XAUUSD Analysis

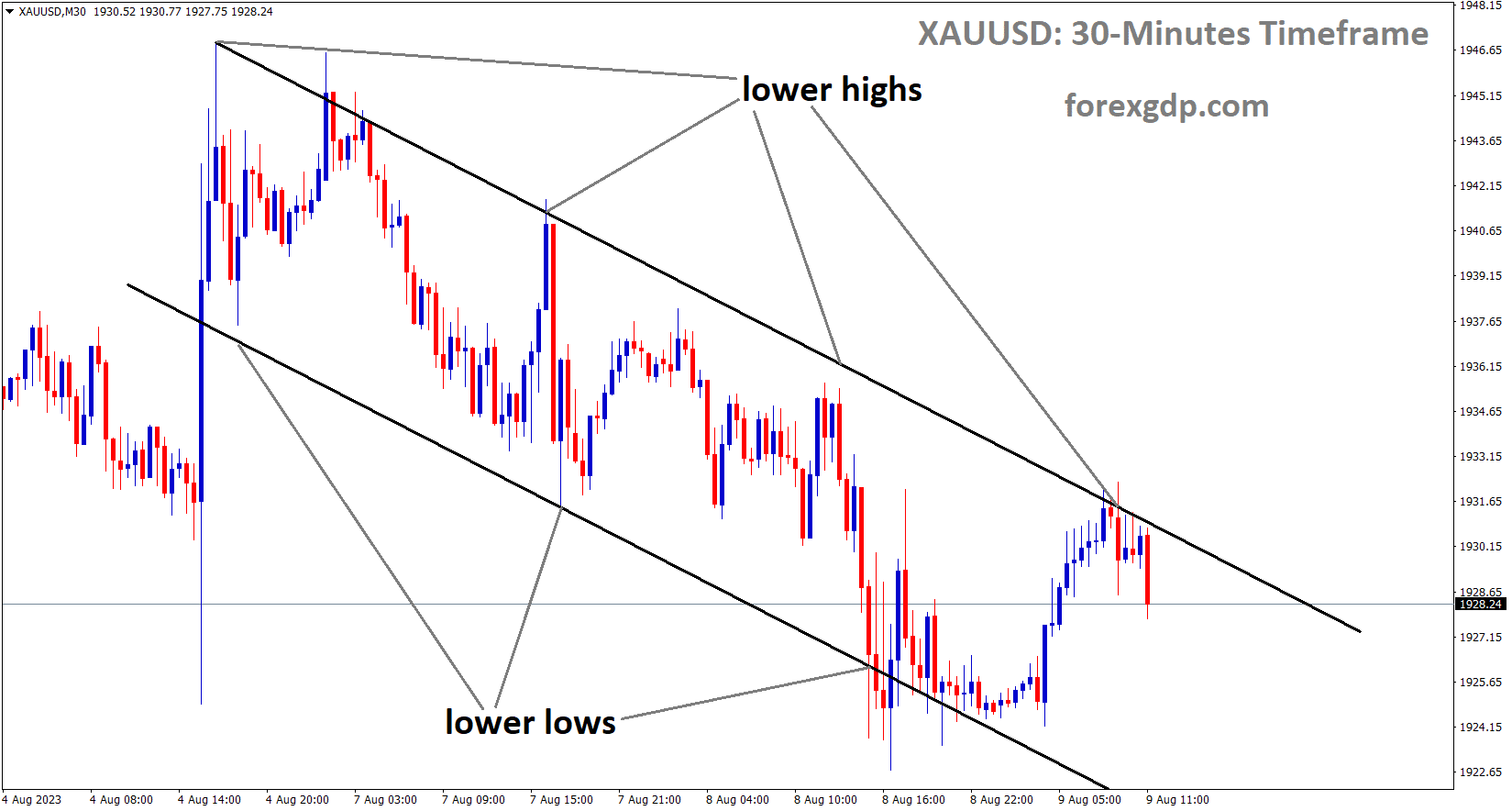

XAUUSD Gold price is moving in the Descending channel and the market has fallen from the lower high area of the channel.

