wake of exceptionally excellent U.S. labour market statistics announced last Friday, gold prices fell on Monday, falling more than 1.0% and threatening to breach below the key $2,000 barrier. As a result of the March U.S. employment data showing 236,000 new jobs were created, traders have increased their wagers that the FOMC would give another quarter-point rate raise at its May meeting, thereby decreasing the likelihood of a pause in the hiking cycle next month. Gold, priced in dollars, will face resistance if the Federal Reserve continues its tightening campaign, and is therefore unlikely to break over the $2,000 level in the days and weeks ahead.

SILVER Analysis

XAGUSD Silver price is moving in an Ascending channel and the market has reached the higher high area of the channel.

Nonetheless, this does not rule out the bullish case. The Fed will certainly adopt a dovish approach whenever the economy takes a turn for the worst, weighed by the lagging effects of aggressive rises and the detrimental impact of the financial sector crisis, but the direction of monetary policy in the immediate future remains unclear. If this occurs, gold prices will be in a good position to surge.

USDJPY Analysis

USDJPY is moving in an ascending channel and the market has fallen from the higher high area of the channel.

The new governor of the Bank of Japan, Ueda, stated that every policy that the former governor had implemented would be continued in the coming year as well. Nothing signifies a modification to YCC control and monetary policy. After the new governor took office, the Japanese Yen continued to weaken.

Yesterday was our first opportunity to see Kazuo Ueda, the new governor of the Bank of Japan, in action. Nothing has changed at all. At first, it was negative JPY. Commerzbank’s Head of FX and Commodity Research, Ulrich Leuchtmann, examines the handling of JPY risks. Nothing he said was good news for the JPY because he promised to keep up the ultra-expansive monetary policies of his predecessor. This may be seen in the yield curve control, which would be the first variable to shift in an exit scenario. Ueda, however, was not open to this sort of alteration. That is to say, nothing has changed. Nothing he said was good news for the JPY because he promised to keep up the ultra-expansive monetary policies of his predecessor. This may be seen in the yield curve control, which would be the first variable to shift in an exit scenario. Ueda, however, was not open to this sort of alteration. That is to say, nothing has changed.

If this change in monetary policy is implemented soon, the yen will likely rise in value over the long term. If the BoJ waits too long, though, the yen might easily decline despite rising yields. Alternatively, inflation falls below the Bank of Japan’s 2% objective. We would essentially be starting over, making a shift away from the current ultra-expansive monetary policy highly implausible. Objectives can be broken up into three distinct time frames. If you read the recent globe Economic Outlook from the IMF and share its outlook, you may have concluded that real yields in the rest of the globe will fall once the present inflation shock has gone off. In that situation, the actual yield disadvantage of the Yen would be moderate, therefore advocates of that perspective might not be overly JPY-pessimistic.

