GOLD Analysis

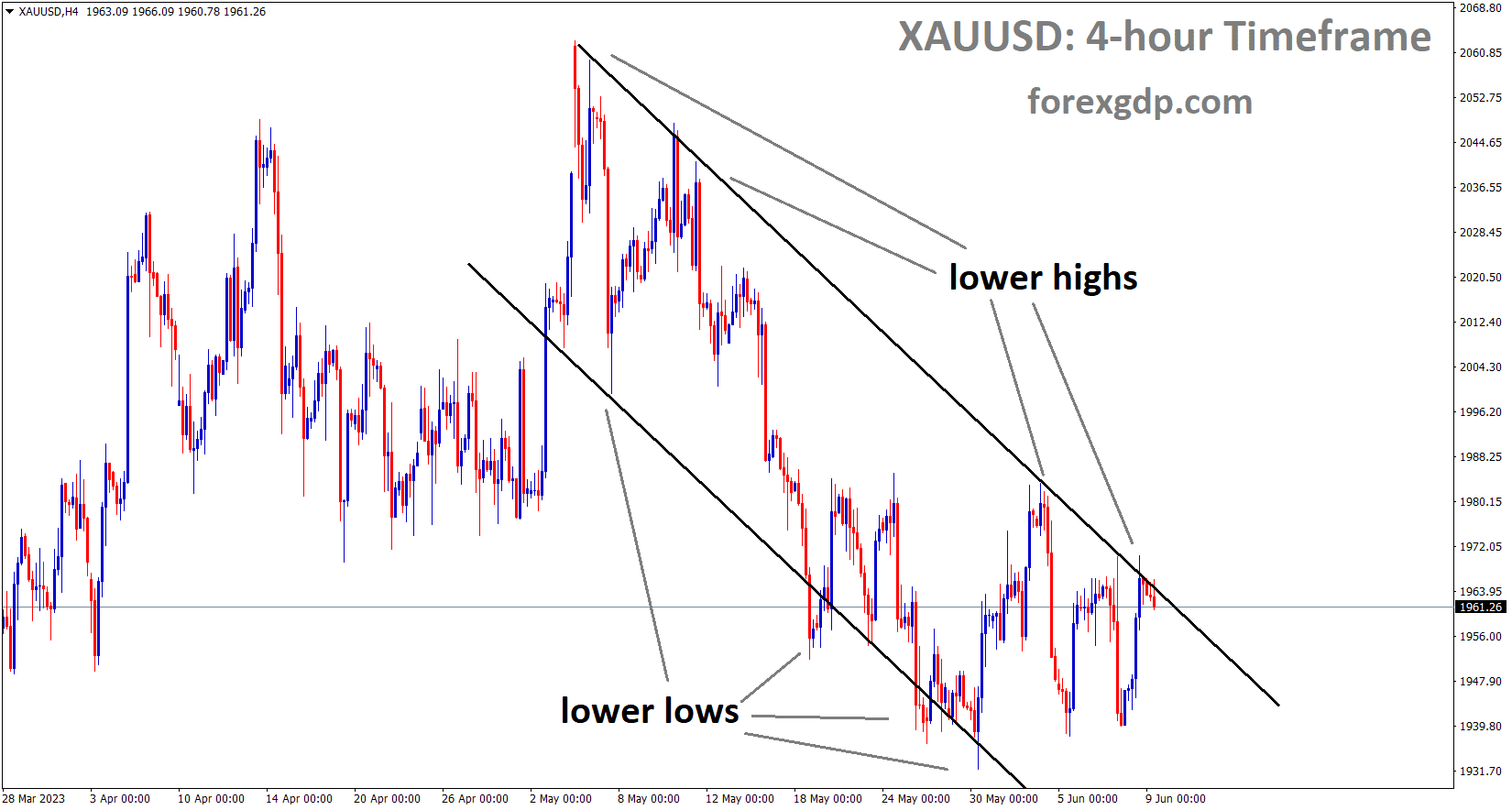

XAUUSD Gold price is moving in the Descending channel and the market has fallen from the lower high area of the channel.

Yesterday’s increase in gold prices was around 1.3%, which is a significant one-day high since May 2nd 2023. Due to rate increases by global central banks, 10-year US Treasury yields fell. More demand for gold was generated than for US government bonds.

Initial jobless claims from the US were higher than anticipated, which yesterday caused the US dollar to decline against gold. The labour market’s cooling is a strong indication that the FED will raise rates in July.

