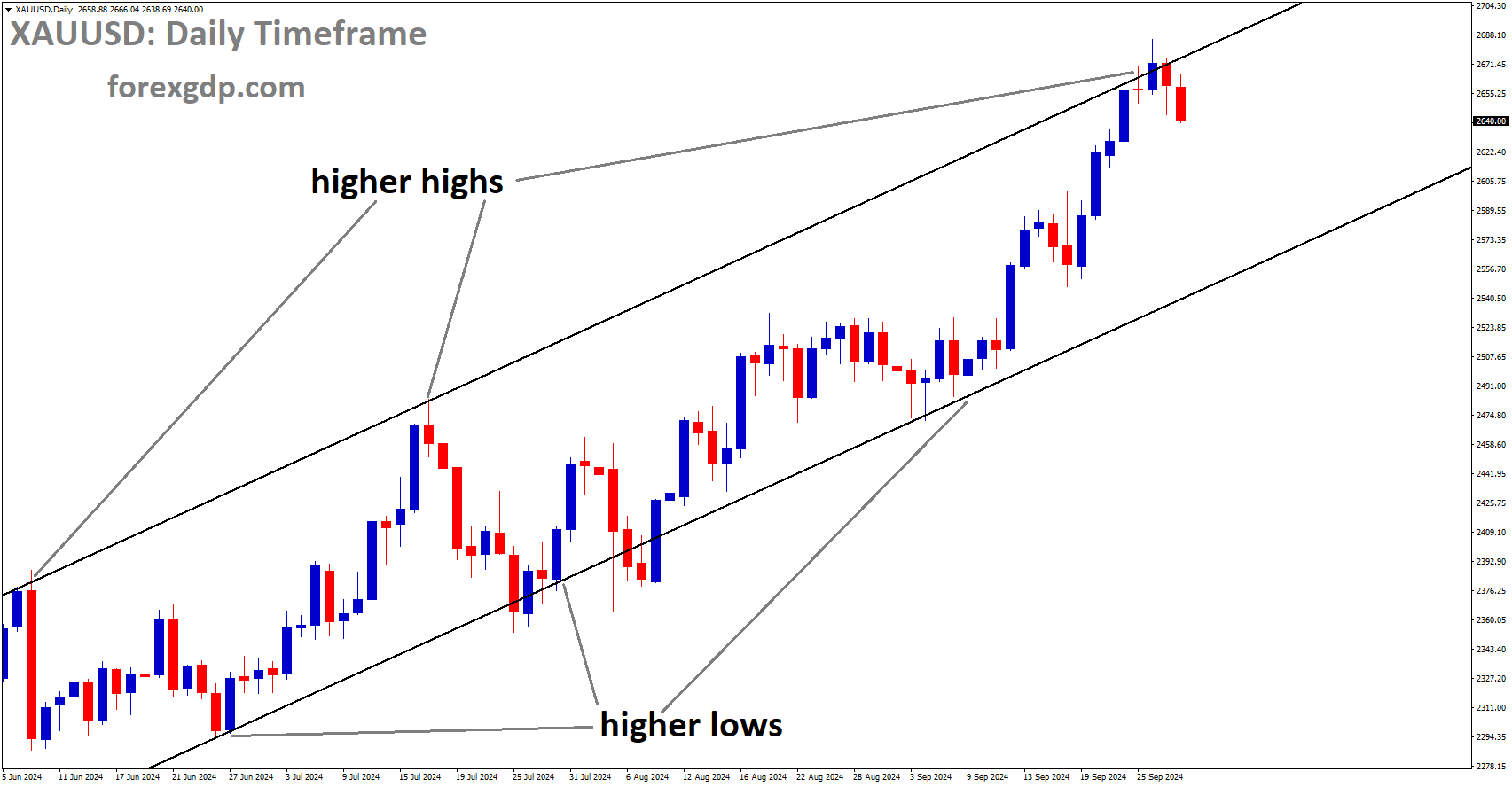

GOLD Analysis

XAUUSD Gold Price is moving in an Ascending channel and the market has reached the higher low area of the channel.

Due to US GDP data coming in slightly higher than anticipated the previous day, gold prices have fallen once more. After White House Speaker Kevin McCarthy gives the option for the deal to close at any time, the US debt ceiling limit could increase. The wealthy Americans’ taxes and further concessions have already been ruled out at this meeting. The Federal Reserve meeting minutes were vague about whether rates would be increased next month; a less hawkish stance is anticipated at the monthly meeting in June.

