USDCAD Analysis

USDCAD is moving in Ascending channel and market has reached higher high area of the channel

For the second day in a row, the USD/CAD pair continues to rise, closing Friday’s European session at 1.3590. The positive US employment data contributed to the strengthening of the US dollar USD, which furthers concerns about the outlook for inflation. The index fell to 230K for the week ending August 18, from a previous reading of 240K, which was predicted to stay unchanged. The US Dollar Index DXY, which compares the US Dollar USD to six major currencies, is currently trading at 104.20. In order to shape possible strategies in response to wagers on the USD/CAD pair, market participants await US Federal Reserve Fed Chair Jerome Powell’s speech at the Jackson Hole Symposium. Powell is expected to share insights into the financial and economic outlook.

Moreover, hawkish remarks made by James Bullard, the former president of the St. Louis Federal Reserve, supported the US dollar USD. According to Bloomberg, Bullard announced, “The reacceleration could put upward pressure on inflation and thus makes it impossible for the Fed to start cutting rates anytime soon.” In contrast, Patrick Harker, the president of the Federal Reserve Bank of Philadelphia, proposed that the rate-hike trajectory be stopped, and the president of the Federal Reserve Bank of Boston argued that there should continue to be a bias towards keeping rates high for an extended period of time. The Fed’s hawkish approach continues to be well-received by investors, which has raised US Treasury yields and supported the greenback. Because China is one of the countries that exports crude oil, the economic difficulties it faces are causing oil prices to decline, which is negatively affecting the value of the Canadian dollar CAD.

XAUUSD Analysis

XAUUSD is moving in Descending channel and market has reached the lower high area of the channel

The price of gold extends the late retreat from a two-week high, or the $1,923–$1,924 region, from the day before and declines during Friday’s Asian session. With over 0.15% loss on the day, the XAUUSD pair is currently trading slightly below the $1,915 mark, as investors await Federal Reserve Fed Chair Jerome Powell’s eagerly awaited speech at the Jackson Hole Symposium. The next leg of a directional move for the price of gold will be determined by investors, who will be on the lookout for new clues regarding the Fed’s path forward with rate hikes. These factors will also have a significant impact on the near-term dynamics of the US Dollar USD price dynamics. Expectations for additional Fed tightening were dashed by the dismal release of the flash PMI prints from the United States USD on Wednesday, which revealed that business activity in the largest economy in the world approached the point of stagnation in August. Nevertheless, the possibility of another 25 basis point bps lift-off by the end of the year remains due to the hawkish comments made by Fed officials overnight.Although she acknowledged that further rate hikes are conceivable and that it is too soon to announce when rate cuts will occur, Boston Fed President Susan Collins stated that the Fed may be in a position to maintain current rates. In a related statement, Philadelphia Fed President Patrick Harker said that the central bank must maintain its tight policy and added that further inflation reductions are necessary in order to allow for rate cuts.

Meanwhile, the hawkish outlook keeps pushing higher US Treasury bond yields and raises the USD Index DXY to its highest point since June 6. This is expected to divert some capital from the price of gold denominated in US dollars.However, concerns about a more severe global economic downturn may provide some backing for the safe-haven precious metal and help keep the downside in check, at least temporarily. A number of manufacturing surveys released on Wednesday fueled recession fears by painting a dire picture of the state of economies around the world against the backdrop of China’s rapidly deteriorating economic conditions. This is still having an impact on investor sentiment, as seen by the generally downbeat tone surrounding the equities markets. It also supports the price of gold, so it is advisable to exercise caution before positioning for any additional intraday decline. Additionally, the 200-day Simple Moving Average SMA support is a technically significant support level that the XAUUSD has managed to hold above thus far. Therefore, significant follow-through selling is required to verify that this week’s moderate recovery from levels below $1,885, or the lowest since March 13, has peaked. Even so, it appears that the gold price has ended its four-day winning run for the time being, though it is still expected to post its first weekly gains in the previous five.

USDJPY Analysis

USDJPY is moving in Descending channel and market has reached lower high area of the channel.

