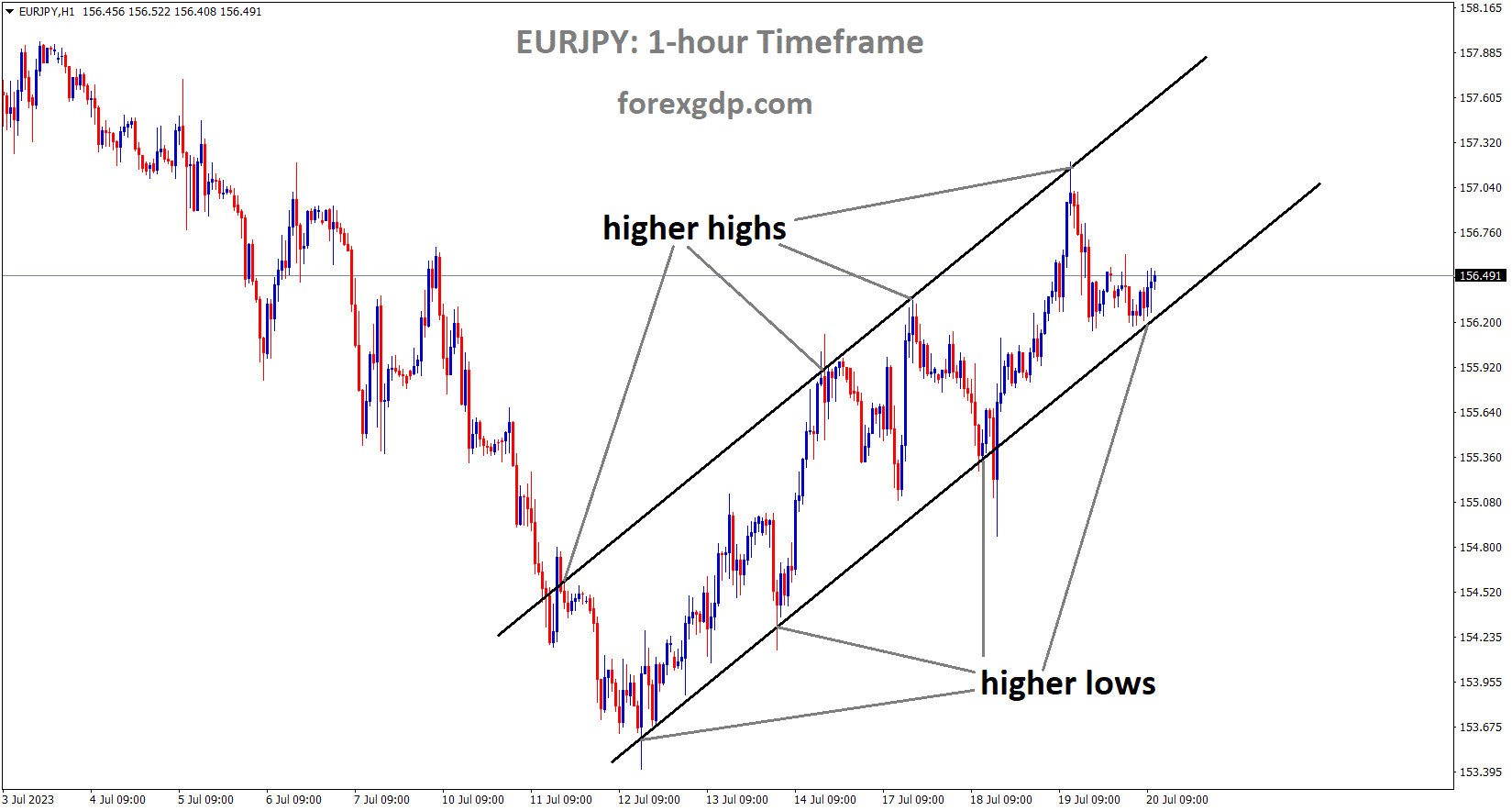

EURJPY Analysis

EURJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

Less enthusiasm for the yen against other currencies was generated by Japan’s June trade balance figures, which were higher than anticipated. Tokyo’s decision-makers predicted that growth in FY2023–2024 will be 1.3% rather than the 1.5% initially anticipated. Fumio Kishida, the prime minister of Japan, declared that the Dovish policy would continue until wages returned to normal.

