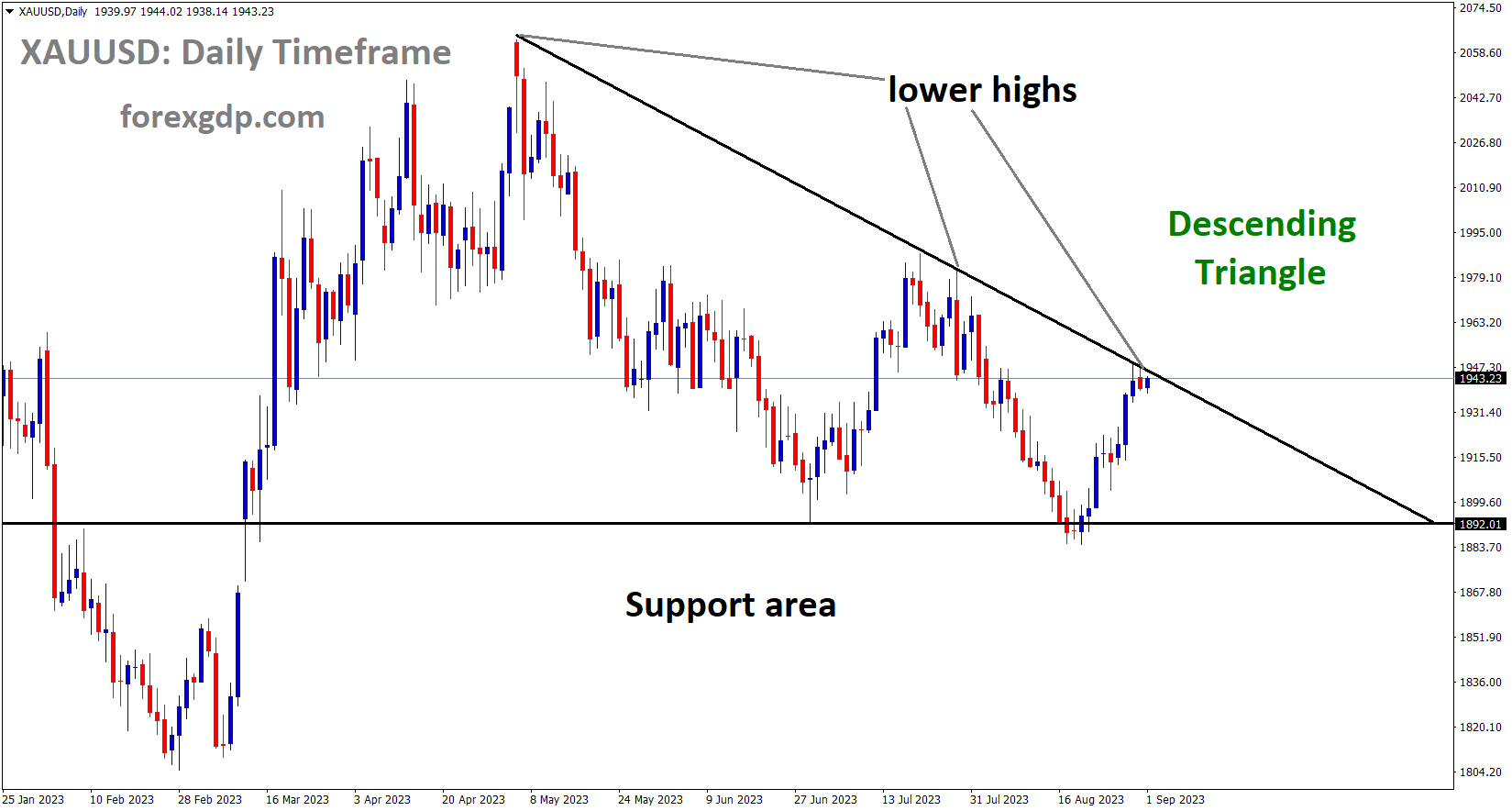

XAUUSD Analysis

XAUUSD Gold price is moving in the Descending triangle pattern and the market has reached the lower high area of the pattern

The US Core PCE index data for August came in at 4.2%, down from 4.1% in July, which caused a decrease in gold prices. Data on consumer spending increased to 0.80% for the month of July, up from the previous reading of 0.60%.

