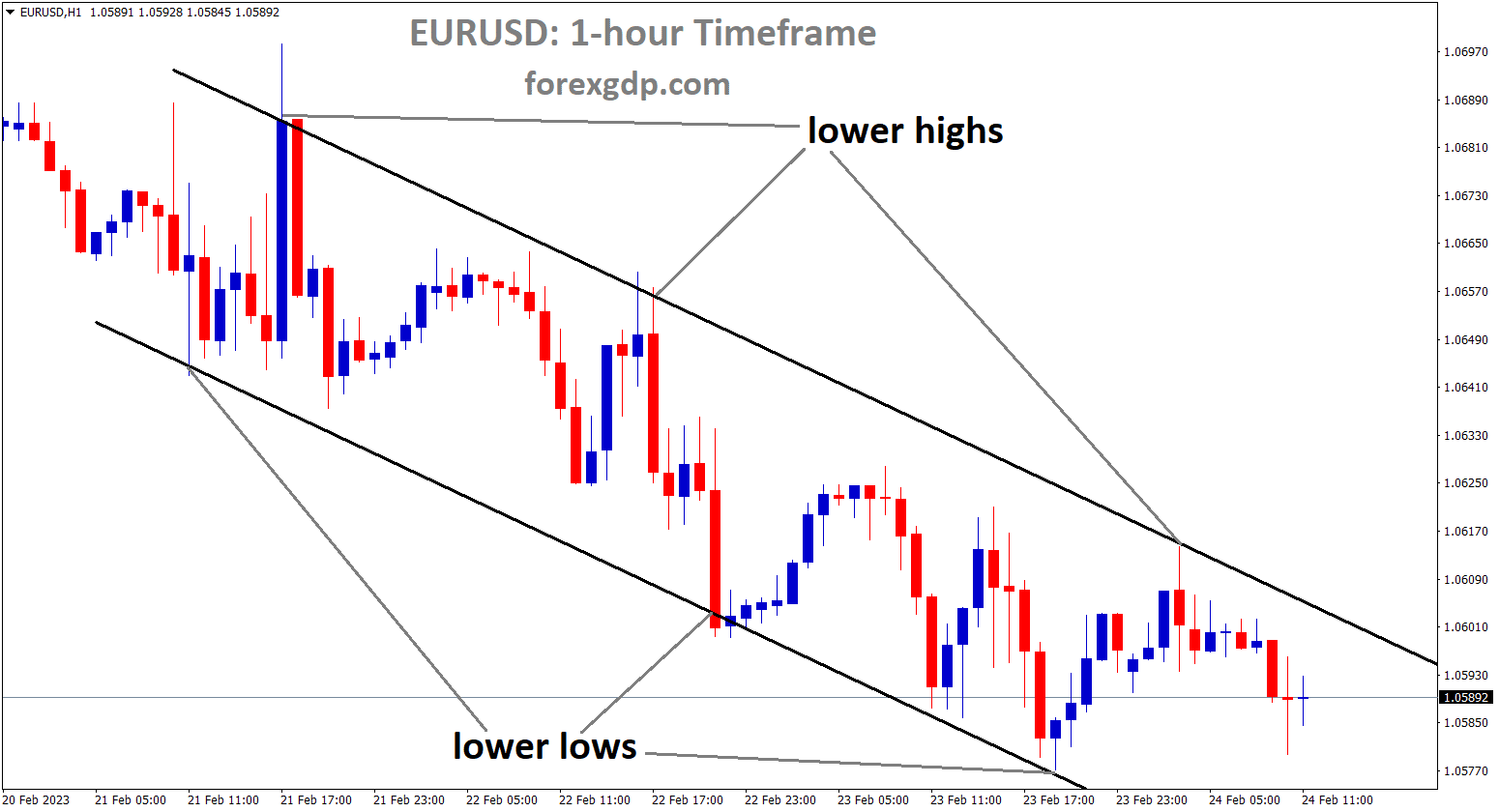

EURUSD Analysis

EURUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel.

Klass Knot, an ECB policymaker, stated that there will not be any rate increases following the July meeting because more economic contraction is still possible even if tightening measures are supported. The Euro did not increase this week relative to the USD.

