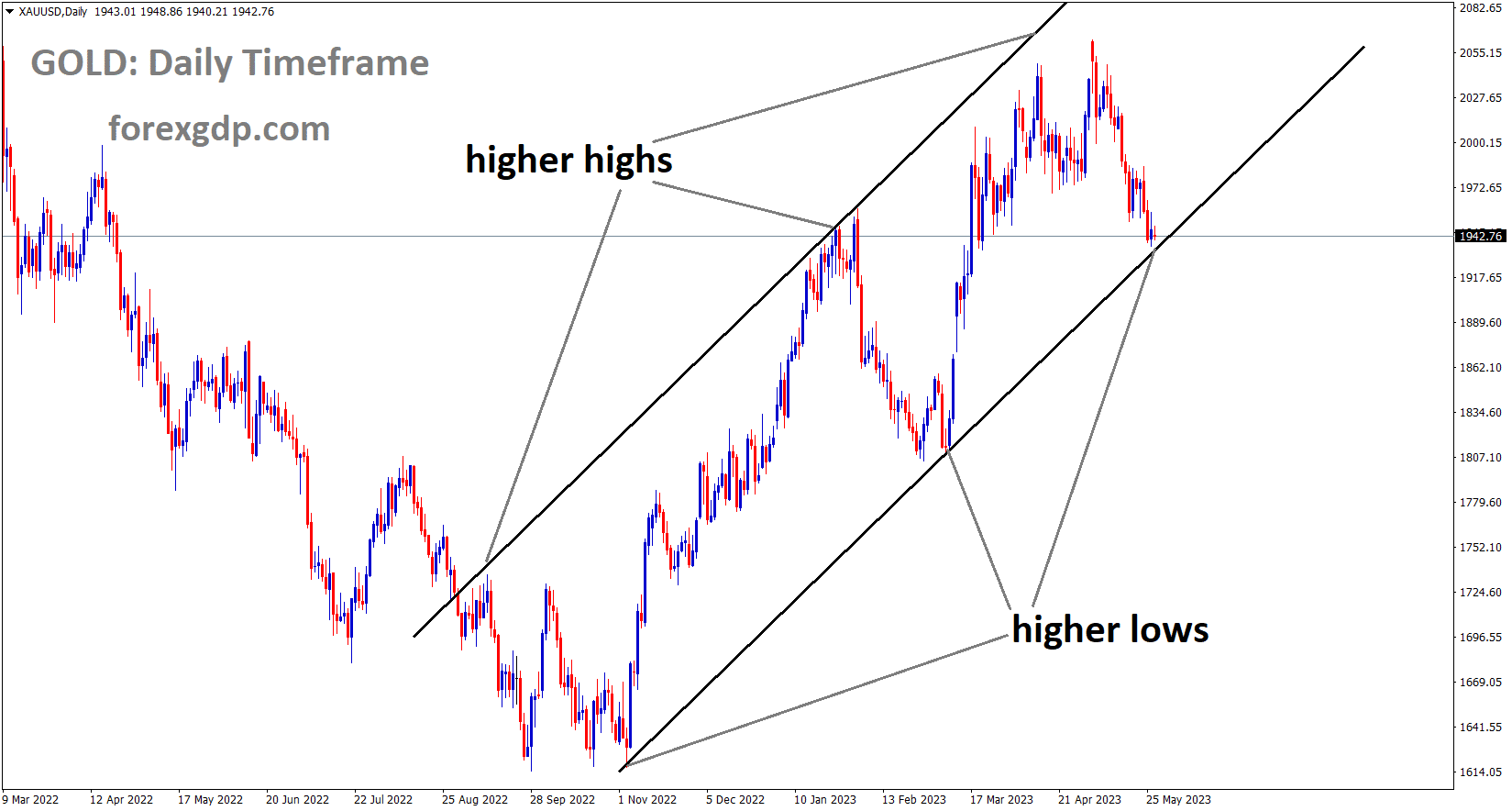

GOLD Analysis

XAUUSD Gold Price is moving in an Ascending Channel and the market has reached the higher low area of the Channel.

