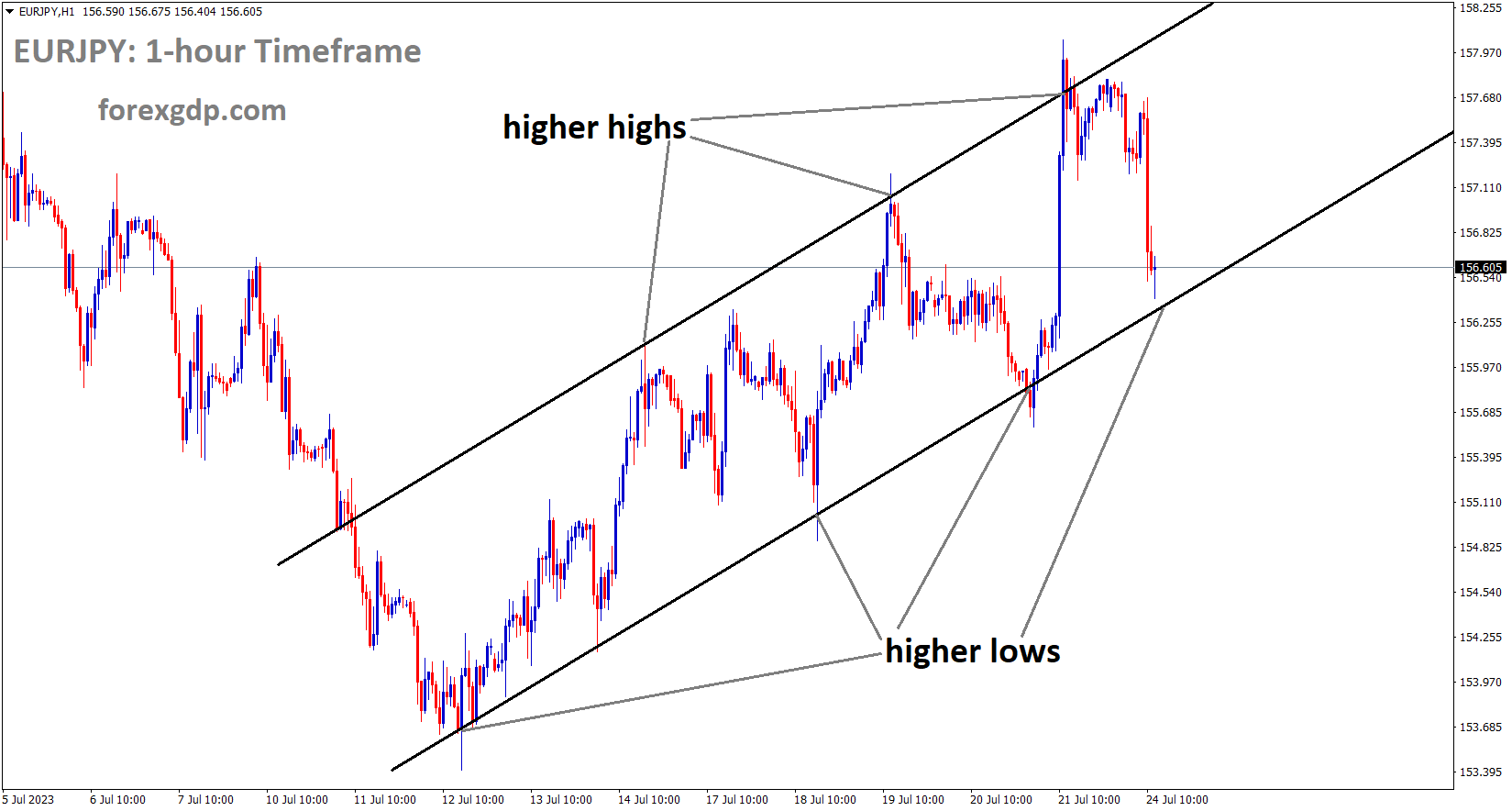

EURJPY Analysis

EURJPY is moving in an Ascending channel and the market has reached the higher low area of the channel.

Japan’s June inflation data showed a reading of 3.3%, which is higher than the desired level of 2%. The Bank of Japan did not raise interest rates at its upcoming meeting, as was more likely anticipated. As a result, the JPY continues to weaken against other currency pairs in the market.

The Bank of Japan’s BoJ monetary policy meeting this Friday, the Yen has weakened. In order to maintain yield curve control YCC, the BoJ has a policy rate of -0.10% and targets a band of +- 0.50% around zero for Japanese Government Bonds JGBs out to 10 years. There has been much talk about BoJ Governor Kazuo Ueda trying to change the YCC this year, but it is unclear when that might happen. As a result, the market is uncertain about monetary policy, which has caused the USDJPY to move noticeably. Masazumi Wakatabe, a former deputy governor of the Bank of Japan, mentioned today on Bloomberg television that he believes Governor Ueda has been attempting to improve clear communication.