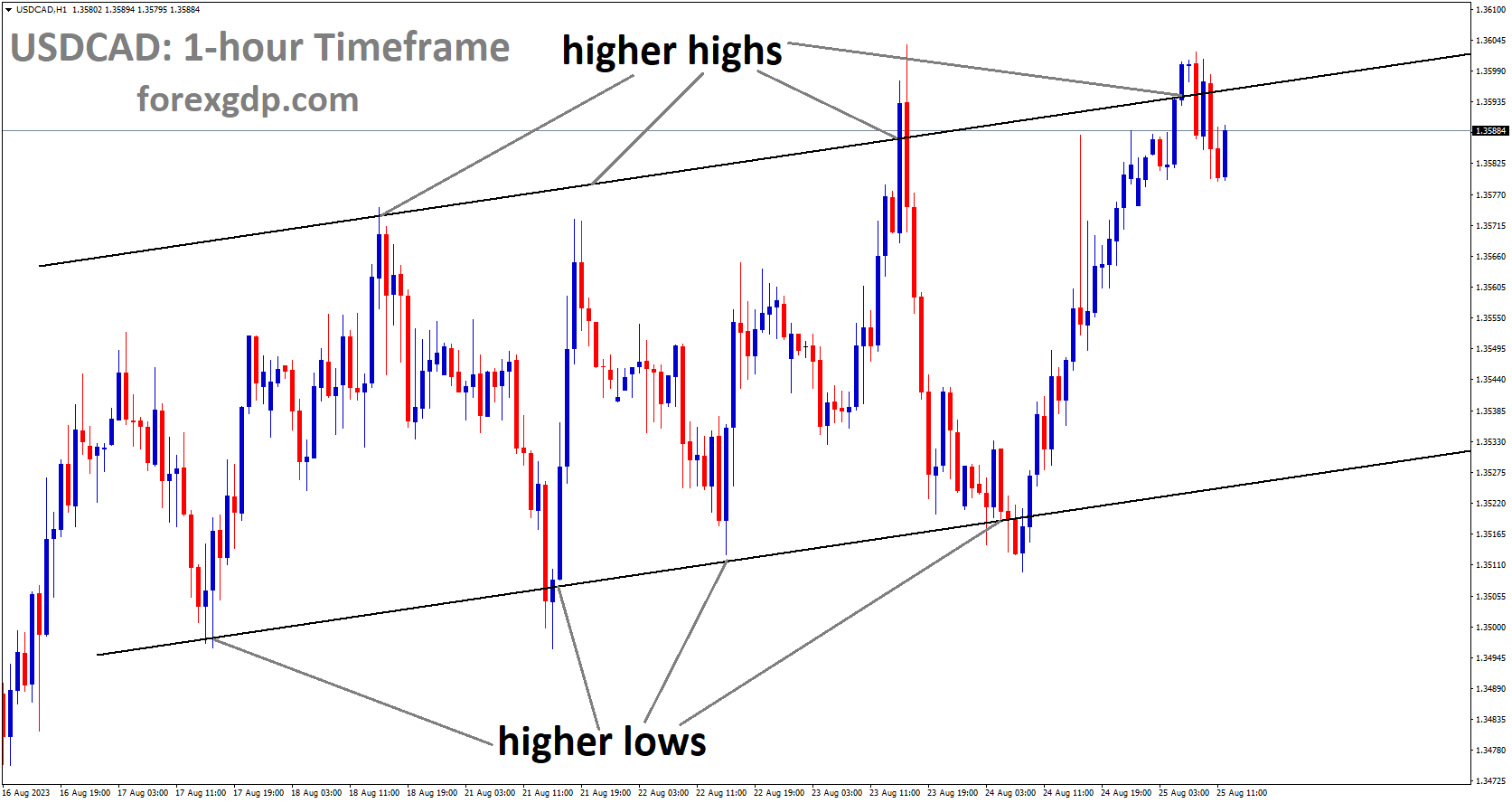

USDCAD Analysis

USDCAD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

After Chinese inflation came in lower than anticipated, oil prices sharply increased. Oil prices increased against the USD as a result of OPEC+ supply curbs. As oil prices rose, the Canadian Dollar gained more.

In the wake of modestly bullish market sentiment and a weaker US Dollar into Tuesday’s European session, WTI crude oil prices have rebounded to hit their intraday high near $80.40. As regular trading resumes after a long weekend, the price of black gold is still within a week-old range of around $2.0.

At press time, the US Dollar Index had fallen to 102.35, down 0.20% from its previous close. This is despite the fact that John Williams, Vice Chairman of the Fed’s rate-setting committee and President of the Federal Reserve Bank of New York, has been blaming rising inflation expectations on the weakening dollar. In a similar vein, Rick Rieder, CIO of global fixed income at BlackRock, the largest asset manager in the world, told Reuters late on Monday that the Federal Reserve may not need to raise interest rates further to fight inflation because the aftermath of last month’s banking sector turmoil and a string of recent labour data point to a slowing US economy.

Contrast this with the cautious optimism in the markets, which has been depicted by events such as the conclusion of China’s military manoeuvres near Taiwan, the Australian-China trade pact, and anticipation for additional investment in Japan. Headlines from the International Monetary Fund’s Managing Director Kristalina Georgieva on Monday also favoured the optimists, as she predicted that India and China would be responsible for half of the world’s growth this year. However, the market sentiment and WTI crude oil purchasers are put to the test by the roughly 71% odds that the US Central Bank would raise rates by 0.25% in May, as printed by CME’s FedWatch Tool. Downbeat China inflation data and a cautious mood before top-tier US data/events may also be dragging on risk appetite and the price of the energy benchmark. WTI crude oil’s upward trend is mostly supported by the OPEC+ production cutbacks and rising expectations of increased energy demand from the world’s largest energy user, China. Next, WTI prices may be influenced by the American Petroleum Institute’s weekly report on oil stocks (previously -4.346M). Nonetheless, the Fed Minutes, the IMF’s spring conference, and US inflation will all be watched closely for cues.

USDCHF Analysis

USDCHF is moving in the Descending channel and the market has fallen from the lower high area of the channel.

Credit Switz Leaders from the bank have stated that there will be no layoffs and instead a complete freeze on hiring. The SNB’s prudent measures in the banking sector and currency strengthening have helped the Swiss franc gain ground versus the US dollar and other major currencies in recent days.

