GOLD Analysis

XAUUSD Gold price is moving in the Box pattern and the market has reached the horizontal support area of the pattern.

The FED’s decision to delay a rate hike this month, along with two more rate increases anticipated through the end of 2023, caused a decline in gold prices. In 2023, it will not be possible for yellow metal to turn negative due to rate reductions.

The Federal Reserve is anticipated to hold interest rates steady later today, but it could issue a warning that, based on the data, rates could increase further in July as part of the central bank’s ongoing fight against inflation. Recent factory and consumer inflation numbers dipped slightly last month, but they are still far too high in Jerome Powell’s opinion. The dot plot, a closely watched visual for traders to ascertain the FOMC’s thoughts on rates in the coming weeks, is included in the Quarterly Economic Projections, which are also released today. The updated Fed projections for GDP, unemployment, and inflation for the following three years are also included in these economic projections.

SILVER Analysis

XAGUSD Silver Price has broken the Ascending channel in downside.

Ahead of the meeting, gold is edging closer to $1,960 per ounce, helped in part by today’s PPI release that was weaker than anticipated. It will take a significant hawkish surprise at tonight’s meeting for the precious metal to break through this level since it has tested and rejected support zones on either side of $1,935/oz. A hawkish outlook cannot be discounted, though, as Fed chair Powell will want to give himself as much leeway as possible for the upcoming meetings.

USDJPY Analysis

USDJPY is moving in an Ascending channel and the market has reached the higher high area of the channel.

Japan’s Bank The Japanese Yen is expected to decline against counter pairs because there will not be any changes to monetary policy at tomorrow’s meeting. On the final day when the JPY/USD exchange rate turned negative, the FED paused the rate hike. Weakness for the Yen against counter pairs is caused by the Bank of Japan’s loose monetary policy.

On Wednesday, the Japanese Yen gained a little bit against the US Dollar. However, the longer-term outlook for the USD/JPY remains unwaveringly bullish in a week that will undoubtedly highlight the monetary policy differences that favour the dollar so much. The US Federal Reserve will announce its monetary policy decision later on Wednesday, and the Bank of Japan will announce its decision on Friday. The US central bank has tightened lending conditions significantly over the last eleven meetings in response to rising inflation, even though it is expected to pause its protracted cycle of interest rate hikes. In contrast, the Bank of Japan has maintained its ultra-loose monetary policy and views inflation as primarily a global phenomenon. It continues to struggle to create the domestic Japanese demand it so desperately wants to. It is believed unlikely that any automatic monetary tightening would be brought on even by an improvement in the BoJ’s internal inflation view.

Governor Kazo Ueda has emphasised the need to maintain current policy parameters until there is consistent wage growth to go along with price increases. It continues to set a cap of zero percent on local bond yields and targets short-term interest rates at minus 0.1%. At this time, those are a glaring outlier among the major central banks and would be an incredibly loose set of policy objectives at any time. By stating last week that it does not believe there is a need to change its yield policy this month, the BoJ set the stage for market expectations. The Yen will continue to be the primary funding currency for so-called “carry trades,” in which it is exchanged for numerous, higher-yielding units, most notably the US Dollar. The BoJ has a history of intervening to maintain this process’ ‘orderly’ nature; in fact, it did so in September of last year when USD/JPY rose to the 145 handle. The market may be on the lookout for further “intervention” action as the pair approaches that level once more. The BoJ is also most likely to maintain its position that the third-largest country in the world is poised for a modest post-pandemic recovery, buffeted by headwinds from its major export partners. If so, attitudes towards the currency are not likely to change as a result.

