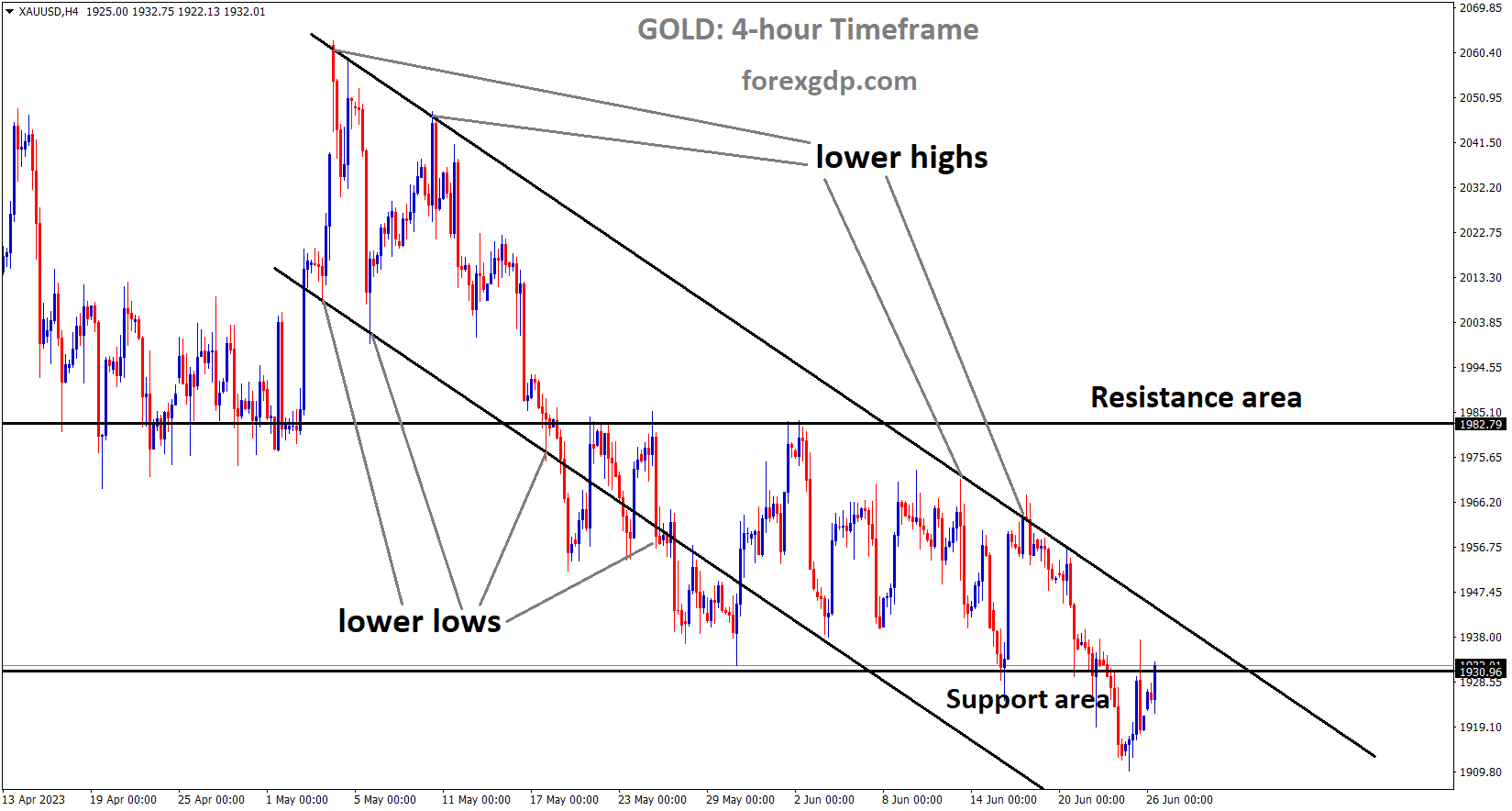

GOLD Analysis

XAUUSD Gold price is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

After the US dollar continued to rise last week, gold prices fell. Powell, the chairman of the Federal Reserve, reiterated that rates would rise in July due to a pause in June. Russia-Ukraine conflict and China’s recovery from Covid-19 are both negative factors for the consumption of gold.

