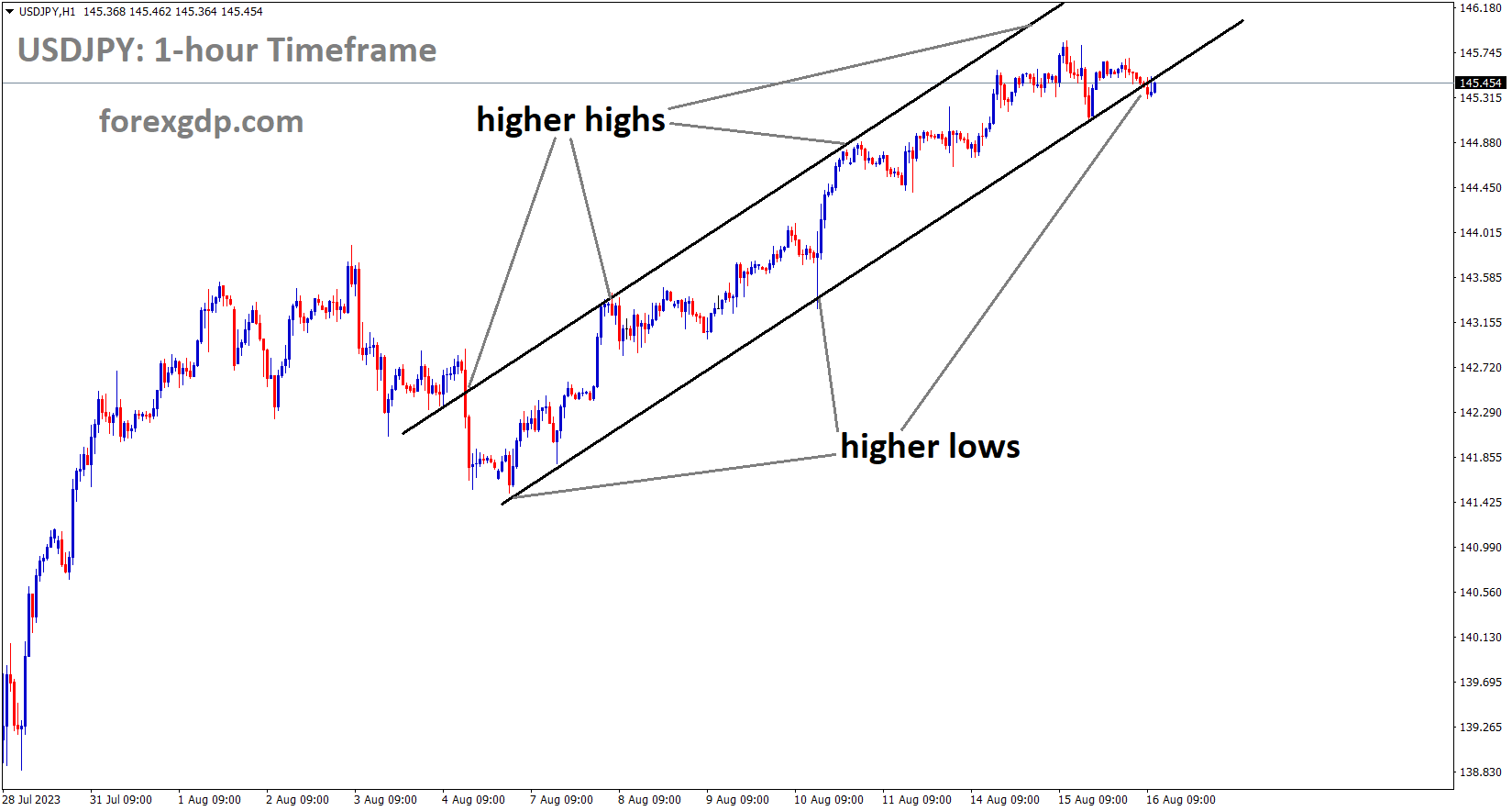

USDJPY Analysis

USDJPY is moving in an Ascending channel and the market has reached the higher low area of the channel

The US dollar strengthened following the release of retail sales data for July that showed 0.70% growth in July compared to 0.30% in June.