From early March to early May, gold prices put on a strong rally that left them just short of setting new all-time highs in the wake of the financial market turmoil caused by the failure of a few local banks. The strong recovery in U.S. Treasury rates since then, which has driven real yields sharply higher and brought the 10-year TIPS close to the 1.5% threshold, the best mark in nearly three months, has caused the precious metal to claw back at least half of those gains. Bullion has been hampered by the strength of the US dollar. Economic resilience can be partly blamed for the increase in yields. Wall Street was concerned at the start of the year that the economy, which was buckling under the weight of an overly restrictive monetary policy, would soon enter a recession. These worries were made even more pressing by the unrest in the banking sector. However, the U.S. economy has consistently outperformed pessimistic predictions, in part due to the remarkable strength of the labour market. This has led forecasters to push back the timing of a downturn to a later date, possibly in 2024.

SILVER Analysis

XAGUSD Silver Price is moving in the Descending Channel and the market has reached the lower high area of the Channel.

Inflation has been sticky as well, with American business activity and consumer spending holding up better than anticipated. Even though the overall trend is downward, price pressures are still excessively high and favour the upside, suggesting that the hiking cycle may still be ongoing. The core PCE data for April demonstrated this. Even though the Fed hinted it might hit the pause button at its meeting in June, further tightening should not be completely ruled out. There is currently no consensus opinion, but recent Fedspeak is pushing markets in the direction of higher rates for a longer period of time and a further 25 bp hike for next month.Nominal and real yields will increase further if the outlook for monetary policy continues to move in a more hawkish direction, strengthening the dollar in the process. Gold will be more exposed and susceptible to weakness in this situation. Although the near-term outlook for gold is deteriorating, the bullish trend is still alive and may pick up later this year. The economy will find it more difficult to stay afloat the longer rates remain high. In any case, gold may start to shine again once the economy falters and a recession becomes inevitable.

USDJPY Analysis

USDJPY is moving in an Ascending Channel and the market has reached the higher high area of the channel.

In the early Tokyo session, the USDJPY pair is attempting to overcome the pivotal resistance of 141.00. Since the Federal Reserve is expected to continue its policy-tightening spree in order to keep pressure on inflation, the asset is expected to continue its rally towards $110.00. This expectation comes from the street. As US President Joe Biden is sending the US debt-ceiling raise deal to Congress after receiving Republican support, S&P500 futures have experienced spectacular gains in early Asia. Fears of a US economic default have begun to subside as a result of a two-year increase in the $31.4 trillion borrowing ceiling. According to the White House, the agreement will not result in a decrease in health insurance or a rise in poverty.

The United States economy is demonstrating resilience despite increased pressure on pockets brought on by higher rates, but worries of additional interest rate announcements have increased. Compared to an estimate of 0.3%, the US core personal consumption expenditure increased in April by 0.4%. Increased spending by US citizens is anticipated to increase inflationary pressures. Aside from them, US durable goods orders increased by 1.1% when the market was anticipating a 1.0% decline. The Japanese Yen market will be closely watching Tuesday’s employment data. The unemployment rate is projected to drop from its previous reading of 2.8% to 2.7%. The Job/Applicant Ratio, meanwhile, remains constant at 1.32. Investors are continuing to pay attention to the Bank of Japan’s adjustments to the Yield Curve Control in the meantime. BoJ Governor Kazuo Ueda stated that the bank is thinking about ways to modify YCC. He continued by saying that YCC includes reducing bond yield targets from the current 10-year range to a 5-year range.

USD Index Analysis

USD index is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

As markets process the prospect of a debt ceiling agreement being approved by Congress this week, the US dollar is stable at the start of the week. US President Joe Biden and House Speaker Kevin McCarthy both stated over the weekend that they have reached a consensus and that it will be voted on in the coming days. To prevent a US default, both parties appear to have made concessions. Treasury has warned that if the ceiling is not raised in time, they might run out of money by June 5th. Due to perceptions that it had been purchased as a haven asset, the resolution of the debt ceiling issue might be seen negatively for the US Dollar. Treasury yields, however, have also been rising; on Friday, the 1-year bond reached 5.30%, up nearly 130 basis points from its March low.