Bulls and bears have been vying for position in the recent gold market battle, but no side has so far managed to win. Prices are stuck between the $1950 and $2050 handles, and any movement seems to be fleeting without any follow through. The $1950 support area has been resisting a downside breakout in price action on the daily timeframe for the past week and a half. Prices continue to fluctuate due to the US policymakers’ inability to reach a consensus on the US debt ceiling. The US ‘AAA’ Long-Term Foreign-Currency Issuer Default Rating (IDR) was placed on Rating Watch Negative by Fitch Ratings Agency yesterday. Let us hope this is the final push that policymakers need to reach a deal. While ruling out tax increases on the wealthy and affirming that a significant number of concessions have already been made, House Representative Kevin McCarthy did remain relatively upbeat in his remarks during a press conference.

SILVER Analysis

XAGUSD Silver Price is moving in the Descending channel and the market has reached the lower high area of the channel.

In addition, despite a number of recent hawkish statements from policymakers, the Federal Reserve minutes release did not offer any additional clarification on US monetary policy. The main conclusions from the minutes are that decision-makers are divided over whether to continue hiking or to stop now. Prior to the Fed’s June meeting, we will undoubtedly have this week’s PCE data and one more CPI print, both of which could be crucial for determining the next course of action for central banks. A significant amount of US data is on the docket today in advance of tomorrow’s important Core PCE release. The US dollar may continue to find support and gold may move closer to the $1950 support area if the second estimate of the GDP growth rate and the jobless claims report both come in positively.

USD Index Analysis

USD index is moving in an Ascending channel and the market has fallen from the higher high area of the channel.

The one-month US -T Bill traded at 6%+ to maturity, just after June 01 maturity has 7%, so US Dollar demand is rising in the short term. As a result, US Dollar remains positive on the markets. Short-term debt yields are higher. Negotiations to raise the US debt ceiling are ongoing, and analysts only expect optimism to come from this meeting. There is a 33% chance of a rate hike at the FED meeting on June 14 and a 46.5% chance at the meeting in July.

The US dollar continues to be supported by the ongoing impasse in the debt ceiling talks as US short-dated debt yields rise. Even shorter down the curve, T-bills maturing just after the June 1st potential default date were seen trading with yields above 7%. The one-month US T bill is offered with a 6%+ yield to maturity, a new multi-decade high. As the short-term rate differential between the other G7 currencies widens, these previously unheard-of yields are giving the US dollar a strong boost higher. As market anticipation grows for a further 25 bp rate hike at the June 14 meeting, the re-pricing of interest rate increases continues in the US bond market. According to CME Fed Fund probabilities, there is now a 33% chance of a rate hike in June with this probability rising to 46.5% at the July meeting. A multi-week high yield of 4.42% is currently being offered on the rate-sensitive UST 2-year, which is nearly one full percentage above the low from March 24th. Only recently has the first Fed rate reduction been priced in for the December meeting. After months of the market ignoring the US central bank’s advice to hold rates at their current levels or slightly higher for longer, it appears that the market is now paying attention to the Fed.

EURUSD Analysis

EURUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel.

Eurozone Given the technical recession that will affect the Eurozone in the second half of 2023, German GDP this week was lower than anticipated. German manufacturing and orders decreased in the first quarter, making the euro weaker than the dollar.

Yesterday, the Fitch Rating Agency downgraded the US’s AAA Long-Term Rating to Negative, stating that the US could default at any time and that the debt ceiling could not be raised.

The German GDP surprised markets this morning, signalling that the biggest economy in Europe has technically entered a winter recession. As a result, the euro has continued to fall against the US dollar. The official definition of a recession is two consecutive quarters of negative revenue, which gives the euro bulls little hope in a risk-averse environment. The US debt ceiling is still on investors’ minds, and since there is still no agreement on the table, markets are getting jittery, which benefits the dollar as a safe haven. The US was placed on negative watch by the ratings agency Fitch for a potential downgrade as a result of the ongoing debt ceiling negotiations, adding to the market’s already uneasy state.