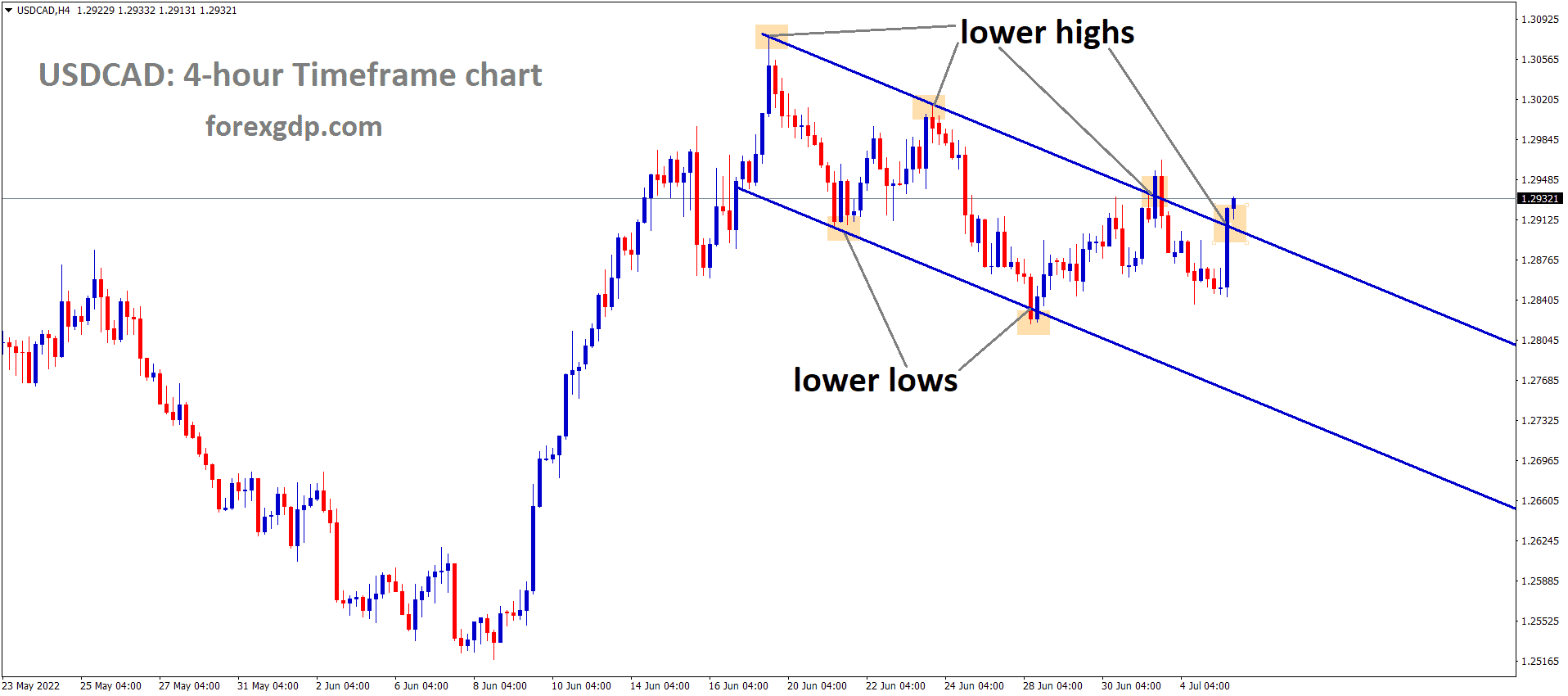

USDCAD Analysis

USDCAD is moving in the Descending channel and the market has fallen from the lower high area of the channel.

The hawkish monetary policy of the Bank of Canada and the current monetary policy pause by the FED benefit the Canadian Dollar. Due to a 33% reduction in US Oil SPR reserves this year, oil prices are still in demand. The Canadian dollar gained strength against other currencies last month as a result of positive domestic data from Canada.

USDCHF Analysis

USDCHF is moving in the Descending channel and the market has fallen from the lower high area of the channel.