The price of gold is up to start the new week and hopes to build on Friday’s modest recovery from the $1,910 region, which would be its lowest point since March 16. Although it has increased by almost 0.35% on the day, the XAUUSD is still trading well below the 100-day Simple Moving Average through the Asian session. The US Dollar faces some supply on Monday in the midst of a slight decline in US Treasury bond yields as it struggles to capitalise on its recovery move over the past two days from its lowest level since May 11. This helps to support the price of gold, a safe haven, along with concerns about the fallout from the Russian mutiny. When a deal guaranteeing their safety and the exile of their leader, Yevgeny Prigozhin, to Belarus was reached, Russian mercenaries who had taken over the southern city of Rostov on Saturday and moved towards Moscow withdrew. However, as evidenced by the generally positive sentiment surrounding US equity futures and what may be a cap on gains for the safe-haven Gold price, the markets do not respond significantly to the most recent geopolitical development. In addition, major central banks taking a more hawkish stance could help keep a lid on the non-yielding yellow metal. Recall that this month saw a surprise 25 basis point rate increase from the Reserve Bank of Australia and the Bank of Canada, while the European Central Bank increased interest rates to their highest level in 22 years.

Additionally, on Thursday, the Bank of England, the Swiss National Bank, and the Norges Bank all increased their benchmark interest rates. The Federal Reserve hinted that by the end of this year, borrowing costs might still need to increase by as much as 50 basis points. Additionally, Fed Chair Jerome Powell reiterated during his two-day congressional testimony last week that the central bank is likely to increase interest rates again this year, albeit cautiously, in order to combat persistently high inflation. This should prevent further USD losses and dampen the price of gold.The Core Personal Consumption and Expenditure Price Index, the Fed’s preferred inflation indicator, is due out on Friday. Traders may decide to hold off until then. The market’s expectations for the Fed’s next course of action will be significantly influenced by the data, which will also have a significant impact on USD demand and the price of gold denominated in US dollars. This makes it wise to hold off on positioning for any significant appreciating move until there is strong follow-through buying before determining that the XAUUSD has formed a near-term bottom.

USDJPY Analysis

USDJPY is moving in an Ascending channel and the market has reached the higher low area of the channel.

The Bank of Japan is under pressure to tighten policy after Friday’s decline in CPI data. If not, the YCC Control area will need to be modified in the upcoming months to keep inflation under control at a target of 2%. This week’s Fed Powell speech is scheduled, and another 25 basis point rate hike in July is anticipated to weaken the Japanese Yen relative to the US Dollar.

Due to last week’s challenging trading conditions, the Japanese Yen is starting this week on a generally weaker note as a result of Fed Chair Jerome Powell’s hawkish testimony and Friday’s drop in Japanese CPI. Although the Bank of Japan will find it challenging to abandon its ultra-loose monetary policy, changes to Yield Curve Control are still a possibility. The majority of the upcoming week’s data will be US-focused, including the core PCE print, the Fed’s preferred inflation indicator. As money market probabilities inch closer to a 25bps hike in July, Mr Powell will likely continue on his path of tightening policy during his upcoming speech rather than holding the interest rate steady. Durable goods orders, GDP, and Michigan consumer sentiment are additional important releases that will help paint a clearer picture of the overall US economy. Recessionary fears may resurface if data indicate that the economy is slowing, which could benefit the safe-haven Yen.

USD index Analysis

USD index is moving in the Descending channel and the market has reached the lower high area of the channel.

Data from the US Core PCE Index show an annual growth rate of 4.7%, but 3.8% is predicted for May after 4.4% in April.

Before the important US PCE price index data is released on Friday, the US dollar may stay in a range. The US Federal Reserve also continues to be data dependent, focusing on changing economic activity and inflation data. Markets, who are not convinced that the Fed can hike twice more this year, may be swayed by the Fed’s preferred inflation gauge. At a Wall Street Journal forum, Chicago Fed President Austan Goolsbee reaffirmed this, saying the institution was in a “wait and see” mode as more data came in.

Earlier in the week, Powell reiterated the central bank’s hawkish stance in testimony to lawmakers on Capitol Hill, saying that additional rate hikes may be necessary. He also added that interest rates would increase gradually going forward. Powell stated this during a Thursday hearing before the Senate Banking Committee: “We are at least close to where we think our destination.” Regarding the June skip, Powell provided a little more context by stating that the purpose of keeping rates constant was precisely to slow the rate at which the Fed was raising borrowing costs. In a separate statement, Fed Governor Michelle Bowman indicated on Thursday that at least two additional rate hikes were necessary. While the PCE Price Index is anticipated to have slowed from 4.4% in April to 3.8% in May, the Core PCE Price Index is predicted to remain unchanged at 4.7% on a yearly basis. Aside from the inflation data, convergent monetary policy outlooks (as global central banks continue to tighten), the resilience of the global economy, and tight ranges of currencies all contribute to the continuation of this trend.

Agustin Carstens of the Bank for International Settlements issued a warning that the public and corporate financial stress brought on by central banks’ rising interest rates could have a material impact on risk. In order to prevent a recession, the central bank must modify its tightening policies.