There are several speakers from the European Central Bank scheduled for the day, so it will be interesting to see if they mention the most recent German GDP report in light of the recent trend towards extreme hawkishness. From a US perspective, the only other significant event to coincide with Collins’ speech from the Fed is the US GDP. The FOMC minutes from yesterday did not help the euro’s situation because many members were considering either a pause or another hike at the June meeting. However, going forward, the possibility of further rate increases remains open. Important US economic data, such as the current GDP and tomorrow’s core PCE price index, durable goods orders, and Michigan consumer sentiment, gain more significance as a result.

EURCHF Analysis

EURCHF is moving in the Descending channel and the market has fallen from the lower high area of the channel.

Yesterday, the European Commission approved the eagerly anticipated merger of Credit Suisse and UBS; there will be no harm to European banks from the merger and no competition. The Swiss National Bank, the Financial Market Authority, and the Finance department now send pre-agreement closures to UBS.

The sale of Credit Suisse Group AG to UBS Group AG, which was facilitated by the Swiss government, was approved by the European Union after regulators determined there would not be any significant competition issues. Following a brief one-month review that revealed there would be no harm to competition in any of the markets examined in wealth and asset management as well as investment banking, the European Commission approved the merger on Thursday. The combined entity, it said in a statement, will continue to face significant competitive pressure from a wide range of competitors in all of those markets. After government intervention to avert a disorderly bankruptcy, UBS and Credit Suisse reached an agreement in March to purchase the latter in an all-share transaction for approximately $3.25 billion. Given the risks to the financial markets, it was widely believed that the EU would approve the transaction.

Since Switzerland is not a member of the European Economic Area, which is the subject of the EU’s merger investigations, the commission would have found it more difficult to act against the deal. The banks were given permission by the commission to depart from the norm in April, allowing them to carry out the merger before the review’s conclusion. When the deal was first announced, UBS secured pre-approval from a number of regulatory bodies, including the Swiss Federal Department of Finance, the Swiss National Bank, and the Swiss Financial Market Supervisory Authority. Credit Suisse and UBS declined to comment.

GBPUSD Analysis

GBPUSD is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

US GDP came in slightly better than anticipated on Monday, printing at 1.3% as opposed to the 1.1% forecast. The UK economy is doing well, but inflation is increasing. The report from last month shows that MoM was below double-digit levels. The Bank of England keeps interest rates high to control UK inflation.

As investors in Europe and Asia pore over the most recent remarks from the US Federal Reserve, the British pound joined many other currencies in making a small gain against the US dollar on Thursday. However, in Sterling’s case, those gains once again proved fleeting. The Federal Open Market Committee meeting minutes from May suggested that rate-setters may now be inclined to wait and consider the effects of earlier increases in borrowing costs before releasing more. This was not exactly a resounding rejection of higher rates, but it was enough to cause the dollar to tremble a little—especially as investors anxiously anticipate more difficult-than-usual talks about the federal debt ceiling. In the meantime, sentiment towards the Pound is still clouded. Since September 2022, the British pound has increased significantly as a result of (reasonable) expectations that local interest rates would continue to rise. With the Pound struggling to maintain any momentum in the face of still-high inflation and the obvious possibility of further increases in interest rates from the Bank of England, it appears investors are now running out of reasons to buy.

Even though the UK economy appears to be doing better than expected, many of those predictions were already very pessimistic. When you factor in necessities like food and fuel, it also has some of the highest inflation in Europe, and government borrowing has increased significantly. The official US growth figures for the first quarter of this year were revised higher, according to news from Wednesday’s session. The current estimate for annualised growth is 1.3%, which is still abysmally low but better than the 1.1% initially reported. This was sufficient to cause the GBPUSD to resume its daily downward trend. The official UK retail figures and US inflation data, both of which are due on Friday, will be the subjects of immediate attention.

GBPJPY Analysis

GBPJPY is moving in an Ascending channel and the market has reached the higher high area of the channel.

In April, UK retail sales increased by 0.50% versus the forecasted 0.30% and a 1.2% decline in March. English Central Bank Jonathan Haskel, who sets interest rates, stated that if inflation rises in the coming months, interest rates will stay higher for a longer time. As promised by UK PM Rishi Sunak, the UK Finance Minister stated that in the second half of 2023, inflation will be cut in half. The Japanese Yen was the focus of discussions regarding the Bank of Japan’s control over the yield curve. More economists anticipated that bond yields would decrease in duration from 10 to 5 years.