The US Dollar Index DXY rises above 103.00 on Wednesday as bulls maintain control despite the lack of movement during the early Asian session. Despite this, the US dollar index fell to 102.80 in the early hours of Tuesday’s trading, teasing bears. However, positive US data combined with risk aversion brought on by China helped to rouse buyers. Notably, the DXY traders have been more agitated lately due to the fear surrounding China’s market opening and the cautious attitude preceding the Federal Open Market Committee’s FOMC most recent Monetary Policy Meeting Minutes. Moreover, hawkish remarks from the Fed are another factor that has been helping the USD Index recently. President of the Minneapolis Federal Reserve Neel Kashkari recently dismissed discussions of a policy change, pointing to the high rate of inflation and the lack of confidence in the Fed’s ability to control it. According to Reuters, the policymaker also stated that he is not yet prepared to declare that rate hikes by the Fed are over. Fed’s Kashkari appeared to have rung the hawkish bells while keeping an eye on the positive US data. Tuesday saw a 0.7% MoM increase in US retail sales in July, up from 0.4% predicted and 0.3% revised from 0.2% reported in June. According to the details, the Retail Sales Control Group increased from 0.5% of the previous readouts which were revised from 0.6% to 1.0% for the same month, while the Core Retail Sales, or the Retail Sales ex Autos, grew 1.0% against 0.4% market forecasts.

Furthermore, the US Export Price Index and Import Price Index increased on a month-over-month basis in July but declined marginally on an annual basis for the same month. Meanwhile, the US NY Empire State Manufacturing Index fell to -19.0 from 1.1 prior and -1.0 market forecasts. Aside from that, analysts at the international rating company Fitch Ratings informed CNBC on Tuesday that, in response to Reuters’ report, the agency may downgrade a number of significant lenders, including JPMorgan. This would increase risk aversion and support the DXY. Above all, negative data from China and the unexpected rate cuts by the People’s Bank of China PBoC fuel economic concerns about the second-largest economy in the world and increase demand for US dollars as a safe haven. The One-year Medium-term Lending Facility MLF rate and Standing Lending Facility SLF rates were lowered by the People’s Bank of China PBOC to 2.50% from 2.65% previously, shocking the markets. Additionally, the Reverse Repo Rate was lowered from 1.9% to 1.8%. To highlight the concerns surrounding the Dragon Nation and feed the DXY, the same was combined with China’s disappointing July Retail Sales, which increased 2.5% YoY vs. 4.8% expected and 3.1% prior, and the Industrial Production, which came in at 3.7% YoY vs. 4.5% estimated and 4.4% prior. Wall Street closed lower while expressing the mood, and the yield on US 10-year Treasury bonds rose above the annual high. It should be mentioned that as of press time, the S&P500 Futures are still boring. Next, the US housing data, the Industrial Production, and China’s House Price Index for July could amuse DXY traders prior to the Fed Minutes.

According to August data from Japan’s major manufacturers, the country’s sentiment index was 12 in July compared to 3 in July, and its non-manufacturing data was 32 compared to 23. This data is supportive of the Japanese yen even though China’s economy is in jeopardy.

The latest Reuters Tankan monthly survey for August indicates that while worries about China continue to pique optimism, large manufacturing and non-manufacturing companies in Japan are feeling more upbeat. Nevertheless, the headline big manufacturers’ sentiment index for August was 12 as opposed to 3 from July, while the non-manufacturers’ sentiment index increased to 32 from 23 from July. Additional information reveals that the November big manufacturer Outlook Index was 14 while the services sector’s could have flashed the 26 mark.

