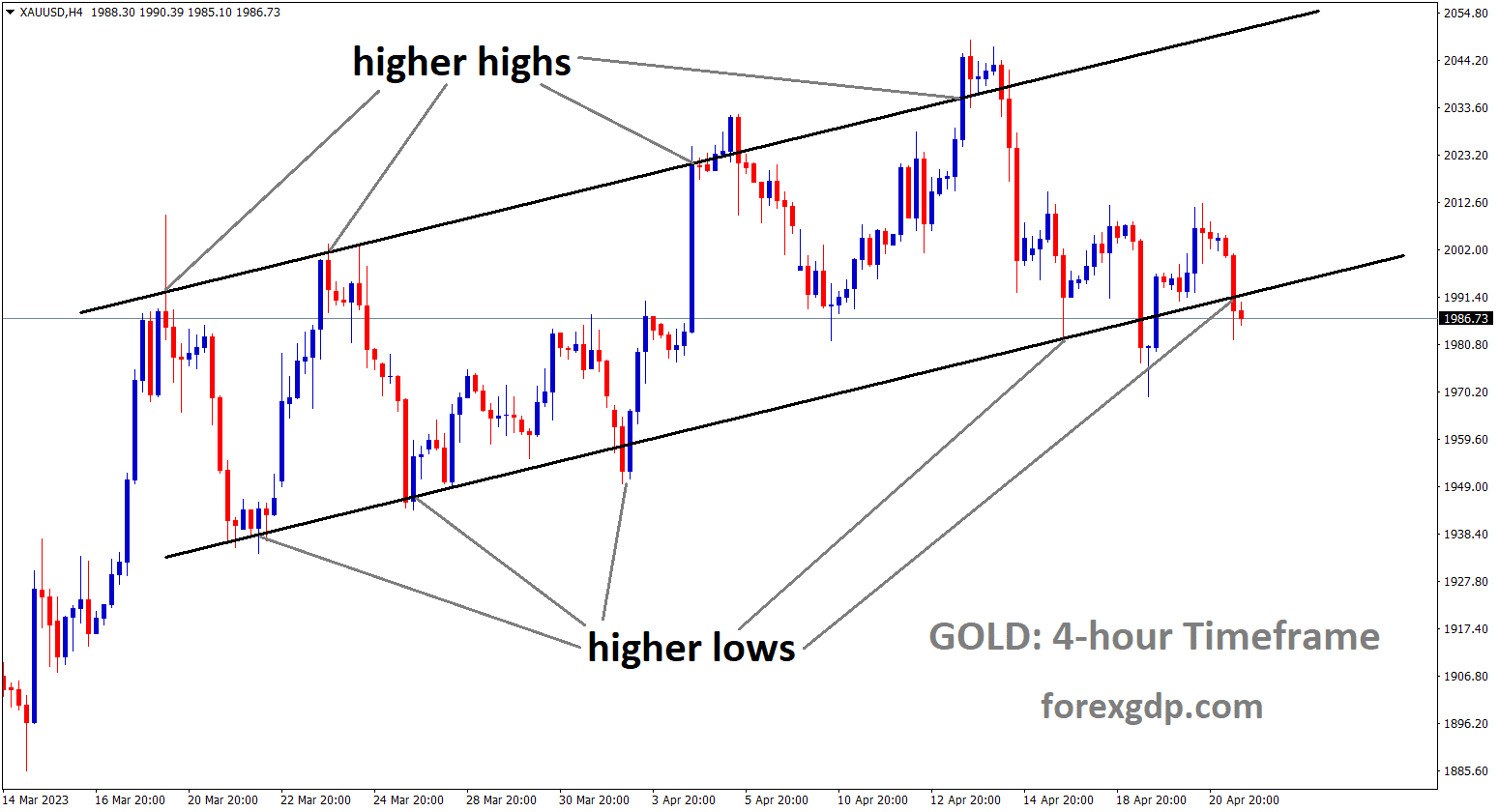

GOLD Analysis

XAUUSD is moving an Ascending channel and the market has reached the higher low area of the channel.

During the Asian session, the price of gold is moving back and forth above the psychological support level of $2,000.00. Investors are waiting for the preliminary United States S&P PMI data to be released for new momentum as the precious metal has swung sideways to close to $2,005.00 after a modest uptrend. Following three consecutive settlements that were bearish, S&P500 futures have made some gains during the Asian session. Market sentiment was negatively impacted by Tesla’s dismal revenue guidance as a result of Elon Musk’s price-cutting campaign. The US Dollar Index has continued to decline, approaching 101.77. The USD Index is consolidating, having spent the previous three trading sessions in a range between 100.90 and 102.03, inside the forest. A move that crosses the aforementioned boundary will be viewed as decisive.