Early in the European session, the GBPJPY pair has fallen below the 172.30 immediate support level. After the release of the mixed United Kingdom Retail Sales data, the cross has come under a lot of pressure. Monthly Retail Sales increased by 0.5% versus the 0.3% forecast and a 1.2% decline that had been previously reported. While annual Retail Sales fell short of forecasts and shrank by 3.0% instead of the expected 2.8%. When volatile fuel factors are excluded, monthly retail sales increased by 0.5%, versus the street’s expectation of 0.3% growth.The Bank of England will continue to face pressure as a result of the UK’s monthly retail sales, which show a strong expansion. Jonathan Haskel, the BoE’s interest rate setter, stated on Thursday that if additional evidence of inflation persistence is found, policy will be tightened.

UK Prime Minister Rishi Sunak promised that inflation would be cut in half by year’s end, and the UK Finance Minister is confident that this will happen. He continued by saying that in order to reduce taxes for households and relieve them of the burden of persistent inflation, inflation must be brought under control because doing otherwise could have disastrous consequences. Discussions about Bank of Japan Kazuo Ueda’s proposed adjustment to the Yield Curve Control have focused attention on the Japanese Yen. Shortening the target bond yields from the current 10-year zone to the five-year zone could be one option, according to BoJ Ueda.

GBPCAD Analysis

GBPCAD is moving in an Ascending channel and the market has reached the higher low area of the channel.

Following yesterday’s positive US GDP data, oil prices fell. US debt ceiling negotiations yield no conclusions Global nation demand for oil is declining. Global bank interest rates are higher, which reduces demand for oil consumption. The decline in the Canadian Dollar is caused by the falling oil price.

Due to ongoing anxiety over the debt ceiling and traders taking profits from the recent rally, the price of oil rolls over and declines on Thursday. The US dollar, which is also strengthening and is the primary currency used to price crude, is under pressure. Following the release of encouraging data, the Dollar Index (DXY) has broken through the psychological level of 104.00 and is now rising. WTI crude oil is currently trading in the lower $71s, while Brent crude oil is trading in the mid-$75s. On the 4-hour chart, a bullish right-angled triangle has formed, challenging the general bear trend. Lack of progress in negotiations to raise the US debt ceiling raises the possibility of a US default and a subsequent global recession, which weighs on oil prices. A combination of safety flows and rising expectations that the Federal Reserve will keep raising interest rates causes the US dollar to gain strength. The dollar continues to be supported by US macroeconomic data. From a 1.1% initial estimate, the gross domestic product annualised was revised up to 1.3%. In addition, the GDP price index was raised from 4.0% to 4.2%. Core Personal Consumption Expenditures for the first quarter were increased from 4.9% to 5.0%.

The US dollar is supported further by labour market data after initial claims for unemployment insurance came in lower than expected at 229K versus 245K. Data from the Energy Information Administration (EIA)’s inventory showed a much larger-than-anticipated drawdown of 12.5 million barrels on Wednesday, pointing to strong demand. Analysts had anticipated a rise of 775,000. Prince Abdulaziz bin Salman, the Saudi Arabian oil minister, made remarks that helped the price of oil. He cautioned oil speculators to be careful because they might suffer the same fate as they did in April. His remarks were interpreted as a warning to short-sellers that the price of oil might increase. At its meeting in October 2022, Abdulaziz defended OPEC and its choice to reduce production by 2 million barrels per day (bpd). Given that the price of oil is now near where it was in October, there is a possibility that the cartel will announce another supply cut in June. The US summer driving season begins on May 27 with the start of Memorial Day weekend, which will give demand a seasonal boost and support oil prices. A report released on Thursday by the Energy Information Agency (EIA) predicts that as nations work to achieve their net-zero emissions targets by the year 2050, investment in solar power ($380 billion) will surpass that in oil ($370 billion) for the first time in 2023.

AUDUSD Analysis

AUDUSD has broken the Descending channel in upside.

After the retail sales growth in April decreased from 0.40% to 0.0%, the Australian dollar falls. Australian dollar fell against the US dollar yesterday as US GDP data came in higher than anticipated.

