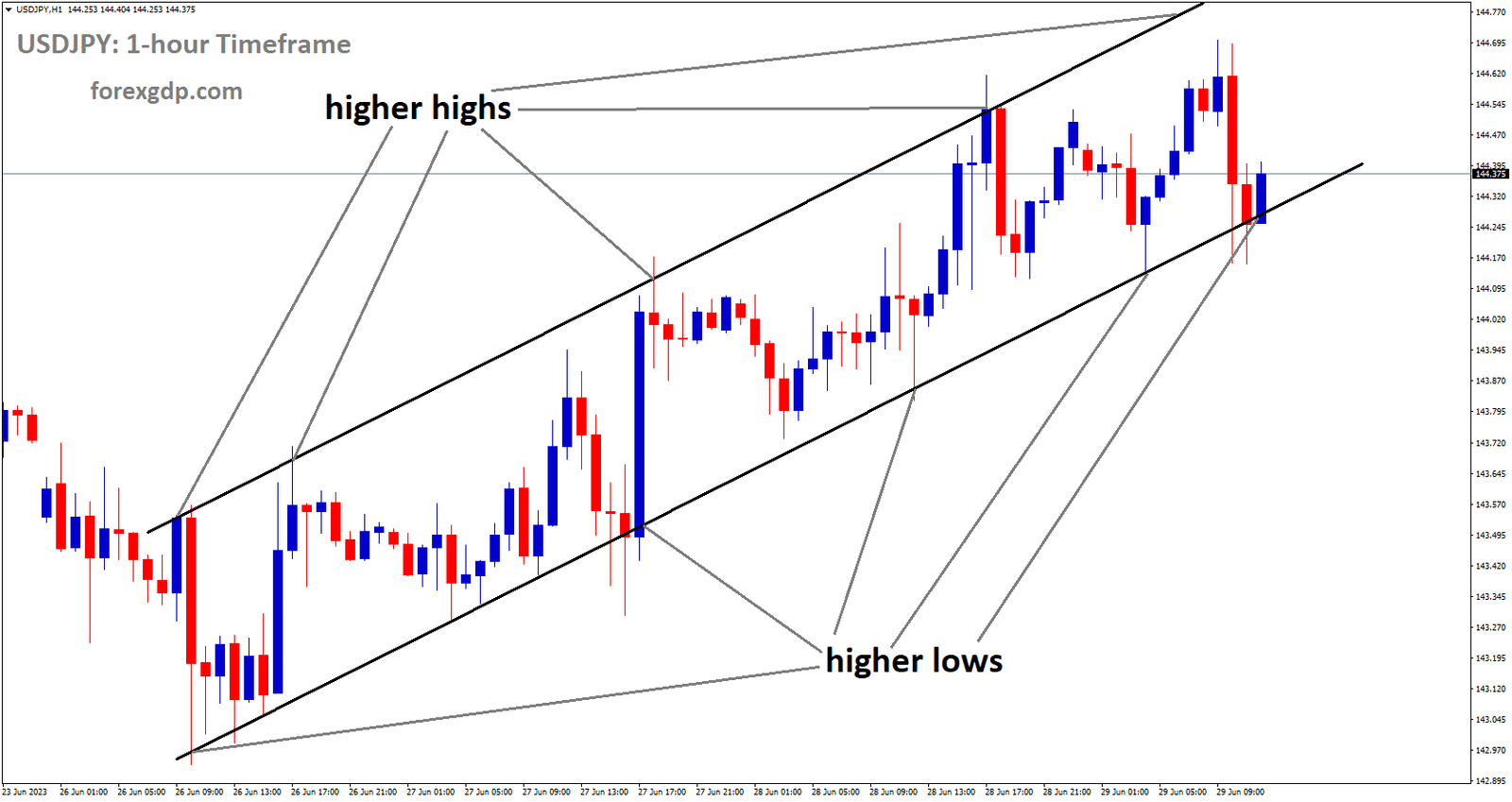

USDJPY Analysis

USDJPY is moving an Ascending channel and the market has reached the higher low area of the channel.

