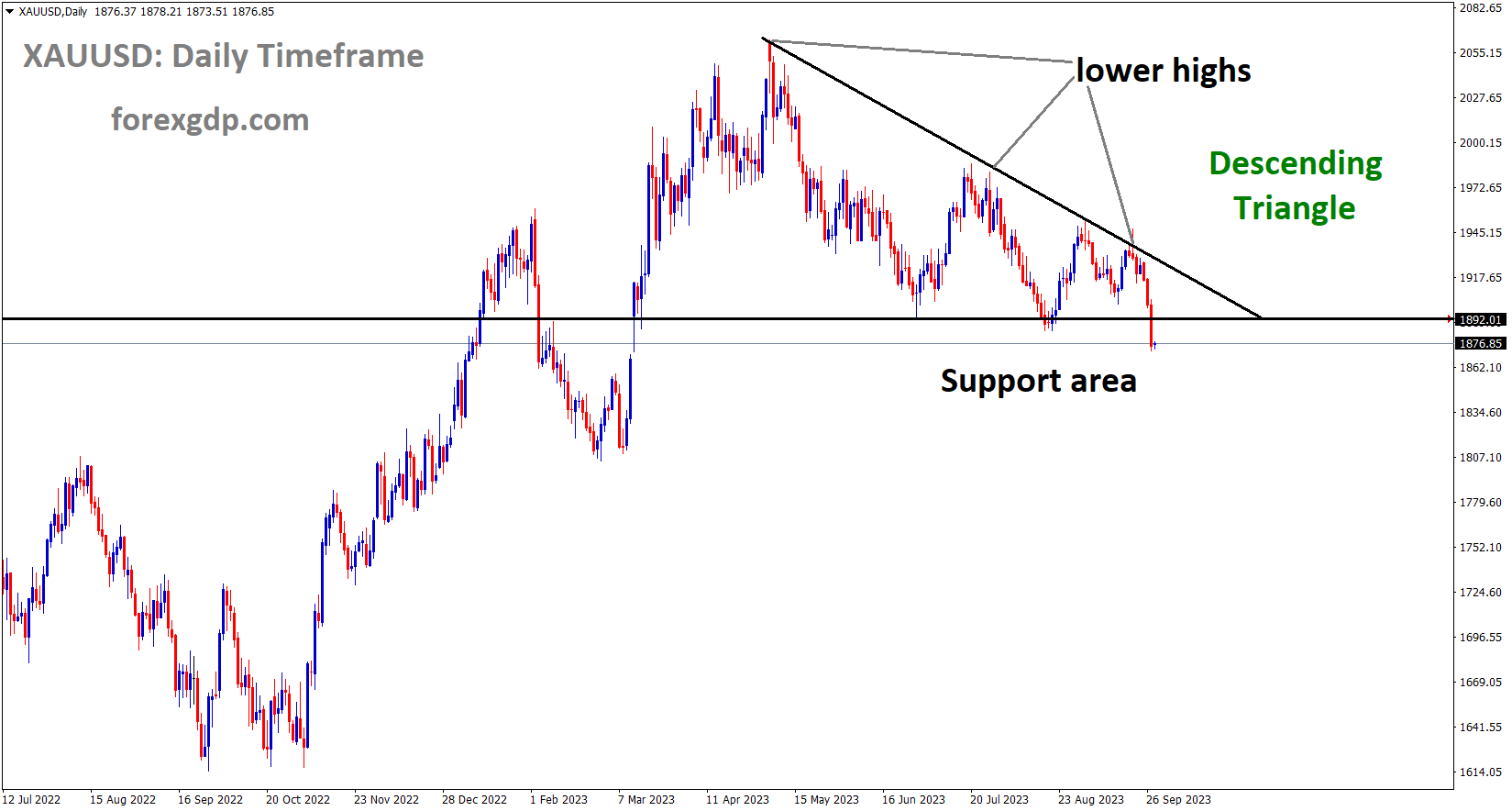

XAUUSD Analysis

XAUUSD Gold price is moving in the Descending triangle pattern and the market has reached the support area of the pattern

Gold prices are declining ahead of today’s US GDP Q2 data; selling pressure is applied to the gold side due to the potential downturn in the Chinese real estate market.