The Yen pair explains recently negative macros and news about Japan while failing to support the US Dollar’s decline during the day’s slow trading. Despite this, the Japanese government recently disclosed a downward revision to its growth projections for the Asian giant’s Financial Year FY 2023–24. By doing this, Tokyo’s policymakers expect the FY 2023–24 growth to be 1.3% rather than the earlier predicted 1.5%.

On the other hand, Japan’s trade data for June showed a positive merchandise trade balance total amid negative import and positive export numbers. In other places, Japan’s Prime Minister PM Fumio Kishida supports the dovish concerns about the Bank of Japan BoJ by demonstrating his willingness to foster an environment in which wage increases are accepted as the norm.

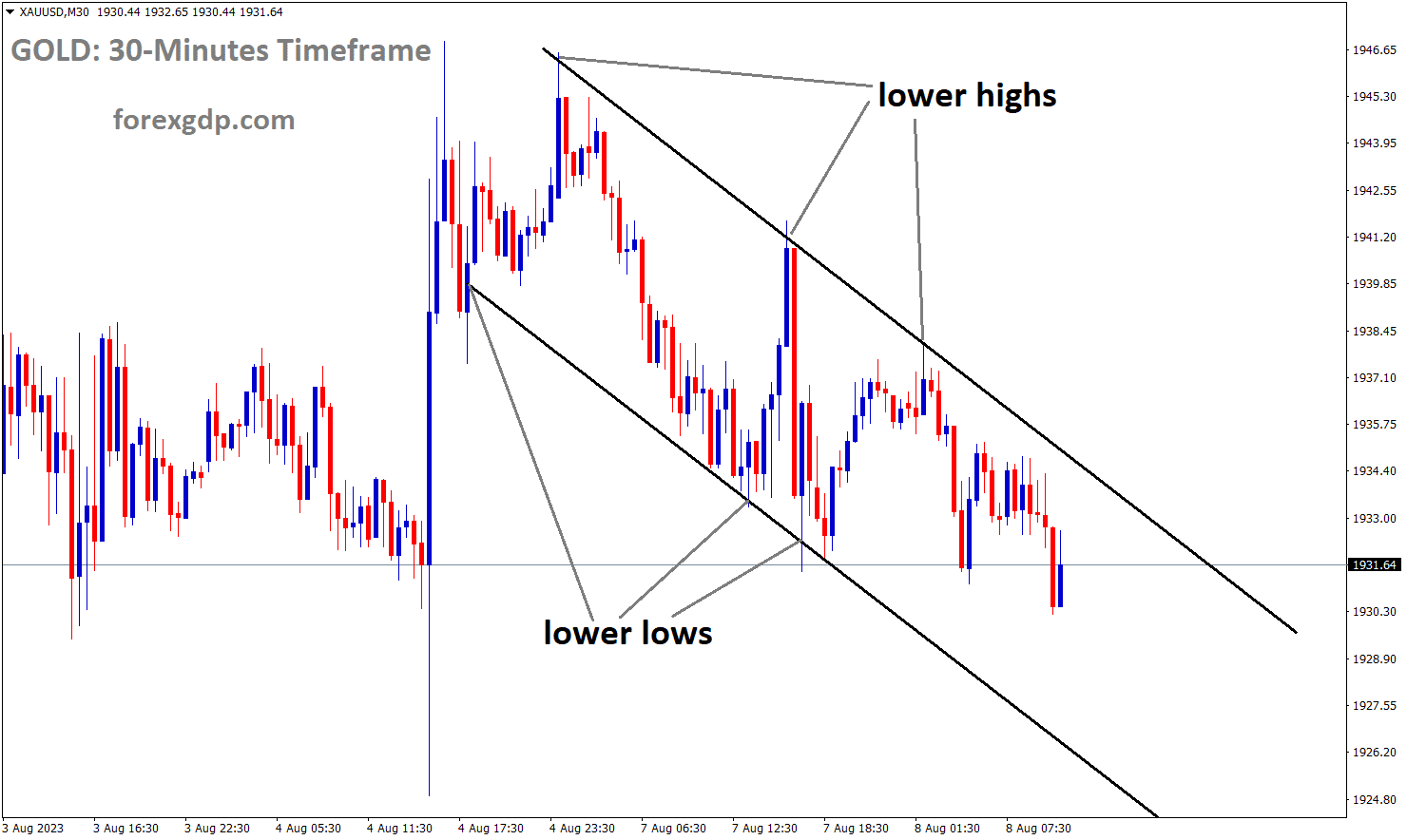

GOLD Analysis

XAUUSD Gold price is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

XAUUSD Gold price is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

Due to central banks’ pause in raising rates after inflation rates started to decline in major nations like Australia, the UK, the Eurozone, the Swiss region, the US, and Canada, gold prices have increased. Non-Yielding Assets enjoy the benefits of concerns about paused rate hikes. Tensions between the US and China are a result of the US restricting China’s imports of AI chips. Russia threatened to launch an attack if any ships carrying military cargo passed through Black Sea ports on their way to Ukraine.

Following a brief pause the day before, the price of gold picks up steam once more and reaches a new two-month high on Thursday during the Asian session. As of right now, the XAUUSD is trading in the $1,984–$1,985 range and appears ready to continue its recent steady upward trajectory seen over the past three weeks or so. The US Dollar USD struggles to take advantage of its recent rise from its lowest point since April 2022 and continues to fall from a one-week high reached on Wednesday. This is then seen as providing some support to the price of gold expressed in US Dollars. In the wake of a further easing of inflationary pressures, the markets began pricing out the possibility of any additional interest rate increases by the Federal Reserve Fed, following the anticipated 25 basis points bps lift-off in July. Investors now appear to believe that the Fed’s current policy tightening, which was a major cause of a sharp decline in US Treasury bond yields and is still acting as a drag on the greenback, is about to come to an end.