Gold buyers are disappointed by China’s dismal CPI data, and the US has restricted US investments in China, which provided 50% of the revenue for Chinese companies.

In the early hours of Wednesday’s Asian session, Gold Price XAUUSD, which has fallen to its lowest point in a month, poked an upward-sloping support line from February at around $1,925. This explains the stronger US Dollar and the market’s recent worries about the banking and real estate sectors before the most important inflation cues from China and the US. The previous day, the gold price experienced its largest daily loss in a week as a result of volatile market sentiment brought on by unfavourable concerns about China, as well as the larger baking and real estate sectors. Additionally, the US Dollar was able to maintain its strength and put pressure on the price of XAUUSD due to worries sparked by Italy’s unexpected tax increase and generally positive US data. In contrast, the NFIB Optimism Index for July increased to 91.9, the highest level in nine months, from 91.0 previous readings and 90.6 market forecasts. On Monday, the US Goods and Services Trade Balance for June came in at $-65.5 billion, compared to $-65 billion expected and $-68.3 billion previously. In addition, the US IBDTIPP Economic Optimism for August dips to 40.3 from 41.3 in July and 43.0 market expectations, while Wholesale Inventories for June fell to -0.5% versus analysts’ expectations of reprinting the -0.3% figures. It should be noted that Patrick Harker, president of the Philadelphia Federal Reserve Bank, supported the Fed’s policy change while stating, according to Reuters, “I believe we may be at the point where we can be patient and hold rates steady and let the monetary policy actions we have taken do their work.” On the other hand, Thomas Barkin, president of the Richmond Fed, said that the GDP was still strong.

XAGUSD Analysis

XAGUSD Silver Price is moving in the Descending channel and the market has reached the lower low area of the channel.

When it comes to risk factors, China’s headline Trade Balance improves in July, but the details show declining Imports and Exports for the same month, pointing to the Dragon Nation’s economic challenges as it already struggles with geopolitical issues. Despite this, India has stopped importing laptops and computers and now forbids the manufacture of drones using Chinese equipment. Furthermore, according to Reuters, Chinese real estate behemoth Country Garden reported missing $22.5 million worth of two dollar bond coupons that were due on August 6. Even though Country Garden has a 30-day grace period to avoid such hardships, the news revives fears of bankruptcy among Chinese realtors. Concerns about rating juggernaut Moody’s downgrading to nine US banks, joining Fitch Ratings’ downgrading of cutting the credit rating and warning about the outlook of a few US financial institutions, also stoked new worries about the banking industry. However, the Euro is under pressure to fall and the US Dollar is allowed to stay firmer as a result of Italy’s announcements of a windfall tax on bank profits. This in turn puts pressure on the price of gold.

In light of this, Wall Street ended the day in the red with significant losses in bank stocks, and 10-year Treasury bond yields in the US fell to a weekly low of about 3.98% before rebounding to 4.03% by the end of the day. The US Dollar Index DXY also increased to its highest level in a week before the Tuesday North American session ended at around 102.55. The release of China’s headline inflation data, which includes the Producer Price Index PPI and Consumer Price Index CPI, is scheduled for today, which could make the Asian trading for gold more interesting. In spite of this, the CPI is predicted to show deflation in one of the largest markets for XAUUSD, posting -0.4% YoY figures compared to 0.0% prior, while the PPI is predicted to improve to -4.1% YoY from -5.4% prior. Given the likely weaker inflation data from China, the price of gold could continue to decline if price pressures continue to match forecasts. However, a change in market sentiment may allow the Gold bears to pause at the crucial support line.

USDCHF Analysis

USDCHF is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

The July unemployment rate in Switzerland was 1.9%, in line with this week’s published expectations. Following the peaks in respective country’s inflation, geopolitical tensions between the US and China, Japan, and Taiwan matter, and the Swiss Franc increases against Counter pairs.

