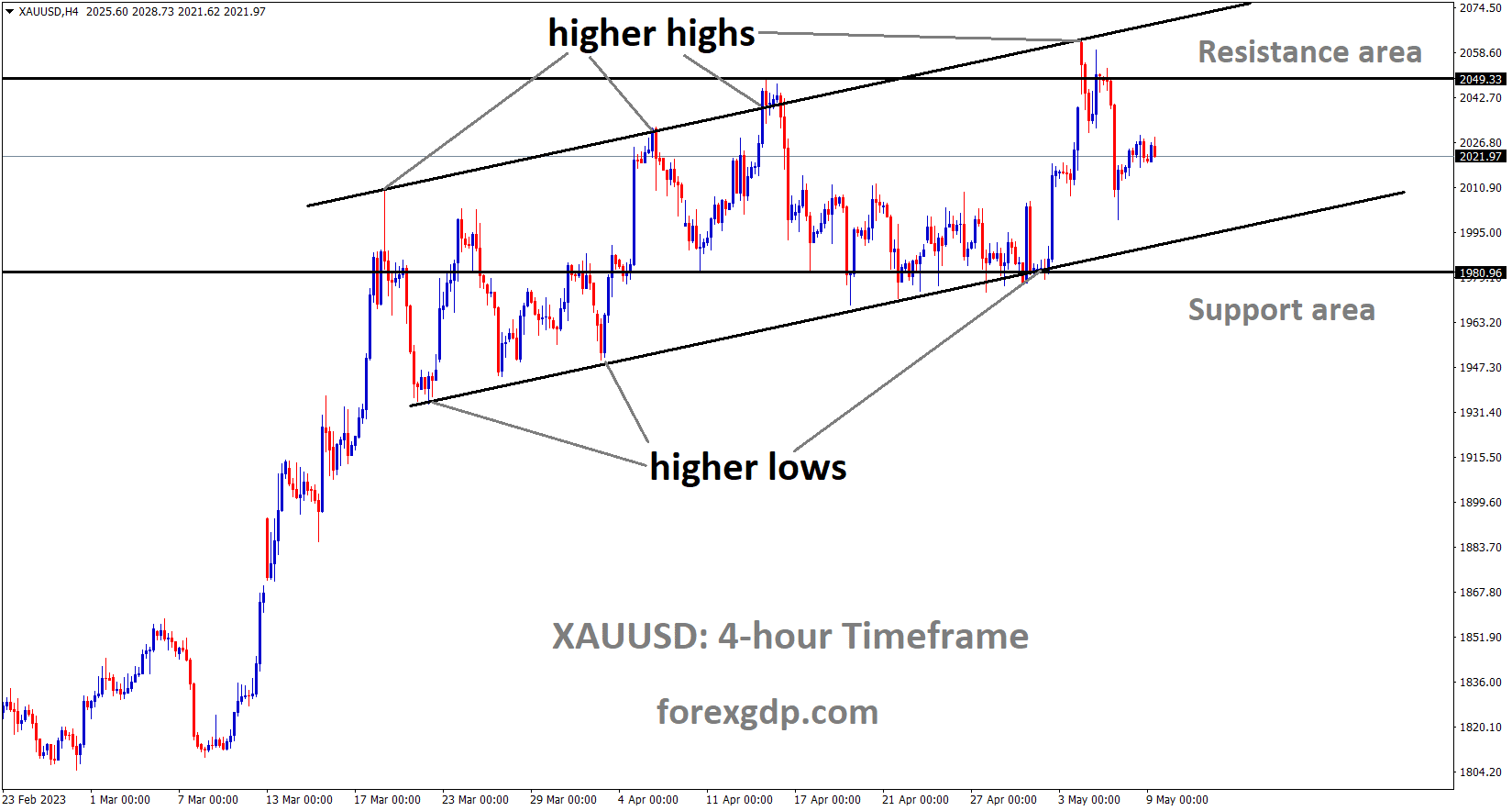

GOLD Analysis

XAUUSD Gold price is moving in an Ascending channel and Box pattern, Market is falling from the higher high area of the channel and resistance area of the pattern.

Following a little increase in US Treasury yield prices as a result of the FED’s 25 basis point rate hike last week, gold prices are currently consolidating.

If the US CPI comes in higher than predicted, which is expected to be 5.0% YoY in April, the US dollar would appreciate.