On Thursday, gold prices rose 1.3 percent, which was their best single-day performance since May 2nd, over a month ago. The rise of the yellow metal was accompanied by a weaker US dollar. The DXY Dollar Index lost 0.76 percent, which was the worst 24-hour performance since March 13th, almost three months ago. A trading instrument with anti-fiat characteristics is gold. It should be noted that Treasury yields fell on Thursday, particularly for longer-term maturities. The 10-year rate dropped to 2.03%, which was a day after rising by +3.74% as a result of this week’s major central banks’ unexpected tightening. Therefore, a weaker US Dollar and lower government bond yields worked together to create a favourable environment for gold. A closer examination of the previous 24 hours revealed that the financial markets gave the most recent US initial jobless claims report a lot of attention. Last week, those unexpectedly increased by 261k, far more than the consensus estimate of 235k. Additionally, it represented the peak since November 2021. These statistics on the state of the US labour market are some of the most recent that we have.

SILVER Analysis

XAGUSD Silver Price is moving in an Ascending channel and the market has reached the higher high area of the channel.

Unexpected increases in unemployment claims dampened expectations that the Federal Reserve would have to raise interest rates once more in July. The central bank is expected to pause tightening next week, according to consensus. The jobless claims report alone is probably not enough to spark a recession panic given that the economy has been largely holding up despite growing recession concerns. Markets for stocks rose broadly. In light of that, this is positioning gold for possible follow-through over the next 24 hours. The week’s end sees a noticeable slowdown in the economic agenda. As a result, this might put market sentiment in charge of where XAUUSD goes next.

USD Index Analysis

US Dollar index is moving in an Ascending channel and the market has reached the horizontal support area of the minor box pattern.

The global economy is expected to grow by 2.7% this year, which is the slowest annual rate since the 2008 financial crisis, according to the OECD Group. Prior to the FOMC Meeting the following week, the US Dollar started to decline, which was disappointing given that the US Dollar had been rising.

The US Department of Labour reported on Thursday that the number of Americans filing new claims for unemployment benefits increased more than anticipated, to a 20-month high, and that the US Dollar remains depressed near its lowest level since May 24. This in turn confirms market expectations that the Federal Reserve will halt rate increases, which have been weighing on the US dollar and were the cause of the overnight decline in US Treasury bond yields. However, the markets continue to factor in the possibility of a second 25 basis point Fed rate hike in July. The Reserve Bank of Australia and the Bank of Canada this week both surprised market participants by raising interest rates, which raised expectations for further Fed policy tightening. This suggests that the fight against inflation is still ongoing. As a result, traders are being discouraged from making aggressive USD bearish bets.

In the meantime, any significant improvement for the major still seems elusive in the wake of concerns about a slowdown in the global economy, which could temper any optimism. In fact, the Organisation for Economic Co-operation and Development (OECD) predicts that the global economy is likely to experience a sluggish recovery over the next few years as demand is weighed down by persistent core inflation and tighter monetary policy. Including the pandemic-affected year of 2020, the OECD now projects that the global economy will grow by 2.7% this year, which would be the slowest rate of growth since the 2008–2009 financial crisis. Aside from the most recent US consumer inflation data, investors may want to avoid the key central bank event risk of next week’s eagerly awaited FOMC monetary policy meeting. In the interim, in the absence of any pertinent market-moving economic data from the US, the US bond yields will have a significant impact on the USD price dynamics.

USDJPY Analysis

USDJPY is moving in the Descending triangle pattern and the market has rebounded from the horizontal support area of the pattern.

Governor Ueda of the Bank of Japan stated that we are putting policies into place to hit the 2% inflation target. Finances managed by the government would not be impacted by policies. We can react appropriately to FED moves after seeing them. Prior to implementation, we evaluate the benefits and negative effects of monetary policies.

USDCAD Analysis

USDCAD is moving in the symmetrical triangle pattern and the market has reached the bottom area of the pattern.

The unexpected rate increase by the Bank of Canada this week strengthens the CAD relative to the USD. Due to lower US inflation, the FOMC meeting next week can anticipate a pause in rate increases. We anticipate a rate increase of 25 basis points at the meeting the following week if US CPI data were higher than anticipated.

