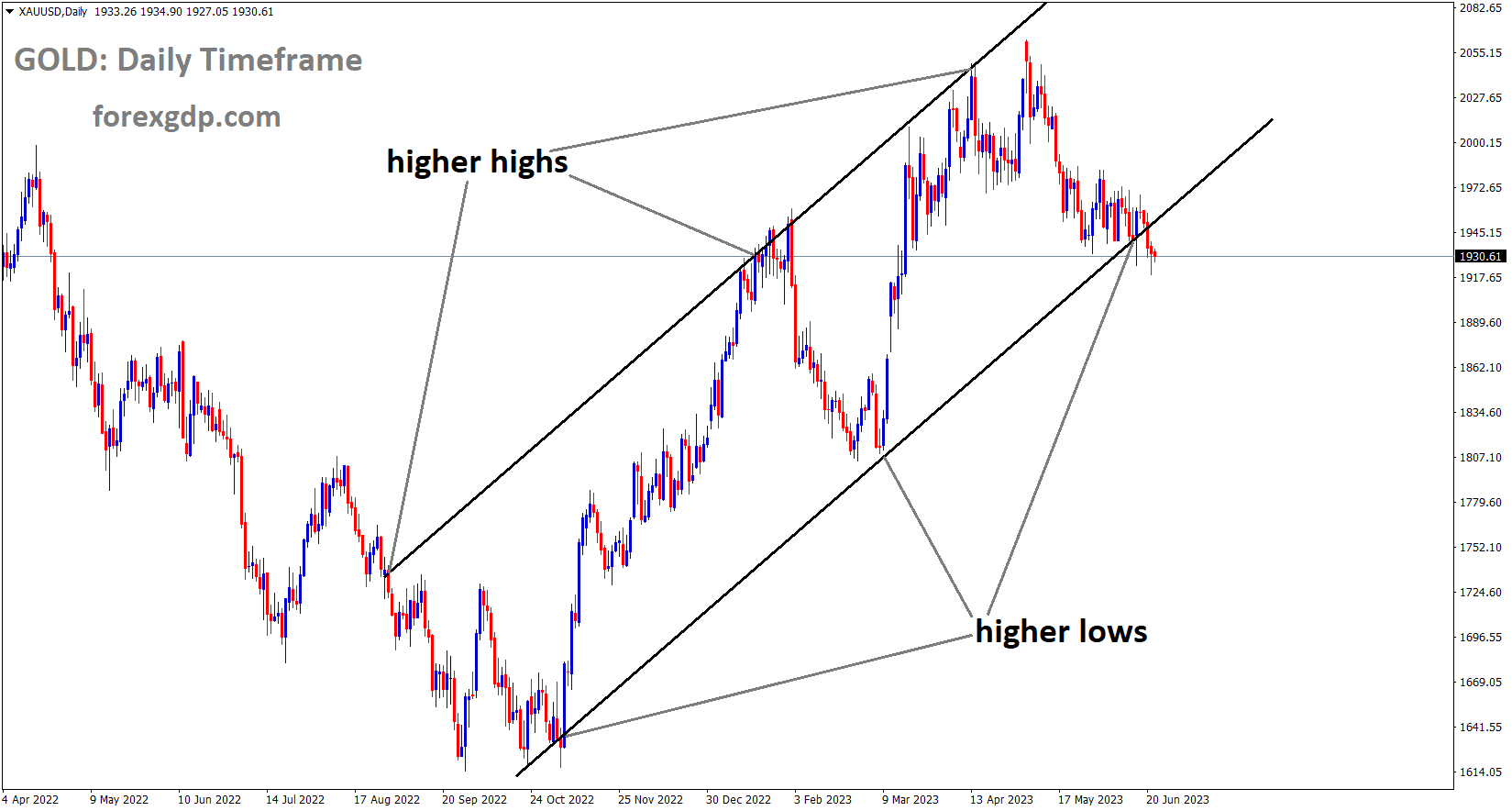

GOLD Analysis

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel.

It’s regrettable that big banks are raising rates in response to the People’s Bank of China lowering its lending rates to 1.9% from 2.0%. Gold prices are feeling the effects of the PBOC’s rate cut. As a considerable boost is being allocated to China’s recovery from Covid-19, the country’s demand for gold has fallen.

As markets wait for a flurry of central bank decisions, the gold price continues to lag behind, even as it struggles to break through critical support levels in the medium run. Gold Price movements are constrained not just by pre-announcement jitters, but also by the holiday in China and a lack of clear catalysts about the Federal Reserve. In his semi-annual hearing before the US House Financial Services Committee the day before, Fed Chairman Jerome Powell maintained his hawkish slant. There have been no new comments, and other Fed officials’ contradictory pronouncements have weighed on the US Dollar, limiting XAUUSD’s ability to move. However, the Gold Price is under pressure due to the Sino-American friction and the defence of the higher for longer interest rate perspective by major central banks. Moving on, the market could get a shot of volatility from upcoming monetary policy statements in the UK, Switzerland, Mexico, Turkey, and Indonesia.