Following the Federal Reserve Chairman’s repetition of the previous day’s remarks on early Thursday morning in Europe, USDJPY exhibits nearly 20 pip of seesaw momentum. However, the Yen pair increased to its highest levels since November 2022 before falling from 144.70, at the latest around 144.60. At the Fourth Conference on Financial Stability, hosted by the Bank of Spain in Madrid, Fed Chair Jerome Powell stated that a significant majority of Fed policymakers anticipate two or more rate hikes by year’s end. Nevertheless, it should be noted that his remarks that “Bank stresses that emerged in March’may well lead’ to a further tightening in credit conditions, seemed to have triggered the USDJPY pair’s retreat from the multi-day top afterward. On the other hand, positive data from Japan also encourage Yen pair buyers. On the other hand, Japan’s Retail Trade growth for May jumps to 5.7% YoY versus 5.4% expected and 5.1% prior, while the country’s Consumer Confidence Index for June matches 36.2 forecasts versus 36.0.

Additionally, the USDJPY bulls appear to be encouraged by worries that the Japanese government will intervene to defend the Yen given that policymakers recently demonstrated their readiness to do so in an emergency. However, dovish remarks from Governor of the Bank of Japan Kazuo Ueda and optimistic US Treasury bond yields give USDJPY buyers hope. The Japanese economy will continue to grow slightly above potential for a while, according to Ueda of the BoJ, but there is still a ways to go before we can sustainably achieve 2% inflation and adequate wage growth. When it comes to yields, the US 10-year and 2-year Treasury bond yields at the latest consolidate the losses from the previous day at 3.48% and 4.75%. Moving forward, traders of the USD/JPY pair will be looking for direction in the second-tier US employment and activity data as well as the revised US Gross Domestic Product for the first quarter of 2023.

GOLD Analysis

XAUUSD is moving in Descending channel and the market has reached the lower high area of the channel.

Following an intraday increase to the $1,912-$1,913 range, the price of gold draws new sellers and drifts into negative territory on Thursday for the fourth straight day. The XAU/USD is currently trading near its lowest level since mid-March, just above the $1,900 round-figure level, as the European session gets underway. The US Dollar strengthens after its sharp increase on Wednesday and reaches a new two-week high, which is perceived as a major factor undermining the price of gold. In remarks made on Wednesday at a conference hosted by the European Central Bank, Federal Reserve Chair Jerome Powell reiterated the likelihood of two rate increases this year and stated that the Fed’s 2% inflation target is not likely to be reached until 2025. This confirms market expectations for a 25 basis point lift-off at the upcoming FOMC policy meeting on July 25–26, which would increase US Treasury bond yields and strengthen the US dollar. In addition, a more pessimistic outlook by other significant central banks encourages flows away from the non-yielding Gold price. In fact, according to Christine Lagarde, president of the European Central Bank (ECB), inflation in the Eurozone has entered a new stage and may persist for some time. Lagarde continued by saying it is unlikely that the central bank will be able to confidently declare that the peak rates have been reached any time soon. Additionally, Bank of England (BoE) Governor Andrew Bailey hinted that rates might stay high for longer than market participants currently anticipate.

The aforementioned fundamental environment appears to be heavily skewed in favour of bearish traders and supports expectations for a further near-term decline in the price of gold. However, for the time being, the safe-haven XAU/USD may receive some support from the worsening global economic outlook and worries about the state of US-China relations. Ahead of Friday’s important releases, which include the official Chinese PMI readings for June and the US Core PCE Price Index, the Fed’s preferred inflation indicator, traders may also refrain from making risky bets and withdraw from the market.

USDCAD Analysis

USDCAD has broken Descending channel in upside.

For the third straight day, the USDCAD pair trades favourably. It is currently trading near the two-week high reached the day before, in the 1.3265–1.3270 range. The hawkish comments made by Federal Reserve Chair Jerome Powell on Wednesday help the US Dollar to be close to its highest level since June 15, which is seen as a major factor supporting the USDCAD pair. At a conference hosted by the European Central Bank, Powell reaffirmed the likelihood of two rate increases this year and left open the prospect of one at the upcoming FOMC policy meeting on July 25–26. Powell added that he does not anticipate inflation reaching the Fed’s target of 2% until 2025. On the other hand, the softer domestic data released on Tuesday, which showed that consumer inflation declined to its slowest pace in two years, undercut the Canadian Dollar (CAD). However, the markets continue to reflect a higher likelihood that the Bank of Canada (BoC) will raise rates by another 25 basis points in July. This, along with a slight increase in Crude Oil prices, supports the commodity-linked Loonie and limits gains for the USD/CAD pair, so it is prudent to exercise caution before positioning for a potential recovery from the YTD low reached on Tuesday.