US Treasury yields are also being impacted by the weak USD index. In spite of an increase in weekly jobless claims, demand for US government bonds has increased. Compared to the consensus estimate of 240K, the number of people claiming unemployment benefits increased to 245K. This indicated a slowdown in the tight labour market and gave rise to expectations that the Federal Reserve (Fed) would refrain from raising interest rates after its monetary policy meeting in May. The impact of increasing interest rates from the Fed on the scope of economic activity will be determined by the release of the preliminary US S&P PMI data in the future. Manufacturing and services PMI are predicted to decline to 49.0 and 51.5, respectively. The US Dollar may suffer greatly if preliminary PMI readings are lower than anticipated.

USDJPY Analysis

USDJPY is moving an Ascending channel and the market has reached the higher low area of the channel.

In the early hours of the European session on Friday, the USDJPY pair drifts lower for the second straight day, reaching a four-day low in the vicinity of the 133.70 area. The Japanese Yen receives a goodish boost from a number of reasons, which pulls the USD/JPY pair away from the multi-week high it reached on Wednesday, in the 135.10–135.15 range. Data released earlier this Friday showed that Japan’s National Consumer Price Index decreased from 3.3% YoY in February to 3.2% YoY in March. However, this was significantly more than the 2.6% predicted and the Bank of Japan’s target range. In addition, the Core CPI, which excludes volatile food and oil prices, increased from 3.5% in February to 3.8% YoY, exceeding forecasts for a reading of 3.4%. In turn, this points to expanding pricing pressure in the third-largest economy in the world and maintains hopes that the BoJ will start winding down its enormous stimulus programme later this year. In addition, the relative safe-haven character of the JPY and the offered tone around the USDJPY pair are both benefited by a generally lower tone surrounding the equities markets. Investors are still concerned about economic challenges brought on by increased borrowing costs, which is having a negative impact on investor sentiment globally.

The US Treasury bond yields continue to decline as investors seek safety, which causes the US Japan rate divergence to close and supports the JPY even more. Nevertheless, the US Dollar benefits from the growing consensus that the Federal Reserve will keep rising interest rates, which may assist to keep the major’s decline in check. This calls for considerable care while making aggressive negative trades and before setting up for any significant intraday slide. Traders are now anticipating the publication of the US flash PMI prints, which are scheduled for later in the early North American session. This will affect the USD price dynamics and give the USDJPY pair some momentum, along with the US bond yields. The demand for the safe-haven JPY will also be influenced by the general risk attitude, which will help create short-term trading opportunities on the penultimate day of the week.

USDCAD Analysis

USDCAD is moving an Ascending channel and the market has reached the higher high area of the channel.

In the Asian session, the USDCAD pair reached a new weekly high of 1.3500. The Canadian dollar’s two-day winning streak has been extended as it surpassed Thursday’s high of 1.3490. A sharp decrease in oil prices has put tremendous pressure on the Canadian dollar. The price of black gold has plummeted as more rate increases from international central banks will significantly reduce demand for oil worldwide. Prior to the announcement of the preliminary US S&P PMI data, the US Dollar Index has shifted sideways around 101.80. In order to plan a workable course of action, investors want to carefully examine how the Federal Reserve’s (Fed) increased interest rates will affect economic activity. The Manufacturing PMI will arrive at 49.0, which is less than the previous report of 49.2, according to consensus. The Services PMI is likewise assessed as being lower at 51.5 compared to the originally reported value of 52.6.

S&P500 futures are currently indicating modest advances throughout the Asian session. Before investing money into the S&P500, investors should exercise caution because earnings season is gaining up steam and midcap companies will take the lead. US Treasury yields are being impacted by the USD Index’s mediocre performance. On US Treasury bonds with a 10-year maturity, the alpha has fallen below 3.53%. Prior to the release of retail sales statistics, the Canadian dollar is anticipated to stay active. In contrast to the 1.4% rise seen in January, the street expects a 0.5% decline in monthly retail sales figures. Tiff Macklem, governor of the Bank of Canada, is concerned that a labour shortage and strong consumer demand may push the institution to increase interest rates further. For the BoC, a decline in retail sales statistics would be a relief.