SILVER Analysis

XAGUSD Silver price is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

In addition, worries about a global economic slowdown, deteriorating US-China relations, and geopolitical tensions support the price of safe-haven gold. On Wednesday, China’s ambassador to Washington stated that China does not desire a trade or technology war but will retaliate if the US places additional restrictions on imports of machinery used to produce advanced chips. Additionally, the Russian defence ministry announced that starting on Thursday, any ships sailing towards the Black Sea ports of Ukraine would be treated as potential carriers of military cargo and participants in the conflict. As a result, the recent uptick in optimism in the equity markets is contained, and some haven-seeking flows are directed towards the precious metal.In addition, the non-yielding Gold price appears to benefit from expectations that the European Central Bank ECB will declare victory over inflation and halt its rate-hiking cycle. In fact, a large number of ECB Governing Council members this week heightened uncertainty about further rate hikes after the July meeting and reaffirmed the idea that inflation may decline more quickly than anticipated. Moreover, for the first time since March 2021, Canadian inflation declined to levels that are within the Bank of Canada’s BoC acceptable range. This in turn suggests that the XAUUSD will continue to move upward along the path of least resistance, though bulls may hold off on placing new bets until there has been some follow-through buying above the weekly high.

USDCHF Analysis

USDCHF is moving in the Box pattern and the market has rebounded from the horizontal support area of the pattern.

Swiss trade balance for the month of June increased to 4823M from the anticipated 4031M, but it is still lower than the previous print of 5442M. In the month of May, imports increased to 20093M from 18438M and exports increased to 24917M from 23879M. After the readings were printed, the Swiss Franc appreciated against Counter pairs.