The gold price XAUUSD, which reversed from its highest level in a month the day before, eased to $1,940 in the early hours of Friday, illustrating the regular consolidation ahead of the US Nonfarm Payrolls NFP. In addition to the pre-data positioning, the traders of XAUUSD also convey the market’s uncertainty regarding the Federal Reserve’s Fed next move, which is caused by the market’s disapproval of China’s stimulus as well as the lack of clarity in the recent US data. After reversing from the multi-day peak, the price of gold is still low as markets stay erratic ahead of important data or events. This is particularly true given that the most recent round of US data was mixed and China’s stimulus policies failed to impress bulls of XAUUSD. After the dismal consumer confidence and employment indicators, the US economic calendar showed marginally better data on Thursday, which led to the monthly high of the gold price to decline. As market participants await today’s crucial US jobs report, the same joins the pre-data consolidation to help the DXY pare weekly losses, the first in seven. The US Core Personal Consumption Expenditure PCE Price Index for August, the preferred inflation indicator of the US Federal Reserve, met market expectations on Thursday by increasing by 4.2% YoY and 0.2% MoM from prior estimates of 4.1% and 0.2%, respectively. Furthermore, the Chicago Purchasing Managers’ Index increased to 48.7 for August compared to 44.1 expected and 42.8 previous readings, while the Initial Jobless Claims decreased to 228K from 232K prior revised versus 235K market forecasts. Furthermore, in July, Personal Spending increased to 0.8% from 0.6% in the previous readings and the market forecast, while Personal Income decreased to 0.2% from 0.3% in the previous readings and the market forecast.

XAGUSD Analysis

XAGUSD Silver price is moving in the Descending triangle pattern and the market has fallen from the lower high area of the pattern

Recall that the US Dollar’s increase the day before was supported by Atlanta Fed President Raphael Bostic’s defence of maintaining high interest rates, which put pressure on the XAUUSD. In other news, numerous Chinese banks announced a decrease in the required down payment for first- and second-home loans, which coincided with a cut in their Yuan deposit rates. The Dragon Nation has been announcing steps to protect the COVID-19 economic recovery with great success. But recently, these measures have become less effective because of the market’s scepticism about their legitimacy. Amid these plays, US stock futures decline following a mixed Wall Street close, and the yields on US 10-year and two-year Treasury bonds stay depressed, hovering around the lowest level in three weeks. In addition, the US Dollar Index DXY tests the resolve of gold traders by failing to maintain the previous day’s gains.

Numerous economic factors are in place to guide the gold price, even as traders are stirred by conflicting emotions regarding the US Federal Reserve Fed. Among these, the US ISM Manufacturing PMI, China’s Caixin Manufacturing PMI, and the US employment report for August, which includes the elite Nonfarm Payrolls NFP, will attract significant attention. Nevertheless, as they project 170K Nonfarm Payrolls NFP figures against the previously optimistic results of the JOLTS Job Openings, ADP Employment Change, and higher prints of the US Continuing Jobless Claims, market participants are looking for more hints to counter the Gold buyers. Furthermore, compared to a year ago, the US NFP’s three-month average has decreased by half, to 218K. Consequently, the US job market scenario as a whole seems bleak, and the only way to protect the gold sellers is to produce a very strong result; failing to do so could help the XAUUSD start September strongly.

USDCHF Analysis

USDCHF is moving in the Descending channel and the market has fallen from the lower high area of the channel

August Non-Farm Payrolls data for the United States are anticipated to be 170K, up from 187K in July. The projected unemployment rate is 3.5%. It was ahead of today’s NFP that the US Dollar gained ground against counter pairs.

Following a decline in US job openings to levels not seen since early 2021, traders are reducing the likelihood that the US Federal Reserve (Fed) will hike interest rates one last time this year. The US JOLTS Job Openings data caused a prolonged US Dollar correction from the 12-week highs set last Friday, as well as renewed speculation about a rate pause by the Fed. It was thought that Fed Chair Jerome Powell’s much awaited speech at the Jackson Hole Symposium on Friday was too aggressive. Powell’s remarks supported the narrative of higher rates for longer by suggesting that there would be one more rate hike this year. As a result of his hawkish comments, the US Dollar Index sharply increased and tested the crucial 104.50 level. The likelihood of a November Fed rate hike increased to about 57% after Powell’s speech. In light of the dismal US jobs data, this probability has decreased to 40%, according to data from the CME Group’s FedWatch Tool. On Friday, the spotlight will be on the crucial August US jobs data. Important employment data will verify whether conditions in the labour market are improving despite worries about a potential hard landing. In contrast to the 187K jobs added in July, the Nonfarm Payrolls data is predicted to indicate that the US economy added 170K jobs in the eighth month of the year. It is anticipated that the unemployment rate will remain at 3.5% for the duration of the report.

