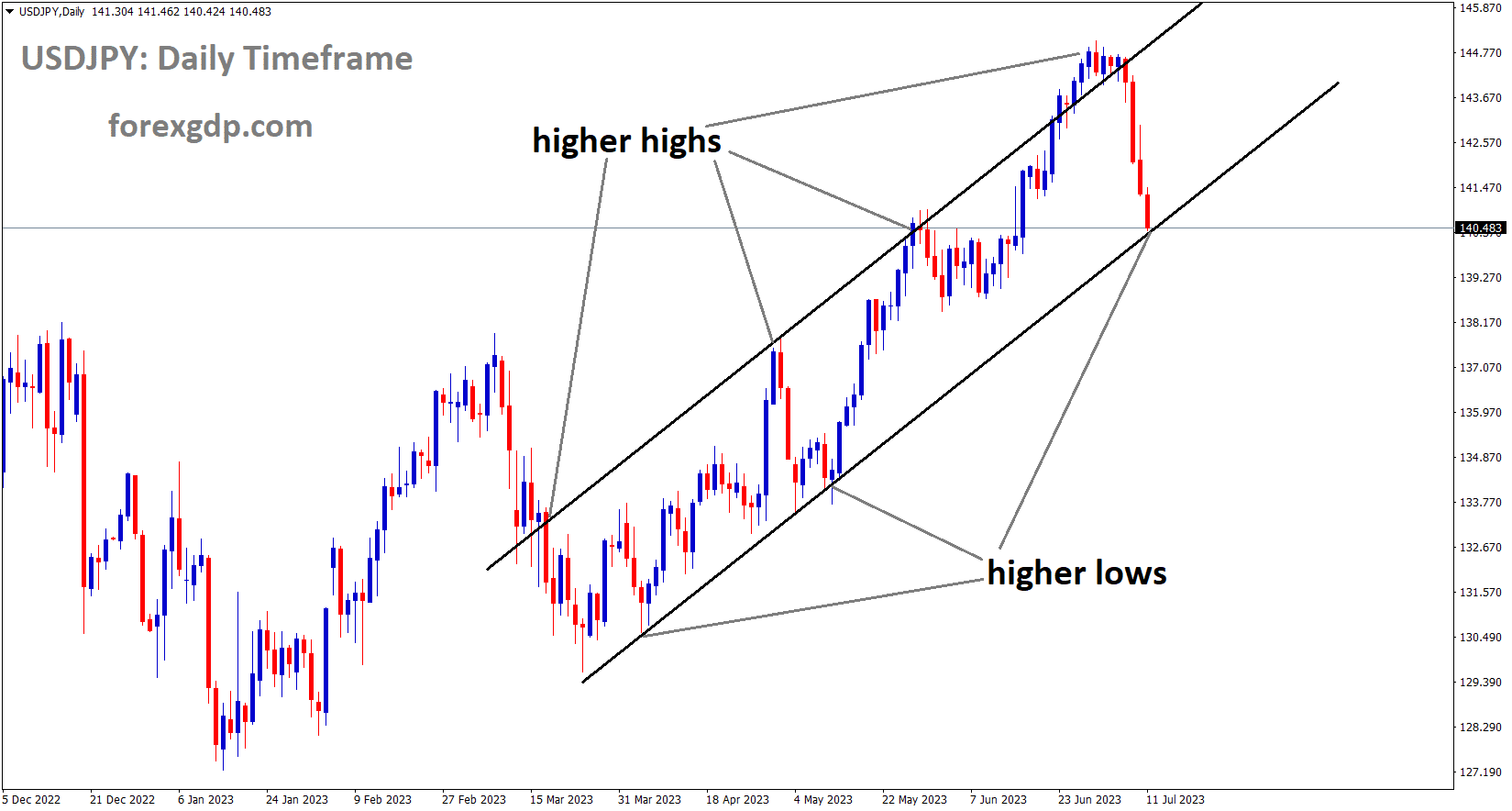

USDJPY Analysis

USDJPY is moving in an Ascending channel and the market has reached the higher low area of the channel.

Particularly when compared to the US Dollar, the Japanese Yen performed better than its major rivals. The USDJPY exchange rate dropped by about 1.9% over the last two days, which was its worst performance since May. Beyond that, the move was a fairly uncommon occurrence. Using data going back to the start of 2000, the 1.9% decline amounted to -2.2 standard deviations from the mean. A closer examination of the price movement of the Yen over the previous day reveals that the strengthening of the currency was accompanied by a decline in the yields on longer-term US government bonds. The 10-year Treasury yield experienced its worst performance since June 20th, falling nearly -1.8%. This was in spite of numerous instances of Fedspeak in which decision-makers reaffirmed that higher interest rates are likely to continue for some time to come.

