GBPUSD Analysis

GBPUSD is moving in an Ascending channel and the market has reached the higher low area of the channel.

The UK employment change was 182K instead of the 160K expected in the 3-month average data. Part-time and self-employed workers contributed to the majority of new jobs. In March, the unemployment rate increased to 3.9% from 3.8%. A 0.10% increase in unemployment during the first quarter of 2023 indicates that the UK economy is struggling as a result of the Bank of England raising interest rates.

In the UK, the average earnings including bonuses were 5.8%, which is in line with expectations.

K Claimant Count Change increased by 46.7K in April versus -10.8K expected and 26.5K prior, and the ILO Unemployment Rate for the three months to March increased to 3.9% versus expectations of seeing no change at 3.8%. These are UK employment numbers going into Tuesday’s London open. In addition, the Average Earnings for the three months ending in March, excluding bonuses, came in below expectations. But the most recent data supports Huw Pill, the chief economist at the Bank of England (BoE), who made hawkish remarks on Monday. According to Reuters, “The Bank of England needs to be on the lookout for second-round inflationary effects that could cause inflation to bottom out at 4% or 5% rather than return to its 2% target. The weak US Dollar provides support for the GBPUSD price even though the negative UK data weigh on the Pound Sterling price. Despite rebounding from the intraday low to 102.45 by press time, the US Dollar Index maintains the week-start decline from the monthly high.

However, the latest decline in the US dollar may be related to Monday’s NY Empire State Manufacturing Index, which showed the largest decline since April 2020, falling to -31.8 for May. The same signals support the Federal Reserve’s (Fed) dovish hike and the pessimistic trends in US inflation data that emerged over the past week. The likelihood of the Fed not raising interest rates in 2023 has recently gained popularity. On a different page, there are conflicting opinions about how prepared US policymakers are to prevent the debt ceiling from expiring, and the world’s financial markets are turning cautious as President Joe Biden and House Speaker Kevin McCarthy get ready for their crucial talks, which are set to begin at 19:00 GMT. However, recent remarks from US House Speaker Kevin McCarthy, who said, “I do not think we are in a good place,” appear to have put a floor under the US Dollar rate due to concerns over a deadlock over an extension of the country’s debt ceiling as Republicans may stick to their demand.

Following the initial market response to the UK employment figures, the GBP/USD pair may experience lacklustre movements due to fear regarding the US Retail Sales for April, which are predicted to increase by 0.7% MoM from a previous -0.6%. Following that, it will be important to follow the discussions between US President Biden and House Speaker McCarthy to prevent debt expiration as the impending US default deadline, which was recently moved to the first week of June, looms. The GBP/USD may rebound if US data continue their recent downward trend and US policymakers solve the mystery of default or release a plan to raise the debt ceiling.

GOLD Analysis

XAUUSD Gold price is moving in the Descending channel and the market has fallen from the lower high area of the channel.

We are not in a good position to address the debt ceiling limit right now, according to US House Speaker Kevin McCarthy. Due to US retail sales expected to increase this week from the previous month’s -0.60% to 0.70% MoM, gold prices are expected to decline. This month’s primary focus for Gold direction is the US debt ceiling limit.

As offers are needed to reverse the week’s initial corrective bounce going into Tuesday’s European session, gold price retraces its intraday low near $2005.00. In doing so, the bright metal carries the weight of the markets’ cautious attitude ahead of the crucial US debt ceiling negotiations and the US Retail Sales for April, both of which are scheduled for 19:00 GMT. After a depressing Monday, it is important to note that the US Dollar Index picks up bids to regain its intraday high near 102.50, which encourages the market’s fears of a US default and nervousness ahead of the crucial US data. It is important to note that US House Speaker Kevin McCarthy’s most recent remarks, “I do not think we are in a good place,” appear to have put a floor under the value of the US dollar by raising concerns about a potential impasse over raising the country’s debt ceiling if Republicans stick to their demand. The XAUUSD is also affected by the negative data from China, one of the main consumers of gold, in addition to the US Dollar’s movements. In spite of this, China’s industrial production increased by 5.9% in April instead of the expected 10.9% and 3.9%, and retail sales increased by 18.4% YoY instead of the anticipated 21.0%.