On Thursday, the gold price XAUUSD attracted some haven flow and appears to have broken a three-day losing streak to a six-and-a-half-month low, around the $1,873-1,872 zone touched the previous day. Furthermore, a slight decrease in US Treasury bond yields prevents USD bulls from placing new bets, which turns out to be another factor supporting the precious metal. Any meaningful recovery in the gold price, however, remains elusive in the face of rising bets on the Federal Reserve Fed tightening policy, which should act as a tailwind for the USD and US bond yields. The US Federal Reserve warned last week that stick inflation was likely to prompt at least one more interest rate hike by the end of the year. Furthermore, the resilience of the US economy should allow the Fed to maintain its hawkish stance.

As a result, it is prudent to wait for strong follow-through buying before concluding that the Gold price has formed a near-term bottom and positioning for further gains. Traders may also prefer to stay on the sidelines ahead of the release of the US Core PCE Price Index on Friday, which will provide new clues about the Fed’s future rate-hike path and provide a new directional impetus to the non-yielding yellow metal. The gold price fell the most in a single day in two months, owing to a stronger US dollar and rising US bond yields. Investors are still concerned about China’s property sector and the effects of rapidly rising borrowing costs. Republican US House Speaker Kevin McCarthy voted against a Senate stopgap funding bill on Wednesday. This pushes the US government closer to its fourth partial shutdown in a decade, weighing on risk sentiment. The US Dollar extends its recent strong gains to the highest level since November 2022, as US bond yields fall. Minneapolis Fed President Neel Kashkari’s hawkish comments raise expectations for at least one more rate hike by the end of the year. The stronger-than-expected US Durable Goods Orders data ensures that the Fed will keep interest rates higher for an extended period of time. Thursday’s US economic calendar includes the final US Q2 GDP and the weekly initial jobless claims. The US Core PCE Price Index, which is due on Friday, is still being watched for clues about the Fed’s future interest rate hike path.

XAGUSD Analysis

XAGUSD Silver price is moving in an Ascending channel and the market has reached the higher low area of the channel

FED Minneapolis President Neel Kashkari stated that if the economy did not slow down as expected, interest rates would be raised this year. There will be no rate increases until 2024. On the one hand, the US economy is doing well, while oil prices are rising.

Minneapolis Federal Reserve President Neel Kashkari told CNBC on Wednesday that if the economy does not slow as planned, the Fed may have to raise interest rates further. However, he cautioned that if negative growth scenarios such as the government shutdown or the auto strike hit the economy, they may have to do less with monetary policy to bring inflation back to target. According to Kashkari, the US economy has been surprisingly resilient. In terms of projections, he sees no rate changes in 2024. “Higher oil prices will not alone warrant more rate hikes,” he stated.

USDCHF Analysis

USDCHF is moving in an Ascending channel and the market has fallen from the higher high area of the channel

The US Dollar strengthened against the Swiss Franc last month, and the SNB kept interest rates unchanged last week, leaving it disappointed with the Swiss Franc’s strength against counter-pairs. The Chinese property sector also contributed to the Swiss Franc’s demand for safe currency.

The USDCHF pair recovered from a slight decline during the Asian session on Thursday and is currently trading above 0.9200, very close to its highest level since late March, which was touched the day before. The US Dollar (USD) holds steady near a 10-month high and proves to be a significant factor acting as a tailwind for the USDCHF pair despite a slight decline in US Treasury bond yields. Market players have been pricing in the possibility of at least one more rate hike by the end of this year, as they now appear certain that the Federal Reserve (Fed) will maintain its hawkish stance. The bets were reinforced by Minneapolis Fed President Neel Kashkari’s hawkish remarks overnight, which stated that despite ample evidence of continued economic strength, it is unclear whether the central bank has finished raising rates.