GOLD Analysis

XAUUSD Gold Price is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

After a sluggish start to the week, Gold Price XAU/USD picks up bids to renew intraday high around $1,928, during the mid-Asian session on Tuesday. It is important to note that the main driver of the XAU/USD price appears to be the US Dollar’s general weakness, which is caused by unfavourable US employment and inflation concerns. The precious metal ignores the looming economic concerns coming from China as well as the hawkish Federal Reserve Fed speech in doing so. Following a lacklustre day, the Gold Price picks up steam to the upside as the US Dollar Index DXY snaps a four-day losing streak and falls to its lowest point in two months near 101.90.

However, after the dismal US employment data, pessimistic US inflation expectations weigh on the US Dollar and drive up the XAU/USD Price. According to the Federal Reserve Bank of New York’s monthly Survey of Consumer Expectations, the US public’s expectation for inflation over the next year fell from 4.1% in May to 3.8% in June, which is the lowest level since April 2021. It is important to note that the depressing inflation signals increase hopes for a softer US Consumer Price Index CPI, which is due on Wednesday. This raises doubts about the Federal Reserve’s Fed most recent hawkish remarks and boosts the price of gold. According to Mary Daly, president of the San Francisco Federal Reserve, we are likely to need a couple more rate hikes over the course of this year to really bring inflation sustainably back to the Fed’s 2% goal. According to Cleveland Fed President Loretta Mester, the Fed will need to tighten monetary policy somewhat further to reduce inflation. Michael Barr, the vice chair for supervision at the Federal Reserve, added, We are quite attentive to bringing inflation down to target.

SILVER Analysis

XAGUSD Silver price is moving in the Descending channel and the market has reached the lower high area of the channel.

On the other hand, the most recent US employment report for June was unexpectedly unfavourable and dealt the US Dollar a severe blow, resulting in the biggest daily loss in three weeks. However, the disappointing inflation data from China published on Monday raised concerns about deflation in the largest industrialised nation, allowing the US Dollar to lick its wounds and restrain the demand for gold. However, the headline US Nonfarm Payrolls NFP fell to 209K, versus 225K market forecasts and 309K prior revised, marking the first below-expectations print in 15 months. Meanwhile, the unemployment rate was in line with analysts’ expectations at 3.6%, down from 3.7% previously. The Producer Price Index PPI decreased below the -4.6% yearly prior marked in May to -5.4%, while China’s Consumer Price Index CPI eased to 0.0% YoY in June from 0.2% prior.

The rising US-China tension is also affecting other markets and nudges the XAU/USD bulls. US Treasury Secretary Janet Yellen claimed that the discussions were direct and productive following her four-day trip to China, stabilising the tumultuous US-Sino relationship. The decision-maker did, however, add, The U.S. and China have significant disagreements. However, in response to China’s major concerns regarding the US economic sanctions and crackdown, the US was urged to take concrete action, according to a statement released by the Chinese Finance Ministry on Monday. Beijing’s concerns pique the interest of the XAU/USD bulls given that the dragon nation is one of the largest consumers of gold.

It should be noted that the low US Treasury bond yields, along with the markets’ cautious optimism, drive up the price of gold. S&P500 Futures show a positive Wall Street performance while portraying the mood, and US Treasury bond yields are under pressure. However, the benchmark US 10-year Treasury bond yields posted their first daily loss in July the day before, and their two-year counterpart experienced a second straight day of declines, falling to respective levels of close to 4.00% and 4.86%. Moving on, gold traders should pay attention to the risk catalysts mentioned above for guidance ahead of Wednesday’s release of the June Consumer Price Index CPI for the United States.

USD Index Analysis

USD index is moving in the Descending channel and the market has reached the lower low area of the channel.

After falling for three straight days, the US Dollar Index DXY is still in the red at its lowest levels in three weeks as bears push against the 101.90 support during Tuesday’s Asian trading session. Thus, despite hawkish remarks from Federal Reserve Fed officials, Friday’s dismal US employment data and the weaker US Treasury bond yields weigh heavily on the greenback’s gauge against the six major currencies. The risk-on attitude even as China flags economic concerns is another factor putting downward pressure on the DXY. In a recent statement, San Francisco Fed President Mary Daly said, We are likely to need a couple more rate hikes over the course of this year to really bring inflation sustainably back to the Fed’s 2% goal. In a similar vein, Cleveland Fed President Loretta Mester said that the Fed will need to tighten the monetary policy somewhat further to lower inflation. The hawkish remarks from the Fed officials fail to entice the US Dollar Index buyers amid Friday’s depressing US jobs report and the recently softer US inflation expectations, adding that We are quite attentive to bringing inflation down to target.