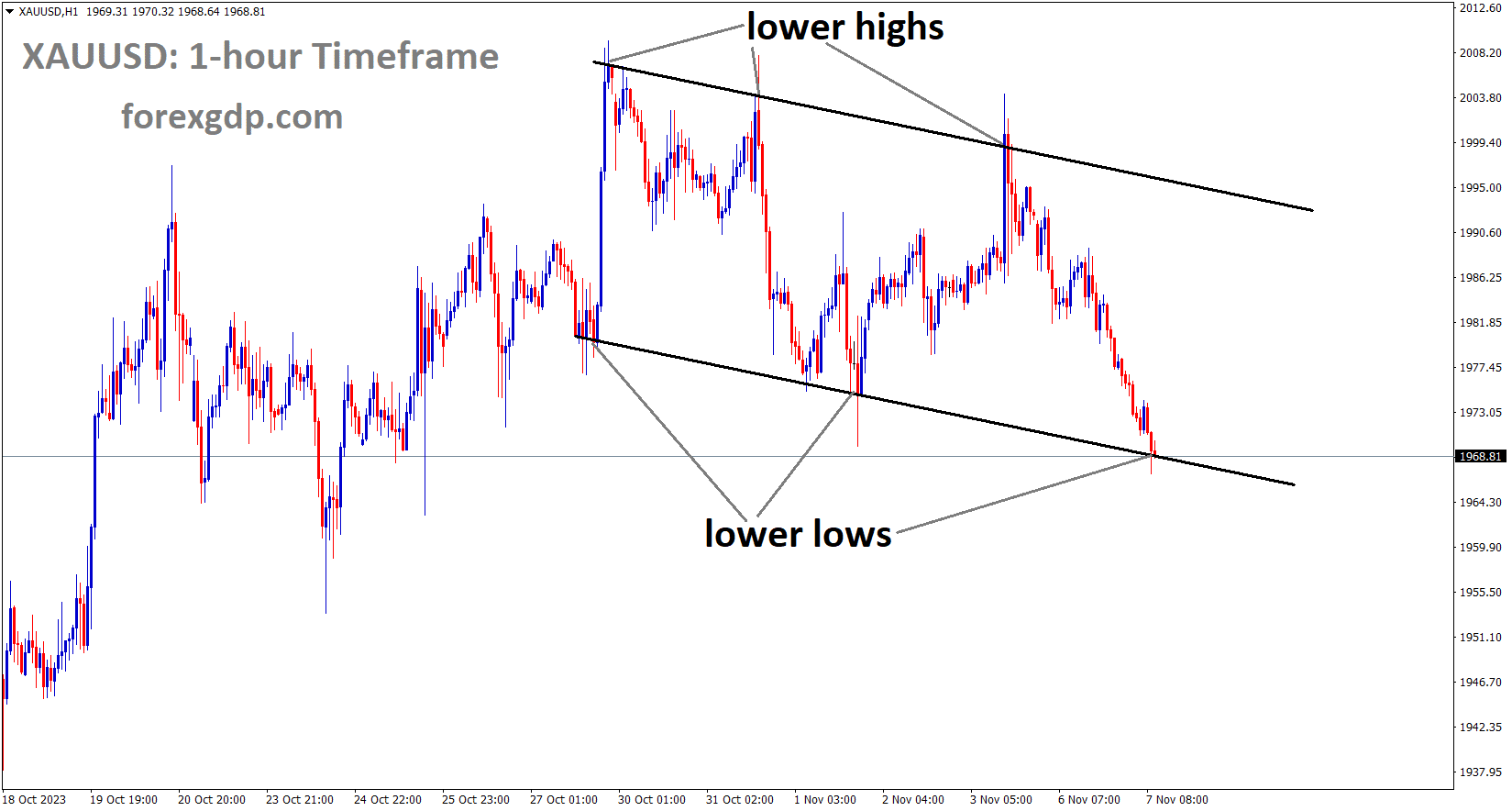

XAUUSD Analysis

XAUUSD Gold price is moving in the Descending channel and the market has fallen from the lower high area of the channel

Due to a decline in all domestic data, including retail sales and industrial production, China lowered its medium lending rates from 2.65% to 2.50%. Pressure to sell gold increases after China lowers lending rates.