Furthermore, some economists revised up their estimates of third-quarter GDP growth in response to the better-than-expected release of US durable goods orders, which should enable the Fed to maintain higher interest rates for an extended period of time. As a result, the yield on the benchmark 10-year US government bond increased to a 16-year high, which is good news for USD bulls. Nevertheless, the extreme overbought conditions and growing likelihood of a US government shutdown prevent the bulls in the USD from making new wagers. On Wednesday, US House Speaker Kevin McCarthy, a Republican, rejected a temporary funding bill that was making progress in the Senate. This is in addition to ongoing concerns about China’s failing real estate market and economic challenges brought on by quickly increasing borrowing costs, which in turn reduces investors’ desire for riskier assets. The prevailing risk-off climate makes this clear and supports the Swiss Franc’s (CHF) status as a relative safe haven, which limits future gains for the USDCHF pair. The US economic docket, which includes the final Q2 GDP figure and the weekly initial jobless claims, is now of interest to traders. This could affect the USD and give the USDCHF pair some momentum, along with the US bond yields.

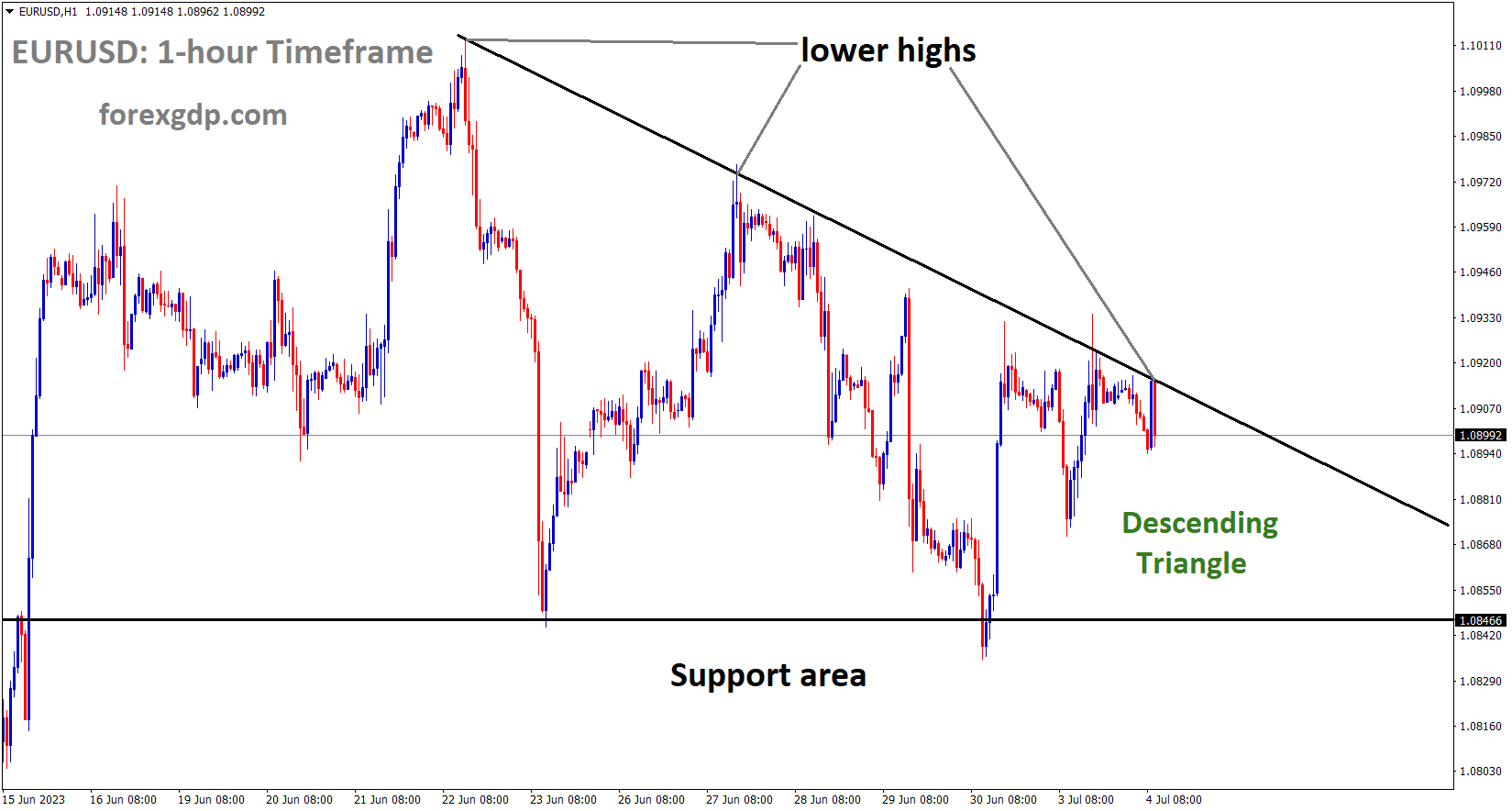

EURUSD Analysis

EURUSD is moving in the Box pattern and the market has reached the support area of the pattern

The euro pair has corrected more against the US dollar this month after the ECB stated that this is the final rate hike for the year and that additional hikes will depend on data. German yields are declining, resulting in losses for Euro pairs relative to Counter pairs.

According to the USD Index (DXY), the Greenback has been strengthening for the fourth session in a row and has reached its highest levels for 2023 at roughly 106.50. No observations of this level have been made since late November 2022. Despite generally unchanged expectations in the monetary policy scenario, the pair’s further decline is accompanied by a corrective move in US and German yields, which leave the area of recent multi-year highs. In reference to the latter, investors continue to factor in a 25 basis point increase in interest rates by the Federal Reserve (Fed) by year-end.

")

In the meantime, market talks still point to a deadlock at the European Central Bank (ECB), despite inflation rates that are consistently much higher than the bank’s objective. According to GfK, consumer confidence in Germany is predicted to marginally decline to -26.5 in October on the European calendar.