ZURICH The Swiss Bank Employees’ Association demanded in an open letter to the Swiss parliament on Tuesday that Credit Suisse and UBS immediately halt any planned layoffs as part of their emergency merger. Natalia Ferrara, CEO of SBPV, recently penned a letter to legislators pleading for a moratorium on layoffs until the end of 2023, citing the plight of employees affected by the demise of Credit Suisse. In a letter seen by Reuters, Ferrara pleaded with lawmakers to back his proposal to halt layoffs until the end of 2023. She also stressed the need of politicians taking on their duties honestly. Swiss lawmakers will hold a special session on Tuesday to address the government’s recent bailout of Credit Suisse. The Swiss government, central bank, and market regulator worked together to broker a deal whereby UBS would acquire Credit Suisse, a Zurich-based competitor, for 3 billion Swiss francs.

According to Ferrara, many of the roughly 17,000 Credit Suisse employees and the 22,000 UBS employees in Switzerland have been looking at their future with worry for the previous three weeks.

Credit Suisse has 45,000 employees across the world, whereas UBS has 74,000.However, the affected employees of the two banks continue to be an afterthought. That has got to alter. UBS CEO Sergio Ermotti foreshadowed change and hard decisions in the wake of the merger last week. According to Swiss news outlet Tages-Anzeiger, the newly formed megabank may decrease its employees by 20%-30%, which would result in the loss of 11,000 jobs in Switzerland. UBS has stated that it is too soon to speculate about potential layoffs. Ferrara stated that the rescue effort was not the employees’ fault and that UBS’s preparations would take months to develop.

In a letter published by the Swiss newspaper Blick on Tuesday, Ferrara urged the banks to protect and respect their affected staff. It cannot be that during the emergency session, parliament spends days debating the financial and technical issues of the CS rescue while the people affected are disregarded.

USD Index Analysis

US Dollar index is moving in the Descending channel and the market has reached the lower high area of the channel.

After Friday’s positive US jobs data, the US dollar recovered from its lows. The FED now has a 70% likelihood of raising interest rates in May, which is higher in surveys than it was 10 days ago. Low inflation and tight labour markets force the FED to increase rates by 25 basis points in May.

On the back of risk-off sentiment and higher U.S. treasury rates, the U.S. dollar had a strong Monday, rising by more than 0.65% to 102.75 despite thinner liquidity and lower trading volume as European markets were closed for the Easter holiday. Despite growing macro headwinds, such as more restrictive credit conditions for households and businesses, bond yields continued their recovery that began on Friday after the latest U.S. nonfarm payrolls report showed that job gains remained remarkably strong last month, with U.S. employers adding 236,000 workers versus 239,000 expected. The robust labour market may provide the Fed reason to keep hiking interest rates in the foreseeable future, suggesting a pause is not likely in May. Even though the baseline scenario envisaged no change 10 days ago, traders now see a greater than 70% chance of a 25 bp raise at next month’s FOMC meeting.

Despite the fact that investors seem to be leaning in favour of the Fed continuing its tightening campaign, the possibility of a pause should not be discounted, especially given concerns that March employment data may be exaggerating strength by failing to account for the full impact of the banking sector turmoil that led to the failure of two regional banks. The March inflation report, due out on Wednesday, will be a key piece of information in determining the central bank’s next move. According to projections, annual core inflation is expected to rise to 5.6% from 5.5% in February, while annual headline CPI is predicted to have dropped to 5.1% from 6.0%. Inflation measures need to surprise on the downside and show compelling signals of downshifting across categories for markets to shift towards more dovish monetary policy expectations. Given the volatility of recent markets, we can’t rule out the possibility of this happening. On the other hand, everything is up in the air if inflationary factors don’t moderate noticeably and pricing pressures persist. The market may price in a somewhat higher peak rate and discount rate decreases for the second half of the year if they anticipate further rate hikes beyond the May meeting. The dollar index would likely rise as a result of this.

EURUSD Analysis

EURUSD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

While the United States and China may exert pressure on Taiwan, according to French President Emmanuel Macron, Europe is a third power and would not cave to such pressure. We are keeping an eye on strategic shifts in reliance on both the military and the economy.

