GBPUSD Analysis

GBPUSD is moving in an Ascending channel and the market has reached the higher low area of the channel.

UK Manufacturing PMI dropped from 46.5 in June to 45.0 in July. In the UK, this is the 12th consecutive contraction. Aggressive rate increases by the Bank of England reduce manufacturing and consumption in an effort to lower the UK’s inflation rate.

The GBPUSD pair is still under stress and finds it difficult to increase during Tuesday’s Asian session. The important pair is currently up 0.1% for the day as it trades near the 1.2840 level. In anticipation of the Federal Open Market Committee’s FOMC meeting on Wednesday, the market has turned cautious. In July, US business activity hit a five-month low. S&P Global Composite PMI dropped from 53.2 to 52. Overwhelming market expectations, the US S&P Global Manufacturing PMI increased from 46.3 to 49. The Composite PMI index dropped to 52 from 53.2 in June, while the Services PMI dropped from 54.4 to 52.4, below the predicted level of 54. Some have speculated that the Fed is about to end its tightening monetary policy as a result of recent economic data showing cooling inflation and a tight labour market. On Wednesday, the FOMC meeting is widely anticipated to increase its benchmark rate by another quarter-point. It is widely believed that the Fed will increase interest rates by a quarter point, to between 5.25 and 5.50 percent. However, hints about the potential for interest rate guidance will be dropped during Fed Chairman Jerome Powell’s press conference on Wednesday. The US Dollar may spike if the Fed adopts a hawkish stance.

The preliminary PMI data for the UK, on the other hand, showed that economic activity in July was weaker than anticipated. The Manufacturing PMI for July dropped to 45.0 from 46.5 in June, which was worse than the 46.1 expectation. The manufacturing sector experienced its 12th consecutive decline with this number. The preliminary Services PMI, meanwhile, dropped from 53.7 expected and 53.0 prior to 51.5. On August 3, market participants predict that the Bank of England BoW will increase the interest rate from 5% to 6%. However, the BoE’s second rate increase fuels more worries about the Bank’s most pronounced rate increases in three decades and their effects on the UK economy. The value of the USD will probably continue to affect the movement of the pair in the absence of significant economic data released from the United Kingdom. Market participants will monitor the FOMC meeting and the press conference of Fed Chairman Jerome Powell. In addition, traders will pay attention to the Advance GDP QoQ, US CB Consumer Confidence, and the Fed’s preferred inflation indicator, the core Personal Consumption Expenditure PCE Price Index MoM. These statistics may have a significant effect on the US Dollar’s dynamics and provide the GBPUSD pair with a clear trend.