CADJPY Analysis

CADJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

3.3% year-on-year inflation in Japan is significantly higher than the target of 2% inflation. The central bank is concerned about how long such levels can be sustained. A premature shift towards hawkishness could lead the third-largest economy in the world back towards deflation, which has periodically threatened the economy for decades

XAUUSD Analysis

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel.

In advance of this week’s FOMC and ECB meetings, gold prices are declining. The demand for non-yielding assets like gold declines as rates rise. Due to higher storage costs, the FED rate hike that began in 2007 and continues to this day will worry for gold.

On the first day of a new week, the price of gold finds it difficult to gain any traction and stays confined in a small band near the 100-day Simple Moving Average SMA throughout the Asian session. As traders eagerly await this week’s key central bank event risks before positioning for a firm near-term direction, the XAUUSD is currently trading just above the $1,960 level, virtually unchanged for the day. The Federal Reserve Fed is anticipated to increase interest rates by 25 basis points bps when it releases the results of its two-day policy meeting on Wednesday. Investors are also placing bets that the Fed will indicate that the current rate-hiking cycle is about to come to an end. However, the US Dollar USD is helped to maintain its goodish recovery gains from the lowest level since April 2022 touched last week and acts as a headwind for the Gold price due to doubts that the Fed will commit to a more dovish policy stance. Therefore, the accompanying monetary policy statement and Fed Chair Jerome Powell’s remarks at the press conference following the meeting will be of particular interest to the market.

The European Central Bank ECB meeting will take place on Thursday after this. According to the general consensus, the ECB will increase borrowing costs by 25 basis points once more and reaffirm its commitment to continuing the cycle of rate increases to control stubbornly high inflation, which is expected to continue to rise above the 2% target through the end of 2025. Another factor limiting the upside for the non-yielding gold price is the likelihood of further Fed and ECB policy tightening. Despite this, any significant decline in the XAUUSD seems elusive in the wake of mounting worries about China’s sluggish economic growth, the deteriorating US-China trade relations, and geopolitical risks. Therefore, it will be wise to wait for significant follow-through selling before making aggressive bets against the price of gold and setting up for an extension of the recent pullback from a peak reached last week that was over a two-month period. Market participants are now anticipating the release of the US and Euro Zone’s flash purchasing managers’ index PMI. Fresh information about the state of the economy will be revealed by the data, which will in turn influence people’s perceptions of risk more broadly and give the safe-haven precious metal some impetus. In addition, the USD pricey dynamics will be observed to take advantage of near-term trading opportunities near the XAUUSD.