USDCHF Analysis

USDCHF is moving in Descending channel and the market has reached the lower high area of the channel.

Prior to comparable official economic data, the S&P Global Purchasing Managers Index analyses private sector business activity in major economies on a monthly basis. Today, the business will release the United States’ April preliminary PMI figures for manufacturing and services.After the pandemic-related setback that caused the globe to come to a standstill three years ago, businesses throughout the world are still working to recover. The central banks’ moves to tighten their monetary policies took a toll on businesses, with activity declining throughout the majority of 2022. It has been a difficult road with back and forths in the middle.

But in March, unexpectedly strong demand, particularly in the services sector, caused economic activity in the US to rebound. The S&P Global preliminary US Composite PMI increased from 50.1 in February to 53.3 in March. The Manufacturing PMI increased to 49.3 from 47.3 while the Services PMI Index increased to 53.8 from 50.6. Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, cautioned that inflation remains a troubling problem despite the encouraging rebound in business activity last month, adding that “the purchasing managers surveyed indicated that selling prices were increasing at a quicker rate despite lower costs in the manufacturing sector and that the services sector is also raising prices, primarily as a result of faster wage growth.”

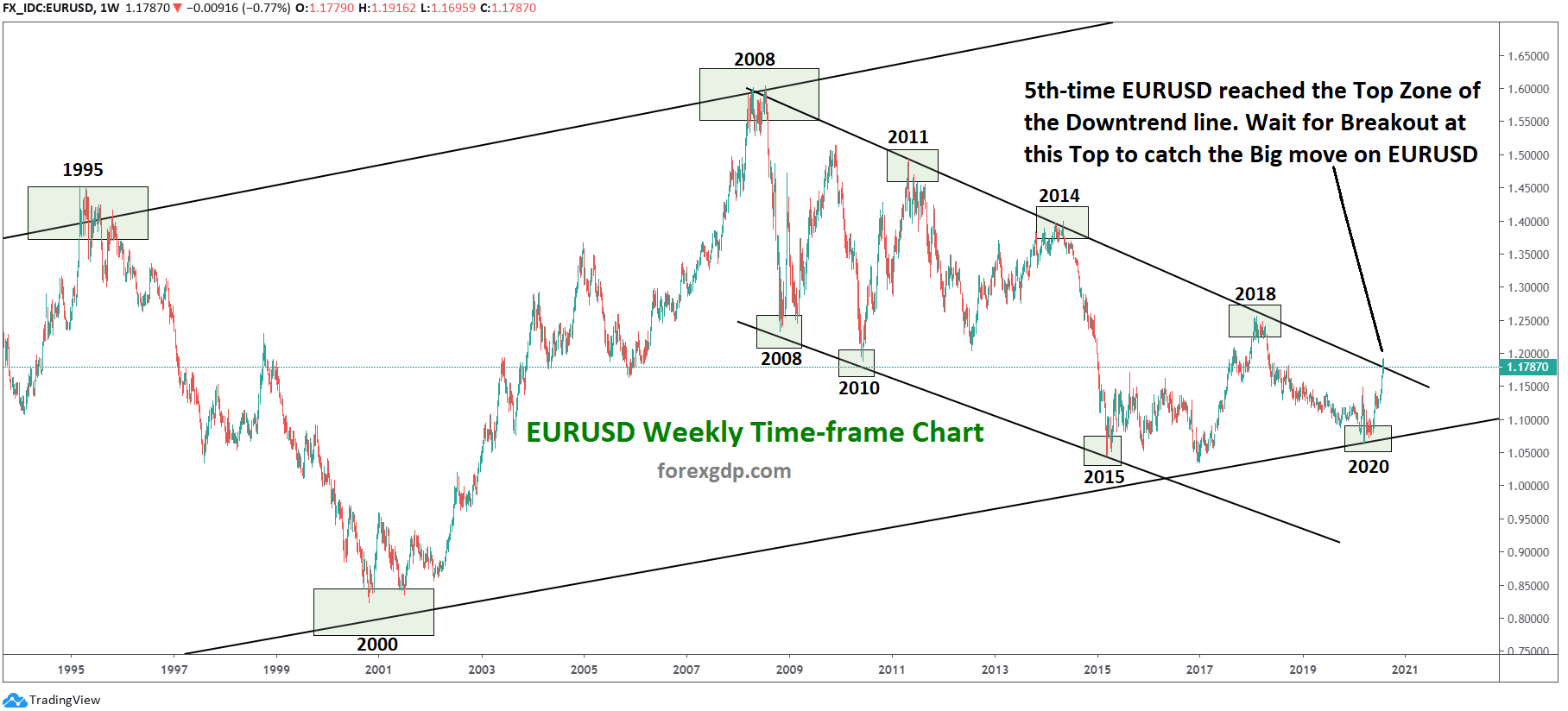

EURUSD Analysis

EURUSD is moving an Ascending channel and the market has reached the higher low area of the channel.

