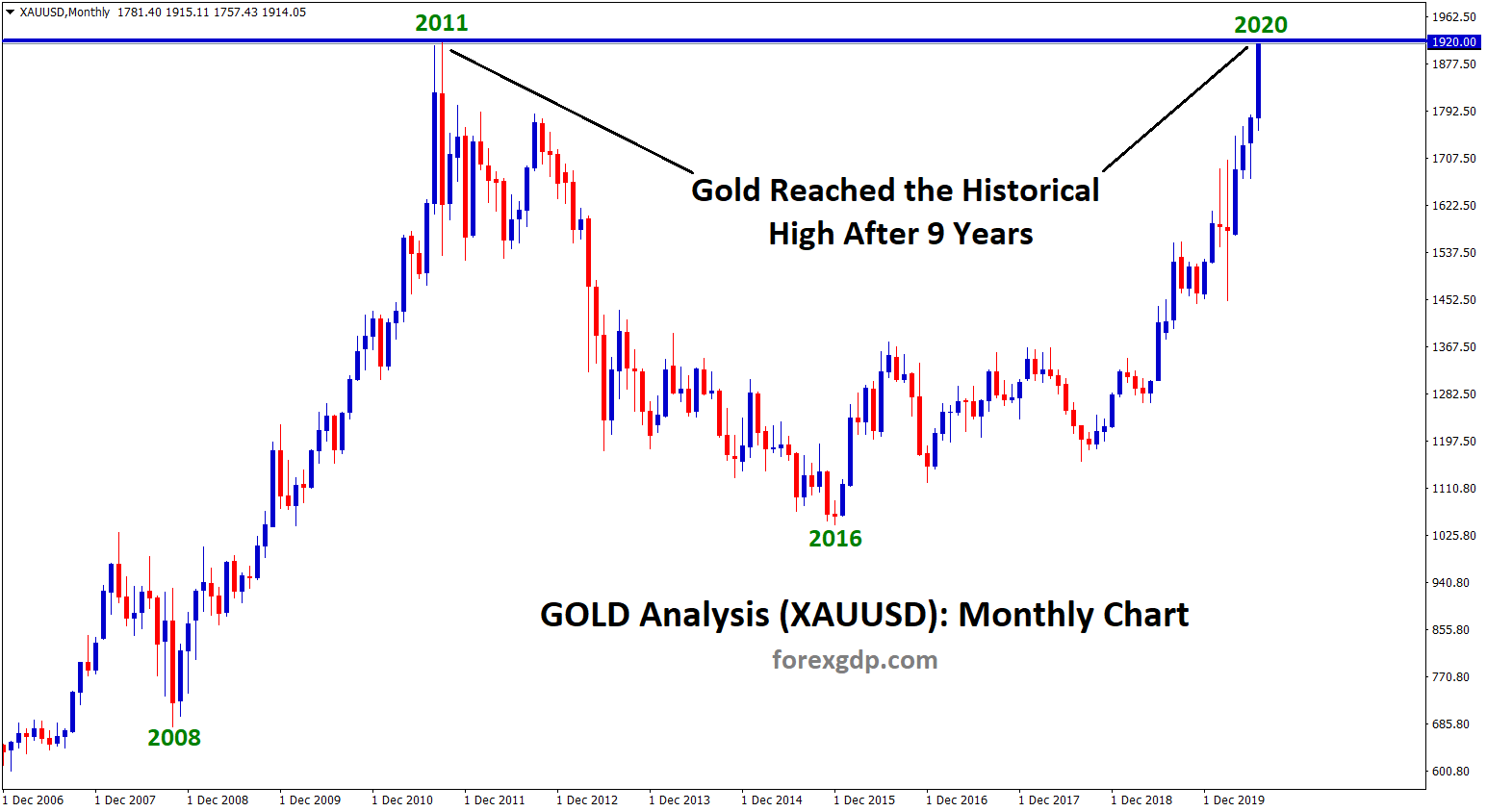

GOLD Analysis

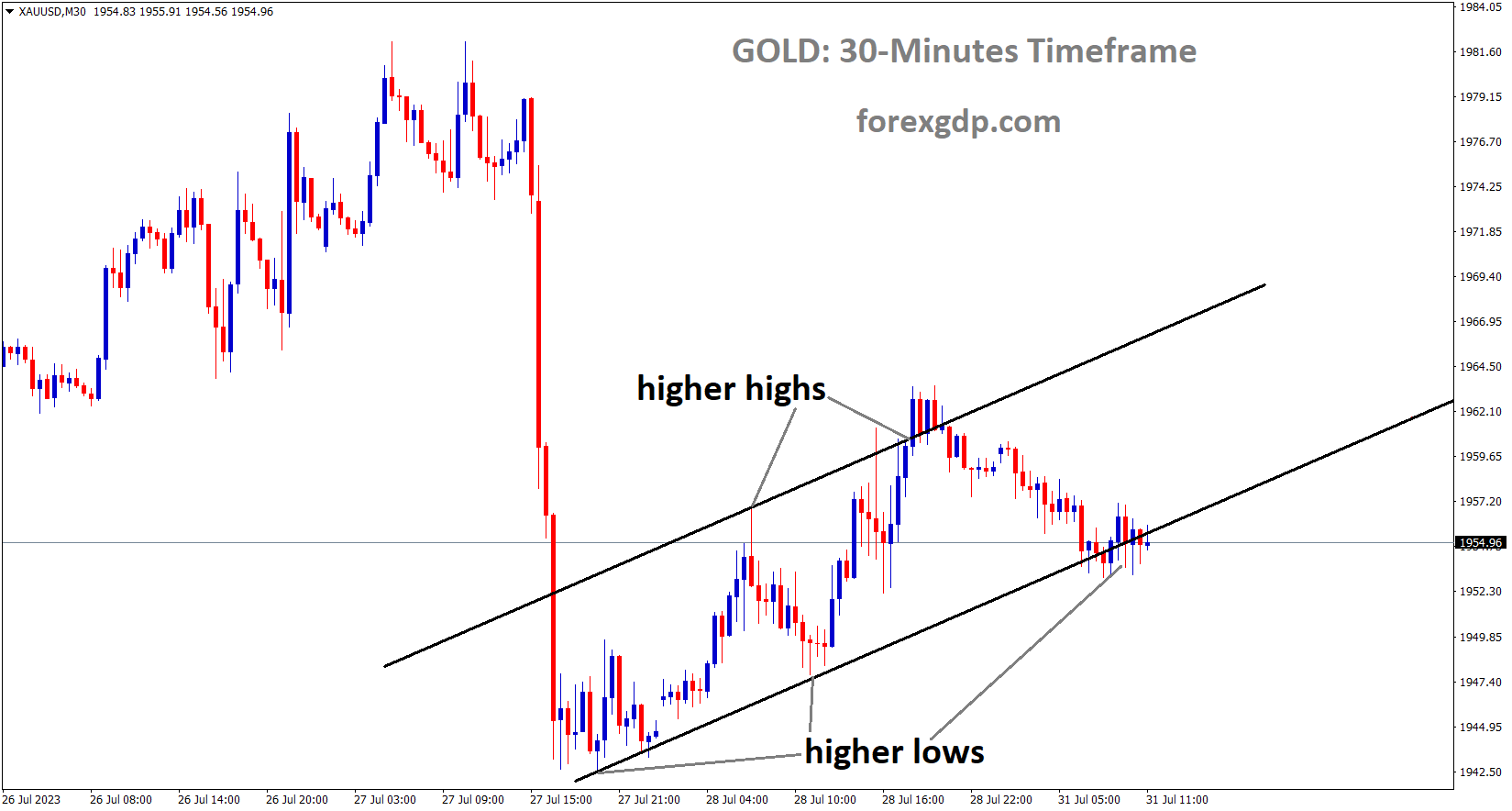

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel.

Gold prices against the USD decrease as inflation declines and central banks raise interest rates. Due to anxiety over risks in environments at the global level, demand for gold has significantly decreased. Gold prices are stable at a higher level because China only needed more stimulus, and if China performs well in COVID-19, global demand for gold will decline.