In other places, the Fed policymakers’ reluctance to give up their hawkish bias combines with worries about a recession and banking problems to upset the risk environment and put downward pressure on the price of gold. In the midst of these manoeuvres, the S&P 500 Futures fell by 0.30 percent intraday even though Wall Street ended up higher and the yields are still under pressure, demonstrating the market’s uncertainty as it waits for the key information or events to provide clear direction. Moving on, the market’s risk-off sentiment is likely to keep the price of gold under pressure ahead of the US Retail Sales for April, which are predicted to come in at 0.7% MoM versus -0.6% previously. Following that, it will be crucial to keep an eye on the discussions between US President Biden and House Speaker McCarthy to prevent debt expiration as the deadline for US default, which was recently brought forward to the first week of June, looms.

SILVER Analysis

XAGUSD Silver price has broken the Box pattern in downside.

According to US Treasury Secretary Janet Yellen, if Congress does not raise the debt ceiling by June 1st, the US will fail to uphold its global leadership obligations and harm its citizens’ families. The problem was addressed so quickly, and both parties successfully resolved it.

The US Treasury Department reaffirmed on Monday that it anticipates the US government will only be able to pay its bills through June 1 without an increase in the debt ceiling, putting more pressure on congressional Republicans and the White House to reach an agreement in the coming days, according to Reuters. The US Treasury Secretary Janet Yellen is quoted in the news as saying, “The debt ceiling could become legally binding by June 1. Congress failing to raise the debt ceiling would be extremely difficult for American families, damage our nation’s standing as a global leader, and cast doubt on our capacity to protect our interests in terms of national security, says US Treasury Secretary Yellen. However, Reuters also stated that before a scheduled Tuesday meeting between Biden, McCarthy, and the three other top congressional leaders, Democratic and Republican staff were attempting to reach an agreement on spending caps and energy regulations.

USDJPY Analysis

USDJPY is moving in an Ascending channel and the market has reached the higher low area of the channel.

The PPI data for Japan were less favourable than anticipated, coming in at 5.8% from 7.4% in YoY (April) and 0.20% from 0.10% in MoM (April).

I am glad that Japan’s PPI inflation rate has decreased and that the Bank of Japan will maintain its ultra-dovish monetary policy for the remainder of the year. After PPI data dropped last day, the yen eases.

Japanese PPI continued to decline in April compared to the same month last year. In addition, after reaching highs in January, Japan’s CPI and core CPI figures have consistently decreased. Lower inflation lessens pressure on Mr. Kazuo Ueda, the new head of the Bank of Japan, to alter the ultra-dovish monetary policy. After finding support at the lower end of the zone at 134.00, USDJPY has been able to extend its gains from the previous week. However, upside potential is severely constrained at 138.20, which the USD/JPY bulls have twice failed to cross. In actuality, both attempts turned below the level and failed to reach it. A brief examination of bank distress in 2023 reveals the yen’s continued strength as a safe haven currency. The USDJPY plunged in March as the SVB saga came to light, and earlier this month there was another wave of anxiety as JP Morgan acquired First Republic Bank, with PacWest and Western Alliance appearing to be the next distressed lenders on the chopping block. Over the next three weeks, risk aversion may return due to the US regional banking sector’s ongoing decline in confidence and the approaching debt ceiling deadline. The levels to the downside in that case are 134 and 131.35.

This week’s major risk event will probably be the ongoing standoff between Republicans and Democrats over raising the US debt ceiling. The US government would need to prioritise its spending by June 1 in order to prevent a default. Markets will be eagerly awaiting tomorrow’s discussions because in the past, collaboration has a tendency to increase in the two weeks prior to the deadline. In addition, the Japanese GDP for the first quarter is due on Wednesday, and the inflation report will be released on Friday, which also happens to be the day Jerome Powell is scheduled to speak at a Fed-sponsored event called “Perspectives on Monetary Policy.”

USDCAD Analysis

USDCAD is moving in the Descending triangle pattern and the market has fallen from the lower high area of the pattern.

The major oil producing province of Canada, Alberta, experienced a wildfire, which has resulted in a supply shortage for US petroleum reserves. From lows, oil prices jumped to $71.40. This week’s main focus is on Canadian CPI data.