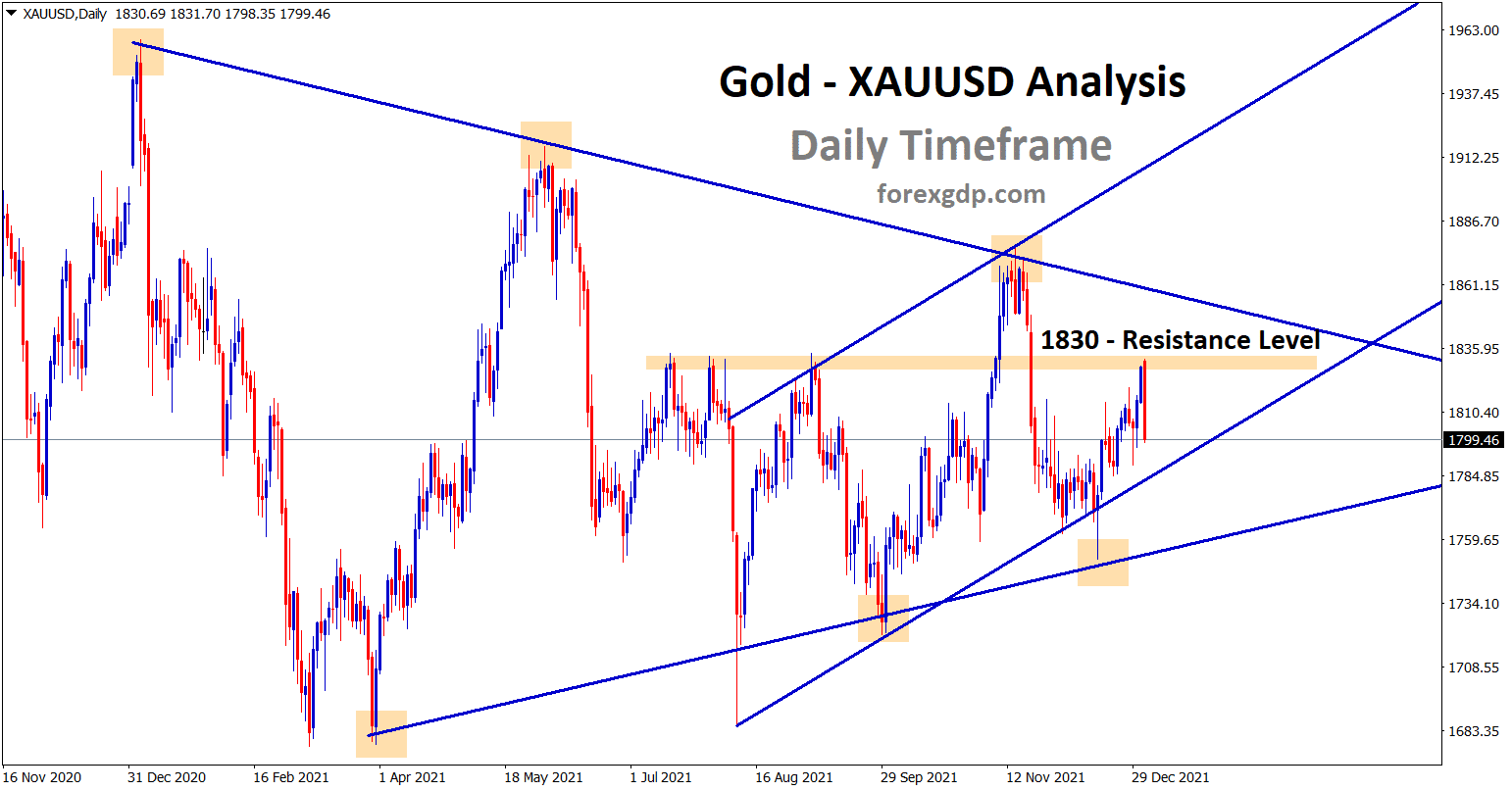

XAUUSD Analysis

XAUUSD Gold Price is moving in an Ascending channel and the market has reached the higher low area of the channel.

China expresses greater interest in the stimulus injection and offers support for gold. The recovery of China’s economy benefits consumers of gold in general. Due to higher storage costs, higher interest rates cause a slower rate of demand for gold. When rate increases are stopped, gold prices will likely move higher.

Tuesday’s Asian session sees a modest increase in the price of gold. The price of XAU/USD is currently trading near $1,960, up 0.36% on the day. Investors anticipate additional guidance for the entire year at the Federal Open Market Committee (FOMC) meeting and Fed Chairman Jerome Powell’s press conference. Data from the July S&P Global Composite PMI for the US were weaker than anticipated. The number decreased from 53.2 to 52, versus the predicted 53.1. While the S&P Global Services PMI fell to 52.4 from 54.4, the S&P Global Manufacturing PMI increased to 49 from 46.3. In addition, the depressing US housing and inflation data released last week support the US Dollar and suggest that the Fed may be nearing the end of its cycle of rate hikes. As the opportunity cost of holding non-yielding bullion increases with rising interest rates, it is important to note that gold is sensitive to these changes. The Federal Reserve’s (Fed) decision on interest rates on Wednesday will be the major event of the week. It is widely believed that the Fed will increase interest rates by a quarter point, to 5.25–5.50%. Market participants believe that the Fed is about to end its tightening monetary policy and that it will get further direction from the press conference of Fed Chairman Jerome Powell. The US Dollar could be sparked by the Fed’s hawkish stance, which would also be detrimental to the price of gold.