EURCHF Analysis

EURCHF is moving in the Descending channel and the market has reached the lower high area of the channel

In the US, Durable Goods Orders increased 0.2% in August compared to the previous month, while Mortgage Applications, as measured by MBA, decreased 1.3% in the week ending September 22.The offered position is maintained by the EUR versus the USD. The correction of US and German yields is downward across various maturities. Investors anticipate that before the end of 2023, the Fed will raise rates by 25 basis points. The markets make assumptions about potential Fed interest rate reductions in Q3 2024. The market is still buzzing with talk of an ECB pause. Rates have not necessarily peaked, according to Frank Elderson, an Executive Board member of the ECB. Concerns about interventions regarding the USDJPY are still valid. The BoJ Minutes supported maintaining the present monetary policy.

EURJPY Analysis

EURJPY is moving in the Box pattern and the market has reached the support area of the pattern

According to the BoJ meeting minutes, YCC may need to be adjusted based on the inflation data method. Experts anticipated Rate increases are anticipated in January 2024 regardless of whether wage growth and inflation meet their targets, so YCC tweaks will not pave the way for them.

Japanese Finance Minister Shinichi Suzuki, a plan will be put in place to prevent excessive FX movements against the Japanese yen. The movement of forex pairs must be stable. Refuse to respond to inquiries from the reporter regarding rate increases or omit questions.

The minutes of the July meeting of the Bank of Japan were made public this morning, and they revealed that participants thought it was crucial to discuss the revisions made to the Yield Curve Control (YCC) policy. The goal of the explanation, according to policymakers, is to prevent market participants from reading the changes as an indication that accommodative monetary policy is about to end. While this is going on, market players are pricing in a probability of slightly more than 60% for a rate hike in January 2024—even though the BoJ has not yet managed to sustain wage growth above inflation. The Yen has been struggling recently, especially versus the Greenback, but it has also made some progress against the Euro and the GBP. This is mostly due to concerns about a slowdown for the EU and the UK, as both economies have seen sharp declines in value after recent central bank meetings.