Although lacking bullish conviction, the EURUSD pair edged up slightly during Friday’s Asian session and is currently trading just a few pips above a one-week low hit the day before in the 1.1135–1.1140 range. The US Dollar USD is seen extending recent strong gains driven by positive US Jobless Claims data and emerging as a major factor supporting the EURUSD pair. It is important to remember that during the week ending July 15, the number of Americans requesting unemployment insurance for the first time decreased by 9K, to 228K, marking the lowest reading since mid-May. The data confirmed market expectations for a 25 basis point rate hike by the Federal Reserve Fed in July and pointed to a still tight labour market. Additionally, the USD benefits from uncertainty surrounding the Fed’s commitment to a more dovish policy stance. The European Central Bank ECB officials’ recent mixed signals about the upcoming policy changes following the July meeting, on the other hand, undermine the common currency. Rate increases later this year may not be necessary, according to Klaas Knot, an ECB policymaker who is generally more hawkish. On the other hand, investors appear to be certain that the ECB will raise borrowing costs in July and September.

Consequently, it is prudent to exercise some caution before making aggressive directional bets on the EURUSD pair and setting up for an extension of the recent retracement from the 1.1275 region, or the highest level since February 2022 touched earlier this month. Ahead of next week’s major central bank event risks, which include the hotly anticipated FOMC monetary policy decision on Wednesday and the crucial ECB policy meeting on Thursday, market participants might also prefer to take a back seat. However, in the absence of any pertinent market-moving economic releases, either from the Euro Zone or the US, the EURUSD pair continues to be on track to post weekly losses and is at the mercy of the USD price dynamics.

