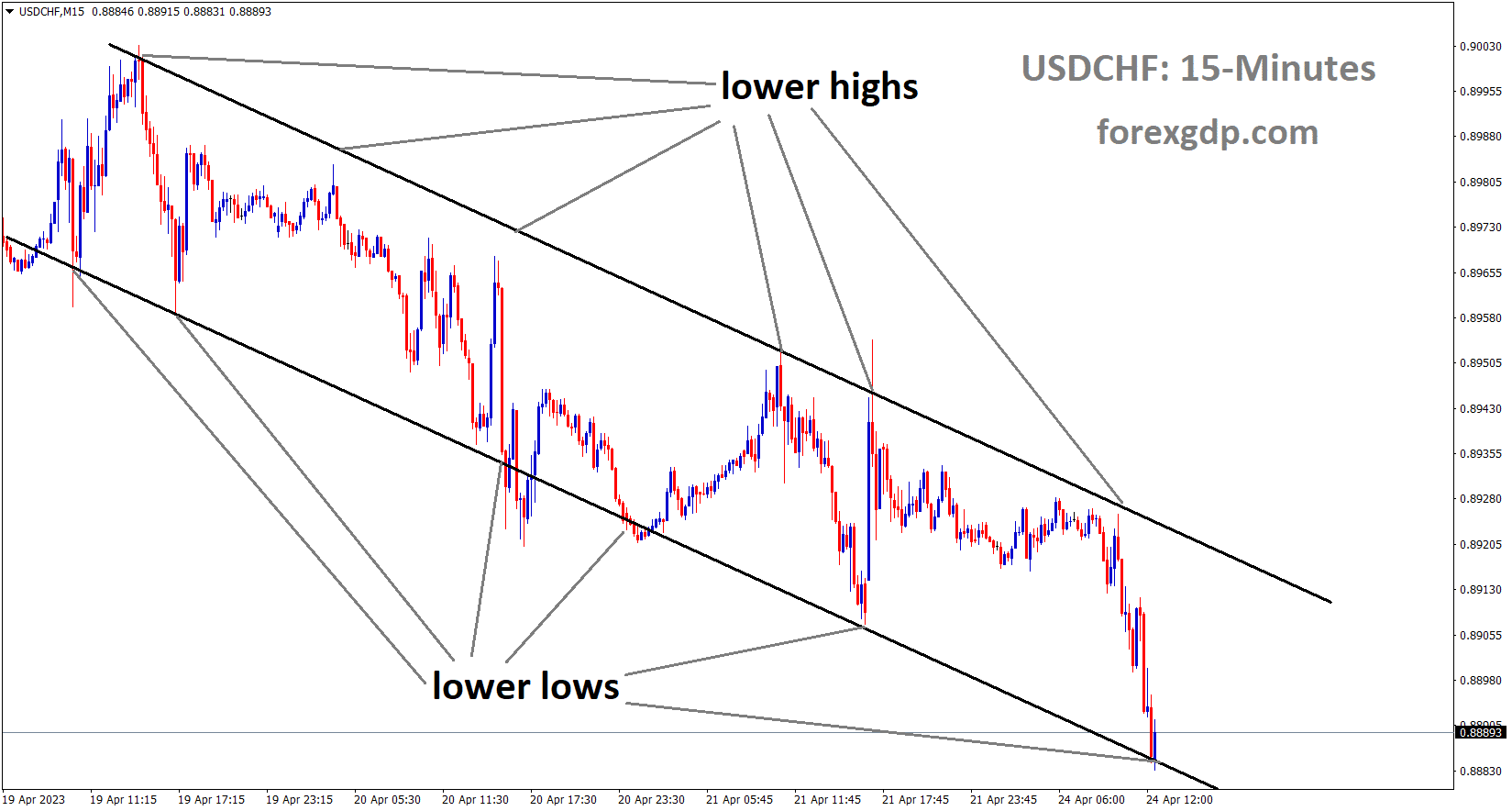

USDCHF Analysis

USDCHF is moving in the Descending channel and the market has reached the lower low area of the channel.