According to the Federal Reserve Bank of New York’s monthly Survey of Consumer Expectations, the US public’s expectation for inflation over the next year fell from 4.1% in May to 3.8% in June, which is the lowest level since April 2021. On the other hand, the most recent US employment report for June was unexpectedly unfavourable and dealt the US Dollar a severe blow, resulting in the biggest daily loss in three weeks. However, Monday’s disappointing inflation data from China raised concerns about deflation in the largest industrialised nation, allowing the US Dollar to lick its wounds. However, the headline US Nonfarm Payrolls NFP fell to 209K, versus 225K market forecasts and 309K prior revised, marking the first below-expectations print in 15 months. Meanwhile, the unemployment rate was in line with analysts’ expectations at 3.6%, down from 3.7% previously. The Producer Price Index PPI decreased below the -4.6% yearly prior marked in May to -5.4%, while China’s Consumer Price Index CPI eased to 0.0% YoY in June from 0.2% prior.

Austan Goolsbee, president of the Federal Reserve Bank of Chicago, stated that concerns about inflation do not require a recession in response to the depressing US jobs report. Amid these manoeuvres, Wall Street closed in the green while US Treasury bond yields decreased. The policymaker also stated, It is clear the job market is strong but cooling. However, the benchmark US 10-year Treasury bond yields posted their first daily loss in July the day before, while the two-year counterpart saw a decrease for a second straight day, to near 4.00% and 4.86%, respectively. Looking ahead, DXY traders will focus on the risk catalysts ahead of Wednesday’s US inflation data for clear indications.

According to San Francisco Fed President Mary Daly, in order to truly bring inflation sustainably back to the Fed’s 2% goal this year, we are likely to need a couple more rate hikes over the course of this year. The US economy’s momentum is still surprising. We still need to do more to raise rates in light of that momentum. We must also balance potential risks. The risks are now more evenly distributed. The risks of doing too little outweigh the risks of doing too much because the labour market is still strong and inflation is high. It makes sense to gradually increase interest rates. We must exercise resolve and consideration. The lags are longer than we anticipated. It is too soon to declare success in achieving supply and demand parity. Depending on the data, we might decide to raise rates less frequently or more frequently than twice this year. One thing the previous cycle taught us is that the Fed could raise rates even if its balance sheet was still growing. It is likely that the credit tightening caused by the March banking stresses is less than the quarter-point to 50 bps rate hike I had anticipated.

EURAUD Analysis

EURAUD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

The Westpac Consumer Confidence Index for Australia rose 2.7% in July, exceeding analysts’ expectations by 0.2%, while the National Australia Bank’s (NAB) monthly business sentiment figures also showed encouraging results for June. In spite of this, the NAB’s business conditions score increases to 9 from 8 and its business confidence score increases to 0.0% from -4.0 previously. The latest US inflation expectations have raised concerns about deflation, especially in light of the day before disappointing China Consumer Price Index (CPI) and Producer Price Index (PPI) data. However, Australian sentiment data continue to give buyers reason for optimism. Nevertheless, according to the Federal Reserve Bank of New York’s monthly Survey of Consumer Expectations, the one-year inflation expectation for US consumers fell to its lowest level since April 2021 in June, falling from 4.1% in May to 3.8%.

EURCHF Analysis

EURCHF is moving in the Descending channel and the market has fallen from the lower high area of the channel.

We are approaching the peak of interest rates, according to European Central Bank ECB Governing Council member Francois Villeroy de Galhau on Tuesday. A savings account’s livret rate needs to be balanced. We are beginning to receive positive inflation news. By 2025, inflation will have returned to its pre-crisis level of 2%. Next year, inflation should be 2.5% on average. We must remain at this level for a while after we reach the peak. predicts 0.7% growth in France in 2023. France lacks the resources to lower taxes again. In ten years, France could reduce its debt-to-GDP ratio to below 100% if it could control its spending.

EURGBP Analysis

EURGBP is moving in the Descending channel and the market has reached the lower high area of the channel.