In the second half of the week, the price of gold reversed course and fell towards $1,950. TD Securities economists evaluate the prospects for the yellow metal. As it became clear that a July hike was a done deal, investors were persuaded to reduce their long exposure and increase their short exposure out of concern that the US central bank might be forced to continue on its tightening cycle, as indicated by the dots. At the same time, disproportionate increases in oil prices sparked worries that the rate of CPI depreciation may no longer be expected for the remainder of this year.

At a time when the economy continues to surprise to the upside, higher energy and grain prices as a result of Russia blocking shipping lanes suggest that the risk of higher-than-expected rates is real. This mentality, along with statements from Mr. Powell that the monetary policy will depend on data, has recently pushed Gold down to technical support near $1,950. Gold will remain under pressure as long as data remains solid and other central banks keep tightening; only a material deterioration in economic conditions would be a catalyst for a material move higher.

USDCAD Analysis

USDCAD is moving in an Ascending triangle pattern and the market has reached the resistance area of the pattern.

Canadian GDP for June decreased by 0.20% month over month but increased by 0.30%. Recent production reductions by Saudi Arabia help to support oil prices. Following the publication of encouraging domestic data last Friday, the Canadian Dollar increased against other currency pairs.

Prior to Monday’s European session, USDCAD drops to 1.3230, resetting its intraday low. The recent decline in the Loonie’s value may be related to both the US Dollar’s placement in this week’s top-tier and the price recovery of WTI crude oil, Canada’s largest export earner. The Canadian Dollar (CAD), also known as the Loonie, is getting ready for Friday’s release of the top-tier Canada employment report, which strengthens the downside bias. The market is also consolidating at the end of the month. Despite this, WTI crude oil bounces back from its intraday low of $79.95 to $80.25 by the time of publication, recording its first daily loss in three days. As a result, the black gold boosts expectations for increased energy demand as a result of China’s stimulus programme, one of the world’s largest oil consumers. The expectation that Saudi Arabia will extend its production cuts may also be driving up the price of black gold. In other news, on Friday, the Canadian GDP for June increased to 0.3% MoM from previously revised downward figures of 0.1%, which contrasts with the dismal US Core Personal Consumption Expenditure (PCE) Price Index for June to give the USDCAD bears some hope. Neel Kashkari, president of the Federal Reserve Bank of Minneapolis, raised concerns about job losses and slower growth during the weekend interview, which prompted the Fed’s doves and weighed on the value of the Loonie pair.

Crude Oil Analysis

Crude Oil price is moving in the Descending channel and the market has reached the lower high area of the channel.

It should be noted that positive Manufacturing PMI figures for July from China and announcements of stimulus measures to increase consumer demand should be taken into consideration. combined waning hawkish bets on the major central banks to encourage optimism in the markets and weigh the US Dollar. In this environment, the US Dollar Index licks its wounds close to the three-week high of approximately 101.70–80, and the S&P500 Futures remain mediocre at 4,605 after briefly touching the yearly high last week. However, as of the time of publication, US Treasury bond yields are rising. In the near future, as traders get ready for the monthly employment data from the US and Canada, the USDCAD pair could experience further decline. The US ISM Manufacturing and Services PMIs for July are also significant.

USD Index Analysis

USD index is moving in the Descending triangle pattern and the market has rebounded from the horizontal support area of the pattern.

In June’s data, the US Core Personal Consumption expenditure reading came in lower than anticipated, making the US Dollar slightly less strong against other currency pairs. In June, PCE data show 4.1% YoY, compared to an expected 4.2% and a prior reading of 4.6%. Due to the FED’s rate hike last week and the higher-than-expected Q2 GDP numbers, the US Dollar is stronger against other currency pairs.