61 billion Swiss francs ($68 billion) in assets left Credit Suisse in the first quarter, and outflows were still occurring, the bank said on Monday. This highlights the difficulty UBS Group will have in saving its rival. In the quarter, customer deposits fell by 67 billion Swiss francs, and the bank highlighted that many time deposits that had reached maturity had not been renewed. As of April 24, 2023, these withdrawals “have moderated but have not yet reversed,” according to Credit Suisse, which also noted that the majority of the funds leaving the bank came from its wealth management division and occurred in all geographical areas. The bank’s net asset outflow came after customers withdrew 110.5 billion francs in the fourth quarter. As its state-engineered marriage with UBS is anticipated to be consummated shortly, the 167-year-old bank’s results announcement is likely to be the last. If the two strategically vital systemic banks can be successfully integrated, it will have a significant impact on Switzerland’s reputation as a reliable international financial centre, particularly for the exceedingly affluent. In the early trade, shares of UBS and Credit Suisse were up by 2%, with some analysts remarking that the withdrawals were not as bad as anticipated.

Others, however, deemed the magnitude alarming. According to a note to clients from London-based analyst Thomas Hallett at KBW, Credit Suisse’s ability to generate revenue appears to have been severely affected. “The deal could well remain a drag on UBS operating results unless a deeper restructuring plan is announced,” Hallett said. At the end of March, the flagship wealth management division’s managed assets were 29% lower than they were at the same time last year, totaling 502.5 billion francs. As soon as scandal-plagued Credit Suisse became embroiled in the market turbulence brought on by the failure of American lenders Silicon Valley Bank and Signature Bank, clients began quickly withdrawing funds. UBS consented to acquire Credit Suisse for 3 billion Swiss francs in stock and up to 5 billion Swiss francs in losses as part of the hastily put together rescue package by Swiss regulators. State financial guarantees of 200 billion francs are also part of the agreement. After paying back 60 billion Swiss francs in borrowings from the central bank, Credit Suisse reported having 108 billion francs in net borrowings at the end of the first quarter. It has since repaid an additional $10 billion.

The controversial write-down of AT1 bonds to zero and a gain from the sale of a sizable chunk of its Securitized Products Group to Apollo Global Management, however, were the main reasons for the bank’s pre-tax profit, which came in at 12.8 billion francs. It had a loss of 1.3 billion francs for the quarter after accounting for these aspects. Credit Suisse stated that the group is also anticipated to make a deficit this year and that the wealth management and investment banking divisions will continue to operate at a loss in the second quarter. UBS will release its first-quarter earnings report on Tuesday. The bank has stated that it anticipates the purchase to result in $8 billion in cost savings by 2027. It said on Monday that Christian Bluhm, whose departure had already been announced, would stay on as its chief risk officer for the foreseeable future to work on the acquisition. Other significant information from Credit Suisse’s report on Monday is as follows: – Operating expenses rose 30% over the prior quarter, according to the bank, which was primarily attributable to a goodwill impairment charge and increases in compensation and benefits.

In response to uncertainty regarding the future of the Credit Suisse subsidiary in Switzerland, private clients withdrew 6.9 billion Swiss francs from the bank’s Swiss division. The bank employed just over 48,000 full-time workers at the end of the first quarter, a 5% decrease from end-December ($1 = 0.8920 Swiss francs). Credit Suisse’s proposed $175 million acquisition of Michael Klein’s investment banking unit was cancelled by mutual agreement.