The prospect of FX intervention is still a source of support for the Yen. Remarks from BoJ policymakers and Japanese officials continue to support the Yen and prevent a bigger decline. Though recent statements from the Central Bank have insisted that it does not target levels, former BoJ officials have discussed how the psychological level of 150.00 is crucial for the BoJ and appears to be influencing market participants’ thoughts. The likelihood of a pullback in the USDJPY increases as we approach 150.00 or break above it. Bulls may decide to exit their long positions as the threat of intervention is sure to intensify. In the next week or so, the US, UK, and EU will pose the majority of the risk to Yen pairs. There are very few high impact risk events, none of which are from Japan, and any events that move the market are probably going to be comments about intervention. In order to support the currency, the BoJ has employed this strategy rather successfully. None of the anticipated data releases stand out to me as possibly changing the narrative that currently holds higher rates for longer. However, weak data from the UK and the EU could encourage further weakness in the GBP and the Euro, while strong data from the US could maintain the advance of the Dollar Index (DXY), which would encourage the need for BoJ officials to step in.

Shunichi Suzuki, the finance minister of Japan, reiterated on Thursday that he would not rule out taking action in the event of excessive foreign exchange volatility. It is crucial that currencies move steadily. Keep an eye on FX movements as they move quickly. When questioned about any plans for a rate check, they declined to comment.

GBPCAD Analysis

GBPCAD is moving in the Descending channel and the market has reached the lower high area of the channel

Differences in interest rates weaken the pound relative to counter pairs. The BoE held rates last week, which made the GBP less valuable relative to the USD. Economists predict that rates will remain unchanged until July 2024. At 6.7%, inflation is significantly higher than the BoE’s target of 2%.

The markets, anticipating yet another hike, were taken aback last week when the Bank of England decided to maintain its key lending rate at 5.25%. The base case, according to a Reuters poll of economists, is that rates will remain unchanged, at least through July 2024. However, a sizable minority of respondents apparently still anticipated rate increases.It is not hard to understand why there is not consensus. Even though the rate of inflation in UK consumer prices has decreased over the last three months to 6.7%, it is still significantly higher than the BoE’s 2% target. From the retail sales numbers from last month to the more recent Purchasing Managers Index figures, it is undeniable that recent economic data have been weak, and it is likely that prices will eventually reflect this.

However, it has not actually occurred yet. In fact, this month’s decisions to hold or hike rates were equally divided among the Bank of England’s own rate setters. The governor’s casting vote was necessary for the “hold” side to prevail. This week’s availability of UK economic data is not particularly strong to keep traders interested in the “GBP.” The final British Gross Domestic Product figures for the second quarter will be released to the market. They are predicted to rise marginally, but even if they do, the meagre 0.4% annualised gain is predicted to prove too historic to have a significant effect on the weakening sterling.

CADCHF Analysis

CADCHF is moving in the Descending channel and the market has reached the lower high area of the channel

According to ANZ Bank economists, the Canadian dollar is outperforming because of rising oil prices and encouraging economic data in recent months. A rise in oil prices devalues the GBP, EUR, and JPY.

Improved labour market conditions and rising oil prices helped the CAD bounce back on most crosses during the latter half of Q3, despite weaker economic data during that time. Analysing Loonie’s prospects are ANZ Bank economists. A stronger CAD should be aided by rising oil prices.

AUDUSD Analysis

AUDUSD is moving in the Box pattern and the market has reached the support area of the pattern

Data on Australian retail sales for the month of August showed 0.20%, a decrease from 0.50% in the previous month. Following the release of the data, the Australian dollar declined.