XAGUSD Analysis

XAGUSD Silver Price is moving in the Descending channel and the market has reached the lower high area of the channel.

China, the biggest consumer of gold worldwide, also indicated additional support for the real estate industry and a number of initiatives to boost domestic consumption in the midst of a sluggish post-COVID recovery. This in turn encourages the price of gold to rise further. Market participants are currently intently observing the Fed’s meeting on monetary policy in the future. The price of gold in US dollars could be significantly impacted by this circumstance. Also due later this week are the Advance GDP QoQ and US CB Consumer Confidence. Investors will keep an eye on this development and look for opportunities as the price of gold changes.

USDCHF Analysis

USDCHF has broken the Box pattern in upside.

The US S&P Global manufacturing PMI showed improved results, while the Composite PMI showed lower results and the Service PMI showed lower results, pushing the US Dollar up against the Swiss Franc. The US dollar is more valuable against the Swiss franc in advance of the FOMC meeting and the potential for a 25 basis point rate hike.

The USDCHF pair encounters resistance near the 0.8700 level and drops a few basis points from a nearly two-week high reached earlier on Tuesday during the Asian session. Spot prices are currently trading around the 0.8685 area and are down 0.10% for the day. The US Dollar USD is the primary driver of the modest intraday decline. In fact, a one-week-old recovery trend from the USD Index’s DXY lowest level since April 2022, which was reached last week, now appears to have come to an end. This index tracks the value of the US dollar against a basket of currencies. However, traders may choose to wait for new cues regarding the Federal Reserve’s Fed future path of rate hikes rather than making aggressive USD bearish bets. In addition, the current risk-on environment may weaken the safe-haven Swiss Franc CHF and further limit the downside for the USDCHF pair, at least temporarily. It is important to note that the markets have been pricing out the possibility of any additional rate increases following the widely anticipated 25 bps lift-off on Wednesday at the conclusion of a two-day FOMC policy meeting. The question of whether the US central bank will commit to a more dovish policy stance or stick to its forecast for a 50 bps rate hike by the end of this year, however, has investors wary. Therefore, the accompanying policy statement and Jerome Powell’s remarks from the Fed will be the main points of discussion. In turn, the outlook will have a significant impact on the dynamics of the USD price in the near term.

The recent optimism regarding additional Chinese stimulus measures, however, continues to support the risk-on rally across the Asian equity markets. China will accelerate economic policy adjustments, concentrating on increasing domestic demand, boosting confidence, and mitigating risks, according to the Politburo, the top decision-making body of the ruling Communist Party, as quoted by the state news agency Xinhua. This calls for caution before placing bearish bets on the USDCHF pair as it could drive flows away from conventional safe-haven currencies, such as the CHF. Market participants are now looking to the US macro data, specifically the Richmond Fed Manufacturing Index and the Conference Board’s Consumer Confidence Index, for some traction later during the early North American session. The Advance Q2 GDP print and the Core PCE Price Index, the Fed’s preferred inflation gauge, are also on this week’s rather full US economic calendar, and they should help determine the next leg of a directional move for the USDCHF pair. Therefore, significant follow-through selling is required to verify that the recent rebound from a multi-year low has peaked.

EURCAD Analysis

EURCAD is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

Euro is HCOB Manufacturing PMI printed at 42.7, down from 43.4 previously and 43.5 anticipated, marking the lowest level since May 2020. The services PMI decreased from 52.0 to 51.1, while the composite PMI decreased from 49.9 to 48.9. Germany’s Manufacturing, Composite, and Services PMI all printed lower than anticipated, raising concerns about a possible recession in the continent.