Following a gloomy start to the week, USDCAD is stagnant near 1.3470 going into Tuesday’s European session. Thus, the Loonie pair accurately captures the trader’s cautious attitude in advance of important US and Canadian data/events amid mixed sentiment. As President Joe Biden and House Speaker Kevin McCarthy prepare for the crucial negotiations scheduled for 19:00 GMT, the world’s financial markets become cautious due to the conflicting opinions surrounding the US policymakers’ readiness to prevent the debt ceiling expiration. However, recent remarks from US House Speaker McCarthy, who stated, “I do not think we are in a good place, have caused investors to fear a deadlock over raising the US debt ceiling as Republicans may stick to their demand, which has helped to support the US Dollar. The US Dollar Index , it should be noted, maintains the week-start pullback from the monthly high, falling to 102.40. While the US Energy Information Administration’s most recent oil report provides conflicting information, the US is prepared to replenish its Strategic Petroleum Reserve, and there are concerns about a supply shortage as a result of wildfires in Alberta, Canada, one of the major global oil producers, WTI crude oil has fallen from its intraday high to $71.40 as of press time.

The previous day’s biggest daily decline in the USD/CAD pair in more than a week was caused by a combination of upbeat Crude oil price, upbeat Canadian statistics, and negative US data, among other factors. In contrast, Canada’s housing starts for April and wholesale sales for March exceeded expectations and prior levels, while the NY Empire State Manufacturing Index experienced its largest decline since April 2020, falling to -31.8 for May. S&P 500 Futures print modest losses while Wall Street closed positively, reflecting the market’s mood, and yields continue to be under pressure, indicating the market’s uncertainty and the need for important data or events to provide direction. Moving forward, the key data to watch for the USDCAD pair’s traders will be Canada’s Consumer Price Index, the Bank of Canada’s CPI Core for April, and the US Retail Sales for the same month. Above all, traders of the Loonie pair should keep an eye on how US policymakers respond to default fears for a better indication.