The threat of a non-yielding asset like gold is increased rate hikes by central banks.

Following a decline on Friday, gold has now stabilised around the US$ 2,020 handle as swings in risk sentiment appear to be driving the price of the precious metal. Since the Federal Open Market Committee increased its target rate by 25 basis points to 5-5.25% last week, Treasury rates have risen slightly across the curve. Last Thursday, the benchmark 2-year note traded as low as 3.66%, but today it is somewhat higher at 4%. On the same day that Treasury yields rose from their lows, gold reached its 33-month high on the COMEX futures market at US$ 2,085.4 before tumbling ever since. Real yields also seem to have recently changed in an inverse correlation to the price of yellow metal. The 10-year rate reached 1.29% overnight, far higher than the previous week’s low of 1.11%.

SILVER Analysis

XAGUSD Silver price is moving in the Box pattern and the market has fallen from the resistance area of the pattern.

The market-priced inflation rate determined from Treasury inflation-protected securities with the same tenor less the nominal yield results in the real yield. As the market anticipates Wednesday’s US CPI data for hints on the Fed’s rate path moving forward, WTI crude oil likewise exhibits this inverted price movement. According to a Bloomberg survey of economists, headline inflation will be 5.0% year over year until the end of April. The decline in the price of gold coincided with a decline in volatility. Similar to how the VIX index gauges S&P 500 volatility, the GVZ index gauges the volatility of gold.

USDCAD Analysis

USDCAD is moving in the Box pattern and the market has reached the horizontal support area of the pattern.

The key factor driving the USDCAD exchange rate tomorrow will be the US CPI report. After repeated FED rate increases since June 2022, oil prices have fallen. Consumer spending increases in Canada due to changes in employment and a low unemployment rate, which increases the possibility of a rate hike by the Bank of Canada at its next meeting.

As it struggles to hold onto the week-start comeback amid lacklustre markets early on Tuesday, USDCAD retraces its intraday low near 1.3365. The US Dollar’s inability to defend the prior gains amid a cautious atmosphere ahead of the crucial US debt-ceiling talks in the White House may be strengthening the Loonie pair’s retreat movements. It’s interesting to note that the quote can potentially entice bears because WTI crude oil, one of Canada’s main exports, is only lightly bid. However, despite intraday gains being stabilised, the US Dollar Index (DXY) declines to 101.42 due to disappointing information from the Federal Reserve’s quarterly bank loan survey. However, optimistic forecasts for US inflation, as measured by the 10-year and 5-year breakeven inflation rates from the St. Louis Federal Reserve statistics, combine worries about dire circumstances if the US fails to raise its debt ceiling to support the dollar.

WTI crude oil holds onto modest gains near $73.00, up for the fourth day in a row, as recession worries clash with cautious optimism as key Asian countries open their borders internationally. Additionally, the US Dollar’s struggle to gather upward momentum and the subsiding concerns about the bank crisis both contribute to the oil price’s steady ascent. S&P 500 Futures are unsure about 4,150 amid these bets, but US Treasury bond yields are on a three-day gaining streak. Moving forward, the USD/CAD movements may continue to be constrained by a light calendar and a cautious mindset before to important data or events. However, to predict short-term market movements, today’s White House negotiations on changing the debt ceiling expiration, which is due in June, will be very important. The likelihood of hesitation and a weight on the US Dollar cannot be ruled out given the stark differences of opinion among US policymakers on the subject. However, if the dovish Fed worries weigh on the quotation while other factors remain the same, the probable positive US inflation statistics for April may defend the Loonie buyers.

USDCHF Analysis

USDCHF is moving in the Descending channel and the market has reached the lower high area of the channel.

Due to UBS acquisitions, Credit Suisse Chief Economist Zoltan Pozsar resigned from his position as head of Credit Suisse’s short-term interest rate strategy. He was employed for the US Treasury and the FED of New York prior to joining Credit Suisse in 2015.

According to the Wall Street Journal, Zoltan Pozsar, a well-known Credit Suisse market expert, has departed the company as part of a worker exodus that began in the months prior to the lender’s shotgun purchase by competitor UBS (UBSG.S). According to the story, which cited a person familiar with the situation, Pozsar left Credit Suisse recently. Prior to joining Credit Suisse in 2015, he held positions at the Federal Reserve Bank of New York and the U.S. Treasury, according to the Wall Street Journal. He was Credit Suisse’s global head of short-term interest-rate strategy.