This weekend, the Swiss government will vote on raising the corporate tax from the current rate of 11% to 15%. There are 140 counties where this 15% minimum low tax is already in effect. Therefore, the minimum increase that corporate giants can use is 15%, up from 11%. This vote on a corporate tax increase will prevent corporations from receiving a share of profits from high-tax nations that are made in low-tax nations. 2000 foreign companies like Google and 200 Swiss MNCs like Nestle will be impacted by a tax increase.

This weekend, Swiss citizens will decide whether to increase business taxes from the current average of 11% to 15% in order to comply with a global minimum tax rate. Even after the increase, the country would still have one of the lowest corporate tax rates in the world. The Organisation for Economic Cooperation and Development (OECD) and Switzerland reached an agreement in 2021 to ensure that large corporations pay a minimum tax rate of 15%. This will prevent these corporations from trying to evade taxes by moving their profits to low-tax nations. The increase is anticipated to raise $220 billion globally for governments that are struggling to survive a cost-of-living crisis and are cash-strapped in the wake of the Covid-19 pandemic. According to a survey by researchers GFS Bern, 73% of voters will support the change under Switzerland’s direct democracy system, which puts legislation to a public vote. The Swiss government supports the change. Around 2,000 foreign companies, including Google, as well as 200 Swiss multinationals, like Nestle, have offices in Switzerland. The federal government would impose a top-up tax to ensure that businesses are paying 15 percent in corporate taxes, generating up to 2.5 billion Swiss francs ($2.76 billion) in tax revenue. Each of Switzerland’s 26 cantons is free to set its own corporate tax rate.

That would still leave Switzerland with a corporation tax rate that is roughly half that of nations like Germany and Japan and behind the average rate of about 21% in member states of the European Union. According to the plan, the central government would receive 25% of the additional funds, and the cantons would receive 75% of them. The revenue distribution plan, which would see wealthy cantons with low tax rates like Zug and Basel receiving the most money back, was criticised by Social Democratic lawmaker Fabian Molina as absurd. According to the proposed plan, cantons would be able to use the extra money to provide subsidies to draw and keep business. Childcare, research grants, and additional training are a few of the policies being discussed. Karin Keller-Sutter, the finance minister, is in favour of the new tax. The minimum tax is coming, she said last month, whether Switzerland is present or not. According to the OECD plan, if businesses pay taxes that are less than 15% in a given nation, their home governments may add to them until they reach that percentage, eliminating the benefit of shifting profits. The minimum tax was backed by Swiss Holdings, a coalition of 62 foreign corporations with operations in Switzerland, including Nestle, Johnson & Johnson, and IKEA. If the answer is yes, Switzerland will be prepared on time. According to the organisation, it would demonstrate to the world that we should no longer be viewed as a tax haven.

Perhaps most importantly for many, it would guarantee that the funds would remain in Switzerland. The proposal has the support of business groups as well because it will offer certainty even if Switzerland loses some of its allure as a low-tax country. No other nation will have less expensive taxes either. Christian Frey from the lobbying organisation Economiesuisse said, “We want the extra tax revenue to stay in the country and be used to improve its attractiveness for businesses.” The top-up tax, according to Stefan Kuhn, Head of Tax and Legal at KPMG Switzerland, gives cantons the resources to take proactive measures to maintain their competitiveness. Kuhn declared he would support the plan, which goes into effect in 2024. There is not a logical defence for this that I can think of.

EURUSD Analysis

EURUSD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

In order to control the 6.1% inflation rate in the Euro region over the coming days, the ECB is anticipated to raise interest rates by 25 basis points at its meeting today. The FED paused the rate increase on the final day and hinted that there would be additional rate increases at the July or September meeting. After two GDP-negative quarters, Germany entered a recession period.