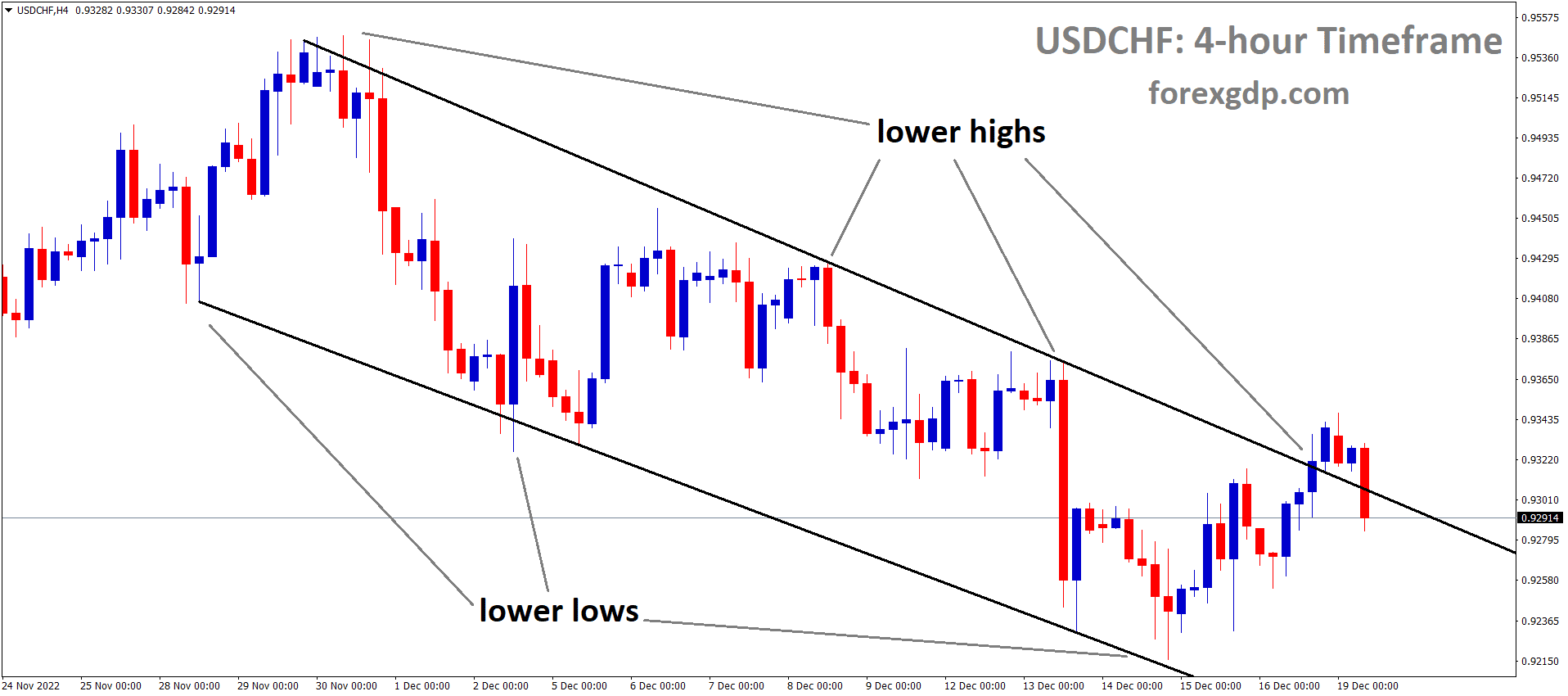

USDCHF Analysis

USDCHF is moving in an Ascending channel and the market has reached the higher low area of the channel.

The company is more focused on ESG products, which are better for investments in the environment, social issues, and corporate governance. Debt for nature swaps are also receiving a lot of attention, and UBS’s acquisition of Credit Suisse may occur during the first week of June, according to a senior investment banker at Credit Suisse.

A senior investment banker at Credit Suisse AG claims that his team is actively looking for new deals in a rapidly expanding area of ESG financing, despite uncertainty surrounding the unit is future following the unit is acquisition by UBS Group AG.In a niche of environmental, social, and governance investment known as debt-for-nature swaps, a market that it has so far dominated, the Swiss bank stands out as a pioneer. However, this year’s close call and UBS Group’s government-engineered rescue have caused businesses in the loss-making investment bank to be scrutinised for how well they fit into the longer-term UBS strategy. Ramzi Issa, global head of credit investor products structuring at Credit Suisse, states that despite having just completed the largest debt-for-nature swap ever, a $656 million deal for Ecuador, his team still intends to expand its business. In that deal, Credit Suisse acquired some bonds from Ecuador at a discount and exchanged them for a new, smaller loan in return for pledges from the nation to safeguard its marine life. By issuing brand-new bonds linked to marine conservation, Credit Suisse paid for the transaction. The Swiss bank previously completed swaps worth $150 million for Barbados last year and $364 million for Belize in November 2021. Ecuador’s record deal comes after those two transactions.

According to Issa, in total, Credit Suisse has retired about $2.3 billion of debt and replaced it with about $1.2 billion of new financing. So, even on the financial side, that has a significant impact. On the environmental front, we are talking about $680 million in funding that simply did not exist before for ocean protection. Issa stated, “We are actively considering other transactions. “I have a lot of hope. An inquiry for comment was not immediately answered by a UBS spokesperson. UBS has made it clear that it plans to close down most of Credit Suisse’s investment bank and will interview any remaining employees to determine whether they are compatible with its stricter risk culture. Since the future of many Credit Suisse bankers is uncertain until the deal is finalised in the coming weeks, other banks have seized the chance to hire experienced personnel. Competitors are also attempting to enter the debt-for-nature swap market. In the upcoming months, Bank of America plans to set up a $500 million swap deal for Gabon. As banks from across Europe and the US compete for a role in such deals, Deutsche Bank AG has also expressed interest in the market.

A number of Credit Suisse’s ESG bankers have left the company as a result of the crisis, some of whom have followed Marisa Drew, who left her position as chief sustainability officer at the Swiss Bank last year to accept an equivalent position at Standard Chartered Plc. Drew recently told Bloomberg that she is eager to expand the StanChart ESG team, including by hiring biodiversity specialists. She stated earlier this month that the field is essential to safeguarding the natural capital of the world. Issa claims that after organising a number of marine conservation swaps, he is eager to expand into more land-based deals. The number of nations showing interest in debt-for-nature swaps is expanding in the meantime. Both Suriname and Sri Lanka are reportedly considering their options. Additionally, representatives from Kenya, Eswatini, Pakistan, Colombia, and Gambia all endorsed such financing arrangements.