French President Emmanuel Macron has been panned for his comments that Europe should not become a vassal and should stay out of any conflict between the United States and China over Taiwan. The French leader made the comments in an interview while returning home after a three-day state visit to China, where he was given a red carpet greeting by Chinese President Xi Jinping. When asked about the world order by reporters from Les Echos and Politico, Macron said Europe should be a third power alongside the United States and China. Although Macron’s comments on Taiwan sparked fury and worry on both sides of the Atlantic, they did reinforce his long-term goal of strategic autonomy for Europe, which is to avoid military and economic ties.Worse yet would be the belief that Europe must follow the lead of the United States and China on this issue, adopting their pace and responding more aggressively than is warranted. He continued by saying that it would be a mistake for Europe to get sucked into crises that are not its own, given the increased independence it has enjoyed since the Covid epidemic. We will be reduced to vassals of the American and Chinese duopoly if their fight escalates quickly, but we have the potential to become the third pole if we are given a few years to build this capability. According to Macron, the need for strategic autonomy in Europe is now universally understood, and Europe’s influence has never expanded so quickly as it has in recent years. The US Inflation Reduction Act, a $369 billion green subsidy package, and Europe’s reliance on the dollar were among issues he raised as concerns. However, he noted that Europe has responded swiftly by developing our European IRA, which he defined as initiatives to increase domestic production of green technology and strategic raw commodities. And he hinted that his meeting with Xi had been fruitful in challenging China’s apathy towards Russia. According to Macron, the talks with China were intended to strengthen mutual understandings over the conflict in Ukraine. Politico reports that as a condition of providing the interview, the Élysée presidential palace vetted Macron’s statements before publication and insisted on the removal of paragraphs where Macron had spoken even more candidly about Taiwan and Europe’s strategic autonomy.Senator Marco Rubio, a Republican from the United States, said in a social media post that linked to the Politico interview that if Macron spoke for all of Europe, the United States should consider focusing its foreign policy on controlling China and letting Europe handle the crisis in Ukraine.

Former Republican presidential nominee Marco Rubio said he was in favour of US aid for Ukraine, but that Europe should reconsider its stance on Taiwan if it was going to take sides with China: Maybe, we should basically say we are going to focus on Taiwan and the threats that China poses, and you guys handle Ukraine and Europe. Using the caveat from Politico, Rubio claimed that Macron had made even more offensive remarks before they were removed by the Élysée.According to an editorial published by The Wall Street Journal, the French president’s remarks were counterproductive because they would weaken the deterrence of the United States and Japan against China in the western Pacific and give cover to lawmakers in the United States who want to diminish American commitments in Europe. If Vice President Biden is still conscious, he should question Mr. Macron if he is working to ensure Trump’s re-election. The French president does not represent EU policy, one MEP emphasised. While Macron claims Europe should and we Europeans, he is just speaking for France and not Europe as a whole. The world has changed in the previous 14 months, the source added, making it surprising for Macron to propose Europe as a third force in the global order in April 2023. This is because the Russian invasion of Ukraine has cast doubt on Europe’s ability to do so. German centre-right lawmaker and former chair of the Bundestag’s foreign affairs committee Norbert Röttgen remarked that Macron had made Xi Jinping’s visit to France a public relations triumph. He is becoming increasingly isolated in Europe due to his concept of sovereignty, which he defines in terms of demarcation rather than partnership with the USA. Macron’s trip to China was a complete disaster, according to the chairman of the European Parliament’s China delegation, Reinhard Butiköfer. The German Green MEP, who has been sanctioned by Beijing for his stance on human rights in Xinjiang, stated that Macron’s pipe dream of EU strategic autonomy and becoming the third superpower was beyond the pale. He added that the European Commission president, Ursula von der Leyen, had shown a better alternative. While Macron was praised in Brussels for inviting Von der Leyen to join him in Beijing, the reality of the visit only highlighted China’s attempts to divide and rule. While China rolled out the red carpet for Macron with a state banquet and military parade, Von der Leyen was given a chilly reception and excluded from the pageantry. Supporters of Macron said the interview contained little that was new to either him or French foreign policy since Charles de Gaulle. Gérard Araud, a former French ambassador to Washington and the UN, said Macron had started an important debate at a time when the temptation exists to consolidate into a western bloc under American direction assured to be on the side of ‘good, adding: It would be a mistake to give into this. The row recalls previous controversies such as when Macron declared in 2019 Nato was experiencing brain death, or when last year he infuriated central and eastern European allies by saying Russia would need security guarantees when the time came to negotiate a peace settlement with Ukraine. Mujtaba Rahman, the head of Europe at the research firm Eurasia Group, said the timing of Macron’s latest comments was poor. To make these remarks as Chinese military exercises encircled Taiwan and just after his state visit to China was a mistake. It will be interpreted as appeasement of Beijing and a green light to Chinese aggression. Rahman added that Macron’s interview was being seen as a parting gift to Xi another doomed attempt to sweet-talk an autocrat and suggested the French president may have been trying to boost his poll ratings in France by emulating De Gaulle. More likely, it was just Macron being Macron, thinking ahead in an interesting way but not measuring the immediate political impact.