At its intraday low of around 0.8735 in the early hours of Wednesday’s European session, USDCHF is still in decline. As a result of the US Dollar reversing from the crucial upside hurdle as a result of the market positioning for the crucial inflation data, as well as being supported by China news, the Swiss Franc (CHF) pair prints its first daily loss in three days. As the market’s prior risk aversion wanes, the US Dollar Index (DXY) retreats from a downward-sloping resistance line from May 31 and records its first daily loss in three days at 102.35, down 0.16% intraday. The US 10-year Treasury bond yields continue to be under pressure at the lowest level in a week marked the previous day, around 4.0% by press time, while the S&P 500 Futures recover from the monthly low marked the previous day and print modest gains around 4,525. To temper gloom about the biggest industrial players in the world, it is important to note that China’s Producer Price Index (PPI) for July improved in contrast to the dismal Consumer Price Index (CPI) data for the same month. News from the White House, which signals relief for Chinese technology companies under the Biden Administration, also increases risk appetite. According to the news, The US plans to only target those Chinese companies that get more than 50% of their revenue from industries like quantum computing and artificial intelligence (AI).

On the other hand, the unexpected tax Italy imposed on banks’ windfall profits, combined with the previous day’s downgrade of US banks and financial institutions by all major rating agencies, weighed on the risk sentiment. Concerns about the UK recession, China’s slowing economic growth, and the Dragon Nation’s geopolitical conflict with the US and Japan over Taiwan may all be on the same wavelength. The USDCHF may continue to decline given the market’s preparations for the US CPI for July, which is scheduled for release on Thursday. However, the Swiss Franc pair may be pushed in the direction of the major technical resistances by the US inflation data and the risk-off sentiment.

EURUSD Analysis

EURUSD is moving in the Descending channel and the market has reached the lower high area of the channel.

The government of Italy imposed taxes on banks’ windfall profits, causing the eurozone’s inflation expectations to slightly decline. Inflation for the next 12 months is 3.4% in June, down from the projected 3.9% in the May survey, according to the ECB. The unemployment rate is staying the same, and economic growth is expected to be slightly negative over the next 12 months.

Bears take a break after a two-day losing streak amid Wednesday’s sluggish Asian session, keeping EURUSD defensive near 1.0960. The previous day, following news from Italy that added to the general risk aversion, the Euro pair fell to its lowest level in a week. But sellers of the key currency pair appear to be encouraged by the cautious atmosphere ahead of China’s inflation and recent news stories that have tamed pessimism. The European Central Bank ECB monthly survey report’s downward revision of the inflation forecasts for the Eurozone and Italy’s announcement of a surprise windfall tax on bank profits combined to weigh on the EURUSD price the day before. According to the European Central Bank’s ECB monthly survey of consumer inflation expectations, consumer expectations for the next 12 months have decreased even more, from 3.9% in May to 3.4% in June. Expectations for economic growth over the next 12 months became slightly less negative, while the expected unemployment rate in 12 months was unchanged, the ECB survey report added.

EURCHF Analysis

EURCHF is moving in the Descending channel and the market has reached the lower high area of the channel.

However, the sentiment and the price of the EURUSD were affected by China’s trade figures and worries about the international banks. Although China’s trade balance improved in July, the details show that imports and exports declined, indicating that the Dragon Nation, which is already experiencing geopolitical difficulties, faces economic difficulties. In a similar vein, India forbids the use of Chinese equipment by drone manufacturers after previously banning the import of laptops and computers. Additionally, according to Reuters, Chinese real estate behemoth Country Garden reported missing $22.5 million worth of two dollar bond coupons that were due on August 6. Even though Country Garden has a 30-day grace period to avoid such hardships, the news revives fears of bankruptcy among Chinese realtors. Concerns about rating juggernaut Moody’s downgrading to nine US banks, joining Fitch Ratings’ downgrading of cutting the credit rating and warning about the outlook of a few US financial institutions, also stoked new worries about the banking industry. It is important to note that the mixed US data and the Fed discussions appear to nudge the EURUSD bears. While the NFIB Optimism Index for July increased to 91.9, the highest level in nine months, from 91.0 previous readings and 90.6 market forecasts, the US Goods and Services Trade Balance for June came in at $-65.5 billion compared to the $-65 billion expected and $-68.3 billion prior. In addition, the US IBDTIPP Economic Optimism for August dips to 40.3 from 41.3 in July and 43.0 market expectations, while Wholesale Inventories for June fell to -0.5% versus analysts’ expectations of reprinting the -0.3% figures.