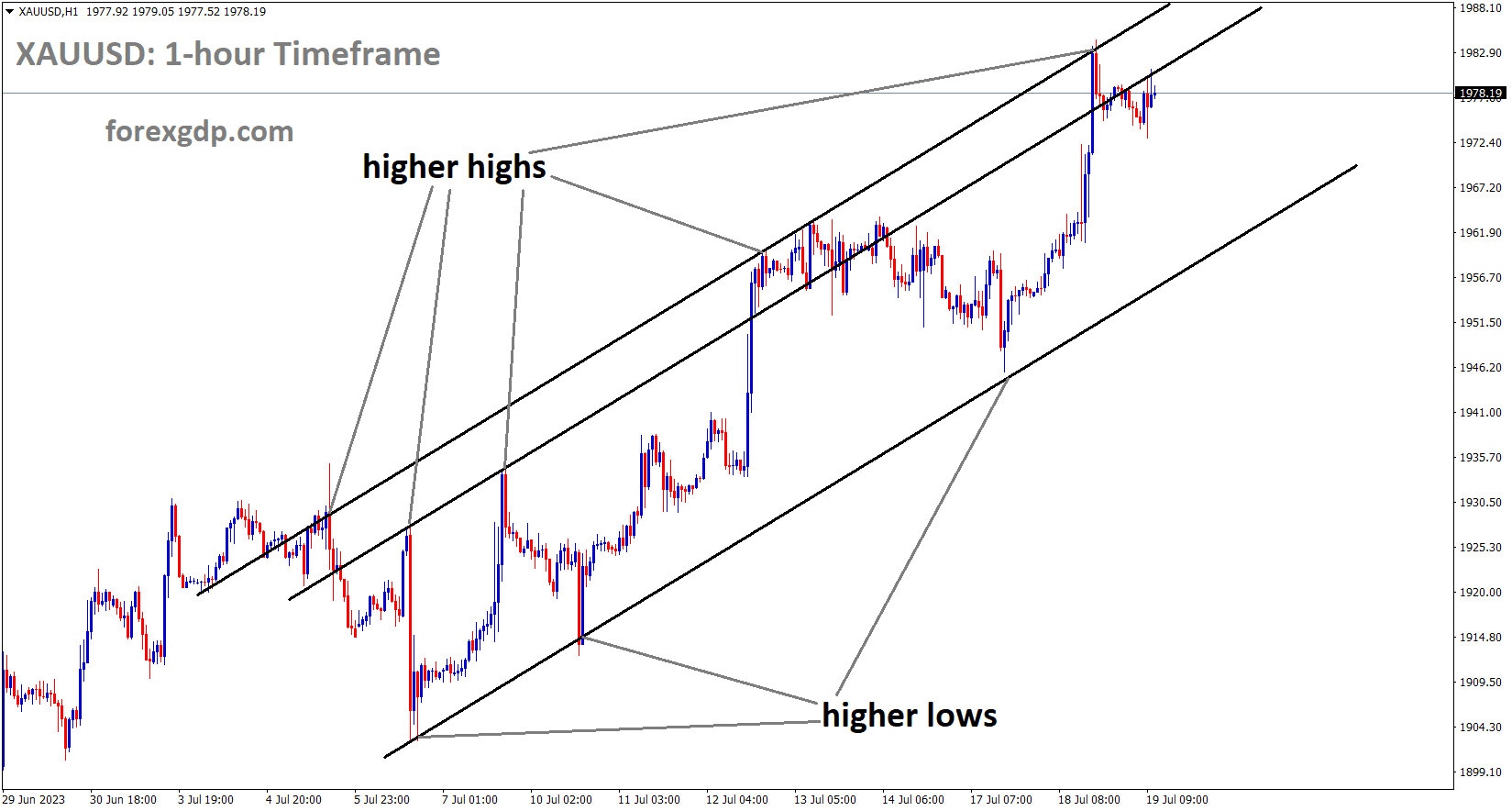

XAUUSD Analysis

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel.

After US initial jobless claims came in at a lower level than 242000 expected and the prior reading of 237000, the gold market is making corrections from its highs. The US dollar recovers from lows when the reading for the country is consistently positive.

Gold prices, which had been performing well earlier in the week, were muted on Thursday, dropping about 0.5% to $1,967 as a result of rising U.S. bond yields and a stronger U.S. dollar as a result of better-than-expected economic data in the United States. According to a Department of Labour report released in the morning, the number of Americans applying for unemployment benefits unexpectedly fell in the week ended July 15, from 237,000 to 228,000 compared to the expected 242,000, marking the lowest level since mid-May and indicating that mass layoffs have not yet taken place.

A strong rally in U.S. Treasury yields, particularly those at the front end of the curve, was sparked by positive labour market data, which also strengthened the dollar. Traders predicted that the U.S. economy’s remarkable resilience would force the Federal Reserve to tighten again in the autumn and maintain high rates for a longer period of time in order to combat inflation. When the Federal Reserve announces its monetary policy decision next week, we will have more information to evaluate the Fed’s plan, but one thing is certain: gold could take a beating if the institution indicates that more work is necessary to restore price stability and signals support for additional tightening. With attention on the FOMC meeting the following week, the bank is anticipated to increase its important benchmark rate by 25 basis points to a range of 5.25% to 5.50%, the highest level since 2001. Since this possibility has already been fully priced in, the outlook will be crucial for markets. If the outlook is still pessimistic, expectations for the terminal rate may rise, which would be unfavourable for precious metals.

USDCHF Analysis

USDCHF is moving in the Falling wedge pattern and the market has rebounded from the lower low area of the channel.

The Swiss trade balance has decreased from the previous reading of 5442 million to 4823 million. Imports increased while exports slightly increased. Tensions in the US-Sino relationship are concerning for the USD’s position against the CHF.

In the Asian session, the USDCHF pair maintains its recent gains above the 0.8660 level. Following the US Unemployment Claims data and the potential for another Fed rate increase after the July meeting, the pair reversed from the 0.8560 level on Thursday. According to data released on Thursday by the US Department of Labour DOL, initial jobless claims for the week ending July 15 totaled 228,000, lower than the previous week’s 237,000 total and below the expected 242,000. The number revealed the lowest reading since the middle of May. The Philadelphia Federal Reserve Manufacturing Survey, in contrast, registered a reading of -13 as opposed to the consensus of -10. The US Dollar Index DXY, which gauges the value of the dollar against six different currencies, has gained momentum in the wake of the data even though existing home sales from June also showed a contraction of 3.3% MoM against a 0.2% prior gain. The index has since bounced off the 100.00 level. The USDCHF pair then benefits from this as a windfall.

The Greenback has recovered as a result of market participants repricing another Fed rate increase following the July meeting. The odds for the November meeting increased from 19.8% a week ago to 32.2%, according to the CME FedWatch Tool, indicating that traders’ opinions of Fed monetary policy are shifting. The Swiss Trade Balance, on the other hand, increased from the previous 5,442 million to 4,823 million and was 5,442 million less than anticipated. Imports increased to 20,093M from 18,438M, while exports increased to 24,917M from 23,879M in May. In light of this, the cautious market sentiment regarding the US-China relationship may work in favour of the safe-haven Swiss Franc. The escalating trade conflict tension could limit the US Dollar’s gains and act as a drag on the USDCHF exchange rate. There were no noteworthy data releases on Friday. The announcements from the Federal Open Market Committee’s FOMC monetary policy meeting are anticipated by the market. This important occasion might have a significant effect on the US Dollar’s dynamics and provide the USDCHF pair with a clear trend.