The general manager of the Bank for International Settlements (BIS), Agustin Carstens, issued a warning in the organization’s annual report, which was released on Sunday, stating that the world economy was at a critical juncture as nations struggled to control inflation. Monetary and fiscal policies should have more modest goals going forward. It is necessary to correct unrealistic expectations regarding the scope and durability of financial and fiscal support. A significant risk exists for an inflation psychology to emerge. There is a significant risk of additional financial strain.

EURGBP Analysis

EURGBP is moving in the Descending channel and the market has fallen from the lower high area of the channel.

Euro was too weak compared to other currency pairs last week due to Euro PMI data’s disappointing results. Therefore, the ECB is faced with the decision of whether or not to proceed with a further rate hike in upcoming meetings. This week’s CPI data for Germany and the Eurozone are scheduled.

In the wake of Friday’s disappointing release of Eurozone PMI prints, traders also appear hesitant to make aggressive bullish bets around the common currency, which worsens a policy conundrum for the European Central Bank (ECB). Recall that the two largest economies in the Eurozone, France and Germany, showed a sharp slowdown in business activity in S&P Global’s preliminary report. Additionally, the flash Composite Eurozone PMI from HCOB dropped to a five-month low, adding to concerns about economic headwinds brought on by rising borrowing. Since neither the Eurozone nor the US released any pertinent market-moving economic data on Monday, traders will look to ECB President Christine Lagarde’s speech for motivation.. However, attention is still on Friday’s release of the US Core PCE Price Index, the Fed’s preferred inflation indicator, which will be crucial in determining the direction of future spot price movements and driving the USD.

GBPCAD Analysis

GBPCAD is moving in an Ascending channel and the market has rebounded from the lower low area of the channel.

The unexpected rate increase by the Bank of Canada this month helped the Canadian Dollar appreciate against the US Dollar. The S&P Global rating agency reduced China’s GDP from 5.5% to 5.2%, which has led to lower oil prices.

The Loonie pair ignores the depressed Oil prices and celebrates the US Dollar’s depreciation amid cautious market optimism. Despite risk-positive headlines suggesting further stimulus from Beijing, WTI crude oil accepts offers to recover from its intraday low near $69.50. Despite this, the global credit rating agency S&P recently lowered its estimates for China’s GDP growth for 2023 from 5.5% to 5.2%. In addition to the S&P news, the oil price has been impacted by headlines that suggest major investors have halted their optimism regarding China, as well as hawkish remarks from Fed officials and relatively positive US data. However, reports suggesting earlier Chinese stimulus and scepticism about Russian President Vladimir Putin’s influence in Moscow favour sentiment, support the price of WTI crude oil, and weaken the US dollar.

Crude Oil Analysis

Crude Oil price has broken the Ascending channel in downside.

Concerns about earlier stimulus from China were raised by Ning Jizhe, a former vice head of the National Development and Reform Commission and deputy head of the economic committee of the Chinese People’s Political Consultative Conference. In this regard, Reuters reported that “heavily armed Russian mercenaries withdrew from the southern Russian city of Rostov under a deal that stopped their quick advance on Moscow but raised questions on Sunday about President Vladimir Putin’s hold on power.

GBPUSD Analysis

GBPUSD is moving in the Descending channel and the market has reached the lower high area of the channel.

In 2008, the Bank of England increased interest rates by 50 basis points to a level close to 5.00%. Due to rising labour costs and wage prices, the Bank of England took action to slow the rate of inflation. YoY inflation May’s printing rate of 8.7% was higher than the Bank of England’s target of 2%.

The lacklustre response to the Bank of England’s (BoE) unexpected interest rate increase last week may indicate that the British pound’s recent rally against some of its competitors is about to experience a slight setback. The BoE shocked the markets by increasing its benchmark rate by 50 basis points vs 25 basis points expected to 5%, the highest level since 2008 and its largest increase since February. BoE noted that second-round effects in domestic price and wage developments caused by external cost shocks are likely to take longer to unwind than they did to emerge. The UK’s central bank was under pressure to take action after data released last week revealed that headline inflation was unchanged in May at 8.7% on-year.

After pausing in April, the BoE increased its benchmark rate by 25 basis points in May prior to last week’s increase. The benchmark rate is currently expected to peak at 6.25% by the end of the year, according to the markets. Forecasts for economic growth for the current year have been updated as a result of a strong run of UK data since mid-February, as indicated by the Economic Surprise Index. Aggressive tightening, however, could harm 2019 prospects, increase the chance of a recession, and threaten the overbought GBP.

NZDUSD Analysis

NZDUSD is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

S&P Global reduced its forecast for China’s GDP to 5.2% from 5.5% this year as a result of the RBNZ’s aggressive rate hike in the cycle similar to the 1999 year.The NZD fell against the USD after US Fed Powell’s last week’s speech, which was hawkish on rate hikes. Due to Covid-19 Comeback, China has suffered in the areas of manufacturing, industry, consumer spending, and sales.