Following the release of the data, Patrick Harker, president of the Philadelphia Federal Reserve Bank, urged the Fed to change its course, telling Reuters, I believe we may be at the point where we can be patient and hold rates steady and let the monetary policy actions we have taken do their work. On the other hand, Thomas Barkin, president of the Richmond Fed, said that the GDP was still strong. As we move forward, the July releases of China’s Consumer Price Index CPI and Producer Price Index PPI will be important for intraday directions. Forecasts indicate that while the PPI is anticipated to improve to -4.1% YoY from -5.4% prior, the CPI is predicted to signal deflation while posting -0.4% YoY figures compared to 0.0% prior. If the market’s concerns about China’s inflation numbers grow, the US Dollar may strengthen ahead of Thursday’s release of the US CPI data, which would allow the EURUSD bears to break the crucial 100-DMA support.

GBPCHF Analysis

GBPCHF is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

According to NSIER (National Social and Economic Research), Britain’s output will not reach its pre-pandemic peak until the third quarter of 2023. In four years from this year, inflation will reach the 2% target level once more. Only during the recession do polls show a 60% risk for the government.

During the sluggish markets, there are a variety of central concerns, including the UK’s economic slowdown.The National Institute of Economic and Social Research (NIESR), the top think tank in the UK, predicted earlier in the day that British output would not reach its pre-pandemic peak until the third quarter (Q3) of 2024, according to The Guardian. According to the NIESR and The Guardian, there was a 60% chance that the government would hold elections during a recession. Positively, the NIESR anticipates UK inflation to exceed the Bank of England’s (BoE) target of 2.0% for the ensuing four years, which will pressure the “Old Lady”—as the BoE is sometimes referred to—to take hawkish action and support the British Pound GBP bulls.

In other news, the 10-year Treasury bond yields in the US fell to a weekly low of about 3.98% before rebounding off 4.03% by day’s end, making rounds to the said levels recently, while the S&P500 Futures remain mildly bid around 4,520 in response to Wall Street’s negative performance. The market’s most recent stabilisation may be related to China’s mixed inflation data and the US government’s lax stance on Beijing’s ban on technology firms.

AUDUSD Analysis

AUDUSD is moving in the Descending channel and the market has reached the lower high area of the channel.

Since 2021, Chinese inflation data for year over year comparisons have been negative; for the month of July, they were -0.30% and -4.4%, respectively. The Australian Dollar is weaker against the USD as a result of China’s disappointment data.

China’s exports and imports both declined yesterday, resulting in a string of negative domestic data.

After hitting a two-month low yesterday due to a stronger US Dollar and growing worries about the outlook for its main trading partner, China, the Australian Dollar held steady today. For the first time since early 2021, the Chinese CPI was negative year over year, coming in at -0.3%. PPI also came in below expectations at -4.4% year over year through the end of July. The disappointing trade data from yesterday, which showed sharp declines in both imports and exports, is followed by today’s data. One of China’s larger companies, Country Garden, missed payments on US Dollar bond coupons, further deteriorating market sentiment. Despite a 30-day grace period, they were due over the weekend and have still not been paid as of Tuesday. Following the Politburo meeting last month, there was some optimism that Beijing would take action to fuel economic growth. Markets appear to be waiting for the Central Government to take action before they are persuaded that the second-largest economy in the world will experience a turnaround.

In any case, APAC equities had a quiet day with most indices dipping a little, with Korea’s Kospi index being the lone exception, rising more than 1%. Futures indicate that Wall Street will begin its cash session at levels that are similar to where it ended yesterday. Similar to this, Wednesday has started out with the currency markets being somewhat quiet. Mostly holding onto overnight gains, the US dollar. As this article goes to print, gold has marginally risen while crude oil has slightly declined. Here are the current prices. After falling during the North American trading day, Treasury yields are little changed today, especially for bonds with a maturity of five years or more.