The 0.25% rate hike is already priced in, the quote fell the day before after disappointing activity data from the Eurozone and Germany raised concerns about a possible recession in the region. The Eurozone HCOB Manufacturing PMI’s preliminary readings for July fell to 42.7 from 43.4 the previous month and fell short of market expectations of 43.5, marking the lowest level since May 2020. Despite this, the Services PMI decreased to 51.1 for the aforementioned month from 52.0 in the previous reading and 52.5 expected, while the Composite PMI decreased to 48.9 from 49.9 in the previous reading and 49.7 predicted by analysts. In a similar vein, the German HCOB Manufacturing PMI also fell to a 38-month low, and the July Services and Composite PMI readings fell short of market expectations.

Black gold Following China’s decision to increase economic stimulus, the price of crude oil changed for the better. China is the world’s largest oil importer, and demand for fuel is expected to rise as a result of the tight supply from the production of the OPEC+ countries. Canadian Dollar is likely to benefit from profits of Oil exports.

The expectation that additional stimulus from China, the world’s largest oil importer, will increase fuel demand is keeping crude oil prices well supported as they consolidate recent strong gains to over a three-month high touched on Monday. In addition, the black liquid is expected to benefit from expectations for a reduction in global supply, which is expected to support the Loonie, a currency linked to commodities.

GBPCAD Analysis

GBPCAD is moving in an Ascending channel and the market has reached the higher low area of the channel.

According to one group of respondents in the Bank of Canada’s most recent survey, the interest rate will remain at 5% until the end of 2023. However, other groups of respondents thought it might drop to 3.5% in the fourth quarter of 2024.

The UK S&P GlobalCIPS Manufacturing PMI preliminary readings for July fell to the lowest level since 2023, at 45.0, compared to the market’s expectations of 46.1 and previous readings of 46.5. However, the Services PMI also registered a six-month low, falling to 51.5 from 53.7 previously and 53.0 predicted by the market. As a result, the initial readings of the Composite PMI decreased slightly to 50.7 from the prior estimates of 52.4 and 52.8 made by analysts. Even though the UK PMIs are not great, the British Pound GBP appears to have a floor because of the time between the Bank of England BoE Monetary Policy Meeting and UK Prime Minister Rishi Sunak’s announcements of numerous stimulus measures to support the Tory government. But the EURGBP bears are put to the test by worries about the UK recession.

AUDUSD Analysis

AUDUSD is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

China is planning to increase its economic stimulus to recover from the effects of COVID-19. China’s action of injecting stimulus to revive the economy has a significant positive impact on the Australian Dollar. Australian exports ought to increase if China’s economy improves.

Following the Asian session dip back towards a technically significant 200-day Simple Moving Average SMA, the AUDUSD pair attracts new buying and turns positive for a second straight day on Tuesday. Spot prices are currently trading in the 0.6765-0.6770 range, up just over 0.40% on the day, having recovered from a one-week low reached on Monday. The risk-on rally across Asian equity markets continues to be supported by the most recent optimism regarding additional stimulus measures from China, which also helps the risk-sensitive Australian Dollar AUD. China will accelerate economic policy adjustments, concentrating on increasing domestic demand, boosting confidence, and mitigating risks, according to the Politburo, the top decision-making body of the ruling Communist Party, as quoted by the state news agency Xinhua. This is considered to be another factor driving the AUDUSD pair higher, along with a slight decline in the value of the US Dollar USD. The USD Index DXY, which measures the value of the dollar relative to a basket of currencies, actually pulls back from a two-week high and, for the time being, appears to have stalled a five-day-old recovery move from its lowest level since April 2022, which it reached last week. The USD decline could only be the result of some profit-taking and is likely to be brief as traders anxiously await new cues regarding the Federal Reserve’s Fed future path of rate hikes. The outcome of the highly anticipated two-day FOMC monetary policy meeting will therefore continue to be the main topic of discussion.

AUDCHF Analysis

AUDCHF is moving in the Falling wedge pattern and the market has reached the lower high area of the pattern.