EURJPY Analysis

EURJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

In the UK, retail sales for the month of June increased to -1.0% YoY from -1.5% expected and -2.1% from the prior reading. The GBP/USD exchange rate is positively affected by this data.

The dovish sentiment surrounding the Bank of Japan BoJ ahead of its monetary policy meeting next week might be strengthening the cross-currency pair’s upward momentum

On the other hand, more than 75% of respondents in the most recent Reuters poll, which was conducted between July 10 and July 19, favoured the BoJ’s inaction during the monetary policy meeting the following week. The survey report indicates that as a result, the Japanese central bank will not even change the Yield Curve Control YCC policy. However, the National Consumer Price Index CPI for June showed an increase in Japan’s inflation rate to 3.3% YoY from 3.2% compared to the expected 3.5%. This pushes back against the BoJ’s dovish stance and in favour of the GBP/JPY bulls. More information reveals that the National CPI ex-Fresh Food is expected to increase by 3.3% YoY, up from 3.2% previously, while the National CPI ex-Food and Energy is expected to decline by 4.2%, down from 4.3% previously. The Japanese government announced on Thursday that its previous estimates for the Asian giant’s Financial Year FY 2023–24 growth had been revised downward to 1.3% from 1.5%. Fumio Kishida, the prime minister of Japan, also supports the dovish concerns about the Bank of Japan BoJ by demonstrating his willingness to foster an environment in which wage increases are accepted as the norm.

In this environment, the Wall Street benchmark closed down while energy and technology shares performed poorly, which put downward pressure on Japan’s Nikkei 225. However, the S&P500 Futures are still unsure after reversing from the yearly high

GBPNZD Analysis

GBPNZD is moving in the Descending channel and the market has reached the lower high area of the channel.

According to the Society General Economist, the Bank of England may raise interest rates by 50 basis points at its next meeting if services and wage inflation do not fall below the 2% target in the two weeks prior to the meeting. Due to the potential burden of higher borrowing costs on the UK Government, investors may withdraw their funds from gilts. The continued lenient monetary policy of the Bank of England will drive up market inflation rates further.

The BoE may still choose 50 bps for three reasons, according to Société Générale economists. First off, despite reaching a peak in June, both wage and service inflation are still uncomfortably high in comparison to the 2% target. Two weeks after the August MPC, the MPC will receive confirmation that service prices are ceasing to rise. Second, investors are staying away from Gilts because UK inflation is still present. Investors demand higher compensation to hold Gilts compared to Treasuries and Bunds as a result of higher and more persistent inflation. The premium and cost of borrowing/interest burden for the government will only decrease when inflation expectations decline consistently. Not letting up on the financial brakes too soon is key to assuring investors. Thirdly, by keeping policy too loose for too long, the BoE and Governor Bailey in particular have come under fire for fanning the inflation flames. This might tempt the bank to go overboard in an effort to disprove its detractors.

NZDUSD Analysis

NZDUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel.

Existing home sales fell to -3.3% MoM in June as opposed to the previous reading of 0.20%, and the Philly Fed Manufacturing data dropped to -13.5 from -13.7. After US Data came in slightly higher than anticipated on the previous day, the NZD Dollar fell.

While reversing late Thursday’s corrective bounce off the weekly low during the early Asian session on Friday, NZDUSD is still declining at the intraday low of 0.6225. In doing so, the Kiwi pair prints the six-day losing streak despite the lack of significant data or events, as well as the market’s negative mood and the majority of negative headlines about China. Fears of rising US Treasury bond yields, the US Dollar, and the NZDUSD price all combine to dampen risk appetite in Asia, following Wall Street’s lead. However, despite the fact that US initial jobless claims decreased to 228K for the week ended on July 14—the lowest level since May—from 237K the week before and 242K market expectations, continuing jobless claims increased to 1.754M, exceeding expectations of 1.729M. In addition, the Philadelphia Fed Manufacturing Survey indicator rose to -13.5 for July from -13.7 the previous month, beating expectations of -10, while Existing Home Sales declined -3.3% MoM in June compared to an increase of 0.2% the month before.

Prior to this, the US Building Permits and Housing Stars both revealed negative results for June, while the Retail Sales growth slowed despite the publication of positive results for the Retail Sales Control Group for the same month. Despite recent encouraging signs regarding US employment, US statistics have not been strong enough to support the Fed’s announcement of additional rate hikes past July in the coming week, which could put the US Dollar bulls to the test. In light of this, the Wall Street benchmark ended the day lower while the S&P500 Futures are still down after hitting a new yearly high on Wednesday. The US Treasury bond yields have recently risen from their weekly lows, which has prompted NZDUSD bears.