The focus will also be on AHE, a gauge of wage inflation that may have a big impact on the path of interest rates set by the Fed. August’s average hourly earnings are expected to increase 4.4% annually, matching July’s rate of increase. August’s monthly average hourly earnings are expected to rise by 0.3% after growing by 0.4% in July. ADP revealed on Wednesday that only 177,000 new jobs were added by the US private sector in August, far less than the revised total of 371,000 jobs added in July. The 2.4% annual rate of growth in the US Q2 GDP was revised down to 2.1% from the preliminary reading. Payrolls probably recorded another sub-200k gain in August, staying close to the gains from June to July, according to TD Securities analysts. Unless there are significant changes, the August increase would keep the three-month pace on its downward trajectory. In addition, we anticipate that the UE rate will remain steady at 3.5% after declining for the second time in a row in July. Furthermore, we anticipate that wages will grow by 0.3% m/m (4.3% y/y). On September 1, at 12:30 GMT, the Nonfarm Payrolls number—which is a component of the US labour market report—will be released. The EUR/USD pair has been battling below the 1.0900 mark in spite of the most recent depressing US data. The labour market data will be crucial in predicting the path that the US dollar will take in relation to the euro going forward. Fed Chair Powell’s hawkish message that another rate hike is imminent would be confirmed by an NFP print that is stronger than anticipated and by hot wage inflation data.

USDCAD Analysis

USDCAD is moving in the Descending triangle pattern and the market has fallen from the lower high area of the pattern

Today’s Canadian Dollar moves up against counter pairs ahead of Q2 GDP and MoM GDP data. Oil imports and China’s challenges in the real estate market had a greater impact on oil prices.

Prior to Fridays European session, USDCAD maintains its defensive position around 1.3510 while recovering from its lowest point in a two-week period. As a result, the Loonie pair fails to boost the stronger prices of WTI crude oil, Canadas primary export, as investors prepare for the US jobs report and the Canadian growth statistics. The prior days USDCAD bears were not deterred by the general US Dollar rally or the markets readiness for important data, as WTI crude oil hit a multi-day high. The sharp revision in the Canadian Current Account data for the first quarter Q1 of 2023 could also put pressure on the pairs downside. Notwithstanding this, WTI crude oil increased for a fourth day running to $83.40, reviving a three-week high in the face of numerous actions taken by China to prevent the economy from devolving into COVID-like conditions. The Peoples Bank of China PBoC cut the foreign reserve ratio by 2.0%, and several Chinese banks lowered the interest rates on Yuan deposits. These two moves attracted the most attention. Nevertheless, unfavourable weather, Hurricane Idalia in the US, and Chinas typhoon anxiety combine with the USs significant inventory draw to drive up oil prices.

In other news, the US Dollar Index DXY is having difficulty maintaining its gains from the 200-DMA, which were made the day before at 103.60. Nevertheless, the quote saw its biggest weekly surge on Thursday as the majority of US data reversed the dovish sentiment surrounding the Federal Reserve Fed. Raphael Bostic, the president of the Atlanta Fed, made remarks that supported the “higher for longer rates” strategy. It should be highlighted that the US Core Personal Consumption Expenditure PCE Price Index for August, the Feds preferred inflation indicator, matched market expectations of 4.2% YoY and 0.2% MoM versus priors of 4.1% and 0.2%, respectively. Furthermore, the Chicago Purchasing Managers Index increased to 48.7 for August compared to 44.1 expected and 42.8 previous readings, while the Initial Jobless Claims decreased to 228K from 232K prior revised versus 235K market forecasts. Furthermore, in July, Personal Spending increased to 0.8% from 0.6% in the previous readings and the market estimate, while Personal Income decreased to 0.2% from 0.3% in the previous readings and the market forecast.

Moving forward, the risk catalysts for the second quarter Q2 and July month Gross Domestic Product GDP from Canada, as well as the US employment report for August, should be of interest to USDCAD traders. Note that the overall picture of the US job numbers is bleak; therefore, a strong US NFP is required in order for the USDCAD bulls to reverse course.

EURUSD Analysis

EURUSD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

Francois Villeroy De Halhau, the policy maker at the ECB, stated that the decline in inflation is more noteworthy. We are currently experiencing peak rates, so rate cuts are not anticipated anytime soon.

Policymaker for the European Central Bank (ECB), Francois Villeroy de Galhau, shared his thoughts on the bank’s outlook for interest rates. Since April, underlying inflation has peaked and seems to be starting to decline. However, this positive indication is still far from enough. At the forthcoming rate meetings, we have options. The peak of interest rates is very near. But still a long way from where we could think about lowering rates. Sufficient duration of high rates is more important than exact level.

EURCHF Analysis

EURCHF is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The Swiss CPI (YoY) was 1.6%, which was in line with the previous reading and 1.5% less than anticipated. The core CPI data decreased from 1.5% YoY to 1.7% YoY. Compared to -0.60% YoY, import prices increased to -0.30% YoY. After the data was released, the Swiss franc gained value.

The 0.2% increase in the Swiss CPI in August was expected. With the exception of fuel, energy, and fresh and seasonal goods, the core CPI increased by 0.1%. The price of domestic goods was zero percent, mom. Import goods prices increased by 0.8% mother. While expected to be 1.5% yoy, the CPI was unchanged at 1.6% yoy from the same month last year. The core CPI decreased from 1.7% to 1.5% year over year. Prices of domestic goods decreased from 2.3% yoy to 2.2% yoy. Prices of imported goods increased from -0.6% yoy to -0.3% yoy.