USDJPY Analysis

USDJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

The Japanese Cabinet Office’s monthly assessment report noted for the first time in 11 months that employment had increased. The global economic slowdown, inflation, and financial market volatility have all contributed to a weak economic recovery. Both corporate profits and private consumption are on the upswing.

USD Index Analysis

USD index is moving in the Descending channel and the market has reached the lower low area of the channel.

For the first time in 11 months, the Japanese Cabinet Office has raised its assessment of the country’s job situation, writing that employment trends showed improvement recently in its monthly assessment report. The economy is showing moderate improvement, which has led analysts to maintain their bullish long-term forecast. However, it maintained its wariness regarding the risks posed by a global economic downturn, price rises, and volatile financial markets. The June report confirmed the optimistic May forecast, stating that private consumption and capital expenditures were on the rise. Overall corporate profits are expected to improve somewhat.

USDCAD Analysis

USDCAD has broken the Box pattern in downside.

Strong consumer confidence and wage growth, along with a pick-up in labour demand, were discussed at length during a Governing Council meeting of the Bank of Canada on June 7th, suggesting that inflation could be considerably higher than projected. To bring inflation under control and back down to the 2% objective, the Fed unexpectedly raised interest rates in June. Based on the resurgence in household spending growth, consumer confidence, and disinflationary momentum, members of the Bank of Canada felt that monetary policy was not restrictive enough and voted to raise the key interest rate by 25 basis points to 4.75% at their June 7 meeting.

Crude Oil Analysis

Crude Oil Price is moving in an Ascending channel and the market has reached the higher high area of the channel.

Members feared inflation would remain over the 2% target and were sceptical about the sustainability and severity of the recent disinflation. The Canadian government’s top policymakers all agreed that the country’s consumption was higher and more evenly distributed than expected. The Governing Council agreed that supply and demand imbalances will take longer to correct than initially estimated. The Governing Council has kept employment regulations at a minimum. Despite this, job growth and openings have slowed from their previous highs. Concerns that inflation could become stranded above the 2% objective and the strength and longevity of continued disinflation were raised in response to the core inflation numbers. Members were concerned that monetary policy was too lax due to rising household expenditure growth, rising consumer confidence, and declining disinflationary momentum. They decided in June to tighten monetary policy after data accumulated since January showed that doing so was necessary to restore equilibrium between supply and demand in the economy and bring inflation back to the 2% target.

EURCHF Analysis

EURCHF is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

Since inflation was so close to 2% in the previous month, the SNB is expected to raise rates by 25 basis points today. Therefore, a more hawkish tone, like as 50bps, may discourage spending by consumers and hamper the efficiency of firms.

Interest rates will be decided at today’s Swiss National Bank meeting. ING’s economists consider the future of the CHF before making a call. Most economists predict a rise of 25 basis points, but a sizeable minority anticipates 50 basis points. Despite a reduction in core inflation to below 2% on an annual basis, the SNB has maintained its hawkish tone in recent statements. We calculated that the SNB sought to manufacture a 5% annual nominal increase to maintain a stable real CHF exchange rate in September of last year. About that much has transpired. We were mistaken since the majority of the flow has been through USD/CHF rather than EURCHF.

GBPUSD Analysis

GBPUSD is moving in the Descending channel and the market has reached the lower high area of the channel.

After the inflation number printed hot this week, the Bank of England is expected to raise interest rates by 25 basis points at today’s meeting. Since March 1992’s CPI was higher than in any other developed country, the Bank of England must be under pressure to immediately bring inflation under control.

This Thursday, the Bank of England is on course to announce its 13th consecutive rate increase as it continues to battle stubbornly high inflation rates. The United Kingdom still maintains one of the highest rates of consumer price inflation among the major advanced economies, despite the fact that it has decreased from double-digit levels. As a result, in the absence of Governor Andrew Bailey’s news conference and revised economic estimates, the primary focus will continue to be on the language of the Bank of England’s monetary policy statement for new clues on its rate hike outlook. Below 1.2800, the GBP/USD is maintaining its rebound gains as the US Dollar licks its wounds close to monthly lows following the sell-off sparked by less hawkish Chair Jerome Powell’s speech. In his testimony on Wednesday before the House Financial Services Committee, Fed Chair Jerome Powell stated that inflation pressures continue to run high, and the process of getting inflation back down to 2% has a long way to go, and that nearly all members expected future rate rises. The Core CPI reached its highest rate since March 1992 in the UK inflation numbers, which were hotter than anticipated. Markets are currently pricing in a 52% probability for a 25 bps BoE rate hike in June, down from about 78% before the release of the UK CPI data. Investors appear to be split between a 25 bps and 50 bps increase. Early on Thursday, markets are cautious due to concerns of additional central bank tightening. The benchmark 10-year US Treasury bond yields are trading close to weekly troughs near 3.70%, while US S&P 500 futures are slightly lower. The US Jobless Claims and Day 2 of Powell’s testimony will also garner some attention, but the BoE’s policy statements will be crucial to the short-term direction of the GBP/USD pair.