Therefore, any further upward movement is more likely to run into resistance near the 1.3300–1.3310 strong horizontal support breakpoint. If this level is crossed, a short-covering move may occur, which could push spot prices up to the 200–day Exponential Moving Average. Investors are now focusing on the US economic calendar, which includes the release of the final Q1 GDP reading, the customary Weekly Initial Jobless Claims report, and Pending Home Sales data later in the early North American session. This could give the USDCAD pair some momentum, along with changes in oil prices. On Friday, however, all eyes will be on the US Core PCE Price Index, which is the Fed’s preferred inflation indicator. This will have a significant impact on market expectations regarding the trajectory of future rate hikes by the US central bank, which will in turn fuel USD demand and determine the next leg of the USDCAD pair’s directional move.

USDCHF Analysis

USDCHF is moving an Ascending channel and the market has rebounded from the higher low area of the channel.

On Thursday, the USDCHF pair draws some buyers for the second straight day and rises to the top of its weekly range, getting closer to the psychological level of 0.9000 during the Asian session. In the wake of Federal Reserve Chair Jerome Powell’s hawkish remarks on Wednesday, the US Dollar (USD) extends the previous day’s strong gains and touches a new high since June 15. Powell reaffirmed the likelihood of two rate increases this year while also stating that he does not anticipate inflation reaching the Fed’s 2% target until 2025 in his remarks at an ECB conference. This in turn confirms market expectations for a 25 bps lift-off at the upcoming FOMC policy meeting on July 25–26, supporting the US dollar and providing support for the USDCHF pair. In addition, a generally upbeat atmosphere in the equity markets is thought to be undermining the Swiss Franc (CHF), a safe haven currency, and providing additional support to spot prices. However, concerns about a global economic slowdown and rumours that the US plans to impose more restrictions on semiconductor exports to China keep any optimism in check. Investors appear cautious ahead of the official Chinese PMI readings on Friday, which are predicted to provide more insight into the world’s second-largest economy’s sluggish post-COVID recovery. This prevents bulls from putting down new wagers on the USDCHF pair.

Even from a technical standpoint, it is prudent to exercise caution before setting up for any further appreciating move given the recent repeated failures to find acceptance above the 50-day Simple Moving Average (SMA). Currently, market participants are focusing on the US economic calendar, which includes the release of the final Q1 GDP print, the Weekly Initial Jobless Claims report, and the Pending Home Sales data, all of which are scheduled for release later during the early North American session. This could have an impact on the USD price dynamics, which, along with the general risk sentiment, give the USD/CAD pair new life and create opportunities for short-term trading.

EURJPY Analysis

EURJPY is moving an Descending channel and the market has fallen from the lower high area of the channel.

On Thursday, the EURJPY cross reverses an intraday decline to the 157.25-157.20 range and moves back towards the high point it reached the day before in September 2008. However, during the early part of the European session, spot prices decline a few pip and remain below the 158.00 level, despite the fact that the fundamental landscape appears to be heavily in favour of bullish traders. Despite concerns about intervention, the Bank of Japan’s more dovish stance has resulted in the Japanese Yen (JPY) continuing its relative underperformance, which ends up being a major factor supporting the EURJPY cross. It is important to remember that the Japanese Finance Minister, Shunichi Suzuki, stated earlier this week that the country would closely monitor the foreign exchange market and would take appropriate action if the currency movements became out of control. Masato Kanda, Japan’s top currency diplomat, reiterated the warning, but it has failed to spur any significant buying around the JPY because investors are confident that the BoJ’s negative interest-rate policy will continue at least through next year.