The USD/JPY trades higher at 146.00, regaining some of the ground lost during Friday’s early trading hours in the European session. The mixed statistics on Japan’s inflation put downward pressure on the Japanese yen. The Tokyo Consumer Price Index (CPI) for August decreased from 3.2% to 2.9% on an annual basis, below the 3.0% forecast. Tokyo CPI ex Fresh Food (YoY) dropped to 2.8% versus the market expectation of 2.9%, while Tokyo CPI ex Food and Energy (YoY) stayed steady at 4%. In July, the index displayed the 3% value.Conversely, US initial claims for unemployment fell to 230K from 240K, which was in line with previous expectations. This was the case for the week ending on August 18. On the other hand, US durable goods orders for July decreased 5.2% from the previous figure of 4.4%, which was in line with the market consensus of 4%.

Prior to Fed Chair Powell’s speech, the US Dollar Index (DXY), which gauges how the USD performs against six major currencies, is trading at roughly 104.20. The Bank of Japan (BoJ) Governor Kazuo Ueda’s speech at the Jackson Hole Symposium on Saturday will be closely watched by USD/JPY traders as they look for insights into the financial and economic sectors to help shape potential strategies in response to placing bets on the USD/JPY pair. Furthermore, the strong US employment data, rising US Treasury yields, and conflicting opinions regarding the US Federal Reserve’s tightening of monetary policy during the September meeting all contributed to the strengthening of the USD/JPY pair. Due to their strong export-trade relations, the US-China relationship and China’s economic difficulties also played a role in the pair’s strength.

EURUSD Analysis

EURUSD is moving in Descending channel and market has fallen from the lower high area of the channel

Today at Jackson Hole, the two most well-known central bankers in the world will both be giving speeches. Although the Eurozone’s economic outlook is becoming more dire, ING economists believe ECB President Christine Lagarde will continue to emphasise data dependence and a hawkish stance. According to our assessment, Lagarde is not happy with the market’s recent reduction of rate expectations in the Eurozone (a hike in September is only 40% priced in). As a result, she might prefer to continue ignoring certain signs of weakening growth and adhere to a strictly data-dependent strategy. In the end, we believe that there is a good chance that the ECB will raise rates in September if inflation surprises to the upside. This is especially true in light of the weakening growth outlook. We believe that following Lagarde’s speech today, there may be some re-tightening, and that the EUR/USD pair will experience a consoling rally following the break below 1.0800, which saw additional bearish momentum building overnight.

EURJPY Analysis

EURJPY is moving in Ascending channel and market has reached higher low area of the channel

August saw a further decline in the headline German IFO Business Climate Index to 85.7 from 87.4 last month and 86.7 predicted by the market. In the meantime, the reported month’s Current Economic Assessment Index dropped to 89.0 points from the predicted 91.4 and 90.0 points for July. The IFO Expectations Index, which measures businesses’ predictions for the upcoming six months, fell from 83.6 in July to 82.6 in August. The data did not meet the 83.8 market expectations.