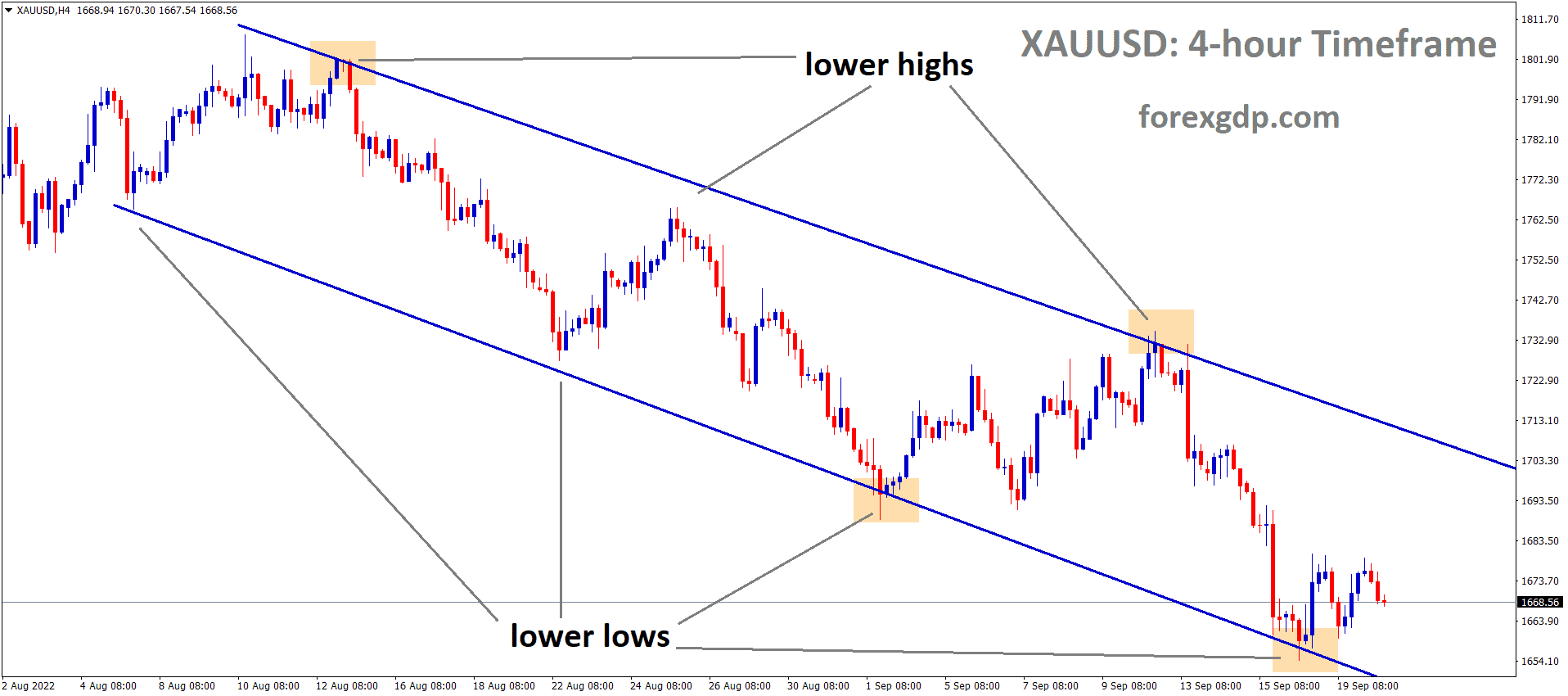

GOLD Analysis

XAUUSD Gold price is moving in the Descending channel and the market has reached the lower high area of the channel.

The bar for a sustained increase is getting higher, according to recent developments on the technical charts of gold, as US inflation stays stubbornly high even as the economy shows indications of resiliency. The yellow metal’s path of least resistance, however, continues to be sideways to upward until it breaks below important support. According to information made public on Friday, US corporate activity reached an 11-month high in April, indicating that the economy is coping with the rise in interest rates. Fair enough, the survey results from Friday might be exaggerating the true situation of the economy. Hard data that has been made public suggests that the economy is weakening, as evidenced by the employment situation and retail sales, precisely as bank credit policies are beginning to hurt individuals and small companies. Data on US GDP growth for the January-March quarter, which are due on Thursday, are now in the spotlight. Growth is predicted to have fallen to 2% on-quarter from 2.6% in the previous quarter.

USDJPY Analysis

USDJPY is moving in the Descending channel and the market has reached the lower high area of the channel.

In the Tokyo session, the USDJPY pair is attempting to overcome the nearby barrier of 134.50. The major has gained momentum as a result of new Bank of Japan Governor Kauo Ueda’s reiteration of the importance of maintaining an expansionary monetary policy. BoJ Ueda is adamantly in favour of maintaining the ultra-loose monetary policy that has been in place for a decade in the hope that Japan’s inflation will peak sooner. According to BoJ Governor, households have borne the brunt of increasing import prices more so than anticipated. Japan’s real estate prices are also not anticipated to become significantly overpriced. Japan’s inflation could lessen in the approaching time if there isn’t any cause for it. BoJ Ueda has chosen not to specify the amount of time necessary for fine-tuning Yield Curve Control.