In the early hours of Wednesday’s Asian session, the gold price XAU/USD is under pressure at $1,901, reversing late Tuesday’s corrective bounce off the lowest level in seven weeks amid a cautious outlook. However, the prior day’s sentiment and the XAU/USD were affected by China-induced risk aversion, positive US data, hawkish Federal Reserve Fed remarks, and worries about seeing credit ratings downgrades of significant US corporations. Nevertheless, early on Tuesday, during the market’s consolidation leading up to today’s Federal Open Market Committee FOMC minutes for the Monetary Policy Meeting, gold prices began to rise again. Even though there was a brief uptick the day before, the Federal Reserve Fed official’s hawkish remarks coupled with stronger US retail sales data and market gloom are keeping the gold price permanently on the bear’s radar. Tuesday’s negative data from China and the unexpected rate cuts by the People’s Bank of China PBoC raised concerns about the second-largest economy in the world and affected the price of gold. The One-year Medium-term Lending Facility MLF rate and Standing Lending Facility SLF rates were lowered by the People’s Bank of China PBOC to 2.50% from 2.65% previously, shocking the markets. Additionally, the Reverse Repo Rate was lowered from 1.9% to 1.8%. To highlight the concerns surrounding the Dragon Nation and feed the DXY, the same was combined with China’s disappointing July Retail Sales, which increased 2.5% YoY vs. 4.8% expected and 3.1% prior, and the Industrial Production, which came in at 3.7% YoY vs. 4.5% estimated and 4.4% prior.

XAGUSD Analysis

XAGUSD Silver price is moving in an Ascending channel and the market has reached the higher low area of the channel

Conversely, US retail sales increased by 0.7% MoM in July as opposed to the 0.4% predicted and the revised 0.3% reported in June. According to the details, the Retail Sales Control Group increased from 0.5% of the previous readouts which were revised from 0.6% to 1.0% for the same month, while the Core Retail Sales, or the Retail Sales ex Autos, grew 1.0% against 0.4% market forecasts. Furthermore, the US Export Price Index and Import Price Index increased on a month-over-month basis in July but declined marginally on an annual basis for the same month. Meanwhile, the US NY Empire State Manufacturing Index fell to -19.0 from 1.1 prior and -1.0 market forecasts. Neel Kashkari, the president of the Minneapolis Federal Reserve, dismissed discussions of a policy change late on Wednesday, citing high inflation and the lack of confidence in the Fed’s ability to control it. According to Reuters, the policymaker also stated that he is not yet prepared to declare that rate hikes by the Fed are over. Aside from that, analysts at the international rating company Fitch Ratings informed CNBC on Tuesday that, in response to Reuters’ report, the agency may downgrade a number of significant lenders, including JPMorgan. This would strengthen risk aversion and benefit gold sellers.

As a result, even though the US Dollar Index DXY recently tested the important resistance level at 103.30, Wall Street ended the day lower than expected, and the yield on the US 10-year Treasury bond rose to a new all-time high. It should be mentioned that as of press time, the S&P500 Futures are still boring. As the price of gold prods the important short-term technical supports, it braces for more declines in the future. The Federal Reserve Fed monetary policy meeting minutes, China data, bond yields, and other factors must all be considered when validating the XAU/USD bears. If the concerns regarding China persist and interest rates continue to rise, supported by hawkish remarks in the Fed Minutes, the price of gold could fall to below $1,900.

USDCHF Analysis

USDCHF is moving in the Box pattern and the market has fallen from the Horizontal Resistance area of the pattern

The data on import and export prices from Switzerland for the month of July was -0.60%, compared to 0.50% the previous month. As anticipated, SNB would like to hike by 25bps at the upcoming meeting to reach the 2% target.

In the early Asian trading session on Wednesday, the USDCHF trades in a narrow trading band between 0.8745 and 0.8800. Consolidating its recent gains, the US Dollar Index DXY, which compares the value of the USD against six other major currencies, is currently trading at 103.20. The US retail sales figures exceeded forecasts, according to the economic data that was made public on Tuesday. The headline number increased by 0.7% MoM, exceeding the 0.4% forecast. Sales that did not include the automobile sector were 1% as opposed to the predicted 0.4%. Finally, the August NY Empire Manufacturing Index dropped from -1 to -19. Neil Kashkari, the president of the Federal Reserve Fed in Minnesota, said that although inflation has decreased, it is still too high. Regarding the uncertainty over whether the Fed has done enough or needs to do more, Kashkari brought it up.