GBPCHF Analysis

GBPCHF is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

Could the BoE boost rates by 50 basis points tomorrow rather than by 25 basis points, wondered Societe Generale analysts. After the most recent inflation shock in the UK this morning, that is the question. In May, Core CPI climbed to a new high of 7.1% yoy. We already know that wage growth surged to 7.2% yoy last week. Both figures are edging further away from the BoE’s 2% inflation objective, suggesting that action may be required. The BoE must decide whether to speed up again in order to attain a higher peak sooner or to extend the tightening cycle by a few months. According to Societe Generale, both possibilities run the danger of destabilising the housing market. On June 22, the BoE is anticipated to increase the benchmark interest rate by 25 basis points, from 4.50% to a 15-year high of 4.75%. At 11:00 GMT, the interest rate decision and meeting minutes will be made public. BoE Governor Andrew Bailey stated last week that the labour market was very tight and that inflation was taking a lot longer than expected to decline. After the most recent data from the Office for National Statistics revealed that the UK’s ILO Unemployment Rate decreased to 3.8% in the quarter to April from the 3.9% reported in the three months to March, exceeding the market consensus of a 4.0% print, Bailey gave a statement. In contrast, fewer persons received unemployment benefits in May. In April, the average weekly wage in the UK, excluding bonuses, was 7.2% 3Mo/YoY, up from 6.8% the previous month and 6.9% anticipated. It’s important to note that the numbers from April include the effects of a 9.7% increase in the minimum wage. Markets increased their bets on the BoE raising rates as a result of the data, pushing two-year government bond yields to their highest level since 2008. Markets increased their forecast for the BoE rates to reach their peak to as high as 6.0% by early 2024.

However, two separate surveys issued a day before the UK Consumer Price Index data suggested that UK food price inflation is falling, suggesting that it may have already peaked, casting doubt on a future BoE hawkish rate hike. The lowest reading this year, according to market research firm Kantar, was reported for the four weeks ending June 11 for supermarket price hikes, which dropped to 16.5% from 17.2% the previous month. According to Lloyds Bank Plc, production costs for UK producers of food and beverages decreased for the first time in December 2016 according to Bloomberg on Tuesday. The crucial UK inflation statistics released on Wednesday confirmed the conventional wisdom that the BoE must maintain its pace of interest rate hikes in order to combat sticky inflation. The UK’s annual CPI increased by 8.7% in May at the same rate as in April, according to the most recent figures released by the UK Office for National Statistics. An 8.4% gain was predicted by the market. Compared to the 6.8% rise witnessed in April, the Core CPI measure gained 7.1% YoY last month, exceeding expectations for a 6.8% growth rate. Nevertheless, it seems unlikely that the Bank will raise rates by 50 basis points because doing so would send the UK economy into a recession. Instead, the markets anticipate that the BoE would favour a number of 25 bps rate increases throughout this year.

NZDUSD Analysis

NZDUSD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

Prime Minister Hipkins of New Zealand has publicly stated his disagreement with Trump’s statements towards China. That Dictator Xi Jinping is in charge of China. If the Chinese people feel that their government is not serving them well, they have the power to form a new one. The Prime Minister of New Zealand will be in China from June 25-30 to give a speech on the topic of maintaining trade relations.

Before his official visit to China at the month’s end, New Zealand Prime Minister Chris Hipkins stated on Thursday that he disagreed with Vice President Joe Biden’s characterization of Chinese President Xi Jinping as a tyrant. Hipkins told reporters, No, and the form of government that China has is a matter for the Chinese people. Hipkins responded to a reporter’s question on whether or not Chinese citizens had a say in the form of government by saying, if they wanted to change their system of government, then that would be a matter for them. From June 25-30, Hipkins will head a trade delegation consisting of some of New Zealand’s largest corporations to China. He’ll talk politics with Xi Jinping, Li Qiang, and Zhao Leji, chairman of the NPC’s standing committee. On Wednesday, China responded to Biden’s characterization of President Xi Jinping as a dictator by calling his comments ludicrous and a provocation. This unexpected escalation came after both countries had made efforts to ease tensions.

AUDCHF Analysis

AUDCHF has retest the broken area of the Box pattern.

This week in Beijing, China’s Vice Premier He Lifeng met with Singapore’s Temasek Chairman Lim Eng Heng and reported that manufacturing, services, and consumer spending are all on the upswing in China as of the first half of 2023. China’s economy is on the mend after suffering damage during Covid-19, with commodity prices remaining constant and industry activity increasing.

He Lifeng, the vice premier of China, told Singapore’s Temasek Chairman Lim Boon Heng during a meeting they had earlier this week in Beijing that the country’s economy is exhibiting strong momentum in the first half of the year. The economy has made a comeback and improved. He claimed that a plentiful grain crop this summer is likely, that manufacturing has been expanding gradually, and that the service sector is expanding relatively quickly. Coordination between investment, consumption, and export played a key role in maintaining stability in employment and commodity prices as well as in the creation of high-quality infrastructure.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/