Furthermore, BoJ Governor Kazuo Ueda recently ruled out the possibility of any modification to the ultra-loose policy framework and hinted that no immediate plans to change the yield curve control measures are being made. In contrast, Christine Lagarde, president of the European Central Bank, confirmed market expectations for a ninth consecutive liftoff in July. Inflation in the Eurozone is too high and is expected to stay that way for too long, Lagarde said in a speech at the Sintra central banking conference in Portugal. This increased expectations for additional rate increases from the ECB this year, which is seen as supporting expectations for a further near-term strengthening movement for the EURJPY cross and acting as a tailwind for the common currency. However, given that the Relative Strength Index (RSI) on the daily chart is still in the overbought region, it would be wise to hold off on adding any new bullish bets until there has been some consolidation in the near term or a slight decline. However, the aforementioned fundamental backdrop suggests that the EUR JPY cross’s direction of least resistance is upward. Because of this, any significant corrective decline may still be viewed as a buying opportunity by bulls and is more likely to be brief.

EURCHF Analysis

EURCHF is moving an Ascending channel and the market has fallen from the higher high area of the channel.

For the SNB in its battle against inflation, the value of the Franc remains crucial. Commerzbank economists evaluate the outlook for the CHF. The recent easing of price pressures in Switzerland is notable. The SNB is still worried about the consequences of the second round, though. As a result, it is likely to continue to be hawkish and support a strong Franc. However, it is likely to accept a slightly weaker CHF if price pressures continue to ease throughout the year. Additionally, the ECB is expected to maintain its hawkish stance, which should support the EUR. In light of this, we see potential for the Franc to lose some ground to the EUR throughout the year.

GBPUSD Analysis

GBPUSD is moving in Descending channel and the market has reached the lower low area of the channel.

Going into Thursday’s London opening, the GBPUSD pair drills the 15-day low at around 1.2620. As a result, the Cable pair traders react less strongly to remarks made by Federal Reserve Chairman Jerome Powell than by Bank of England Governor Andrew Bailey. The relative stronger economic conditions in the UK than in the US may be the cause of the preference for Fed Chair Powell’s speech as the key catalyst. The positive results of the US Banking Stress Test also highlight the resilience of the US Dollar. Despite this, Bank of England Governor Andrew Bailey demonstrated a willingness to take whatever steps were required to bring inflation to the desired level. Data “showed clear signs of persistence of inflation,” the policymaker added, “suggesting further rate hikes from the Old Lady,” as the BoE is known colloquially. However, Jerome Powell, the chairman of the Federal Reserve, stated, “We believe there will be more restriction coming, driven by the labour market.” The policymaker disregarded the recession as the most likely scenario.

According to Reuters, the Fed’s stress test exercise revealed that lenders like JPMorgan Chase, Bank of America, Citigroup, Wells Fargo, Morgan Stanley, and Goldman Sachs have sufficient capital to withstand a severe economic downturn. This opens the door for them to offer dividends and share buybacks. As US Treasury Secretary Janet Yellen ‘hopes’ to visit China to re-establish contacts but also demonstrated readiness to take actions to protect national security interests even at economic cost, it should be noted that mixed headlines about US-China ties add strength to the US Dollar and weigh on the USD Dollar by challenging sentiment. S&P500 Futures are lagging behind these plays despite rising over the previous two days. Additionally, the US 10-year and 2-year Treasury bond yields consolidate the losses from the previous day at the latest around 3.48% and 4.75%. Looking ahead, it will be crucial to keep an eye on Fed Chair Powell’s speech, the updated US Gross Domestic Product (GDP) for the first quarter (Q1) 2023, as well as the secondary US employment and activity data, for clear indications.

AUDUSD Analysis

AUDUSD is moving in Descending channel and the market has rebounded from the lower low area of the channel.

AUDUSD pares the largest daily loss since early March. In doing so, the Australian currency pair eases from the daily peaks while reversing gains associated with the Australia Retail Sales data, but it continues to be mildly bid at press time. It is important to remember that the Australian Monthly Consumer Price Index (CPI), which disappointed the Reserve Bank of Australia (RBA) hawks the day before, unexpectedly increased by 0.7% MoM for May, giving the bears some breathing room. However, concerns over Fed Chair Jerome Powell’s hawkish remarks appear to be weighing on the AUD/USD exchange rate.

AUDJPY Analysis

AUDJPY is moving in Descending channel and the market has rebounded from lower low area of the channel.