Regarding the Swiss franc, the YoY change in Swiss Producer and Import Prices for July was -0.6%, as opposed to the predicted 0.5%. Monthlyly, the figure shrank to 0.1% from 0% previously. In its September meeting, the Swiss National Bank SNB is expected to raise interest rates by 25 basis points bps to 2%, according to Bloomberg. In addition, the headlines surrounding the US-China relationship continue to be prominent. US investors are worried Beijing may retaliate or stop buying US technology in response to President Joe Biden’s decision to limit some US technology investments in China. The safe-haven Swiss franc may gain from the renewed trade tension, which would be negative for the USDCHF pair. And now for Wednesday’s releases: US Building Permits, Housing Starts, and Industrial Production. The main event this week, though, will be the FOMC minutes. Using the data as a guide, traders will look for trading opportunities around the USDCHF pair.

USDCAD Analysis

USDCAD is moving in the Descending channel and the market has reached the lower high area of the channel

The rate of inflation in Canada was (YoY) July is 3.3%, up from 2.8% in June and 3.0% in the forecast. However, despite US retail sales data being higher than anticipated the previous day, the data did not cause the Canadian dollar to rise.

The Canadian inflation number for today was anticipated to serve as a trigger for the CAD bulls to resume their rally, and it did not dissapoint. Even though the core inflation rate was within expectations, both the MoM and YoY prints showed higher-than-expected inflation. Because of the base-year effect, energy prices decreased less (-8.2% vs. -14.6%), mostly because of petrol (12.9% vs. -21.6% in June). Electricity costs also increased more quickly (11.7% vs. 5.8%).

CADCHF Analysis

CADCHF is moving in the Box pattern and the market has rebounded from the Horizontal Support area of the pattern

The largest contributor to headline inflation continues to be the mortgage interest cost index (+30.6%), which posted another record year-over-year gain. There has been a decrease in food prices, which is good news for consumers as sticky prices are being experienced in other developed markets as well.

The first response to the Canadian inflation print was tempered by the positive surprise of the US retail sales data. Later in the session, there are also some Fed speakers scheduled, which could increase volatility and possibly boost the dollar once more.

EURCHF Analysis

EURCHF is moving in the Box pattern and the market has rebounded from the Horizontal Support area of the pattern

Euro economic expansion is anticipated. slowdown from 1.1% in the first quarter to 0.60% in the second. The ECB raised rates earlier than anticipated, and another rate hike is not anticipated until mid-2024.

Prior to the release of the FOMC minutes and the GDP data for the Euro area, the euro is testing important levels against some of its competitors.The impact of aggressive ECB rate hikes is likely to blame for the Euro area’s economic growth slowing to 0.6% on-year in the April–June quarter from 1.1% in the prior quarter due to tighter credit conditions. The Economic Surprise Index (ESI) for the Euro area is slightly above three-year lows, which is indicative of the unimpressive macro data. Even though investor confidence in Germany unexpectedly increased in August, a sustained recovery in the EUR is unlikely unless the economic growth outlook reverses, particularly when compared to the US. The EUR has been relatively strong compared to other currencies, indicating stable expectations for ECB rates through the middle of 2024.

GBPUSD Analysis

GBPUSD is moving in the Descending channel and the market has reached the lower high area of the channel

The UK’s CPI data for July was 6.8%, down from 7.9% in June. This is the lowest level since February 2022. The UK’s Chancellor, Jeremy Hunt, stated that we have implemented measures that are effectively regulating inflation rates.

The Office for National Statistics ONS released its most recent data on Wednesday, indicating that the annual Consumer Price Index CPI for the United Kingdom increased by 6.8% in July, down from a 7.9% increase in June. Although the print met the market’s prediction of a 6.8% increase, it was the lowest level since February 2022. The Core CPI index, which does not include volatile food and energy items, grew 6.9% YoY in the reported month, exceeding estimates of a 6.8% clip but falling short of the 6.9% increase observed in June. In July, the UK Consumer Price Index decreased by 0.4% month over month as opposed to the previously observed 0.1% increase and the -0.5% predicted. In July, the UK Retail Price Index RPI was 9.0% YoY and -0.6% MoM. UK Finance Minister Jeremy Hunt stated, The decisive action we have taken to tackle inflation is working, in response to the country’s inflation data. Price rises are slowing, but we are not at the finish line, he quickly added. Wednesday, August 16, marks the release of the crucial Consumer Price Index CPI data from the United Kingdom UK. In August, the Bank of England BoE increased its policy rate by 25 basis points to 5.25%; however, during the press conference held after the meeting, Governor Andrew Bailey did not pledge to tighten policy any further. Developments in UK inflation may have an impact on the BoE’s rate outlook as well as the value of the pound sterling.