Wednesday marked the 10-month low for the Australian dollar AUD. Despite the release of disappointing Australia’s Retail Sales data, the AUDUSD pair continues to hold its ground. The monthly Consumer Price Index CPI for Australia has increased since July’s reading, which may be related to rising energy costs. Expectations of another interest rate hike by the Reserve Bank of Australia RBA have increased in response to this anticipated increase in inflation. Even so, the Consumer Price Index CPI figures that were positive did not help the AUD gain momentum. Because of the growing market sentiment towards risk aversion, the Australian dollar is experiencing downward pressure. The decline in commodity prices is also restricting the AUDUSD pair’s potential for upside. Driven by strong macroeconomic data from the US, the US Dollar Index DXY is still rising, trading at its highest levels since December. The US Treasury yields’ strong performance over the prospect of a US government shutdown is blamed for the USD’s recent spike. The US Treasury note’s 10-year yield is at all-time highs. The hawkish comments made by Federal Reserve Fed board members serve to further bolster the bullish momentum in the USD. The Minneapolis Federal Reserve President, Neel Kashkari, recently made remarks that alluded to the possibility of future rate increases.

Additionally, Kashkari did not rule out the possibility that interest rates would stay where they are if rate reductions are postponed even longer.Driven by strong macroeconomic data from the US, the US Dollar Index DXY is still rising, trading at its highest levels since December. The US Treasury yields’ strong performance over the prospect of a US government shutdown is blamed for the USD’s recent spike. The US Treasury note’s 10-year yield is at all-time highs. The hawkish comments made by Federal Reserve Fed board members serve to further bolster the bullish momentum in the USD. The Minneapolis Federal Reserve President, Neel Kashkari, recently made remarks that alluded to the possibility of future rate increases. Additionally, Kashkari did not rule out the possibility that interest rates would stay where they are if rate reductions are postponed even longer. After hitting a 10-month low at 0.6331 on Wednesday, the Australian dollar is making an attempt to recover. As of this writing, on Thursday during the European session, it is trading at about 0.6370. After rising by 0.5% in July, Australian retail sales grew by 0.2% in August. In August, it was anticipated that the index would rise by 0.3%. As anticipated, Australia’s Monthly Consumer Price Index CPI increased 5.2% year over year in August, following a 4.9% increase in July. An increasing number of people anticipate that the RBA will raise interest rates at its meetings in November and December.

The strengthening of the US dollar USD is linked to US Treasury yields’ favourable performance in light of the upcoming government shutdown. The US Treasury note’s 10-year yield is at all-time highs. US Durable Goods Orders increased by 0.2%, deviating from the market’s forecast of a 0.5% decline in August and the previous 5.6% decline. Data from the EIA’s Crude Oil Stocks Change report for the week ending September 22nd indicated that, in contrast to the 2.135 million drawdown observed the week before, stocks had dropped by 2.17 million barrels. The oil market had anticipated a much smaller 0.32 million barrel drop in stockpiles. The state of affairs surrounding Evergrande in China is becoming more turbulent, mysterious, and unsettling. On Wednesday, Bloomberg revealed that the company’s chairman was being watched by the police. With over $300 billion in total liabilities, Evergrande is the most indebted developer in the world and is at the centre of an unparalleled liquidity crisis in China’s real estate market. The Minneapolis Federal Reserve President Neel Kashkari’s hawkish comments have caused the US dollar USD to strengthen broadly and have acted as a headwind for the AUDUSD pair. Kashkari underlined the possibility of future rate increases. On Thursday, traders will be watching for the release of the US Gross Domestic Product Annualised, which is predicted to stay at the current 2.1% level. On Friday, attention will be focused on the Core Personal Consumption Expenditure PCE Price Index. It is anticipated that the Fed’s preferred consumer inflation gauge will drop from 4.2% to 3.9%.

NZDUSD Analysis

NZDUSD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

September’s ANZ Business Confidence figures showed a 1.5% decline from the previous month’s 3.5% decline. Following the release of the data, the New Zealand Dollar continued to steadily decline.

According to the National Bank of New Zealand’s most recent data, which was made public on Thursday, ANZ Business Confidence for September increased to 1.5 from a 3.7 decline the month before. In addition, the ANZ Activity Outlook increased from 11.2% in August to 10.9 in September.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/