During the mid-Asian session on Thursday, AUDJPY refreshed intraday high near 95.60 and supported positive Australia Retail Sales figures. In doing so, the cross-currency pair disregards positive Japan Retail Trade data in the midst of firmer yields and cautious market optimism. According to the most recent economic update from the Australian Bureau of Statistics (ABS), Australia’s seasonally adjusted Retail Sales increased 0.7% monthly in May as opposed to the 0.1% expected and 0.0% seen in April. Reuters reported that sales of A$35.52 billion $23.52 billion were up 4.2% from a year earlier, matching April’s growth but being far from the 19% post-lockdown boom levels seen in the middle of last year. The positive Australian Retail Sales helped to stabilise the AUD/JPY pair’s heavy losses from the previous day, which were caused by the underwhelming inflation data from Australia. Australia’s Monthly Consumer Price Index for May decreased to 5.6% YoY on Wednesday, down from the 6.1% forecast and 6.8% recorded the previous day. The Reserve Bank of Australia paused rate increases following two consecutive hawkish surprises, which in turn drowned the Australian Dollar. Concerns about this increased.

In contrast, Japan’s retail trade growth increased to 5.7% YoY in May, up from the expected 5.4% and previously reported 5.1%. Seasonally adjusted data also reversed the previous contraction of 1.2% with a gain of 1.3% in the key statistics for the same month, beating market expectations by a factor of -0.2%. In addition to the Australian data, the AUDJPY pair prices also appeared to have been boosted by Bank of Japan Governor Kazuo Ueda’s defence of the easy-money policy. When defending the dovish slant of the Japanese central bank’s policymakers, Bank of Japan Governor Kazuo Ueda said, “There is still some way to go in sustainably achieving 2% inflation accompanied by sufficient wage growth.” BoJ Governor Ueda further stated that the Japanese economy will continue to grow a little faster than expected for a while. It is important to note that the market sentiment has recently seemed to be favoured by US Treasury Secretary Janet Yellen’s ‘hopes’ of visiting China to re-establish contacts. The central bankers also did not say anything new, giving traders the opportunity to build on yesterday’s movements and advance the AUDJPY pair. While S&P500 Futures post modest gains by press time, US Treasury bond yields recover in the midst of these plays. Future movements in the AUD/JPY will be influenced by Japan’s Consumer Confidence for June, which is predicted to be 36.2 instead of 36.0, but major focus will be placed on yields and risk catalysts for a clear guide.

NZDUSD Analysis

NZDUSD has broken in Descending channel in downside.

The NZDUSD pair rises a few points from a low reached during the Asian session on Thursday that was nearly three weeks old and now trades just below the 0.6100 round-figure level. However, the fundamental environment is still favourable to bearish traders, so it is prudent to exercise caution before making any significant upside positions. Because the Reserve Bank of New Zealand and the Federal Reserve have different views on the direction of monetary policy, the New Zealand Dollar has had one of the worst performances among the G10 currencies over the past 24 hours. It is important to note that the RBNZ signalled in May that its most aggressive rate-hiking cycle since 1999 was over after raising rates by 25 basis points to 5.5%, the highest level in more than 14 years. Rates are expected to peak at their current level, according to the RBNZ, before rate cuts start in the third quarter of 2019.

In contrast, the Fed warned earlier this month that by the end of this year, borrowing costs may still need to increase by as much as 50 basis points. Fed Chair Jerome Powell reiterated on Wednesday that two rate increases this year are likely, which strengthened the outlook. Powell said that he does not anticipate inflation reaching the Fed’s 2% target until 2025 while refusing to rule out the possibility of a rate hike at the upcoming FOMC policy meeting on 25–26 July. The US Dollar is thus still supported by this. Concerns about the deterioration of relations between the two largest economies in the world are further fueled by reports that the US is considering new restrictions on the export of artificial intelligence chips to China. The NZDUSD pair may be restrained by this as well as other factors that weigh on antipodean currencies, including the Kiwi. For a new impetus later in the North American session, market participants are now looking to the US economic docket, which includes the final Q1 GDP print, the Weekly Initial Jobless Claims, and Pending Home Sales.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/