The major indices posted impressive gains on Friday as a result of some positive economic data, and Wall Street futures are now pointing slightly higher. Notably, consumer sentiment, personal spending, and orders for durable goods all exceeded expectations. You can access the complete breakdown here. Crude oil has recovered today after falling to end last week, and APAC equities have been mixed but mostly in the green. While Brent is close to US$ 77.50 bbl, the WTI futures contract is back over US$ 73 bbl. As the week gets underway, gold is struggling, trading close to a 2-month low under US$ 1,950. Due to today’s holidays in the UK, Switzerland, and the US, there may not be much trading activity.

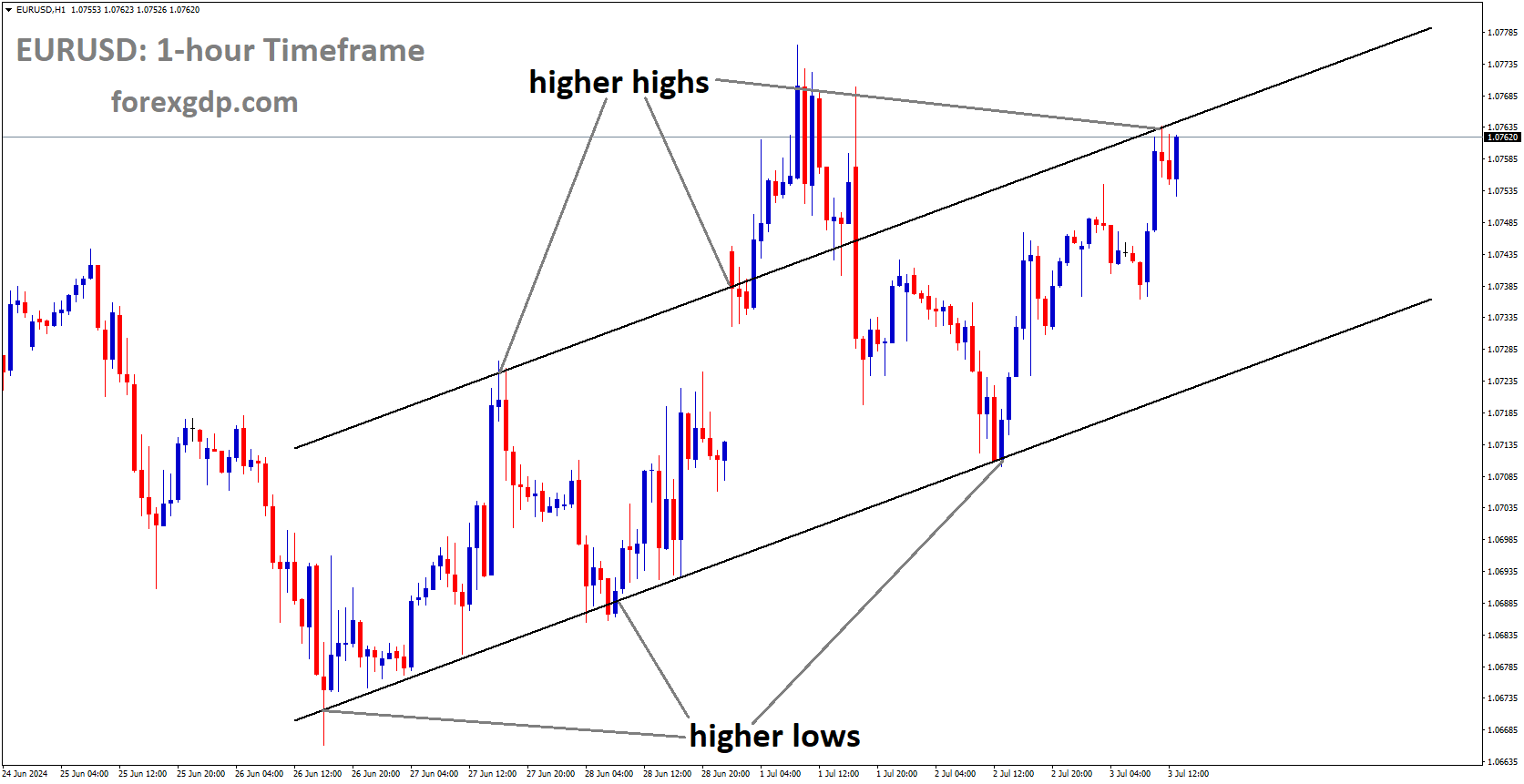

EURUSD Analysis

EURUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel.