In the early hours of Monday in Asia, the US Dollar Index (DXY) is trading aimlessly around 101.70. The Federal Reserve is the subject of conflicting concerns in the market, which is reflected in the greenback’s index against the six major currencies. The cautious mood ahead of this week’s US ISM PMIs for July and the US jobs report for the same month, which includes the headline Nonfarm Payrolls, is another factor that is testing the DXY bulls after a two-week uptrend. The most recent easing in US inflation clues and expectations of Chinese stimulus can be linked to the market’s risk-on attitude. However, according to Bloomberg, China’s State Council Information Office hinted at expectations of a new stimulus announcement from Beijing by announcing an unexpected press conference at 07:00 AM GMT. According to the news, additional measures to increase consumption will be announced at the scheduled media conference, which will also feature Li Chunlin, China’s vice chairman of the National Development and Reform Commission, as well as representatives from the Ministries of Industry and Information Technology, of Commerce, and of State Administration for Market Regulation.

The Core Personal Consumption Expenditure (PCE) Price Index, the preferred inflation gauge of the US Federal Reserve, eased to 4.1% YoY for June compared to 4.2% expected and 4.6% previously, according to US data released on Friday. Additional information showed that Personal Income decreased to 0.3% from 0.5% expected and prior readings, while Personal Spending increased by 0.5% from 0.4% market expectations and 0.1% prior. In addition, the final readings of the Michigan Consumer Sentiment Index for July decreased from initial estimates of 72.6 to 71.6, and the University of Michigan’s (UoM) 5-year Consumer Inflation Expectations also decreased from 3.1% to 3.0%.Neel Kashkari, president of the Federal Reserve Bank of Minneapolis, highlighted concerns about job losses and slower growth while praising the inflation outlook in light of the pessimistic US inflation clues. The central bank’s aggressive programme of monetary tightening to contain price increases was also criticised by the policymaker.

It is important to note that the US Dollar was able to remain firmer for a second week in a row thanks to strong results for the US Gross Domestic Product Annualised for the second quarter and the US Durable Goods Orders for June. The European Central Bank’s dovish shift and emphasis on the next rate decision’s data-dependency are other factors that are likely to have favoured the US Dollar. Wall Street ended the day on a high note, and the yields and the US Dollar both declined. Even so, by the end of Friday’s trading, the US Dollar Index had posted two straight weeks of gains. It is important to note that the S&P500 Futures have posted modest gains as of press time. The US ISM PMIs and risk catalysts can amuse DXY traders in the days ahead of the US jobs report for July on Friday, which will be crucial to watch for clear directions.

EURUSD Analysis

EURUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel.

German retail sales data for June decreased from the previous reading of 0.20% to 0.80%. At a press conference, ECB President Lagarde stated that while the economic data for France, Spain, and Germany is more positive, rate increases will continue until the cost of inflation is reduced.

According to the most recent Destatis data, Germany’s retail sales MoM fell by 0.8% compared to the market consensus of -0.2% and 0.2% earlier. In June, the bloc’s retail sales decreased 1.6% annually, less than the predicted 6.3% decline and the -3.6% decline in May. Interest rates were increased by 25 basis points (bps) to 4.25% by the European Central Bank. The ECB will work to achieve a medium-term inflation target of 2%, according to President Christine Lagarde. Lagarde also stated that the most recent economic output figures from France, Germany, and Spain are very encouraging, according to Reuters on Sunday.

GBPUSD Analysis

GBPUSD is moving in an Ascending channel and the market has reached the higher low area of the channel.

Due to the economy’s greater struggles with consumer spending and business developments, the Bank of England is anticipated to raise rates by 25 basis points rather than by 50 basis points. UK inflation is being held back longer in the UK by a lack of labour and higher food prices.

Even so, UK inflation has decreased from its peak of 11.1% to 7.9%. However, rate increases are still necessary to keep inflation under control at 2%.