Since late May, the Canadian dollar has increased significantly in value relative to the US dollar. The pair is now trading close to C$1.3350 and steadily getting closer to its 2023 lows, as shown in the chart below, which shows how USDCAD has dropped more than 2.0% over the last two weeks. The unexpected decision by the Bank of Canada to resume raising interest rates at its June meeting after pausing its campaign in January has strengthened recent FX dynamics and served as another supportive factor for the Loonie. As long as traders increase their bets on further tightening in response to the central bank’s belief that monetary policy is not restrictive enough to bring inflation down to the target rate of 2.0%, the aggressive stance of the BoC could continue to put downward pressure on the USDCAD in the near term.

The Fed must adhere to the plan and keep borrowing costs steady next week in line with Powell’s guidance for the Canadian dollar’s favourable outlook to succeed. If the bank makes a different move than what was anticipated, interest rate expectations may quickly change to become more hawkish, which could lead to a surge in the value of the dollar. Even though the FOMC prefers not to surprise the markets, current economic conditions might force them to err on the side of tightening. The Tuesday release of the May consumer price index survey is one upcoming report that might tip the scales in favour of additional increases. Consensus projections show that the annual headline CPI decreased from 4.9% to 4.1% and that the core gauge decreased from 5.5% to 5.3% last month. Inflation results that are significantly higher than these projections and demonstrate stickiness could prompt the Fed to act aggressively, delivering another 25 basis point hike and predicting a higher peak rate. For USD/CAD, this would be a bullish result.

USDCHF Analysis

USDCHF has broken the Ascending channel in downside.

Thomas Jordan, the chairman of the SNB, stated yesterday that an increase in interest rates will be made at the June monthly meeting in order to keep inflation within the desired range of 0-2%. The May inflation reading was 2.2%, which is still above our target. In order to reduce the rising costs of consumer spending and manufactured goods, interest rates must be raised.

EURCAD Analysis

EURCAD has broken the Descending channel in upside.

This week’s Q1 GDP for the Euro area was lower than anticipated due to a -0.10% contraction rather than the anticipated 0.10% expansion. After posting negative GDP for two consecutive quarters, Germany already declared a recession. In its meeting the following week, the ECB intends to increase the rate by 25 basis points and control inflation readings.

After finding buying interest near 0.8580 in the early European session, the EURGBP pair has made a comeback. Despite Eurostat reporting a contraction in the final Gross Domestic Product (GDP) figures for Q1, the cross has recovered. The final Q1 GDP was released on Thursday and showed a contraction of 0.1%, whereas the market had anticipated a stagnant performance from an upwardly revised expansion of 0.1%. The annual GDP increased by 1.0%, but at a slower rate than both the forecast and the previous release of 1.2% and 1.3%. Given that the European Central Bank will not stop tightening policy to combat sticky inflation, the odds of the Eurozone entering a recession are very high. Investors should be aware that the German economy has already entered a recession after experiencing two consecutive quarters of declining GDP data.

ECB President Christine Lagarde will increase its key interest rates by 25 basis points on June 15 and again in July before pausing for the rest of the year, according to a clear majority of economists surveyed by Reuters. Rates would reach 4.25% if they were increased by a total of 50 basis points. Investors are now concentrating on the United Kingdom Employment data, which will be released the following week, when it comes to the Pound Sterling. The overall hiring process would continue to be under pressure from higher interest rates set by the Bank of England and anticipation of additional rate hike announcements from BoE Governor Andrew Bailey. Second- or third-tier United Kingdom data has recently been quite inconsistent, according to economists at ING, but next Tuesday’s release of jobs and wages data will be the main event on the data front. We view that as a negative event risk for the pound because it raises the possibility that wage growth will slow down even further and will lessen the momentum behind the 100 bps+ Bank of England tightening expectations that are still factored into the money markets.

AndPaul Beaudry, the deputy governor of the Bank of Canada, stated during this meeting that a hike of 25 bps is necessary to control Canadian inflation. Since living expenses are low, it is beneficial for the poor to stay for longer periods of time. Rate increases at the upcoming meeting are also possible if inflation and consumer spending are not reined in.