Bears in the USDCHF pair maintain control at the lowest levels seen since January 2015, falling for a second straight day while reversing the corrective bounce from the day before. By doing so, the Swiss Franc CHF pair explains the contrast between the weak US dollar and the stronger Swiss trade numbers at around 0.8560 during Thursday’s early European session. Despite being less than the previous balance of 5,442M, the Swiss Trade Balance increased to 4,823M versus the expected 4,031M. According to information, exports increased to 24,917 million from 23,879 million in previous readings, while imports also increased, to 20,093 million from 18,438 million in May. In addition to the generally positive June figures for Swiss foreign trade, widespread US Dollar weakness also permits the USDCHF bears to maintain control. Despite this, the US Dollar Index DXY declines 0.25 percent intraday to test the round number 100.00 and ends a two-day recovery from its lowest point since April 2022. In doing so, the dollar ignores the optimism at US banks and rationalises the negative US housing data from the day before along with mixed Fed concerns.

EURUSD Analysis

EURUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel.

An additional 25 basis point rate increase is not anticipated following the July meeting, according to ECB Governing Council member Yannis Stournaras, because doing so would harm the economy because inflation has slowed down more than anticipated.

While losing the momentum from the previous day’s recovery from the weekly low in the early hours of Thursday’s Asian session, EUR/USD is still down around 1.1200. This helps to explain recent scepticism about the European Central Bank’s ECB hawkish moves amid inflation concerns as well as the strength of the US Dollar. It also keeps the bears in the game following a two-day downtrend from the 17-month high. Yannis Stournaras, a member of the Governing Council, said on Wednesday that he was not sure whether the ECB would hike rates again after a 25 bps increase next week, despite the fact that the final readings of Eurozone Core inflation, as measured by the Core Harmonised Index of Consumer Prices HICP, improved for June on a monthly basis to 0.4% MoM from the 0.3% previous forecasts. The policymaker added that further increases in interest rates could hurt the economy while also arguing that inflation is declining. It is important to note that despite disappointing US housing data, the US Dollar Index DXY increased on the last two days in a row, refreshing the weekly high to about 100.55, close to 100.30 by press time. The market’s worries that the US Federal Reserve Fed might maintain higher interest rates after raising them in July may be the cause.

On Wednesday, US building permits for June decreased 3.7% from a previously reported increase of 5.6%, while housing starts also declined, this time by 8.0% from a previously reported increase of 15.7%. Instead, the slower-than-expected growth in US retail sales for June contrasted with encouraging data to support the Federal Reserve’s decision to keep interest rates higher for longer and support the announcement of a 0.25% rate hike in July. On Tuesday, this same factor led to the US Dollar’s corrective bounce off its 15-month low, and on Wednesday, it helped defend the recovery in the face of dismal US housing data.

In other places, expectations of stronger earnings from US banks, both top-tier and regional, as a result of higher rates combine with conflicting worries about US-China relations to push Wall Street higher and pressurise US Treasury bond yields at the same time. Next, to decorate the economic calendar, the preliminary readings for July’s Consumer Confidence in the Eurozone will be released before the US Initial Jobless Claims and Existing Home Sales. For clear directions, the risk catalysts should receive the majority of attention.