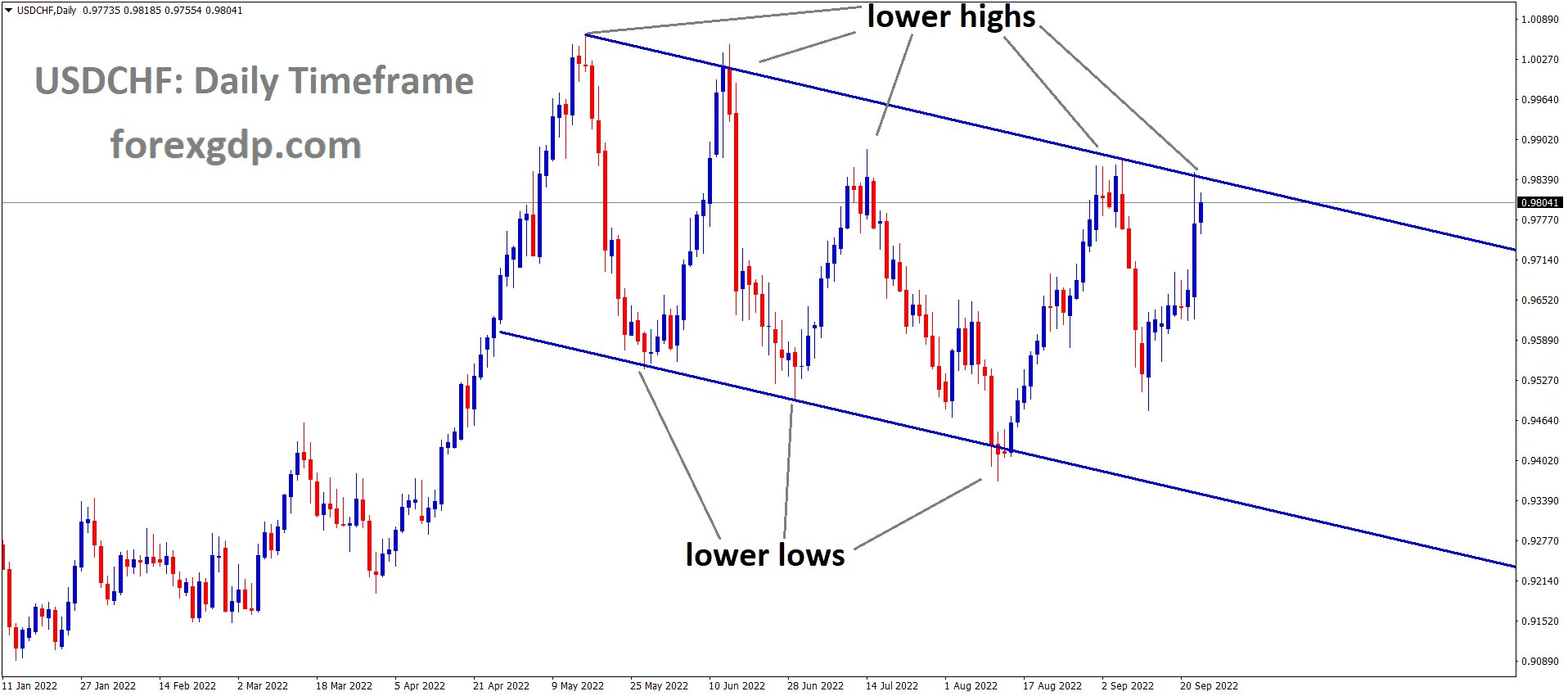

USDCHF Analysis

USDCHF is moving in the Falling wedge pattern and the market has rebounded from the lower low area of the pattern.

Ahead of this week’s FOMC meeting and ECB meeting, the Swiss Franc has been corrected against counterpairs. In their upcoming meeting, SNB has another rate hike planned. This week’s USDCHF pair is driven by US domestic news.

During the Asian session on Monday, the USDCHF pair draws some dip-buying near the 0.8640-0.8635 region, but it is unable to take advantage of the slight intraday increase. Spot prices are currently hovering just above the mid-0.8600s and are still quite close to the one-week high reached on Thursday. The US Dollar USD, which last week reached its lowest level since April 2022, is able to hold onto its recent recovery gains and ends up being a major factor favouring the USDCHF pair. Nevertheless, the belief that the Federal Reserve Fed is nearing the end of its current cycle of policy tightening prevents USD bulls from making aggressive bets and limits the major’s upside potential. Recall that following the highly anticipated 25 bps lift-off in July, the markets have been pricing out the possibility of any additional rate increases by the US central bank. Investors are sceptical that the Fed will stick to its forecast of a 50 basis point rate increase by the end of this year or commit to a more dovish policy stance. As a result, Wednesday’s conclusion of a two-day FOMC policy meeting will continue to be the main topic of discussion.

EURUSD Analysis

EURUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel.

At its monetary policy meeting this week, the ECB is anticipated to announce a 25 bps rate increase. Germany is already in a recession, despite the fact that the Euro CPI is lower than what was anticipated for the month of June. Multiple rate increases may cause the economy to tighten further, which could lead to recession fears in the Eurozone.

At the conclusion of its July meeting on Wednesday, the FOMC in the US is anticipated to increase its benchmark rate by a quarter point, to a range of 5.25% to 5.50%. The focus will be entirely on the guidance now that this decision has already been fully priced in, specifically on whether the institution intends to deliver additional hikes in 2023 as it has previously stated. Although June’s U.S. inflation data were weaker than anticipated, the central bank may decide against changing its outlook in order to preserve its options should price pressures pick up later in the year to the point where additional action is required. This scenario is entirely feasible given how well the economy has held up and repeatedly defied the doomsayers.

Markets are likely to reprice the Fed’s terminal rate upward if it continues to hold a hawkish stance and resists outside pressure to alter course. This will cause Treasury yields, particularly those at the front end of the curve, to spike. The US dollar would benefit from this outcome. The ECB is also seen implementing a 25 basis-point rate increase on the other side of the Atlantic, but with dovish overtones. President Lagarde might take a firm “data-dependent approach,” refusing to pre-commit to another hike at the September meeting, given that several European policymakers are worried about the risks of excessive tightening and the German economy is on the verge of a severe slump. A “dovish hike” is likely to hurt the euro, which will cause traders to reduce their bets on additional monetary tightening. As a result, the common currency might not be able to increase its gains against the US dollar, which might lead to a modest downward correction in the EURUSD rate.