As it rises from the yearly low to 0.6515 ahead of Friday’s European session, the AUDUSD records its first daily gain in the previous four days. In doing so, the Aussie pair cheers the US Dollar’s decline while paying little attention to the gloomy Australian data. In April, Australia’s retail sales growth was only 0.0%, compared to market expectations of 0.2% and 0.4% the month before. It should be noted that the US Dollar Index has fallen from a 2.5-month high to 104.17 by press time due to US policymakers’ failure to reach agreement on the extension of the US debt ceiling, despite rumours that there is still a $70.0 billion gap that needs to be filled by the negotiators in order to reach the long-awaited agreement. Recently, US House Speaker Kevin McCarthy stated that there was no agreement on the debt deal and that negotiations would go on. But we are working and will keep working until we complete this. Despite positive US data, the Federal Reserve’s (Fed) impressive tone encourages the US Dollar bulls ahead of more important statistics.

On a different note, the corrective bounce in the AUDUSD pair is also supported by China’s FX intervention and a moderately upbeat atmosphere in the Asia-Pacific region, despite concerns about the Reserve Bank of Australia’s hawkish moves. Nevertheless, the second estimate of the US Annualised Gross Domestic Product for the first quarter of 2023 was increased from 1.0% to 1.3%. In addition, the April Chicago Fed National Activity Index increased to 0.07 from -0.37 in March and -0.02 in market expectations. In a similar vein, the Kansad Fed Manufacturing Activity increased to -2 in May from -21 in previous readings and -11 in analysts’ estimates. It is important to note that US Pending Home Sales for April rose YoY but fell MoM, and Core Personal Consumption Expenditures increased to 5.0% in the preliminary readings from 4.9% in the previous readings.

Following the release of the data, Thomas Barkin, president of the Richmond Fed, stated that the Fed is in a test-and-learn phase to ascertain how slower demand affects inflation. According to Reuters, Boston Federal Reserve President Susan Collins stated on Thursday that the Federal Reserve may be about to pause interest rate increases. In this environment, the Asia-Pacific equities show slight gains while the US stock futures record minor losses. Additionally, US Treasury bond yields are declining from their multi-day high. Looking ahead, the market’s mood weakens and traders are able to prepare for important data, such as the US durable goods orders for April and the Core Personal Consumption Expenditure (PCE) Price Index for that month, which is known as the Fed’s preferred inflation gauge.

NZDUSD Analysis

NZDUSD is moving in the Descending triangle pattern and the market has reached the Horizontal support area of the pattern.

Cyclone Gabrielle had less of an impact on inflationary pressure than the first one, according to Reserve Bank of New Zealand Assistant Governor Karen Silk. We have already increased interest rates, and we are now waiting for inflation to decline in the coming months. Investors took notice of the RBNZ’s 25 bps rate increase yesterday.

After a slight recovery around 0.6070 in the early London session, the NZDUSD pair is now moving back and forth. The Kiwi asset is anticipated to continue its recovery as the US Dollar Index has turned bearish amid bets favouring a pause in the Federal Reserve’s rate-hike cycle. S&P500 futures have reduced some losses that were added in Asia, signalling a slight improvement in market participants’ risk appetite. The appeal of US equities has increased due to a decline in the US Dollar Index. However, given that the $31.4 trillion US borrowing cap limit has not yet been raised, market sentiment is anticipated to remain cautious overall. The Federal Reserve policymakers are expected to take advantage of the tight credit conditions to put pressure on inflation rather than raising interest rates further, which has put pressure on the USD index.

Data from US Durable Goods Orders will be closely monitored for additional direction. Durable goods orders for April are predicted to decrease by 1.0% as opposed to growing by 3.2%. Poor demand is indicated by a contraction in the economic data, which would have an impact on the US Consumer Price Index. Investors should be aware that persistent core inflation is more of a problem for the US economy than is the headline price index. A decrease in demand for durable goods would help the Fed feel more relief by taking some of the steam out of core inflation.

In terms of the New Zealand Dollar, Assistant Governor of the Reserve Bank of New Zealand Karen Silk noted that Cyclone Gabrielle was not as inflationary as initially thought and said that rates need to be held steady for a while. She advised caution when tightening policy too much and said the RBNZ could hold off for the time being while monitoring developments. Investors should be aware that this week the RBNZ’s Official Cash Rate was increased by 25 basis points to 5.5% by Governor Adrian Orr.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/