In the meantime, as investor apprehension soars, S&P500 futures are regularly accruing losses during the Asian session. Investors are becoming more stock-specific at the same rate that the quarterly results season is gaining momentum, reflecting a cautious market atmosphere. The US Dollar Index has extended its rebound over 101.80 as the Federal Reserve’s demand for additional rate hikes has grown as a result of encouraging preliminary S&P PMI data issued last week. The United States Durable Goods Orders data will be closely scrutinised going forward. Data on March’s orders for durable goods are forecast to increase by 0.8% rather than decrease by 1.0%. Positive figures on durable goods orders will signal strong future demand, which could increase the demand for labour.

USD Index Analysis

US Dollar index is moving in the Descending channel and the market has fallen from the lower high area of the channel.

In early Asian trading, the US dollar is slightly weaker against the majority of the major currencies. The US Dollar Index, or DXY, is trading unchanged above 101.67, but the recent break over 102.036 sets up a test of the high from April 10 near 102.807, as shown below. As investors get ready for the May central bank meetings, the dollar is struggling as we enter the final week of the month. Fed officials have started sounding a little more circumspect as the Federal Reserve has come under scrutiny. For example, Loretta Mester, president of the Cleveland Federal Reserve, stated that “I anticipate that monetary policy will need to move somewhat further into restrictive territory this year, with the fed funds rate moving above 5% and the real fed funds rate staying in positive territory for some time.”

The amount by which the federal funds rate needs to increase moving forward and how long policy must be restrictive will depend on financial and economic developments. Mester continued by saying that banks started tightening their credit requirements even before the pressures in the financial sector in March. The question that needs to be answered moving forward is whether the stress that the banking sector experienced in March will prompt banks to tighten their loan standards more quickly. Lorie Logan, a Fed, said You are aware that inflation has been far too high. In order to better balance the economy, the Fed increased interest rates by 4.5 percentage points over the past year. “I believe we’re getting close to where we need to be,” said Patrick Harker of the Fed. We need to exercise some caution here so that we don’t simply react to the current level of inflation but also where we anticipate it will go, adding that monetary policy lags. For this reason, I do not support the group that believes that we should just keep raising rates and rates and rates. I believe we need to go more slowly.

SILVER Analysis

XAGUSD Silver price is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

Raphael Bostic of the Fed stated that he supports one more increase and added that “our policy works with the lag.” We will have firmly entered a constrained area. Then, in my opinion, it will be appropriate to let the restricting action finish. Furthermore, it will take some time. There will be no Federal Reserve speakers until Chair Powell’s news conference on May 3. Policymakers at the Federal Reserve are largely expected to raise rates by another 25 basis points at this time, but the emphasis will be on providing advice for the future rate path. Between the May 2-3 and June 13–14 meetings, the Fed will have digested two additional job data, two CPI/PPI reports, and one retail sales report, according to analysts at Brown Brother Harriman. They stated that as of right now, a halt in June might be the most likely result, but it will really rely on how all of those statistics come in. After all of that, only one cut—as opposed to two at the start of last week—remains priced in by year’s end. Powell has stated that rate decreases this year are just not anticipated by Fed policymakers in this regard. We agree.

EURUSD Analysis

EURUSD has broken the Ascending Triangle in Upside.

The German economy is far from the significant rebound, according to institute economist Klaus Wohlrabe, who spoke after the German IFO Business Survey was released.The percentage of German businesses wanting to boost prices has once more decreased. The German economy is not moving forward. Export expectations among industry have increased. Chinese and American economies appear to be supporting German manufacturing. Business sentiment has not been affected by the banking crisis. Since December 2015, there have not been more cancellations in the building business.

GBPUSD Analysis

GBPUSD is moving in an Ascending channel and the market has rebounded from the horizontal support area of the minor Box pattern.