The BoE revised down its inflation forecasts in the most recent projections. The bank has revised its forecast for inflation, which calls for it to drop from 5.12% in May to 4.93% in the fourth quarter of 2023. It also sees inflation falling to 2.82% in a year from 3.38% in May. Speaking to reporters about the inflation outlook, Bailey stated that they anticipated inflation to drop to roughly 5% in October. However, the governor of the Bank of England added that since May, there has been unwelcome news regarding the inflation of services prices. The basic wage inflation, as determined by the change in Average Earnings Excluding Bonus, reached a new record growth rate of 7.8% in the three months leading up to June, according to data from the UK released on Tuesday. However, during that same time frame, the unemployment rate increased from 4% to 4.2%. Following these readings, the rate-sensitive 2-year UK Gilt yield began to rise, underscoring the effect of hawkish bets by the Bank of England. The headline annual UK Consumer Price Index inflation rate is predicted by economists to drop from 7.9% in June to 6.8% in July. The Core CPI is expected to decrease slightly from 6.9% to 6.8%. Britain’s CPI inflation is expected to decrease by 0.5% on a monthly basis, after growing by 0.1% in June.

The Bank of England’s monetary policy could be affected by the upcoming UK inflation data, according to analysts at Societe Generale. “With our expectation that core inflation remains unchanged at 7.1% in June, coupled with the continued acceleration in wage growth in the past week, it should keep the Bank hiking,” the analysts add. However, it is less certain whether the Bank will downshift to 25bp or hikes by an additional 50bp, as any surprise to the upside or downside in the CPI data could influence the Bank’s decision. In light of the expectation that more solid indications that the labur market is cooling will gradually accumulate, our prediction is for a downshift to 25bp.

We anticipate that by the end of the week, the unfavourable mortgage rate environment will have a negative impact on retail sales and consumer confidence. After the most recent jobs report, markets are almost fully pricing in a further 25 basis points bps of rate hikes by the BoE in September. Investors may begin to anticipate a 50 basis point increase, though, if the monthly CPI shows positive growth. In that case, Pound Sterling might become more formidable against its competitors. Conversely, if CPI data come in close to expectations and indicate a loosening of price pressure, investors are probably going to back off from wagering on a significant hike in the BoE rate. Even so, it will likely take a significantly lower-than-expected UK inflation reading for market players to wager on the BoE key rate remaining unchanged in September. Therefore, the way the market is positioned, unless there is a big negative surprise, Pound Sterling’s losses may stay contained.

AUDUSD Analysis

AUDUSD is moving in the Box pattern and the market has rebounded from the Horizontal Support area of the pattern

Rate hikes are not expected until the economy expands, according to the minutes of the RBA meeting; data-based rate hikes are anticipated in future meetings. The result of the RBA meeting demoralised the Australian dollar relative to other currencies.

The cash rate will remain at 4.1%, per the Reserve Bank of Australia’s decision. The Reserve Bank of Australia is giving the impression that interest rates may be on hold for some time, which is unusual given that it started raising rates more than a year ago. The phrase some further tightening of monetary policy may be required is no longer present. Rather, the Reserve Bank of Australia RBA is speaking more ambiguously about whether or not a further increase in interest rates is required in its most recent board minutes. Key indicators of the economy, such as declining spending, a softening labour market, and a deepening downturn in growth, indicate why the tone of the economy has changed. Consumer confidence is at recessionary lows, retail sales volumes have declined for three straight quarters, and modern indicators such as Commonwealth Bank’s Household Spending Insights index indicate a weakening of discretionary spending. Activity is being adversely affected by the slowdown in consumption, as the central bank has projected that the GDP will contract to just 0.9% by the end of the year.