Following its Tuesday recovery from its low point in late May and ahead of today’s Federal Reserve meeting, the euro fell today. Tomorrow will be the day for the monetary policy review by the European Central Bank (ECB). US CPI softened to 4.0% year-on-year to the end of May yesterday, down from the anticipated 4.1% and previous 4.9%. Core CPI for the same time period came in higher than expected (5.3% vs. 5.5%), beating expectations of 5.2%. The market’s perception that the Fed may hold off on raising rates today but may do so again when they meet in July or September may be confirmed by the data. The post-decision press conference and the language used by Fed Chair Jerome Powell to provide guidance on the rate path are likely to garner the majority of the attention. Interest rate markets expect the ECB to increase rates by 25 basis points in an effort to control inflation that is over 6%. Ahead of the Norges Bank’s decision on the deposit rate next week, the Norwegian krone is aiming for a 2-month high against the euro.

According to last week’s CPI data, the Nordic country’s annual growth rate accelerated to 6.7% by the end of May. The Norges Bank’s meeting next week may become more hawkish due to rising price pressures. On Tuesday, the price of crude oil had a strong session and has maintained its gains going into trading on Wednesday. At the time of printing, the Brent contract is fluctuating around US$ 74.50 bbl while the WTI futures contract is close to US$ 69.50 bbl. The gold price, which is currently trading around US$ 1,960, seems to have been hurt by the rising Treasury yields so far this week. The North American equity indices all registered respectable gains as the cash market closed, with the Russell 2000 taking the lead with a gain of 1.23%. Ironically, the futures market price for the December Fed funds rate is higher the higher Wall Street travels.

AUDUSD Analysis

AUDUSD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

With 75.9K jobs added in May, Australia’s employment figures were strong compared to expectations of 17.5K and -4.3K in April. 3.6% unemployment rate in May versus 3.7% anticipated. It is widely anticipated that the RBA will increase rates by another 25 basis points in July.

After a strong jobs report on Thursday that included a decrease in the unemployment rate, the Australian Dollar reversed some of its earlier losses. This could reignite price pressures and make the RBA’s July meeting a little more interesting. In May, the unemployment rate was 3.6% as opposed to the predicted and previous 3.7%. Australia added 75.9k new jobs in the month, significantly more than the 17.5k predicted and the -4.3k added the month before. The increase in full-time employment of 61.7k and the slight increase in participation rate to 66.9% from 66.7% were noteworthy. Early this month, the RBA increased interest rates by 25 basis points (bp), to 4.10%. Prior to today’s data, the overnight index swaps (OIS) market gave the RBA’s decision to raise the cash rate at its July monetary policy meeting a 20% chance. They currently estimate that a 25 bp lift has a little bit more than a 40% probability.

NZDUSD Analysis

NZDUSD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

NZD’s 1Q GDP was down 0.10 percent from the previous quarter’s -0.7 percent. Therefore, a technical recession in New Zealand will be identified as negative readings occurring in two consecutive quarters. At 3.4%, the unemployment rate is at a historical low. The annual CPI is currently 6.7%, and the RBNZ will continue raising rates to prevent a severe recession in New Zealand.

Today’s GDP came as a shock to the New Zealand Dollar, which had been on a tear higher thanks to a weakening US Dollar. The S&P/NZX 50 equity index is currently slightly up. The quarterly number met expectations, but there were some downward revisions to the annual read. Quarter-to-quarter GDP for the first quarter was revised down from -0.6% to -0.1%, which was in line with expectations. Lower revisions were also made to earlier quarters. Instead of the 2.6% predicted and the 2.2% previously, the annual GDP as of the end of March was 2.2%. The real estate institute of New Zealand reported that house sales decreased -0.4% year over year to the end of May before the GDP data was released. a significant improvement over the -15.3% figure from April.

According to data released by Statistics New Zealand yesterday, food prices increased by 0.3% in May compared to a 0.5% increase in April. As a result, year-over-year growth was 12.1% to the end of May, slightly less than the previous reading of 12.5%, which was the highest reading in 36 years. Statistics New Zealand also reported earlier this week that there were a net 72,300 migrant arrivals in the April-to-April fiscal year. This was made up of 26,100 migrant departures by New Zealanders and 98,400 non-NZ migrant arrivals. The increase could help to some extent with the labour shortage that is being reflected in the historically low unemployment rate of 3.4%.The RBNZ will need to perform a delicate dance when they meet again on July 12 in order to avoid a severe recession. Two consecutive quarters of negative growth are the general requirements for a recession.