According to S&P Global, Australia’s inflation will remain sticky, forcing the RBA to raise interest rates again in 2023 and 2024. When unemployment reaches a certain level, there will be negative effects on the economy and the financial system.

According to S&P Global’s most recent analysis of the Australian economy, the Australian economy may, but is not guaranteed to, manage a’soft landing’ with inflation decreasing to the RBA’s target range. The main concern is that Australia’s inflation turns out to be stickier than anticipated, necessitating a stronger interest rate increase from the RBA. In addition to a continued expansion in 2023 and 2024, we anticipate a slight increase in unemployment. Economic and financial consequences should remain under control if the increase in Australia’s unemployment rate is kept to less than one percentage point.

Reuters reported on Wednesday that the White House is reportedly outlining plans to limit some US investments in sensitive technology in China, citing a senior government source. The long-awaited executive order, according to the source, is anticipated later today. After anonymous sources told Bloomberg on Tuesday that a US plan to restrict investment in China is likely to apply only to Chinese companies that get at least half of their revenue from cutting-edge sectors like quantum computing and artificial intelligence

NZDUSD Analysis

NZDUSD is moving in the Descending channel and the market has reached the lower high area of the channel.

The Monetary Conditions Survey was conducted by the RBNZ, and two-year inflation expectations increased from 2.79% in Q2 to 2.83% in Q3. Year inflation expectations decreased from 4.28% in Q2 to 4.17% this quarter.

According to the Reserve Bank of New Zealand’s (RBNZ) most recent survey on monetary conditions, New Zealand’s (NZ) inflation expectations increased over a two-year period for the third quarter of 2023 while decreasing even more for the following year. Two-year inflation expectations increased slightly to 2.83% in Q3 from 2.79% the previous quarter, which is thought to be the time period during which RBNZ policy actions will impact prices. The average one-year inflation expectation for New Zealand in 2023 decreased further in the third quarter to 4.17% from 4.28% in the second quarter of this year.

CADJPY Analysis

CADJPY is moving in the Descending channel and the market has reached the lower high area of the channel.

Due to lower household spending in Japan and reading falling to 4.2% in June from 4.0% in May, the Japanese Yen remains weak on the market. Inflation is a global phenomenon, according to the Bank of Japan, and banks should only raise interest rates when companies’ wages start to rise.

The domestic Japanese numbers also contributed to its decline. Chinese trade data, which revealed unexpected drops in both exports and imports last month, dominated the Asian session. The figures painted a picture of a Chinese economy that was still firmly in the doldrums despite the passing of Covid and its terrible effects. They contrast it sharply with the somewhat more productive United States. Of course, there are some gaps in the data there as well, but overall, investors continue to dare to hope for a soft landing in the country with the largest economy in the world. The BoJ’s assertion that there is no need to rethink policy because inflation is an internationally generated phenomenon. The market’s immediate attention will now shift to the upcoming Wednesday inflation data from China. After registering a flat result in June, the annualised rate is predicted to have decreased by 0.4% in July. If confirmed, this will raise concerns about the need for additional stimulus measures for China’s economy.

CADCHF Analysis

CADCHF is moving in the Box pattern and the market has reached the horizontal support area of the pattern.

This week’s Canadian building permits are scheduled, and the rise in oil prices is bolstering the currency. After the FED raised interest rates last month, the US Dollar remains straight in the market.

Oil demand worries are caused by China’s poor CPI data, but the Canadian dollar remains stable.

Thet decline in the Loonie could be the weak Oil Price. To temper gloom about the biggest industrial players in the world, China’s Producer Price Index (PPI) for July showed improvement in contrast to the depressing Consumer Price Index (CPI) data for the same month. Contrarily, WTI crude oil is currently down 0.05% intraday near $82.40 and is stable within the weekly trading range of $82.00-83.00. It is important to note that the looming default of a major China realtor joins the problems with US banks to challenge the supply cuts made by OPEC and its allies, while China’s inflation data and the White House’s trade-friendly news fall flat with energy buyers.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/