Interest rates are anticipated to increase by 25 basis points by the Fed. Market participants are still uncertain as to whether the US central bank will commit to a more dovish policy stance or stick to its forecast for a 50 basis point rate hike by the end of this year. This in turn implies that investors will carefully examine the accompanying policy statement and comments made by Fed Chair Jerome Powell to assess the outlook of the central bank. This will be crucial in determining the near-term USD price dynamics and the next leg of the AUDUSD pair’s directional move. The publication on Tuesday of the Richmond Manufacturing Index and US Consumer Confidence Index by the Conference Board may give the early North American session a boost later on. The following quarter’s Australian consumer inflation data, which is due on Wednesday, will draw the attention of the market. The Advance US Q2 GDP print and the Fed’s preferred inflation indicator, the Core PCE Price Index, are also featured on this week’s busy economic calendar.

AUDJPY Analysis

AUDJPY is moving in the Descending channel and the market has reached the lower high area of the channel.

As the policy divergence between the Bank of Japan and the FED widens, the market weakness of the Japanese Yen continues. The FED was anticipated to raise interest rates this week by 25 basis points, but the Bank of Japan is anticipated to maintain its current monetary policy. Japanese inflation is outpacing the target rate of 2%. In the upcoming months, the economy will be weaker due to loose policy and higher inflation.

In the lead-up to two significant market-moving events later in the week, the Federal Reserve’s interest rate decision on Wednesday and the Bank of Japan’s announcement of its monetary policy on Friday, the USDJPY traded lower on Monday due to cautious sentiment and slightly lower U.S. Treasury yields. The Fed, which is being led by Jerome Powell, is expected to raise interest rates by a quarter point, bringing the target range to 5.25%-5.50%, the highest level since 2001. This action has already been discounted by investors, so forward guidance will now be the main focus.

Although the June U.S. inflation report was weaker than expected, the FOMC may adopt a more aggressive stance to keep its options open in case price pressures pick up later in the year and additional tightening is required. Trading will likely reprice the central bank’s terminal rate slightly upwards, driving Treasury yields higher, if Powell defies external pressure to adopt a dovish stance and indicates that more effort is needed to regain price stability.

NZDUSD Analysis

NZDUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel.

The NZD pair is slightly weaker against the USD ahead of US Consumer Confidence and FOMC data. A pause in the RBNZ’s rate hike this month raises concerns about further strengthening of the NZD against the USD.

On Tuesday, the NZDUSD pair recovers nearly 35 pip from its low from the Asian session and starts to move in the right direction. Spot prices are currently trading in the 0.6210-0.6215 range, up 0.15% on the day, and are supported by a mild decline in the value of the US Dollar (USD). In fact, the USD Index (DXY), which measures the value of the dollar against a basket of currencies, breaks a five-day winning streak to reach a nearly two-week high, and for the time being, it appears to have halted the recent recovery from the low point it reached last week—its lowest level since April 2022. The USD decline, which could only be attributed to some profit-taking in the absence of any fundamental catalyst, is likely to remain contained as traders anxiously watch for clues about the Federal Reserve’s (Fed) likely future rate-hike path. Remember that the markets have been pricing out the possibility of any additional rate hikes following the widely anticipated 25 bps lift-off on Wednesday at the conclusion of a two-day FOMC policy meeting. Market participants are still uncertain as to whether the US central bank will commit to a more dovish policy stance or stick to its forecast for a 50 basis point rate hike by the end of this year. Therefore, the accompanying policy statement and Jerome Powell’s remarks from the Fed will be the main points of discussion.

The outlook will be crucial in determining the near-term USD price dynamics and the next leg of the NZDUSD pair’s directional move. Meanwhile, concerns about a global economic slowdown, deteriorating US-China relations, and geopolitical risks could continue to support the safe-haven Greenback in some ways and limit any significant upside for the risk-averse Kiwi. Aggressive bullish traders should exercise some caution as a result of this. Tuesday’s release of the Conference Board’s US Consumer Confidence Index and Richmond Manufacturing Index could give the NZDUSD pair some momentum later during the early North American session as we approach the key central bank event risk. The Advance Q2 GDP print and the Core PCE Price Index, the Fed’s preferred inflation gauge, are also on this week’s rather busy US economic docket, which should help add some volatility to the markets.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/