Even though there has been a slowdown, the annual CPI is still stubbornly high at 6.7% at a time when the economy is slowing down. The market for overnight index swaps anticipates no additional bank rate increases this year, leaving the overnight cash rate at 5.50%. According to the response to last night’s Federal Open Market Committee meeting, fluctuations in the US dollar may continue to influence the direction of the New Zealand dollar. The Fed maintained rates, and the subsequent statement seems to have been interpreted as remaining hawkish with an improvement in the so-called dot plot. Soon after, Fed Chair Jerome Powell gave a press conference speech that was perceived as having a dovish slant. There are a tonne of data points and Fed commentary between now and the next FOMC on July 26 that the market will need to take into consideration.

GBPCHF Analysis

GBPCHF is moving in the Box pattern and the market has reached the resistance area of the pattern.

UK GDP MoM for April came in at 0.20% compared to -0.30% for March.GBP was strengthened against counter pairs by UK domestic data that came in at positive numbers. According to UK Chancellor Jeremy Hunt, the UK economy will grow as long as there is less inflation, which will cause the reading to drop to half by the end of the year.

This morning, the UK GDP was the main concern for traders, bringing the British pound back into the picture. Due to the UK GDP release being generally in line with expectations, cable is trading relatively flat after yesterday’s positive close.After a 0.3% decline in March, the monthly GDP increased by 0.2% in April. For the three months ending in April, GDP increased by 0.1%. The services sector increased (0.3%) after declining by 0.5% in March. Although the industrial and manufacturing sectors have some shortcomings, the report is overall short-term positive for the pound. Looking at the big picture, it appears that UK growth is somewhat stagnant, which may later give rise to concern. In response to the positive UK economic data, Chancellor of the Exchequer Jeremy Hunt said, High growth needs low inflation and we must stick relentlessly to our plan to halve rate this year. Yesterday, Bank of England (BoE) Governor Andrew Bailey and Dhingra both emphasised similar ideas regarding inflation.

The peak rate for 2023 has increased significantly since yesterday’s jobs report, rising from about 5.48% to almost 5.77% (see table below), or about 30 basis points. The UK 2-year gilt yield is currently above the time period surrounding former PM Liz Truss and at levels last seen in 2008. This might renew worries about Defined Benefit (DB) pension plans because the value of these plans has historically moved counter to gilt yields.

AUDCHF Analysis

AUDCHF is moving in an Ascending channel and the market has reached the higher high area of the channel.

However, the weak Chinese data partially offset the positive domestic data for the Aussie Dollar. Despite the fact that the year-over-year figure of 3.5% was in line, the total industrial production for the year as of the end of May was 3.6% rather than the predicted 3.9%. 12.7% year-over-year growth in retail sales fell short of forecasts of 13.7% and 18.4%, respectively. Fixed-asset investment growth has been slower than expected, at 4% so far this year. As anticipated, the survey’s estimate of the unemployment rate in urban areas remained at 5.2%. When the People’s Bank of China reduced the 7-day reverse repo rate from 2% to 1.9% on Tuesday, the markets received a small boost. Then, today, the rate on the medium-term lending facility for one year was lowered from 2.75% to 2.65%.

The second-largest economy in the world is currently performing poorly, which has sparked speculation about additional stimulus measures from Beijing. The Federal Open Market Committee’s overnight decision to maintain its target rate, as well as the subsequent statement and press conference, set off some fireworks for the AUDUSD. Looking ahead, the pricing of an RBA rate move, Fed comments regarding additional hikes, and the economic outlook for China, if there is a significant change in policy there, could all influence the direction of the Australian dollar.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/