According to the most recent factory activity report from S&P Global research, the activity of the Eurozone’s manufacturing sector unexpectedly decreased further in April. The Eurozone Manufacturing Purchasing Managers Index (PMI) was 45.5 in April as opposed to the 48.0 predicted and 47.3 recorded in the prior month. A 35-month low was reached by the index. In April, the bloc’s Services PMI increased to 56.6 from 55.0 in March and 54.5 estimates, setting a 12-month high. In April, the S&P Global Eurozone PMI Composite increased to 54.4 from the previously reported 53.7. The index hit a new 11-month high.

GBPUSD Analysis

GBPUSD is moving an Ascending channel and the market has reached the higher low area of the channel.

On the final day of the week, the GBPUSD pair experiences some selling pressure and continues to trade in an offered range into the early European session. The pair is currently trading in the 1.2425–1.2420 range, down more than 0.15% on the day, and shows minimal reaction to the most recent UK macroeconomic data. This Friday, the UK Office for National Statistics revealed that domestic retail sales fell by 0.9% in March, which was less than projected and substantially reversed the increase seen the previous month. Furthermore, versus the 1.4% increase reported in February, sales excluding fuel also fell short of consensus expectations and decreased by 1% during the reporting month. This in turn weakens the British Pound, which together with a slight increase in the US Dollar serve as a drag on the GBPUSD pair. The Federal Reserve’s (Fed) potential for more policy tightening and a softer risk tone provide some support for the safe-haven dollar. In reality, the recent hawkish comments by FOMC officials have given the markets more confidence that the Federal Reserve will raise rates by 25 basis points in May and have been pricing in a slim likelihood of another rate hike in June. As a result, investors’ desire for riskier assets is dampened. This fuels concerns about economic headwinds brought on by rising borrowing costs.

But given the increasing odds of another Bank of England interest rate hike, the downside for the GBPUSD pair appears muted, at least temporarily. The persistently high inflation should continue to put pressure on the BoE to hike interest rates further, especially in light of the better UK wage growth figures announced earlier this week. It is therefore wise to hold off on determining whether this week’s rally from the strong horizontal support of 1.2350 has peaked until there has been significant follow-through selling. However, the GBPUSD pair is still expected to post small weekly gains as market players wait for the publication of the flash PMI prints from the US and UK to provide a new boost. This will affect the USD price dynamics and create short-term trading possibilities around the GBPUSD pair as we approach the weekend, along with US bond yields and the general risk attitude.

AUDUSD Analysis

AUDUSD is moving an Ascending channel and the market has reached the higher low area of the channel.

In the early London session, the AUDUSD pair’s negative movement has reached close to 0.6714. As the US Dollar Index has showed a rebound move after forming a foundation around 101.80, it is anticipated that the Australian asset will move even further south. The USD Index has increased to close to 101.86 and is predicted to go even further. Despite being cautious, investors are putting money into the USD Index. After three bearish trading sessions to avoid volatility sparked by the quarter-end result season, S&P500 futures are flat in early Europe. The US Treasury yields are still battling for recovery in the meantime. The return on 10-year US Treasury bonds is currently 3.52% or such. The Financial Times’ report that China is developing sophisticated cyber weapons to “seize control” of adversary satellites and render them useless for data signals or surveillance during wartime has increased interest in the USD Index as a haven currency.

Federal Reserve policymakers are unwilling to moderate their hawkish stance on interest rates despite the fact that manufacturing activity in the United States has been declining for the past few months and labour market conditions have cooled further amid rising weekly jobless claims. According to Reuters, Cleveland Federal Reserve President Loretta Mester underlined on Thursday that the Fed has to do more to address the US inflation rate that is still too high. “Fed will need to hike policy rate to over 5% and hold there for a while, he continued. Due to the conflicting preliminary S&P PMI (April) figures, the Australian Dollar is under a lot of pressure. Manufacturing PMI dropped significantly from its previous reading of 49.1 and the consensus of 48.8 to 48.1. While the Services PMI increased from the previous publication of 50.7 to 52.6.