AUDUSD Analysis

AUDUSD is moving in the Descending channel and the market has reached the lower high area of the channel.

The fact that the latest Westpac Consumer Confidence Index for Australia is better than projected bodes well for the country’s domestic economy. Lower-than-anticipated inflation statistics from China indicates the country’s economy is still trying to recover from the pandemic. China needs additional aid to help its economy recover from the pandemic. China eliminates nearly all tariffs on Australian barley but raises them on wine, coal, and timber.

On this Tuesday following the Easter holiday, the Australian dollar shows some strength, rising by about 0.50% against the United States dollar. Following last week’s robust US employment report, markets have priced in a 25 basis point increase in interest rates for the Fed’s next May meeting. The Australian consumer confidence index saw a huge jump in April, hitting its best levels since June 2022, data showed this morning. From a consumer’s point of view, the study shows that the economy is doing well. After the pandemic, China’s economy has been struggling, and the country’s inflation and PPI data have both fallen short of expectations. The Chinese economy and consumer demand could benefit from additional monetary policy easing if the government decides to go that route. Despite this, the AUD benefited from a settlement between China and Australia in 2020, when diplomatic tensions were high and China imposed tariffs on Australian barley. As China is Australia’s major trading partner, reducing tariffs on coal, wine, and lumber could pave the way for further reductions in other commodity tariffs. Since the US CPI report is coming the next day, attention will turn to the US as the trading day winds down, namely to Fed speakers and their reaction to the present labour market/inflation dynamic.

EURNZD Analysis

EURNZD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

The amount of greenhouse gas emissions from New Zealand exceeds what the global pollution centre expected. If New Zealand is unable to cut its carbon usage, the Carbon Bill is predicted to be $24 billion in 2030. According to carbon usage norms, the $3 to $4 billion utilisation level is lower.

A Government analysis estimates that New Zealand would need to spend $24 billion between now and 2030 to satisfy its international climate change commitments. This would be the case if New Zealand continued on its current path of increasing greenhouse gas emissions and if the worldwide carbon price for offsetting any emissions exceeding the country’s target was high. With a much lower carbon price, the total cost drops to slightly over $3 billion, according to the report, which acknowledges the high uncertainty surrounding international markets. A climate change expert, however, warns that rising demand for carbon credits makes it unlikely that prices will remain low and that domestic reductions, despite their high initial cost, may turn out to be a bargain in the long run. As part of international efforts to keep warming below 1.5 degrees Celsius, New Zealand has pledged to cut its net greenhouse gas emissions by 50 percent below gross emission levels in 2005 by 2030 under the Paris Agreement.To put it another way, New Zealand must limit its emissions to below 571 Mt CO2e between 2021 and 2030 if it is to achieve this goal. New Zealand released 84 Mt CO2e in the year ending in June 2021, which is equivalent to almost 16% of the country’s annual budget. If New Zealand’s emissions exceed its budget, it must engage in offshore mitigation, also known as buying carbon credits, to make up the difference. Officials from Treasury and the Ministry for the Environment compiled the different future economic and fiscal implications of climate change for New Zealand into the paper Ng Krero huarangi Me Te hanga: Climate Economic and Fiscal Assessment 2023, which was released this month.

It comprises the costs of adapting to the effects of climate change, the costs of taking action to cut emissions and the costs of not making those international responsibilities. It draws attention to the fact that agriculture and fishing are only two of many industries that will be struck particularly severely by rising emissions prices and a changing environment. It also highlights how low-income households, especially Maori, will feel the effects of a low-emissions economy and the physical hazards of climate change. The authors state that domestic and offshore mitigation will very probably be required to achieve the 2030 target, or first nationally defined contribution. Cost estimates for making the necessary offshore mitigation purchases to fulfil that pledge are analysed in the report. According to the authors, these prices constitute a substantial financial threat in every scenario taken into account. There was considerable difference, however, in both the amount of domestic emission reduction achieved by New Zealand and, more importantly, the cost of any foreign emission reductions achieved by New Zealand. Since many international markets are still developing, the authors acknowledged that it was impossible to predict what the final cost of these cuts would be. Depending on the trajectory of domestic emissions, New Zealand may be looking at a bill of $7.7 billion to $9.9 billion if the international price matched the average of current prices for well-established international carbon markets. The cost to New Zealand might be between $3.3 and $4.2 billion using a carbon price projected by the International Energy Agency for emerging and developing economies of around $41 per tonne of CO2e on average.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/