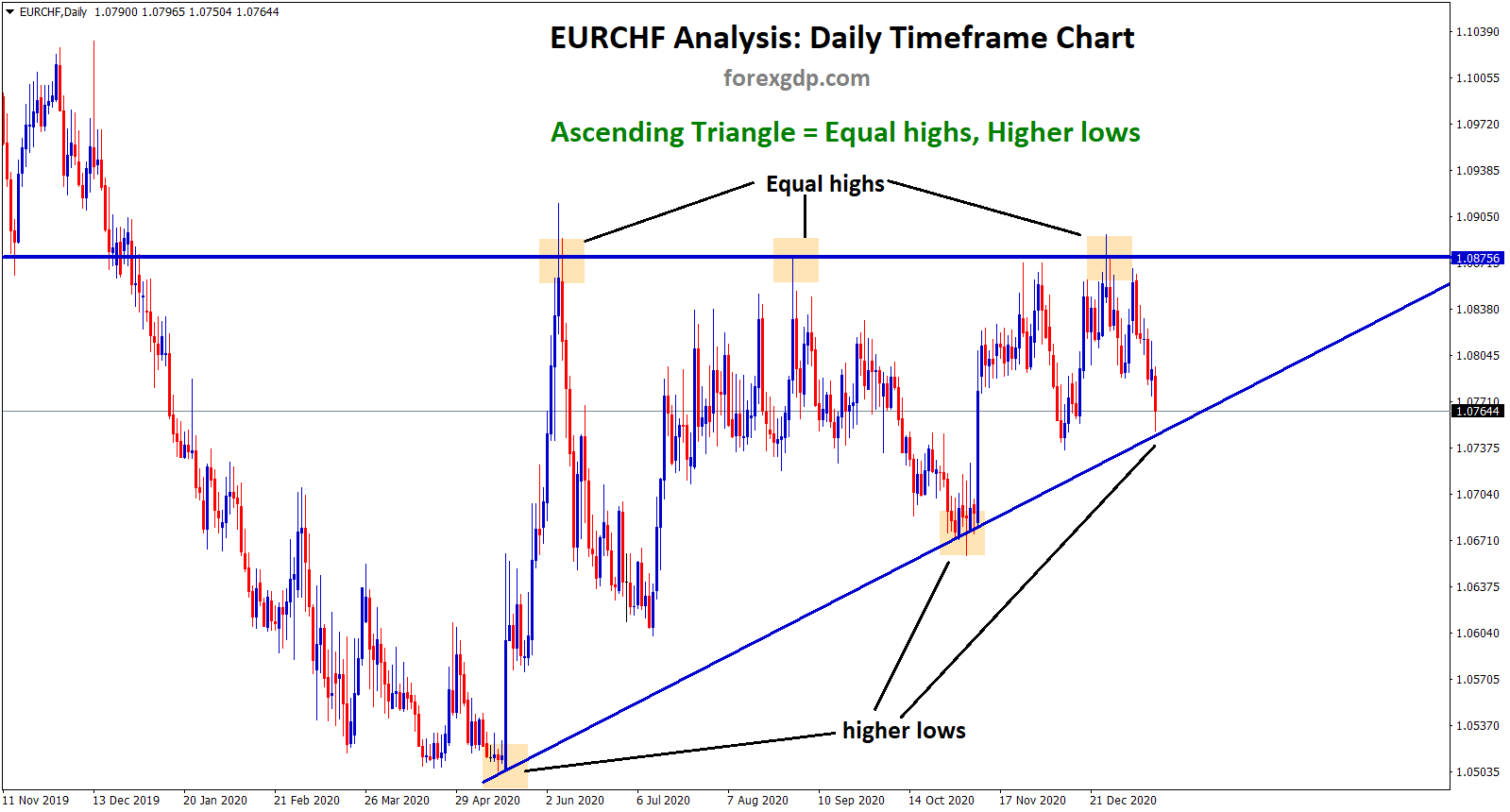

EURCHF Analysis

EURCHF is moving in Descending channel and market has reached lower high area of the channel

Fears of a recession are fueling growing momentum for an ECB rate-hike pause, although there is still room for debate, according to Reuters, which cited sources with knowledge of the discussion on Friday. Supporters of the ECB pause cite China’s slowdown, feeble growth, and better policy transmission. Policymakers concur that the ECB must make it obvious that work is still to be done and that additional rate hikes may be required before deciding to pause. Markets currently project a 50% chance of a hike in September followed by a pause, but later this year, the ECB is expected to raise interest rates by a final 25 basis points (bps), to 4.0%.