The Euro did not have its best week as losses against the US dollar persisted while gains and losses against the British pound alternated. However, EURUSD continued to be the pair of interest, posting its fourth consecutive week of losses to the US Dollar. For the majority of the week, the policymakers at the European Central Bank have maintained hawkish rhetoric while doing little to support the euro. This may be due to the markets’ perception of the ECB as the most pessimistic central bank going forward. Markets seem to have already factored in the recent hawkishness of ECB policymakers, and a significant shift is needed for bulls to reappear. As we approach the start of the new week, a deal on the US debt ceiling remains elusive, fueling the dollar’s rally. However, US Treasury Secretary Yellen changed the date from June 1 to June 5, saying that without raising the debt ceiling, the US could default as early as June 5. Over $130 billion in scheduled payments from the Treasury will be made in the first two days of June, including payments to veterans, Social Security recipients, and Medicare beneficiaries. The new date does give negotiators more time, but the more volatility we might see in the markets the longer this drags on.

We do have some Euro Area data going into the new week, with the flash CPI release being especially significant. However, even if the CPI release surprises me, I do not anticipate any significant changes to the outlook for the euro. The story surrounding the US dollar’s debt ceiling is expected to take centre stage this coming week once more. This will be combined with Friday’s NFP jobs report, which will undoubtedly be important in light of the positive PCE data. However, if a deal is reached on the debt ceiling, the dollar could continue its longer-term downward trend since peaking in September 2022.

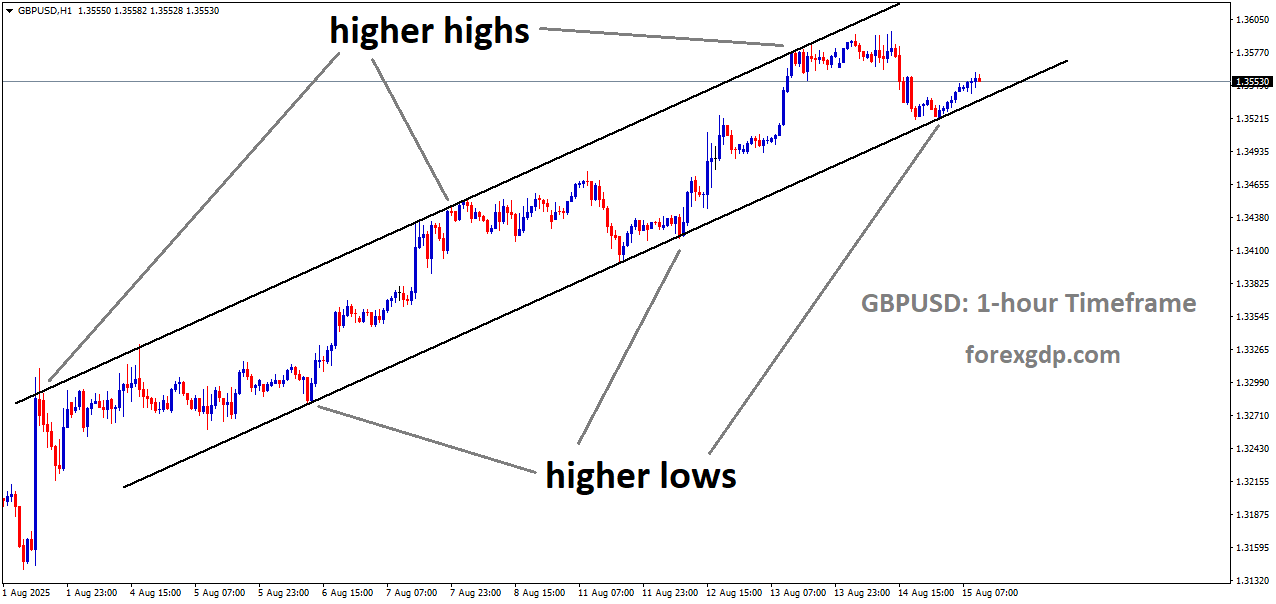

GBPUSD Analysis

GBPUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel.