Despite the fact that there won’t be any significant UK statistics this week, the British pound is still strong against the US dollar as of Monday morning. A short review of last week’s events showed elevated inflationary pressures, slight increases in retail sales and PMI scores, and tightening labour market indicators. The hawkish re-pricing of the Bank of England’s (BoE) interest rate prospects (see table below) as a result of the markets’ quite aggressive response now includes almost 3 further rate hikes this year! It appears evident that the BoE may not cut at all this year, even though this is probably an overestimate. It’s possible that the already strict monetary policy will continue to have an effect, which is why I anticipate fewer than three rate hikes this year and will take a more cautious approach before doing so.

According to the economic calendar below, the US is taking the lead this week. a cascade of highly significant data points that will influence the Fed’s rate decision next week. The Fed’s inflation control strategy has been quite one-sided and in favour of raising rates for a longer period of time. However, given that the Fed’s blackout period has started, investors won’t get any new information until May 4th (when the blackout period ends), putting the focus on incoming data. The majority of data points are anticipated to show a faltering US economy, opening the door for more pound gain should this happen.

GBPCAD Analysis

GBPCAD is moving in an Ascending channel and the market has fallen from the higher high area of the channel

Retail sales in Canada decreased 0.2% in February, which was less than anticipated but more than was projected, according to data released on Friday. The CIBC analysts believe that the slowdown in non-auto spending is evidence that rising interest rates are having an effect. For the remainder of the year, they envision the Bank of Canada on pause. Retail spending’s early-year rise appears to be gradually waning; it is anticipated that a mild dip of 0.2% in February will be followed by a sharper decline of 1.4% in March. Although the first estimate for March indicates a significant 1.4% decline, it should be noted that because it was based on replies from only 28% of the companies typically questioned, it is subject to significant revision.

Although the economy as a whole has recently fared better than anticipated, the slowdown in ex-auto retail expenditure volumes indicates that, notwithstanding the excess levels of savings held by families, higher interest rates are indeed having an effect on consumer purchasing decisions. If supply chain problems don’t get worse again, this slowdown in spending should help keep the inflation of goods prices under control, allowing the Bank of Canada to remain on hold until the beginning of 2024 before beginning incremental rate decreases.

EURAUD Analysis

EURAUD is moving in an Ascending channel and the market has reached the higher high area of the channel.

The Reserve Bank of Australia has so far been struggling with data from both domestic and foreign sources after choosing to suspend rates in the previous interest rate meeting. The RBA’s interest rate probability table below has since been ramped up by money markets to include another potential 25 bps hike in 2023, a sharp change from a few days earlier when no such hike was on the table. The most recent RBA minutes indicated that the door remains open to further hikes if needed. The upcoming week is jam-packed with significant events, most of which are slanted towards the US. From an Australian viewpoint, first-quarter inflation is anticipated to be lower on both YoY and QoQ measurements, which would cause the above rate probability chart to flip back to no future raises if inflation turns out to be low. Last week, a strong Chinese GDP helped commodity prices rise as demand projections were upgraded. However, since then, as global recessionary fears have gained traction, things have gotten worse. Lower prices inevitably pressurise the local currency because exports of raw materials have such a big impact on the Australian dollar.

EURNZD Analysis

EURNZD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

In New Zealand, lessened inflationary pressures have allowed policymakers at the Reserve Bank of New Zealand to sigh with relief. According to Statz NZ’s data from last week, quarterly inflationary pressures increased by 1.2% as opposed to the consensus estimate of 1.7% and the previous release of 1.4%. Despite the street expecting a little slowdown from the previous report of 7.2% to 7.1%, annual inflation slowed to 6.7%. Given that the inflation rate has reached an intermediate peak, it is conceivable that RBNZ Governor Adrian Orr would think about pausing the policy-tightening phase.

Francois Villeroy de Galhau, president of the Bank of France and a member of the Governing Council of the European Central Bank, stated on Monday that price stability is the primary responsibility of central banks worldwide, and that the effects of climate change are already felt in terms of activity and price levels. The markets anticipate the ECB to raise interest rates by a quarter point, with a possible 50 bps increase, when it announces its policy decision next week. This week’s reports on inflation and growth in the eurozone are coming.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/