GBPUSD Analysis

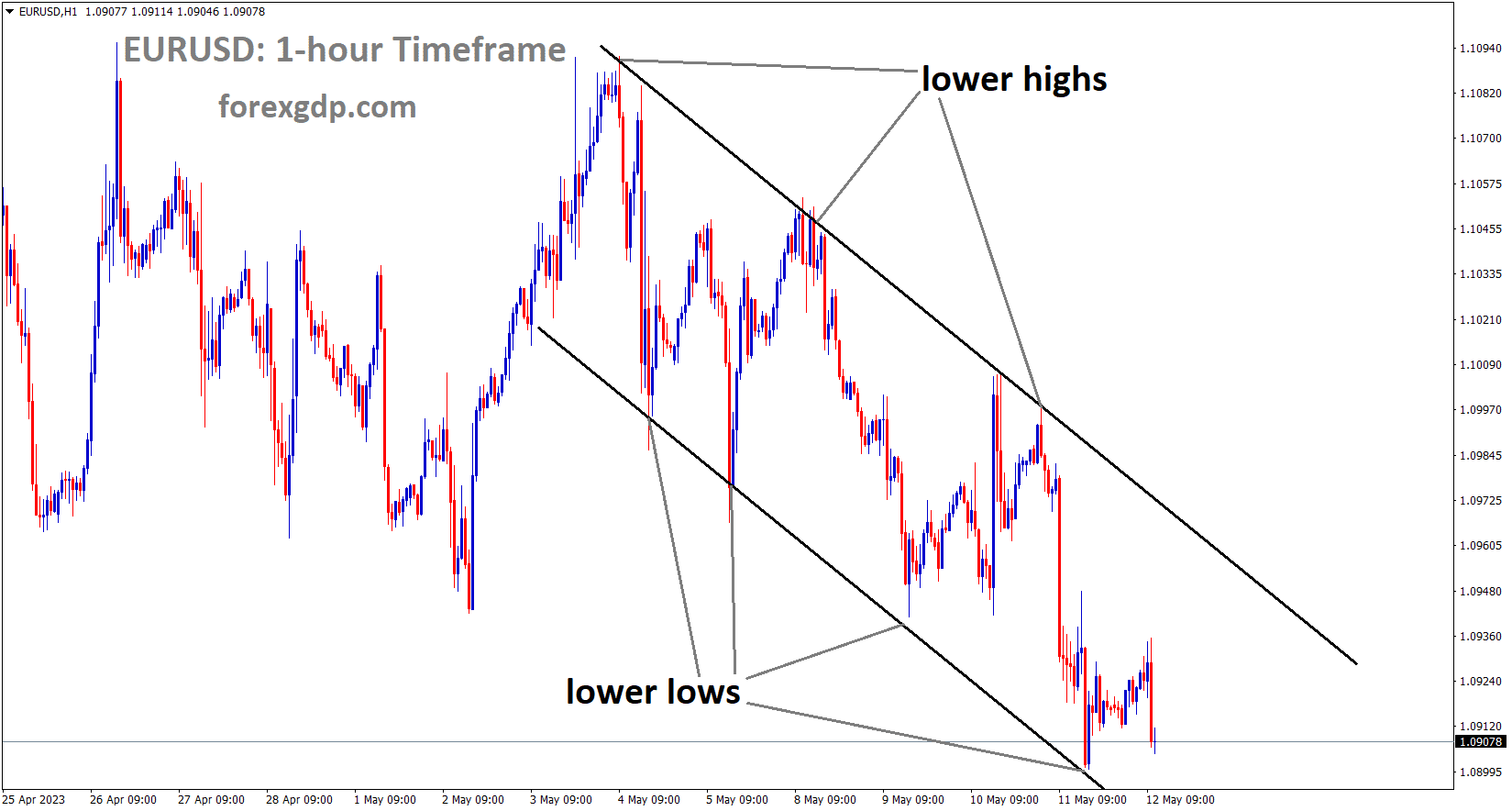

GBPUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel.

In the UK Domestic Data List meeting the following week, the change in the Climant Count is anticipated to decline by 9.6K as opposed to rising by 46.7K. Compared to the previous release of 3.9%, the unemployment rate is predicted to rise by 4.0%. The Bank of England is under increased pressure due to the inflation reading to raise interest rates at upcoming meetings.

After a brief intervention around 1.2560 in the early London session, the GBPUSD pair has resumed moving upward towards the round-level resistance of 1.2600. Due to the US Dollar Index experiencing a significant decline, the Cable has developed sheer strength. As investors wait for Tuesday’s release of the United States Consumer Price Index, S&P500 futures have seen their losses grow in Europe amidst a slight market caution. After a less confident pullback move made after printing a low of 103.30, the USD Index is currently facing strong barriers around 103.41. Investors are selling their holdings in the US dollar after US weekly jobless claims for the week ending June 2 increased significantly by 28K to 261K compared to upwardly revised expectations of 235K. The US Initial Jobless Claims report, which reached a 19-month high, indicates that labour market conditions are not tight enough, and the Federal Reserve may actively consider pausing the policy-tightening phase. The US inflation data will be closely scrutinised for additional cues. Inflation in the headlines is predicted to ease to 4.2% from the previous release’s 4.9%. In contrast to the previous release of 5.5%, the core CPI, which excludes the cost of food and oil, is predicted to increase marginally to 5.6%. Jerome Powell, the chairman of the Federal Reserve, might be more in favour of continuing the policy-tightening phase if core inflation stays persistent.