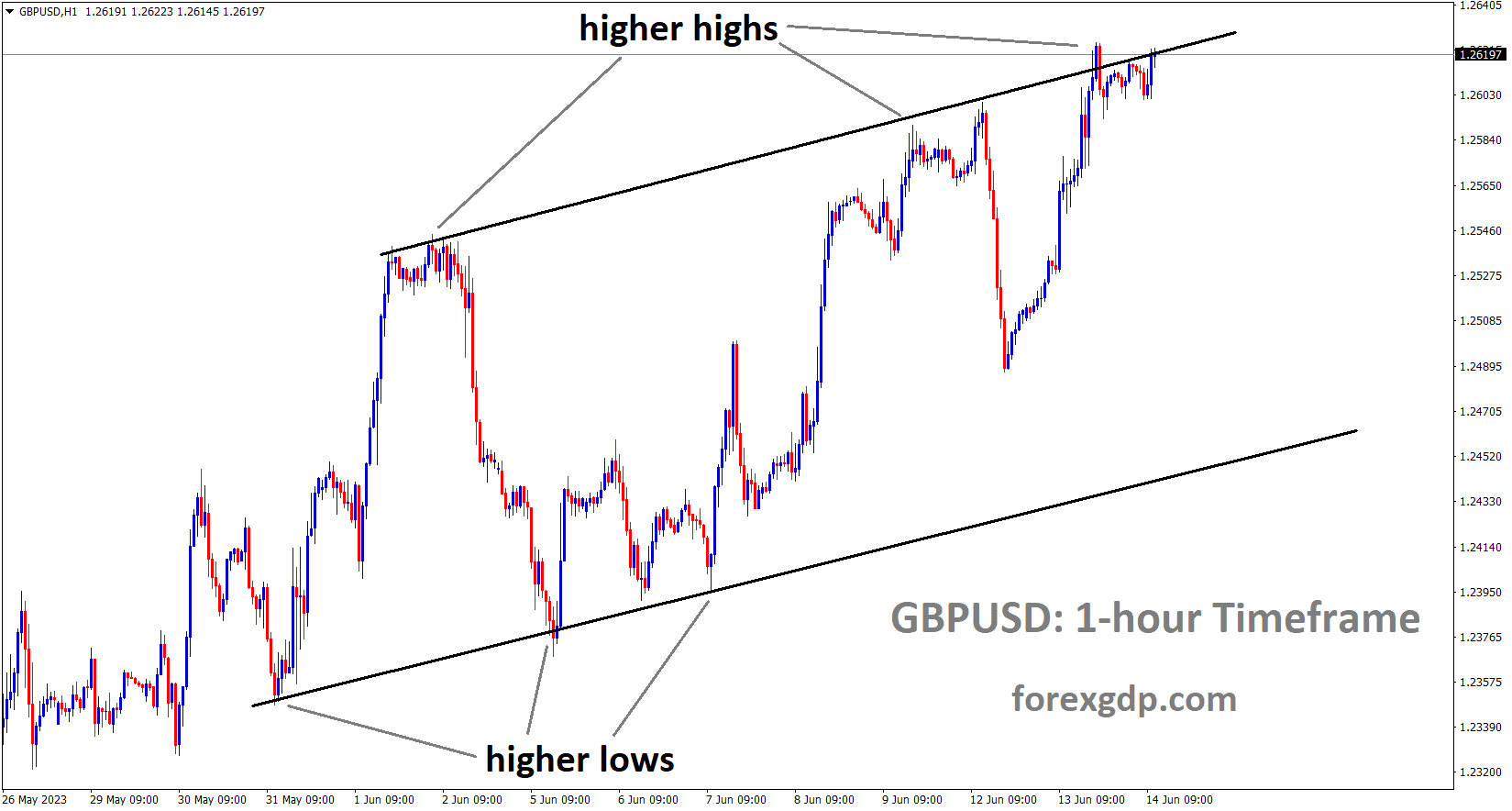

GBPUSD Analysis

GBPUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel.

Inflation measured by the UK CPI for the month of June was 7.9%, lower than the expected 8.2% and May’s 8.7%. Core inflation rate was 6.9% in June compared to 7.1% in May. Due to the UK’s low inflation reading, the Bank of England will raise interest rates by 25 basis points in August rather than the 50 basis points anticipated.

Following indications that price pressures in the UK are finally easing from high levels, the British pound appears poised to retrench slightly against its peers. According to data, annual inflation slowed to 7.9% in June from 8.2% expected and 8.7% in May. From 7.1% in May, core inflation decreased to 6.9% year over year. As a result, the Bank of England’s terminal benchmark rate expectations have been reduced from slightly over 6% on Tuesday to around 5.8% by the end of the year.