USD Index Analysis

USD index is moving in the box pattern and the market has rebounded from the horizontal support area of the pattern.

Business and financial executives were directly contacted by US Treasury Janet Yellen over the impending US debt default. Households and companies will be more impacted if the US government defaults. Both the US and the world economy will be impacted.

During the early Asian session on Tuesday, the US Dollar Index picks up bids to extend the prior daily gains to 101.40. Due to a light schedule and mixed emotion, the greenback’s index against six major currencies fails to counteract positive inflation indications and the market’s hesitation. However, compared to the 0.1% forecast and the month before, US wholesale inventories decreased to 0.0% in March. However, according to the 10-year and 5-year breakeven inflation rates from the St. Louis Federal Reserve (FRED) data, the early signs of US inflation appear to be rising. The US employment data, on the other hand, wasn’t very strong, which in turn raises questions about the US Federal Reserve’s (Fed) upcoming move and puts this week’s US Consumer Price Index (CPI) for April, due for release on Wednesday, in the spotlight.

In light of this, Austan Goolsbee, president of the Chicago Federal Reserve Bank, said, “It is too early to say what the next policy move will be,” adding that there were many unknowns surrounding the effects of credit tightening on the economy. On Monday, two persons with knowledge of the situation told Reuters that US Treasury Secretary Janet Yellen had personally reached out to corporate and financial executives to underscore the disastrous effects a US default on its debt would have on both the US and worldwide economies. Wall Street ended the day with a mixed performance amidst these trades, as the benchmark US 10-year Treasury bond yields had increased to 3.50% over the past three days. Now that the calendar is light, DXY traders must keep a watch on the risk catalysts for guidance.

GBPUSD Analysis

GBPUSD is moving in an ascending channel and the market has reached the higher low area of the channel.

On one side, the UK pound increased before to the Bank of England’s monetary policy meeting. Seven years after the Brexit referendum, EU leaders express a desire for engagement with the UK. The Bank of England declares that if a rate increase occurs at the future meeting, it will be at the high interest rate from 2008.

As it reverses the previous day’s corrective fall from the multi-month top ahead of Tuesday’s London open, the GBPUSD reaffirms its intraday high near 1.2635. Due to the UK holiday on Monday, buyers of the Cable pair took a break, which was reflected in the quote’s decline from its best levels since April 2022. However, the Bank of England’s recent optimism and the US Dollar’s inability to hold onto its recent gains cause the buyers of Pound Sterling to lose interest. The quote excludes the recently released negative UK Halifax House Price data for April, which decreased to -0.3% from 0.2% market expectations and 0.8% previous readings. The Guardian offers positive Brexit news elsewhere, which permits the GBPUSD to maintain its firmer position. After seven stormy years since the seismic Brexit referendum, EU leaders have expressed a willingness to reestablish relations with the UK.

The Financial Times reports that the Bank of England would increase interest rates on Thursday to their highest level since 2008 in response to official statistics released last month that revealed inflation remained persistently high. It should be highlighted that the US Dollar’s corrective recovery amid stronger US Treasury bond yields and the electoral setback for the ruling Conservative Party in the UK’s local elections present challenges for the GBPUSD bulls ahead of crucial BoE and US inflation data. Prior to that, US President Joe Biden can influence market movements as he prepares to debate Republican House Speaker Kevin McCarthy, Republican Senate Minority Leader Mitch McConnell, and senior congressional Democrats on Tuesday at the White House for a debt-ceiling extension. The newly bullish US inflation predictions may allow the GBPUSD pair to pare its recent gains near the multi-month high should the US officials surprise the markets with a positive outcome and a deal to prevent the US default.

GBPJPY Analysis

GBPJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

Governor of the Bank of Japan Ueda stated that the financial system in Japan is strong and unaffected by the crisis in the US and EU banks.

Once the economy has stabilised and reached a sustainable goal, Bank of Japan will discontinue YCC and reduce its balance sheet.

At this week’s G7 Finance Leaders Meeting, we will talk about ways to address the bank liquidity crisis.