This week’s figures for the UK showed that headline inflation dropped back into the single digits, falling short of analyst expectations, while the core reading increased to levels last seen more than three decades ago. Consumers were squeezed as food prices, in particular, continued to rise, even as high energy prices began to decline from the reading. The financial markets anticipate that the Bank Rate will increase over the next couple of meetings from its current level of 4.5% to at least 5%, with some hawkish forecasters speculating that the UK central bank will have to raise it to 5.5% in order to quell sticky price pressures.

GBPCHF Analysis

GBPCHF is moving in the Descending channel and the market has fallen from the lower high area of the channel.

The inflation report and the ensuing high expectations for rate hikes served as a signal to the UK gilt market. Due to increased demand from market participants for higher risk premiums, yields across the curve increased to multi-month highs. In contrast to the most recent IMF update, the UK’s 2-10 gilt curve inverted further, signalling that the UK is likely to enter a recession. This week, the International Monetary Fund (IMF) said that a recession was no longer likely and upgraded the UK’s growth prospects. According to staff projections, the UK economy will grow by 0.4% in Q2 as opposed to the 0.6% contraction the Fund had earlier predicted. According to the most recent S&P UK PMIs, the UK economy will grow by 0.4% in Q2.

NZDUSD Analysis

NZDUSD is moving in the Descending Channel and the market has reached the lower low area of the channel.

The strength of the USD has been detrimental to the Kiwi. However, ANZ Bank economists predict that if the debt ceiling issue is resolved, the NZDUSD will rise once more. Our impression is that the current consolidation reflects carry, with the NZD being the only G10 currency to do so positively. However, as we saw last week, if US bond yields increase slightly or if markets continue to worry about getting the debt-ceiling deal through Congress, it may be vulnerable to Dollar strength. Carry will persist if the latter is resolved as quickly as usual, which is one reason for our expectation of a gradual NZD appreciation over 2023. The MPS from last week came as a dovish surprise, but it is now in the past, and markets are looking ahead.

AUDCHF Analysis

AUDCHF is moving in the Descending Channel and the market has fallen from the lower high area of the channel.

Australian Dollar took a beating on a daily basis, falling to a six-month low. After retail sales for April came in flat month-over-month rather than the 0.3% forecast and 0.4% prior, the fundamental backdrop appears to be deteriorating a little bit. It follows a slight increase in the unemployment rate from 3.5% to 3.7%. The May monetary policy board meeting minutes, which were made public last Tuesday, noted that the data are consistent with RBA expectations. In weighing the two options, members acknowledged that the arguments were closely balanced, but they decided it was appropriate to raise interest rates at this meeting, the bank stated. However, when the US Dollar is dancing on centre stage, as it is at the moment, the domestic economy and the RBA become very unimportant for the AUD pair.

The message that rates will either need to be raised further or, at the very least, that a pause in the Fed funds target rate might be appropriate, was repeated by a number of Federal Reserve speakers. They made it clear that if the latter happens, it will need to remain there for a long time in order to bring inflation back down to their 2% target. By the Federal Open Market Committee meeting in July, interest rates are expected to increase by 25 basis points by about 80% of the time, according to interest rate markets. Treasury yields have risen steadily, and on Friday, the 1-year bond reached a 23-year high of over 5.3% after trading as low as 4.03% in March. The short end yield spread between Australian Commonwealth Government bonds has increased once more, which has likely hurt the AUD. The benchmark 2-year bond spread favours the big dollar by about 90 basis points. The 10-year spread has been relatively stable, which may suggest that the market is currently focused on the Fed’s rate path.

CADCHF Analysis

CADCHF is moving in the Descending channel and the market has fallen from the lower high area of the channel.

This week, amid the release of the Gross Domestic Product (GDP) data on Wednesday, the Canadian Dollar is expected to take a powerful action. According to the preliminary report, monthly GDP for March is expected to decrease by 0.1% after growing by 0.1% in February. In contrast to a flat performance, the first quarter and annualised GDP are expected to grow significantly by 0.4% and 2.1%, respectively. Tiff Macklem, governor of the Bank of Canada, may have to raise interest rates once more if the Canadian economy continues to be resilient. Investors need to be aware that the Bank of Canada will maintain its interest rates at their current levels beginning in March because the current monetary policy is stringent enough to control persistent inflation.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/