According to Rob Weary, an advisor on the Ecuador deal through his company, Aqua Blue Investments, “There are obviously lots of opportunities. Theoretically, he said, any nation with discounted sovereign debt, valuable ecosystems, and access to credit support from the development banks involved in such deals could meet the criteria. Nonprofits and even some financial analysts are beginning to raise concerns about the debt-for-nature swap structures, which are increasingly being handled by private markets rather than through the public or philanthropic financial structures that have been the norm for the past 30 years or so. Though intended to aid developing countries in lessening their debt loads while safeguarding the environment, some of the bond labelling in such deals has raised concerns that it may be deceptive. For instance, after learning that not all of the proceeds from the Belize and Barbados swap arrangements would go towards marine conservation, analysts at Barclays Plc questioned the blue bond tag attached to those agreements. Instead, the bonds related to Ecuador’s most recent agreement were identified as being related to marine conservation. According to Issa, the institutional investors who fund these deals have complete transparency regarding the swaps’ terms. Instead of trying to fit into a predetermined category, he said, we are trying to be descriptive. He added that his team, which is part of Credit Suisse’s investing banking operations’ markets division, is eager to keep improving and modifying the product as the market expands. If you keep performing the same action as you carry out more transactions, Issa advised that this is probably not the best course of action. “As you go along, you are trying to learn and get better.

USD Index Analysis

USD index has broken the Box pattern in upside.

This week’s main topic of attention is the US dollar’s consolidation status as a result of the debt ceiling limit. Congress mandated that the US government have two weeks starting June 1 to pay back its debts.

As the market remains cautious ahead of the crucial US debt ceiling talks and the US data amid mixed concerns on early Tuesday, the US Dollar Index continues to decline near 102.40. The market’s optimism that US policymakers will be able to resolve the debt ceiling issues caused the greenback’s index against the six major currencies to reverse from a five-week high the previous day and end a two-day uptrend. Unfavourable US data and conflicting statements from Federal Reserve officials contributed to the DXY’s weakness. The US Dollar Index faces challenges despite recent slight losses, including the recent remarks from US diplomats and the anxiety before the 190:00 GMT talks as well as ahead of the US Retail Sales for April.The US NY Empire State Manufacturing Index fell on Monday to its lowest level for May since April 2020, to -31.8, tracing the negative signals from the recent flashes of US inflation data and supporting the Federal Reserve’s (Fed) dovish hike.

Raphael Bostic, president of the Atlanta Fed, told CNBC on Monday that there is still a long way to go on inflation and added that they may have to “go up on rates,” according to Reuters. As a result of the data, the Federal Reserve signals have been largely positive. Austan Goolsbee, President of the Chicago Federal Reserve Bank, stated the opposite in an interview with CNBC on Monday, claiming that rate increases will still have a significant impact. Neel Kashkari, president of the Minneapolis Fed, added that this indicated that the Fed still has a long way to go before inflation reaches 2.0%. It should be noted that the most recent remarks from US House Speaker Kevin McCarthy, who said, “I do not think we are in a good place,” seem to weigh on the sentiment and put a floor under the DXY amid worries of a deadlock on the US debt ceiling extension as Republicans may stick to their demand. In light of this, the S&P 500 Futures show modest losses even though Wall Street ended the day positively, and the yields are still under pressure, indicating that the market is unsure of its course and is awaiting the release of important data or events. However, prior to the US debt ceiling negotiations, important statistics from China and the US might amuse DXY traders. It is not impossible that the US Dollar will decline if policymakers there give the markets a pleasant surprise. It is important to remember that the US Retail Sales report may have a negative impact on the dollar.

EURUSD Analysis

EURUSD is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

Kazimir, a policymaker at the ECB, stated that the European Commission revised its estimate of inflation to 5.8% in 2023 from the 5.5% predicted in February. GDP in Europe is expected to increase from 0.9% to 1.1%. According to what he said, the second half will be in a good position because the first half was marked by fear and slowdown.