EURCHF Analysis

EURCHF is moving in the Descending channel and the market has reached the lower low area of the channel.

Investors will closely examine the accompanying monetary policy statement and remarks made by Fed Chair Jerome Powell at the post-meeting press conference in addition to the crucial FOMC decision for hints about the trajectory of future interest rate hikes. The outlook will, in turn, have a significant impact on the dynamics of the USD price in the near term and aid investors in predicting the direction of the next leg of the USDCHF pair’s directional move. However, worries about a global economic slowdown, worsening US-China trade relations, and geopolitical risks could destabilise the safe-haven Swiss Franc CHF and limit gains for the major. On Monday, traders will look for short-term opportunities around the USDCHF pair based on the flash US PMI prints for July, which are scheduled to be released later during the early North American session.

GBPCHF Analysis

GBPCHF is moving in the Box pattern and the market has reached the horizontal support area of the pattern.

The Bank of England was under less pressure last week because the GBP CPI data came in lower than anticipated, giving the GBP a weaker tone. The GBP PMI data for this week is concentrated and better than the reading, which is favourable for the GBP.

AUDUSD Analysis

AUDUSD is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

Australian Treasurer Jim Chalmers anticipated that the nation’s budget surplus would be AUD 20 billion, which was higher than what was anticipated in the previous month. The AUD 2.81 billion and AUD 4.2 billion forecasts for the months of May and June, respectively.

Australia Treasurer Jim Chalmers stated that he anticipates the nation’s budget surplus to be set at roughly AUD20 billion during a news conference on Monday in Canberra. The surplus for 2022–2023 is currently anticipated by the officials to be around $20 billion, or more likely just north of that amount, Chalmers noted. The Australian budget surplus for 2022–2023 will likely be higher than the AUD4.2 billion (USD2.81 billion) forecasted in the May budget, Chalmers had hinted in June.

The Australian CPI data for Month on Month is predicted to be 6.2% instead of the 7.0% that was originally planned for this week. Higher CPI favours an RBA rate hike in the August meeting, while Lower CPI favours the RBA pausing a rate hike.

The unexpectedly strong jobs data was the domestic high point of the Australian Dollar’s recent volatile week. The US Dollar’s external gyrations kept the AUDUSD exchange rate volatile. In June, Australia’s unemployment rate was 3.5%, which was lower than the predicted and previous 3.6%. Australian employment increased by 32.6k in the month, significantly more than the 15k predicted and the 75.9k added the month before. The increase in full-time employment of 39.3k positions and the decline in part-time employment of -6.7k positions were noteworthy, and the participation rate fell slightly to 66.8% from 66.9%. Even though the economy has shown some signs of slowing down, the tight labour market makes it difficult to relieve price pressures. The Australian headline CPI for the end of the second quarter will be released on Wednesday. According to a Bloomberg survey of economists, 6.2% is expected as opposed to the previous 7.0%.

The Reserve Bank of Australia’s RBA preferred measure of trimmed mean inflation is expected to be 6.2% for the same period, according to the same survey. During the previous quarter, it was 6.6%. A more reliable indicator of inflation in the Australian economy than the monthly measure is the quarterly CPI. Only 62–73% of the weighted quarterly basket is measured by the latter. You can read more information here. The RBA’s mandate, which entails aiming for average inflation between 2 and 3 percent over time, is tied to the quarterly number. For traders of Australian Dollar financial market products, Wednesday is a special day. A smorgasbord of US data will also be released during the upcoming week, in addition to monetary policy meetings at the Federal Reserve and the European Central Bank. They could all influence markets and the AUDUSD. The Chinese outlook, which is sputtering away in the background as authorities there nibble at the edges to boost the economy, is struggling to gain traction. Before believing that growth and activity will pick back up, the market seems to be looking for much larger doses of support. Although the jobs affected AUDUSD, events may still be dominated by the inverse correlation to the DXY USD Index. A number of markets may experience increased volatility due to the accumulation of upcoming event risks.

NZDUSD Analysis

NZDUSD is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

The NZ economy continues to experience higher inflation, and Q2 CPI results show 1.1% more than the 0.90% expected in June month, making NZ less competitive with the USD. The RBNZ may be able to raise the rate in order to control inflation. According to RBNZ Forecast, no rate reductions will occur before 2024.