Inflation is declining as a result. The previous quarter saw a decline in annual growth from a peak of 7.8% late in the previous year to 6%. The labour market is not progressing as quickly as other areas of the economy, and the unemployment rate is still at a 50-year low of 3.5%. Yet, this is also where the consequences of high net migration and slowing growth are beginning to manifest. The rate of underemployment is increasing, and companies have reported to the RBA that hiring new employees is becoming simpler. The Reserve Bank claims to be seeing the first indications of a shift in the labour market. A growing number of people are also concerned that China may be about to enter a period of deflation. The Asian country is Australia’s main trading partner, and the country’s need for commodities has kept the economy from going into recession during the pandemic and global financial crisis. A number of factors working together have increased central banks’ confidence that inflation is declining. However, up until now, the question has been whether it is falling quickly enough. The RBA has been worried about the possibility that inflation may not be declining quickly enough for the majority of this year, which increases the possibility that decisions about business pricing and worker wages will be influenced by higher inflation expectations.

The central bank is increasingly concerned that additional rate increases may dash hopes of keeping the unemployment rate low. This seems to be a shift in the balance of concerns. The RBA board warned that it would be very difficult to preserve the gains made in employment if interest rates had to rise by more than otherwise in order to reduce inflation. In order to emphasise its more cautious stance on interest rates, the central bank has started to speak of monetary policy decisions as being made over the months ahead rather than as being decided month to month. Rates are currently expected to remain on hold for some time, according to many economists, with some predicting a reduction in March or April of next year. Stephen Halmarick, chief economist at Commonwealth Bank, predicted that three rate cuts by the end of the following year will precede the official cash rate’s mid-2025 settlement at 2.6%. This rate cut is expected to occur in March 2024.

NZDUSD Analysis

NZDUSD is moving in the Box pattern and the market has reached the Horizontal resistance area of the pattern

Today, the RBNZ maintained rates at 5.50%, with the CPI exceeding the 1-3% target area by 6.0%. The economy is struggling in all domestic areas, so this month’s tightening has been stopped, and the rate will remain paused until the economy expands.

Before today’s Reserve Bank of New Zealand (RBNZ) meeting, the NZD had dropped to a 10-month low, but it quickly rose as the bank decided to hold rates steady at 5.50% during the monetary policy committee (MPC) meeting. The current CPI for New Zealand is 6.0%, significantly higher than the 1% to 3% target range. The monetary policy statement (MPS), which the market perceived as being more hawkish than anticipated, seems to have taken Kiwi bears by surprise given the strength of the US dollar prior to the meeting. A 50/50 chance of a 25 bps hike in early 2024 is currently priced into the overnight index swap (OIS) market, while the official cash rate (OCR) stays 525 basis points (bp) above the pandemic low. They had stopped pricing in any more hikes for this cycle prior to today’s meeting. The currency might have been supported by this inclination in the interest rate market.

It was widely expected that the RBNZ would hold rates today. The bank had increased the overnight cash rate (OCR) twelve times since its initial increase in October 2021 before the July pause. Prior to today’s decision, the S&P/NZX 50 equity index for New Zealand hit a 7-week low, and since then, it has had difficulty recovering. Following the North American session, sentiment towards risk and growth-oriented assets had already soured heading into today’s APAC session. Wall Street fell more than 1% across all major indices. The negative outlook resulted from concerns about a more hawkish Fed than previously believed, which were sparked by robust US retail sales. Neel Kashkari, the president of the Minneapolis Federal Reserve, reinforced these ideas in his remarks. He doubted whether the Fed had taken sufficient action to bring inflation down to the 2% target. China’s economic recovery has long been the subject of concern. Recent data indicates that the People’s Bank of China may modify its policies going forward, following yesterday’s reduction in the rate on its medium-term lending facility, which has a one-year duration.

RBNZ Governor Adrian Orr seemed to fall into the chorus of international central banks during the press conference following the decision. He hinted that rather than providing market-specific guidance, the emphasis going forward will be on the data as it becomes available. He was making reference to the view held by the market that the bank had increased its OCR track. “The current and expected OCR settings are contractionary, sitting above our estimates for the neutral OCR,” the statement states explicitly. It is possible that the market overreached itself in anticipating a rate increase. Additionally, on Friday, Governor Orr will testify before the Parliament Select Committee, where he will address the monetary policy statement (MPS) released today. In New Zealand, acronyms are popular! It is anticipated by the market that he will not stray from the plan that he presented today.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/