Following the release of numerous UK and EU data early on Tuesday, the EURGBP reverses from its intraday high and re-tests the daily low near 0.8550. While the ILO Unemployment Rate increased to 4.0% for the three months to May, contrary to market expectations for no change from the 3.8% prior figure, the UK Claimant Count Change increased by 25.7K for June versus -22.5K prior revised. The final readings of inflation in Germany for June according to the Consumer Price Index CPI and the Harmonised Index of Consumer Prices HICP measures are also in line with the initial projections of 6.4% and 6.8% YoY figures. In addition to the data, the cross-currency pair is affected by hawkish remarks from British policymakers, mixed central bank talks, and data from the Eurozone, particularly after the stronger British employment numbers. On Monday, Bank of England BoE Governor Andrew Bailey and UK Finance Minister Jeremy Hunt expressed their willingness to take action to bring inflation back to its 2% target. It is important to note that BoE Governor Bailey made an effort to defend the stringent monetary policy while downplaying worries about the UK’s economic slowdown.

On the other hand, from -17 in June, the Eurozone Sentix Investor Confidence fell to -22.5 in July. Manfred Huebner, managing director of Sentix, added to the negativity by saying, There is also nothing positive to report in terms of forward-looking expectations. The Investor Confidence Index for Germany dropped 7.3 points to -28.4, according to Sentix’s Huebner. According to Governing Council member Francois Villeroy de Galhau, when referring to the ECB discussions, Eurozone rates will soon reach their high point, but it will be more of a high plateau than a peak. In a similar vein, Mario Centeno, governor of the Bank of Portugal and member of the Governing Council, stated that inflation is decreasing more quickly than it is rising. The policymaker further stated that they must support this effort and have complete faith in our ability to succeed. Taking into account that the Euro EUR enjoys comparatively greater market credence than the Pound Sterling GBP, it should be noted that the cautious market sentiment also supported the EURGBP prices. The central bankers’ remarks and Germany’s July ZEW sentiment survey will be scrutinised for any clear indications of direction.

GBPJPY Analysis

GBPJPY is moving in an Ascending channel and the market has reached the higher low area of the channel.

Maybe traders were setting up for the US inflation report this week. Wednesday is expected to see a further slowdown in headline inflation from 3.1% y/y in June to 4.0% y/y in May. However, the disinflation in food and energy prices is largely to blame for this. The core reading, which is much less volatile, is seen edging down to 5.0% y/y from 5.3% previously. This is bad news for the Federal Reserve because it suggests that underlying inflation is solidifying and becoming more difficult to manage. Investors might be anticipating a softer print and a Fed that is less hawkish. As a result of the Bank of Japan’s stagnation, the Japanese Yen would benefit because its fundamentals are dependent on outside factors. Because of this, the USD/JPY is very responsive to Treasury yields.

NZDUSD Analysis

NZDUSD is moving in the Box pattern and the market has fallen from the resistance area of the pattern.

Before the Reserve Bank of New Zealand (RBNZ) announces its interest rate decision on Wednesday, the New Zealand dollar is demonstrating signs of establishing a base against some of its peers. The RBNZ signalled in May that NZ interest rates have peaked, so it is widely expected to maintain its benchmark official cash rate at the 14-year high. Since the second quarter of 2023, NZ’s growth prospects have significantly worsened as a result of the economy being negatively impacted by the massive 525 basis point increase in interest rates.

The bias for rates remains up, though, if RBNZ continues the renewed hawkishness of global central banks in recent months, given that inflation is significantly above the NZ central bank’s target range. Given the neutral speculative positioning of the NZD, this could strengthen the underperforming New Zealand dollar. The US CPI data that is due this week is also a major concern. If price pressures ease more than anticipated, the USD may lose prominence globally. The CME FedWatch tool, however, indicates that the rate futures market currently predicts a 95% chance of a 25-basis-point increase by the US Federal Reserve at its meeting later this month.

AUDCAD Analysis

AUDCAD is moving in an Ascending channel and the market has reached the higher low area of the channel.

On Wednesday, the Bank of Canada will reveal its July monetary policy decision. In an effort to continue combating persistently high price pressures, markets anticipate the central bank to increase borrowing costs by 25 basis points to 5.0%, the highest level since 2001. Following a brief break earlier in the year, the move, if confirmed, would represent the second consecutive quarter-point increase. Traders should pay more attention to forward guidance and general comments about economic prospects rather than just the rate decision itself. The institution led by Tiff Macklem may be inclined to leave the door open to additional tightening in the upcoming months given that the Canadian economy is performing better than expected, labour markets are resilient, and core inflation is struggling to decline. Following the July meeting, a small probability of another 25 bp hike is indicated by market pricing. If the bank continues to signal that the economy is still experiencing excess demand and that its stance is insufficiently restrictive to bring about price stability, the odds of this event could increase and consolidate. However, the Canadian dollar is likely to benefit from a hawkish outlook.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/