The European Central Bank’s policymakers made comments over the weekend that caused some notable indecision and touched various nerves. According to ECB Vice President Luis De Guindos and policymaker Kazimir, the ECB has reached the final stretch of its tightening cycle. According to Kazimir, in order to reduce inflationary pressures, the ECB may need to raise rates for a longer period of time than initially anticipated. Like many Central Banks currently, the best course for monetary policy appears to be a game of “flipping the coin,” with different perspectives from policymakers on how to proceed. This is demonstrated by the revisions made to the EU Commission Forecast, which now projects 2023 inflation to be 5.8%, up from the February forecast’s projection of 5.5%, and 2023 GDP growth to be 1.1%, up from 0.9%. It is still debatable, in my opinion, whether growth will pick up in the second half of 2023 given the recent slowdown and concerns about demand.

The lowest level of industrial production for the Eurozone since October 2021 was reached in March, when it decreased by 4.1% MoM. Irish computer, electronics, and optical products, a volatile industry, saw a 50% drop in production, which contributed to the decline. Despite this, the larger economies in the Eurozone also slowed down, with Germany seeing a decline of 3.1% MoM. The Eurozone data released today will not do much to assuage market anxieties about demand as the number of new orders continues to decline.Despite the fact that the past two weeks have been landmarks in terms of risk events, the Eurozone still has some significant data releases in store. Today’s Fed policymakers set the stage for tomorrow’s release of the GDP Growth Rate QoQ 2nd Estimate, along with the ZEW Economic Sentiment Index and Current Conditions, and Wednesday’s release of the final April inflation data.

AUDCAD Analysis

AUDCAD is moving in the descending channel and the market has fallen from the lower high area of the channel.

The Australian dollar declines against other currency pairs as a result of the RBA’s less hawkish meeting minutes. This week, an increase in the wage price index of 0.90% is anticipated, and further wage increases would lead to rate increases to prevent inflation in 2023.

The MoM inflation rate decreased from 8.4% in March to 6.3%. More rate increases will reduce demand from businesses and consumers, which will lead to decreased spending and recession fears.

Following the publication of the Reserve Bank of Australia (RBA) minutes for its monetary policy meeting in May, According to RBA minutes, the rate increase decision was made in response to a higher inflation outlook. Inflation risks from slow productivity growth, persistently high services inflation, and quicker-than-expected rental increases necessitated additional rate increases. Investors need to be aware that RBA Governor Philip Lowe unexpectedly increased interest rates by 25 basis points (bps) to 3.85%. Given that Australia’s inflation has been steadily declining for the last three months, the market was expecting a policy stance stay the same. Since reaching a peak of 8.4%, monthly inflation has already significantly decreased, reaching a March-recorded 6.3% rate.

The Australian economy is expected to continue to slow down as a result of higher interest rates, which will have a significant impact on future inflation in Australia, according to RBA policymakers. The Wage Price Index data for the first quarter of CY2023, which will be released on Wednesday by the Australian Bureau of Statistics. Estimates indicate that the quarterly labour cost index data will increase to 0.9% from the previous release of 0.8%. In addition, annual data is anticipated to increase from the previous release of 3.3% to 3.6%. An increase in labour cost index data would make it necessary for the RBA to tighten up the economy even more quantitatively

AUDNZD Analysis

AUDNZD has broken the Descending channel in upside and retest the broken area of the channel.

In April’s data, China reported annual retail sales that were weaker than anticipated, which caused Kiwi to fall against counter pairs. 18.4% of the expected amount (21.0%) and the previously released 10.6% were printed.

The annual industrial production for the month of April decreased by 5.6% from the predicted 10.9% and the previous reported 3.9%.

After the Covid-19 lockdown release, China’s growth output is weaker than expected due to lower-than-expected retail sales and industrial production.

One of China’s main trading partners, New Zealand’s currency, the Kiwi, fell against other currency pairs as a result of China’s slowdown.

As a result of the National Bureau of Statistics of China reporting weaker-than-expected annual Retail Sales data, the NZD pair has fallen. The economic data increased at a slower rate 18.4) than anticipated 21.0%, but at a faster rate than the previous release 10.6%. In addition, the annual Industrial Production data came in at 5.6%, which was between the estimates of 10.9% and the previous release of 3.9%. After the full lockdown curbs were rolled back, the growth rates of industrial production and retail demand both slowed, showing that the Chinese economy is at least moving in the right direction.It is important to note that New Zealand, along with the New Zealand Dollar, is one of China’s top trading partners.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/