The People’s Bank of China’s PBoC efforts to defend the second-largest economy in the world are combined with worries about seeing slowing Chinese growth elsewhere to spook NZDUSD traders. The PBoC Moves also pose a challenge to Kiwi pair buyers. During its Interest Rate Decision on Thursday, the People’s Bank of China PBoC maintained its benchmark Loan Prime Rates LPRs, but also took steps to entice foreign investment. As a result, the one-year and five-year LPRs are maintained at 3.55% and 4.20%, respectively, and the cross-border funding adjustment parameter for firms was increased from 1.25 to 1.5. The same makes it easier for Chinese institutes to receive funding from abroad. Moving on, if market sentiment improves, a light calendar might allow the NZDUSD Price to consolidate recent moves. However, the cautious atmosphere in advance of the Fed’s monetary policy decision next week may prevent an increase in risk appetite, which could have an adverse effect on the prices of the Kiwi pair.

AUDCAD Analysis

AUDCAD is moving in the Descending channel and the market has fallen from the lower high area of the channel.

Employment Insurance Beneficiaries Change in May showed a 2.5% increase versus a -0.5% decrease in April, which is good news for the Canadian dollar. The possibility that the Bank of Canada (BoC) will keep interest rates higher for longer in order to combat persistent inflation, however, is another factor that favours the CAD. Additionally, the escalating trade tensions between the US and China could put pressure on crude oil and limit the potential gains for the commodities-linked Loonie. China’s ambassador Xie Feng criticised the US on Thursday for its consideration of restrictions on AI chips and foreign investment. He further stated that China would respond in kind if the US increased restrictions on its chip industry in Beijing. The Canadian Retail Sales MoM is scheduled to be released later that day.

AUDCHF Analysis

AUDCHF is moving in the Descending channel and the market has fallen from the lower high area of the channel.

Following US domestic data showing a decrease in initial jobless claims to 228K, the Australian dollar fell. The public recovery plan in China is boosting demand and inflation, which is helping to boost the country’s auto and consumer electronics industries.

The Investors’ appetite for riskier assets is tempered by worries about China’s slowing growth, as well as the deteriorating US-China relations and geopolitical risks. Losses for the AUDUSD pair are nevertheless constrained by expectations that China will implement additional stimulus measures to speed up a faltering economic recovery and by rising expectations for additional interest rate hikes by the Reserve Bank of Australia RBA. The National Development and Reform Commission NDRC, China’s top economic planner, unveiled new initiatives on Friday with the goal of promoting domestic production, particularly in the automotive and consumer electronics industries. Additionally, the government promised to support domestic consumption in order to aid in the recovery of the economy, particularly in light of data released this week that revealed a sharp slowdown in China’s growth during the second quarter. The RBA is under pressure to take additional action as a result of the positive jobs report released from Australia on Thursday.

CADJPY Analysis

CADJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

The June CPI data from Japan’s National Bureau of Statistics showed a 3.3% increase from the previous month’s 3.2% and a 3.5% expectation. Due to Japanese Prime Minister Kishida’s last-day statement that ultra-loose monetary policy will be continued until wage growth reaches a normal level, this inflation data has no effect on the Japanese Yen.

The National Consumer Price Index (CPI) for June was released by the Japan Statistics Bureau, rising to 3.3% YoY from 3.2% versus the early Friday forecast of 3.5%. More information reveals that the National CPI ex-Fresh Food is expected to increase by 3.3% YoY, up from 3.2% previously, while the National CPI ex-Food and Energy is expected to decline by 4.2%, down from 4.3% previously. Fumio Kishida, Japan’s prime minister, defended the Bank of Japan’s (BoJ) ultra-easy monetary policy on Thursday in light of the country’s recent disappointing inflation data.

Crude Oil Analysis

Crude Oil price is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

The increase in crude oil prices following China’s injection of stimulus to help the nation stand up helped the Canadian Dollar gain ground against similar currency pairs. Today’s scheduled release of Canadian retail sales data has markets waiting.

For the second day in a row, Crude Oil prices increase, supporting the commodity-linked Loonie. The likelihood of tighter global supplies and the expectation that new Chinese stimulus measures will increase fuel demand in the world’s largest oil importer continue to be supportive factors for the dark liquid.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/