GBPUSD Analysis

GBPUSD has broken Ascending channel in downside

Because of the growing effects of the Bank of England’s BoE historically aggressive cycle of rate-tightening, the pound sterling GBP is regularly subject to a sell-off. Rising chances of a UK economic recession and pessimistic market sentiment lead to a new 11-week low for the GBPUSD exchange rate. The BoE hiked interest rates to 5.25% in an effort to combat persistent inflation, which is having an effect on UK corporations and forcing some of them to declare bankruptcy because they can no longer pay their interest. Weaker retail sales have been the consequence of the UK’s ongoing Consumer Price Index CPI inflation and eventually falling real household income, which has created a depressing demand environment. Businesses are now forced to run at reduced capacity as a result. Market players anticipate that as the BoE gets ready to tighten monetary policy even more in September, the effects of its higher interest rate policy will spread even farther. As growing expectations that the UK economy will contract cause market sentiment to remain negative, the pound sterling recovers from an 11-week low near 1.2550. The UK economy is suffering as a result of the Bank of England’s current, historically aggressive tightening cycle. This week, S&P Global released the preliminary August UK Manufacturing PMI, which fell sharply to 42.5 from estimates of 45.0 and 45.3 in July. Since the pandemic, this factory data figure has been the lowest.

Additionally, the Services PMI entered a contractionary phase and stayed below the 50.0 mark. The economic data came in at 48.7, which was less than the 50.8 predictions and the 51.3 release from July. This suggests that businesses are not making the most of their full potential because of the possibility of declining demand driven by increasing pricing pressures. The likelihood of UK companies declaring corporate default has increased due to their incapacity to pay growing borrowing costs. According to a BoE survey, the percentage of non-financial UK companies with a poor debt-service coverage ratio will increase from 45% at the end of the previous year to 50% by the end of the current year. The monthly balance of retail sales decreased to -44 in August from -25 in July, according to a report released on Thursday by the Confederation of Business Industry CBI in the UK. Since March 2021, this decline has been the largest. Retailers in the UK are less likely to invest new money in the upcoming year, according to CBI economist Martin Sartorius. Due to a slowdown in home construction and government projects being postponed because of persistent core inflation, the number of British construction companies going out of business has reached its highest level in ten years. The Insolvency Service of the UK government indicates that, as of June, 4,280 operators had declared bankruptcy. The BoE is unable to halt the rate-tightening phase despite growing recessionary risks because current inflationary pressures are significantly higher than the targeted rate of 2%.

Against the earlier prediction of 6.0%, investors now anticipate that the BoE will hike interest rates by 25 basis points bps in September, with a peak interest rate of approximately 5.75%. By reducing the price cap on household energy bills, the British energy regulator Ofgem has stepped up to offer some relief to UK households in the interim. After a price reduction of GBP 2,074 in July, the cap was reduced to an annual level of GBP 1,923 for a typical dual-fuel household. The UK regulator stated, Households will save an average of GBP 151 compared with the previous quarter. Due to the summer bank holiday, UK markets will be closed on Monday. As a result of investors’ continued concern over Federal Reserve Fed Chair Jerome Powell’s remarks at the Jackson Hole Symposium, market sentiment is pessimistic. Investors are still worried about whether Fed Powell will support higher interest rate requirements or provide guidance on how long rates will stay high. With increasing confidence, the US Dollar Index DXY breaks above the 104.00 resistance as concerns about a slowdown in China intensify due to growing deflation risks. US Treasury yields on the 10-year note also increased to 4.25%.

AUDUSD Analysis

AUDUSD is moving in Descending channel and market has fallen from the lower high area of the channel

After reversing from the weekly high, the AUD/USD pair trades lower during the Asian session on Friday, around 0.6410. The positive US economic data, higher US Treasury yields, and conflicting opinions regarding the US Federal Reserve’s tightening of monetary policy in September all put downward pressure on the pair. Furthermore, because of the complex export-trade relations between the two countries, the Australian Dollar (AUD) is under pressure from declining US-China optimism as well as China’s economic difficulties. Initial Jobless Claims data from the US indicated favourable employment conditions, raising concerns about the country’s inflation outlook. During the week that concluded on August 18, the index dropped to 230K, which was less than the predicted 240K. In contrast to the market consensus of 4%, the US Durable Goods Orders for July showed a 5.2% decrease, which was less than the 4.4% reading from June.