The release of the Employment data on Tuesday would also keep the Pound Sterling on edge. According to the preliminary report, the change in claimant counts is predicted to decrease by 9.6K, down from a significant increase of 46.7K. Compared to the previous release of 3.9%, the unemployment rate is predicted to rise to 4.0%. The three-month Average Earnings excluding bonuses will also be closely scrutinised. Compared to the previous release of 6.7%, the economic data is predicted to increase to 7.0%. The overall demand and eventual inflationary pressures would increase if households had more liquid assets available for disposal. This would increase pressure on the Bank of England.

AUDNZD Analysis

AUDNZD is moving in an Ascending channel and the market has reached the higher high area of the channel

The monthly reading for deflation in China’s economy has increased from 0.10% to 0.20%. According to this reading, orders in New Zealand are down and demand in China is weak. Due to US domestic data weakness rather than this week’s Chinese data impact, the New Zealand Dollar increased against the US Dollar.

The Chinese economy’s deflation, the strength of the New Zealand Dollar has not decreased. In contrast to expectations and the previous report of 0.1% deflation, the Chinese economy experienced monthly deflation of 0.2%. This shows a sharp decline in demand overall. Being one of China’s top trading partners, New Zealand has an impact on the New Zealand Dollar when Chinese demand is weak.

AUDCHF Analysis

AUDCHF is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

In April, Australia’s trade balance came in lower than expected at 11158 million dollars, compared to forecasts of 14000 and 14822. Exports decreased to -5.0% from 4.0% earlier. Imports are up from 2.0% last month to 4.0% this month. Following looming concerns over US domestic data, the Australian Dollar increased.

The inflation data from Australia’s main customer China while also applauding the most recent indications of the Reserve Bank of Australia’s and the US Federal Reserve’s divergent monetary policies. The US Dollar Index sank on Thursday as initial jobless claims in the US increased to their highest levels since October 2021. Despite this, US initial claims for unemployment increased to 261K in the week ending June 2 compared to 235K expected and 233K the week before . As a result, the four-week average increased from previous readings of 229.75K to 237.25K. Additionally, Continuing Jobless Claims decreased from 1.794M the week before to 1.757M in the week ending May 26, which was below market expectations of 1.8M. The US ISM Services PMI, S&P Global PMIs, and Factory Orders all published negative results earlier in the week, rebuffing the Fed doves and depressing the US Dollar. The same almost confirms that the US Federal Reserve will not raise interest rates at its meeting on monetary policy the following week. It also reduces market bets on rate increases in July and devalues the US dollar.

The IMF’s Thursday call for global central banks to “stay the course” on monetary policy and be vigilant in battling inflation, on the other hand, supported the RBA policymakers’ continued hawkishness, according to Reuters. The unimpressive Australian data are therefore overshadowed by the RBA vs. Fed drama. Australia’s trade balance decreases to 11,158 million in April, down from 14,822 million in March and 14,000 million in market expectations. As a result, the Pacific nation’s exports decreased to -5.0% from 4.0% the month before, while its imports decreased to 2.0% from 4.0% growth. Several Chinese state banks, including the Bank of China, the Industrial and Commercial Bank of China, and the Construction Bank, reduced their benchmark rates elsewhere. The People’s Bank of China (PBOC), the central bank of the Dragon Nation, may also lower interest rates as a result of this, according to rumours. Furthermore, as PBoC Vice Governor stated, “We have confidence, conditions, and capacity to maintain stable operations of the FX market. Director of China’s National Administration of Financial Regulation Li Yunze also expressed optimism about the Chinese economy, saying, “Economy still recovering,” and adding that demand will be increased.

In this environment, the yields on US Treasury bonds fell, while Wall Street benchmarks increased and put downward pressure on the US dollar. In light of recent rumours of PBoC rate cuts and the hawkish RBA, China’s inflation gauges for May, the Consumer Price Index and Producer Price Index (PPI), will receive significant attention. While negative results may allow the bulls to retreat ahead of the Federal Open Market Committee’s monetary policy meeting next week.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/