EURNZD Analysis

EURNZD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

From 83.7 to 85, consumer confidence in the New Zealand economy increased. China’s PMI report is 51.0, up from a previous reading of 49.2.

Positive data releases of China’s Caixin Manufacturing PMI for August and New Zealand’s ANZ – Roy Morgan Consumer Confidence have supported the NZD pair’s upward movement. The macroeconomic information released on Friday strengthened the foundation supporting the Kiwi pair’s strength. From 83.7 to 85, consumer confidence in New Zealand’s economic activity increased. In addition, the Chinese PMI report showed a reading of 51.0, down from the previous 49.2 to a better-than-expected 49.3. Nicola Willis is the main opposition party’s finance spokesperson in New Zealand. In an interview with Bloomberg TV, Willis expressed that their party would quickly remove the employment mandate from the Reserve Bank of New Zealand, leaving only the inflation mandate in place if they were elected. As per Willis, this would create assurance that the Reserve Bank will concentrate on fulfilling its inflation mandate.

GBPUSD Analysis

GBPUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

According to UK economist Huw Pill, the interest rate level has peaked and is sustainable, which lowers the value of the pound relative to the US dollar. Higher savings rates in UK banks allow customers to benefit from higher interest rates on their savings.

GBPUSD struggles to regain the losses of the previous day, trading Friday during the Asian session at 1.2680. Ahead of the US government’s release of employment and manufacturing data, the pair is under pressure. The moderate US data that was released on Thursday caused the GBPUSD to lose ground. As of this writing, the US Dollar Index (DXY) is trading higher at roughly 103.60. As previously mentioned, the US Core PCE increased from 4.1% to 4.2% in July, as was predicted. Furthermore, US Jobless Claims for the week ending August 25 showed a reading of 228K, which defied both the previous 232K and the market consensus of 235K. This suggests that the labour market is still strong. Nonetheless, market players are being cautious, hoping that the grim economic outlook for the United Kingdom (UK) and the September meeting of the Bank of England (BoE) will provide new momentum for tightening monetary policy. Despite hawkish sentiment surrounding a 25 basis point (bps) interest rate hike, the pair experienced downward pressure after the hawkish statement made on Thursday by BoE Chief Economist Huw Pill. Pill stated that she thought the policy ought to continue to be quite restrictive for a long time.

Furthermore, early on Friday morning in Asia, the UK’s Financial Conduct Authority (FCA) declared, as Reuters reported, that more savings accounts are offering higher interest rates as a result of a more competitive market. The Financial Conduct Authority (FCA) is striving to guarantee that British savings account holders can immediately benefit from higher interest rates, in the same way that they quickly incur higher borrowing costs. The goal of this programme is to give customers access to a fair and balanced financial environment. Investors will probably keep an eye on the US data that will be released on Friday in an attempt to get additional indications about the state of the nation’s economy. The US Average Hourly Earnings, Nonfarm Payrolls, and ISM Manufacturing PMI are some of these datasets.

CHFJPY Analysis

CHFJPY is moving in the Box pattern and the market has rebounded from the horizontal support area of the pattern

According to Japanese Finance Minister Shunuchi Suzuki, fundamentals have a major impact on FX rates, and the way they are moving is not optimal given our economy.

Shunichi Suzuki, Japan’s finance minister, will intervene verbally on Friday and reiterate that “sudden FX moves are undesirable.” The market ought to determine forex movements. Fundamentals should be reflected in FX rates.

AUDCHF Analysis

AUDCHF is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

China is probably going to pull the real estate industry out of its current slump. There are steps taken to reduce home buying challenges and eliminate price ceilings. However, no action proves effective after it is put into practise.

China is probably going to take more action to boost the nation’s real estate market, according to a Reuters story published on Friday, citing four people with knowledge of the situation. Plans for China’s real estate rebound include easing restrictions on home purchases. Price ceilings on new homes are one of the proposals for China’s real estate comeback. Since the current policies were unable to maintain a sector recovery earlier this year, the plan is to act.

The manufacturing PMI data from China Caixin dropped from 49.2 in July to 51.0, which allayed concerns about the Chinese economy. From 4.1% in July to 4.2% in August, the US Core PCE index increased. Next, the data was printed, and the Australian dollar dropped.

According to a survey sponsored by Caixin, business activity in China’s manufacturing sector defied predictions for a decline for the second consecutive month in August, returning to the expansion territory. The Caixin China Manufacturing PMI actually increased to 51.0 from 49.2 in July, but this does not allay concerns about the deteriorating circumstances in the second-largest economy in the world. This consequently does not give the Australian Dollar (AUD), a proxy for China, any significant boost.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/