Investors are paying close attention to the Bank of England’s BoE monetary policy, which is evident in the Pound Sterling’s GBP directionless performance. The GBPUSD pair struggles to determine its direction as investors fret about deepening recession fears brought on by the aggressive tightening of monetary policy by the Bank of England. The BoE is anticipated to raise interest rates for the fourteenth consecutive time in order to control stubborn inflation. The Bank of England already increased interest rates to 5%, and another increase of 25 basis points bps is anticipated to increase inflationary pressure. High food prices and labour shortages continue to be major factors in the UK’s persistent inflation. Given that the UK economy is experiencing the highest inflationary pressures among the G7 nations, BoE policymakers are also anticipated to consider raising interest rates by 50 basis points. As investors wait for more direction from the Bank of England’s interest rate policy, the pound sterling remains rangebound below 1.2900. As they are dedicated to getting inflation to 2%, BoE policymakers are anticipated to talk about further policy tightening. More interest rate increases are possible because the United Kingdom’s economy is experiencing inflationary pressures that are significantly different from the target rate of 2%.

The UK Consumer Price Index CPI headline and core data are at 7.9% and 6.8%, respectively, and will take enough time to ease to the desired rate. From its peak of 11.1%, headline inflation has decreased to 7.9%, but recent increases in the price of oil have increased concerns about a resurgence of inflationary pressures. Due to higher service costs and a tight labour market, core inflation is still close to a 31-year high of 7.1%. Recently, industry regulators and the BoE and UK authorities discussed ways to prevent overcharging customers in order to reduce the burden on households and anchor inflationary pressures. To better combat inflationary pressures, UK delegates decided to expand their arsenal of inflation-controlling measures. Despite worries about a recession deepening, the BoE is anticipated to increase interest rates one more time by 25 basis points to 5.25%.

According to a Reuters poll, the UK economy’s interest rates will peak around 5.75%. Last week, UK Treasury advisors remained concerned about the escalating recession worries brought on by the BoE’s aggressive tightening of monetary policy. As China’s official Manufacturing PMI declines for the fourth consecutive month amid weak demand, the market’s attitude becomes cautious. The economic data came in 10 basis points higher than anticipated at 49.2. A contraction is a number less than 50.0. The US Dollar Index DXY is close to 102.00 as expectations of additional interest rate increases from the Federal Reserve Fed are stoked by the positive performance of the US economy in the April–June quarter. The US Gross Domestic Product GDP increased by 2.4% in Q2 due to a tight labour market and stronger consumer spending momentum. In contrast to expectations of 1.1% and the Q1 report of 1.2%, the US Labour Cost index for Q2 fell to 1.0% on Friday. This could eventually lessen price pressures and retail demand. Investors are currently getting ready for the release of the US ISM Manufacturing PMI data on Tuesday at 14:00 GMT. It is anticipated that the economic data will keep contracting.

GBPCHF Analysis

GBPCHF is moving in the Box pattern and the market has reached the resistance area of the pattern.

SNB A loss of 13.20 billion Swiss Francs was reported for the second quarter by Swiss National Bank. This is primarily due to Global Bank’s rate increases, which have decreased the value of the SNB’s bond holdings, with bond losses totaling $8.0 billion and a loss in gold holdings of $3.14 billion.

The Swiss National Bank SNBN.S reported a second quarter loss of 13.20 billion Swiss francs on Monday as the value of its enormous bond holdings was negatively impacted by interest rate increases by other central banks. Bond prices dropped as investors feared further interest rate increases by the U.S. Federal Reserve, the European Central Bank, and others. As a result, the Swiss National Bank lost 8.08 billion francs on its 742 billion franc foreign currency positions. The value of the 1,040 tonnes of gold held by the Swiss central bank decreased due to the lower price of the precious metal during the three months leading up to the end of June, resulting in a loss of 3.14 billion francs.

AUDUSD Analysis

AUDUSD is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

Australia’s dollar rose against the US dollar today as a result of China’s Manufacturing PMI, which came in at 49.3 versus 48.9 expected. Tomorrow’s RBA meeting is scheduled, and most economists anticipate no changes as a result of the Australian economy’s weakening retail sales and inflation data.

After the Chinese manufacturing PMI beat expectations, the Australian Dollar initially increased before reversing course and returning to its previous level. The information seems to have given rise to some hope that the second-largest economy in the world might be able to ignite growth as it emerges from the pandemic era. Chinese manufacturing PMI for May came in at 49.3 versus the expected 48.9, and the non-manufacturing component registered at 51.5 versus the anticipated 53.0. As a result, the composite PMI reading decreased from 52.3 to 51.1.