The impact of recent US and European bank failures on Japan’s financial system is likely limited, Bank of Japan Governor Kazuo Ueda said on Tuesday. Lessons from the recent problems in the banking sector are likely to be highlighted at upcoming international gatherings, including this week’s meeting of the G7 financial chiefs. Financial institutions in Japan have enough capital reserves. There will be no predetermined plan for a specific monetary policy action during our scheduled review. Boj will terminate YCC and then reduce its balance sheet if price target is achieved in a sustained, steady way. Positive trends are emerging, notably with regard to inflation predictions. Japan’s inflation expectations have increased and are still high. Despite being hampered by recent increases in the price of raw materials, Japan’s economy is strengthening.

EURGBP Analysis

EURGBP is moving in the Descending triangle pattern and the market has reached the horizontal support area of the pattern.

German industrial production fell by 3.4% in March, instead of the projected 1.3%. German factory orders fell by 10.7% MoM, indicating that other European nations are fearful of a recession.

The EU has begun to worry about a recession as a result of this and Germany’s industrial orders dropping 10.7% MoM over the previous week.Meanwhile, some ECB members started making hawkish comments. Klaas Knot, the president of the Dutch Central Bank, said that while rate hikes are beginning to have an impact, more are still required to reduce inflation. Recently, Philip Lane, the ECB’s chief economist, said that although momentum is still strong, inflation will decline.

EURNZD Analysis

EURNZD is moving in an Ascending channel and the market has reached the higher low area of the channel.

Philip Lane, chief economist of the European Central Bank, stated that there would be “a lot of disinflation” later this year but that there would still be “a lot of momentum” in inflation while addressing at a conference hosted by Forum New Economy. Lane added that food and core price growth were particularly robust.

AUDUSD Analysis

AUDUSD is moving in the Box pattern and the market has fallen from the resistance area of the pattern.

Australian retail sales are down 0.60% compared to expectations of -0.40% and the prior figure of -0.20%. Westpac Consumer Confidence decreased in May from 9.4% to -1.7%. In April, China’s trade surplus was greater than predicted at $90.21 billion compared to the $71.6 billion estimate. After mixed data, the AUDUSD is consolidated.

The AUDUSD currency pair maintains its lower levels near 0.6775, continuing its retreat from the intraday high in the early hours of Tuesday. As a result, the Aussie pair defends April’s largely negative China trade reports and April’s weaker-than-expected Australian retail sales results. While the CNY statistics fell to 618.44B compared to 637.16B market predictions and 601.01B prior, China’s headline Trade Balance increased to $90.21B in April from $71.6B projected and $88.19B prior. However, it’s important to note that both in USD and Chinese Yuan terms, exports and imports fell in the aforementioned month. The AUDUSD exchange rate was affected earlier in the day by Australia’s first-quarter retail sales decline of 0.6%, which was worse than the -0.4% market expectations and -0.2% preceding readings. Westpac consumer confidence for May also declined, falling to -1.7% from 9.4% the month before. In addition to the negative statistics from Australia, its biggest customer, the AUD/USD is also burdened by the cautious atmosphere leading up to the important Australian annual budget and the debt ceiling negotiations.

In light of this, US President Joe Biden is preparing to debate Republican Senate Minority Leader Mitch McConnell, Republican House Speaker Kevin McCarthy, and top congressional Democrats on Tuesday at the White House. Before the meeting, Reuters reports that US Treasury Secretary Janet Yellen will personally contact business and financial leaders to outline the devastating effects a US default on its debt would have on the domestic and international economies. On a different page, the quarterly bank loan survey from the Federal Reserve (Fed) revealed that demand for commercial and industrial loans to large and middle-market businesses as well as small businesses decreased during the first quarter due to tighter standards. The S&P 500 Futures print slight losses around 4,150, the first in three sessions, while the US 10-year and two-year Treasury bond yields battle in the early hours of Tuesday to continue the three-day upswing.

An increase in US inflation expectations, as indicated by the 10-year and 5-year breakeven inflation rates from the St. Louis Federal Reserve (FRED) statistics, may also have an impact on the price of the AUD/USD. In this environment, the S&P 500 Futures register their first minor loss in three days at about 4,150, while the US 10-year and two-year Treasury bond yields struggle to prolong the three-day rise early on Tuesday. Future expectations of the first Australian budget surplus in many years and enthusiastic tax reform initiatives appear to support the AUDUSD exchange rates. Any letdown, however, won’t be taken lightly given the pessimistic market outlook before to the US debt ceiling negotiations and the US inflation figures.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/