During the Asian session on Monday, the NZDUSD pair picks up significant positive momentum and surges to the 0.6175 area in the final hour, breaking a two-day losing streak to a one and a half-week low. On the first day of a new week, the US Dollar is under some selling pressure and, for the time being, it appears to have stalled its recent recovery from the lowest level since May 11 reached last Thursday. A slight decline in US Treasury bond yields is thought to be a major factor weakening the US dollar and supporting the NZDUSD pair. In addition, a bullish outlook for US equity futures appears to weaken the safe-haven dollar and strengthen the risk-averse New Zealand dollar. However, any optimism should be kept in check due to concerns about a global economic downturn, particularly in China. S&P Global revised its estimates for China’s GDP this year from 5.5% to 5.2%, adding fuel to the fears. This follows recent downgrades by several large international banks, including Nomura, Citibank, UBS, and Goldman Sachs. The hawkish outlook of the Federal Reserve should also restrain USD losses and control the NZDUSD pair.

It is important to remember that the Fed decided to pause its rate hike cycle earlier this month, but it also hinted that borrowing costs might still need to increase by as much as 50 basis points by the end of this year. Additionally, Fed Chair Jerome Powell reaffirmed that the central bank will raise interest rates once more this year to control high inflation, albeit at a “careful pace.” Powell added that the Fed will not cut rates any time soon and will hold off until it is certain that inflation is tumbling to the target level of 2%. Apart from that, it is prudent to exercise caution before placing aggressive bullish bets around the NZDUSD pair due to the Reserve Bank of New Zealand’s explicit signal that it was finished with its most aggressive hiking cycle since 1999. This makes it prudent to wait for strong follow-through buying to confirm that the recent sharp pullback from the area of mid-0.6200s, or the monthly swing high, has run its course in the absence of any pertinent macroeconomic data from the US. The US Core PCE Price Index, the Fed’s preferred inflation indicator, will be released this week and is expected to be significant, according to market participants on Friday.

AUDCHF Analysis

AUDCHF is moving in the Descending channel and the market has reached the lower low area of the channel.

After the RBA failed to raise interest rates when a meeting in July was anticipated, the Australian dollar fell from a 4-month high. Recession risk in Australia is indicated by the yield curve inversion for the 3-year bond yield rising to 5 basis points for the 10-year bond.

Following the Federal Reserve’s return to hawkish rhetoric last week at a time when the domestic interest rate market is not anticipating a hike from the RBA in July, the Australian Dollar fell from a 4-month high. Although the market anticipates another 50 basis point increase by year’s end, raising the target cash rate to 4.6%, the next RBA monetary policy meeting may not result in a tightening of rates. Every choice moving forward will be based on the data, as many central banks are arguing at the moment. On July 26, Australia’s second quarter CPI will be released, and the market will be closely watching it for hints about the RBA’s decisions at its meeting in August. On a panel at the European Central Bank (ECB) Forum on Central Banking this Wednesday, Federal Reserve Chair Jerome Powell will participate.

Last week marked the first inversion of the Australian yield curve since the GFC. The 3-year bond had a higher yield than the 10-year note by as much as 5 basis points. The bond market infers that an economic slowdown may occur at some point in the future when yield curves flatten and then invert. Naturally, the RBA is attempting to accomplish this in order to control dangerously high inflationary pressures. RBA Governor Philip Lowe has made an effort to outline a strategy for taking the difficult path of keeping prices in check while preserving economic growth and averting a recession. The likelihood that this plan will be carried out successfully is rising, as seen by the bond market. Given how the situation in Russia is changing, geopolitics may affect markets this coming week.

CADCHF Analysis

CADCHF is moving in the Descending channel and the market has reached the resistance area of the pattern.

Thomas Jordan, the chairman of the SNB, stated in an interview that the most recent rate increase is insufficient to control Switzerland’s inflation reading. Therefore, a rate increase at the SNB’s next monthly monetary policy meeting is anticipated.

The Swiss National Bank’s (SNB) recent interest rate hike was’very likely not quite’ enough to control inflation in Switzerland, according to Thomas Jordan, the SNB’s chairman, who spoke in an interview that was broadcast by Swiss broadcaster SRF on Saturday, according to Reuters. In light of this, the S&P500 Futures recover from their lowest levels in a week and move back towards the round 4,400 mark, rising 0.20% intraday near 4,398 at the latest. However, despite ending a two-week downtrend, US 10-year Treasury bond yields are still stuck around 3.73%, while the two-year counterpart is poised to win for a fourth straight week by press time, hovering around 4.74%. Looking ahead, India’s light calendar highlights the US inflation data and the top central bankers’ speeches at the European Central Bank (ECB) Forum as the main drivers.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/