Due to the broader implications for economic activity, the manufacturing PMI tends to receive more attention from the market. A survey of 3,000 manufacturers across China, mostly large businesses, produced the China PMI indices. Since it is a diffusion index, a reading above 50 is considered to be favourable for the Middle Kingdom’s economic outlook.

AUDJPY Analysis

AUDJPY is moving in the Descending channel and the market has reached the lower high area of the channel.

At its monetary policy meeting last week, the Bank of Japan kept interest rates steady and the yield curve under control, which made the US dollar and other major currency pairs stronger against the Japanese yen.

The BOJ maintained the +/- 0.5% band around the JGB 10-year yield at its meeting on Friday, with a yield target of roughly 0%. To signal its willingness to allow the JGB 10-year yield to briefly rise above the 0.5% upper bound, the Japanese central bank changed the rate at which it offers the fixed-rate purchase operations for consecutive days from 0.5% to 1.0%. the YCC tweak is probably not viewed as a monetary tightening signal but rather as managing the yield curve framework sustainably in an environment of rising global yields. The BOJ is committed to keeping broader policy settings unhanged until it achieves 2% inflation target in a stable and sustained manner.

Firms continue to raise the prices of output in accordance with global risks, according to the Quarterly Forecast of Inflation report released by the Bank of Japan. To make up for the rising costs of output, wages must rise concurrently.

The Bank of Japan BoJ stated in its full quarterly outlook report that “Japan’s core consumer inflation is likely to gradually slow towards year-end. After that, inflation is likely to pick up, but the future is uncertain. High levels of uncertainty exist regarding the global economic outlook, with risks leaning to the negative. Must be alert to the fact that price increases have spread quickly among businesses and sectors that in the past had been wary of raising prices. Must keep an eye on whether price increases to pass on costs continue and grow. As more businesses become receptive to wage increases, it is important to consider whether and how this will impact price developments.

NZDUSD Analysis

NZDUSD is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

NZ This week’s deadlines for business confidence data and Q2 employment data are both on Wednesday. The RBNZ held its interest rate at 5.50% on July 12 of this month, and it is anticipated that it will do so again in August.

In the early Asian session, the NZDUSD pair oscillates within a constrained range. The US Dollar’s general strengthening in response to the robust US Q2 Gross Domestic Product GDP and June Durable Goods Orders data helped to support the decline in the New Zealand dollar. NZDUSD is currently up 0.11% on the day, trading around 0.6155. According to a report released on Friday by the US Bureau of Economic Analysis, the Personal Consumption Expenditures PCE Price Index fell from 3.8% in May to 3% in June. The market expected this report to increase by 3.1%, but it did not. The Core PCE Price Index, the Federal Reserve’s preferred inflation indicator, came in at 4.1% annually, below market expectations of 4.2% and down from 4.6% in May. Personal Spending and Personal Income both increased month over month by 0.3% and 0.5%, respectively.

However, on July 12, the Reserve Bank of New Zealand RBNZ kept the official cash rate OCR at its previous level of 5.50%, causing the Kiwi to lose more ground. On Wednesday, market participants will pay close attention to the Q2 employment data. The unemployment rate in New Zealand is still at an all-time low. At its upcoming monetary policy meeting in August, the RBNZ is likely to keep interest rates at 5.5% unless labour market conditions deteriorate. Later in the day, the New Zealand ANZ Activity Outlook for July and the ANZ Business Confidence report are due. On Wednesday, data on the labour market will be released in New Zealand. Investors will pay close attention to US employment statistics. This week’s releases include the JOLTS Job Openings report, ADP Private Employment, Weekly Jobless Claims, and Unit Labour Cost. The Nonfarm Payrolls report, which is due on Friday, is the main event of the week. With the unemployment rate remaining at 3.6%, 180,000 new jobs should have been created by the economy. The NZDUSD pair may now have a clear direction thanks to these data.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/