Additionally, this suggests that the BOE will move by 25 basis points rather than 50 basis points at its next meeting in August. The downside in the GBP is supported both from an absolute (level of terminal interest rates) and relative (potential for further tightening) monetary policy perspective in comparison to some of its peers because headline inflation is the highest among the G7 economies and significantly higher than the BOE’s 2% target.

GBPCHF Analysis

GBPCHF is moving in the Box pattern and the market has reached the horizontal support area of the pattern.

It is important to note that the USDCHF bears remain in control due to the CHF’s appeal as a safe haven and the market’s cautious attitude in the face of conflicting news about China and the world’s central banks. Additionally, the market’s scepticism about the Federal Reserve’s Fed performance beyond July contrasts with the Swiss National Bank’s SNB hawkish stance to weigh on the USDCHF prices. In this environment, the S&P500 Futures record slight losses while the weekly low in US Treasury bond yields is mixed. Prior to the US Initial Jobless Claims and Existing Home Sales, the risk catalysts may amuse USDCHF pair traders. Above all, it will be important to keep an eye out for any announcements made at the Federal Open Market Committee’s FOMC monetary policy meeting next week.

GBPNZD Analysis

GBPNZD is moving in the Box pattern and the market has reached the horizontal support area of the pattern.

The RBNZ will pause raising interest rates in upcoming meetings as NZD CPI data decreased from 6.7% in the first quarter to 6.0% in the second quarter. Due to US-China tensions and the RBNZ’s paused rate hike this month, the NZD is weaker against counter pair currencies.

AUDCAD Analysis

AUDCAD is moving in the Descending channel and the market has reached the lower high area of the channel.

The employment change in Australia was 32.6K in June as opposed to the 15K expected, and the unemployment rate dropped to 3.5% from the 3.6% anticipated. The tight labour market and expectation of a rate increase by the RBA in August to rein in rising employment levels helped the Australian dollar.

According to a report released on Thursday by the Australian Bureau of Statistics (ABS), the nation’s unemployment rate in June was 3.5% as opposed to the forecast of 3.6% and the previous figure of 3.6%. In June, the number of employed people increased by 32.6K, exceeding consensus expectations of 15K and the previous month’s enormous increase of 75.9K.

Additional information showed that compared to May’s 61.7K increase, full-time employment increased by 39.3K in the reported month. However, compared to a gain of 14.3K in May, part-time employment fell by 6.7K. In June, the participation rate decreased slightly to 66.8% from 66.9% expected and 66.9% in May.

Due to the fact that the economy will contract in 2023 and because it supports households and businesses spending more money to help the economy recover from Covid-19, the People’s Bank of China maintains its lending rates at 3.55% and 4.20%, respectively.

The Loan Prime Rate was maintained across the time curve, the People’s Bank of China declared on Thursday. The one-year and five-year LPRs were held steady by the Chinese central bank at 3.55% and 4.20%, respectively.

CADJPY Analysis

CADJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

In Canada, the June CPI data decreased to 2.8% Y/Y from 3.0% expected and 3.4% reported in May. This strongly encourages the Bank of Canada to postpone raising interest rates at its meeting in September. It is more effective to lower Canadian inflation now than it was earlier this month when rates were raised.

From 3.4% in May, the Canadian Consumer Price Index (CPI) for June dropped to 2.8% YoY. This result fell short of the 3% market expectation. In contrast to market expectations of a 0.3% gain, the CPI increased by 0.1% MoM. In addition, the monthly Core CPI fell 0.1% while the annual Core CPI dropped to 3.2% from 3.7% in May. The Core CPI excludes volatile food and energy prices. The Bank of Canada’s hawkish stance may provide some support for the Canadian Dollar. The BoC will decide on monetary policy at its upcoming meeting in September after receiving new information on inflation and the labour market.

In contrast to expectations of 2.44M and a gain of 5.946M the prior week, the Energy Information Administration (EIA) reported on Wednesday that the EIA Crude Oil Stocks Change in the week ending July 14 was -0.708M. Following the release of the data, the price of oil fell due to this figure’s indication of decreased demand for crude oil.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/