NZDUSD Analysis

NZDUSD is moving in Descending channel and the market has reached the lower low area of the channel.

On Friday, the NZDUSD pair experiences significant selling pressure for the second straight day, falling to a five-week low in the early going of the European session. The pair is under pressure from a number of variables at the moment and is trading in the range of 0.6135–0.6130, down more than 0.60% for the day. The Reserve Bank of New Zealand’s less hawkish approach is necessitated by the weaker domestic consumer inflation statistics that were reported on Thursday. On the other hand, the Federal Reserve (Fed) is anticipated to keep raising interest rates, which, along with a weaker risk tone, favours the safe-haven US Dollar and pushes the NZDUSD pair lower on the final trading day of the week. The markets appear to be certain that the Federal Reserve will increase rates by 25 basis points in May and have factored a slim possibility of another rate increase in June. The recent hawkish remark from numerous Fed members, who believe that inflation is still at unfavourable levels and that monetary policy needs to be tightened still, confirmed the bets. This more than makes up for Thursday’s gloomy US macro data.

Meanwhile, concerns about economic headwinds brought on by rising borrowing prices are exacerbated by the likelihood of further policy tightening by the US central bank. As a result, investors’ desire for riskier assets is dampened, which further discourages investment in the risk-averse Kiwi. But if US Treasury bond rates continue to fall, the USD’s gains are limited, and the NZDUSD pair’s losses might also be constrained. The release of the US flash PMI prints, which are scheduled for later in the early North American session, is now anticipated by the market. On the final day of the week, this will affect the USD price dynamics and create short-term trading possibilities around the NZDUSD pair, along with US bond rates and the general risk attitude.

CHFJPY Analysis

CHFJPY is moving an Ascending channel and the market has reached the higher low area of the channel.

The Bank of Japan stated that the overall stability of the Japanese financial system has been maintained in its semi-annual report on the financial system, which was published on Friday. Despite the tightening of financial conditions globally, Japanese banks have adequate capital bases to carry out financial intermediation activities effectively. Japan’s financial system has been strong and robust, despite increased anxiety about the financial industry in the United States and Europe as a result of u.s. bank failures in March. Tail risks continue to be a concern, therefore caution is advised. Future developments are still very unpredictable because of the uneasy financial and capital markets. Although some loans have a significant credit risk, overall the quality of the domestic and international loan portfolios of banks has remained good. In order to guarantee the stability of Japan’s financial system, it is necessary to assess the risks of financial system contraction and overheating and take the necessary precautions.

Crude Oil Analysis

Crude Oil is moving in Descending channel and the market has reached the lower high area of the channel.

With both Brent and West Texas Intermediate falling in the morning trading, crude oil continued its two-day losing run. Weak U.S. economic statistics will cause crude oil to see significant losses over the course of the next week, barring an unexpected turn of events. Prices are declining despite the fact that the most recent data from China indicated strong demand as the first quarter’s GDP growth exceeded estimates. After the disappointing U.S. economic data and anticipation of interest rate increases, market mood remained negative, escalating concerns about a potential recession that might reduce oil consumption, a Nissan Securities analyst told Reuters. For the upcoming week, WTI is anticipated to trade in the $75-$80 region as investors try to predict whether U.S. petrol demand will rise in anticipation of the summer driving season and whether China’s oil demand will actually increase in the second half of the year.

Traders were cited by Bloomberg as saying that an oil price correction might result in even worse declines. The abrupt and significant price increase that occurred when OPEC+ announced its output cut was the reason for the correction.

According to Dennis Kissler, senior vice president of trading at BOK Financial Securities, “most traders get very nervous when they see large technical chart gaps like we’re seeing in the futures.” The market will almost always move downward after such a gap appears. Then there are the rate increases that economists anticipate the U.S., UK, and eurozone central banks to announce early next month. Higher interest rates tend to strengthen currencies and increase oil prices, which has an impact on demand. Speaking of oil consumption, China’s demand is about to decline as the season for refinery maintenance begins. Meanwhile, according to experts surveyed by Reuters, China may lower gasoline export restrictions when it announces the next batch because of rising domestic demand, which would lessen the need to export as much fuel to support the economy.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/