Following Fed Chairman Jerome Powell’s speech at the Jackson Hole Symposium on Friday, the US Fed’s interest rate hike policy has generated mixed feelings, which has resulted in a weakening of the AUD/USD pair. In addition, hawkish comments made by former president of the Federal Reserve of St. Louis James Bullard supported the US dollar (USD). Because of the potential for inflation to increase, Bullard stated, “the reacceleration makes it impossible for the Fed to start cutting rates anytime soon” – Bloomberg. On the other hand, President Patrick Harker of the Federal Reserve Bank of Philadelphia suggested that the rate hike trajectory may be coming to an end, while President James Baker of the Boston Federal Reserve defended his preference to maintain a bias in favour of holding rates higher for a longer period of time. Ahead of Fed Chair Powell’s speech, the US Dollar Index (DXY), which gauges the performance of the US dollar against six major currencies, is still rising. As of writing, the spot price is trading higher at 104.30. Traders will be attentive to the speeches made by central banks, hoping to glean insights into the state of the economy and the trajectory of inflation that will impact the Fed’s decision-making regarding future monetary policy.

NZDUSD Analysis

NZDUSD is moving in Descending channel and market has fallen from the lower high area of the channel

During the early hours of the European session on Friday, the NZDUSD pair makes a new low since November 2022 as it continues to drift lower for the second day in a row. However, spot prices demonstrate some resilience below 0.5900 once more and bounce back quickly in the last hour, but any significant upside is still elusive given the underlying bullish tone surrounding the US Dollar USD. The USD Index DXY, which measures the value of the US dollar relative to a basket of other currencies, actually rises to a two-and-a-half-month high as traders keep pricing in the possibility of additional Federal Reserve Fed policy tightening. The hawkish comments made by Fed officials overnight confirmed the bets and left the door open for one more 25 bps lift-off before the end of the year. Meanwhile, the outlook continues to support elevated US Treasury bond yields and the value of the dollar.

Concerns about a more severe global economic downturn, aside from the belief that the Fed will maintain higher interest rates for an extended period of time, support the safe-haven value of the US dollar and should help to limit the movement of the NZDUSD pair. A number of manufacturing surveys released on Wednesday fueled recession fears by painting a dire picture of the state of economies around the world against the backdrop of China’s rapidly deteriorating economic conditions. This is likely to be detrimental to the growth-sensitive Kiwi. But, traders may decide to stay away from new bearish wagers on the NZDUSD pair in anticipation of Fed Chair Jerome Powell’s eagerly awaited speech at the Jackson Hole Symposium. Investors are likely to seek out new indications regarding the Fed’s trajectory for raising interest rates in the future, as this will have a significant impact on the dynamics of the USD price and give the major a new direction. Spot prices, however, are still expected to close lower for the sixth consecutive week.

Crude Oil Analysis

Crude Oil is moving in Descending Triangle and market has reached lower high area of the channel

The US benchmark for crude oil, Western Texas Intermediate (WTI), is currently trading at roughly $78.95 on Friday. WTI prices are still under pressure as investors are concerned about the demand for oil and the likelihood of rising US interest rates. The US, UK, Japan, and Eurozone’s business activity slowed down, according to S&P Global PMI data released on Wednesday. The data was below expectations. Consequently, a global economic recession may result in less demand for oil, which would pressure WTI prices. Additionally, Boston Federal Reserve (Fed) President Susan Collins stated that it would be premature to send a clear signal about when rate cuts will occur and that additional rate increases are possible. It is important to remember that higher interest rates result in higher borrowing costs, which can impede economic growth and reduce demand for oil.

Iran’s oil minister said that the country will reach 3.4 million barrels per day (bpd) of crude oil production by the end of September, in spite of US sanctions. Officials from the US are also developing a strategy to remove sanctions against Venezuela. If Venezuela moves closer to holding free and fair presidential elections, it will be able to export more crude. This development raises WTI prices in spite of the US dollar’s strengthening. Moving on, oil traders will be watching Jerome Powell’s speech on Friday. The speech might shed light on the state of the economy and hint at whether inflation is under control or whether more interest rate increases are needed to fight it. The events could have a big effect on the WTI price in US dollars. The data will serve as a guide for oil traders as they look for trading opportunities around WTI prices.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/