It might take a little longer to find directional plays in the New Zealand dollar versus some of its peers, at least until there are indications of divergence in monetary policy outlooks. Currency pairs are now subject to the ebb and flow of data due to convergent monetary policy outlooks, which tends to be noise at best unless viewed from a zoomed-out perspective. The US Fed rate decision on Wednesday is the main topic of attention in this regard. With its forward guidance as the main consideration, the central bank is widely anticipated to increase interest rates for the final time this year.

A hawkish increase could support the US dollar internationally. A dovish hike could put downward pressure on the USD and strengthen NZD, whereas a more data-dependent wait-and-watch could return the USD to its recent ranges. With the belief that NZ rates have peaked, the Reserve Bank of New Zealand kept interest rates on hold earlier this month. The policy outlook is complicated by NZ inflation, which has remained stubbornly high (up 1.1% on-month in the June quarter vs. 0.9% expected). With no rate cuts until mid-2024, markets are currently pricing in a 50% chance of another rate hike by the RBNZ.

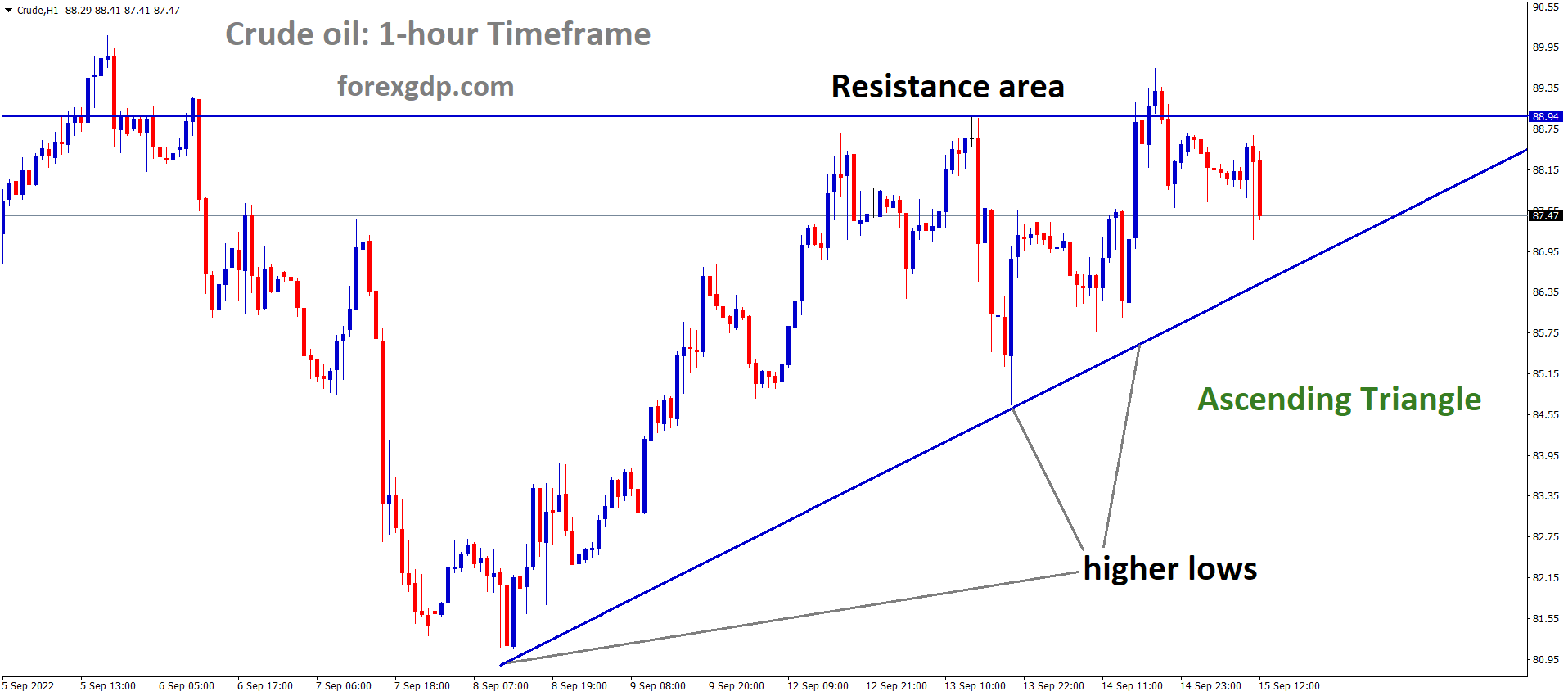

Crude oil Analysis

Crude oil price is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

May retail sales in Canada came in at 0.20%, down from 1.0% the month prior and 0.50% expected. The Canadian Dollar is weaker against counter pairs due to declining sales print. Unexpected rate increases by the Bank of Canada cause the Canadian labour market and consumer spending to tighten.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/