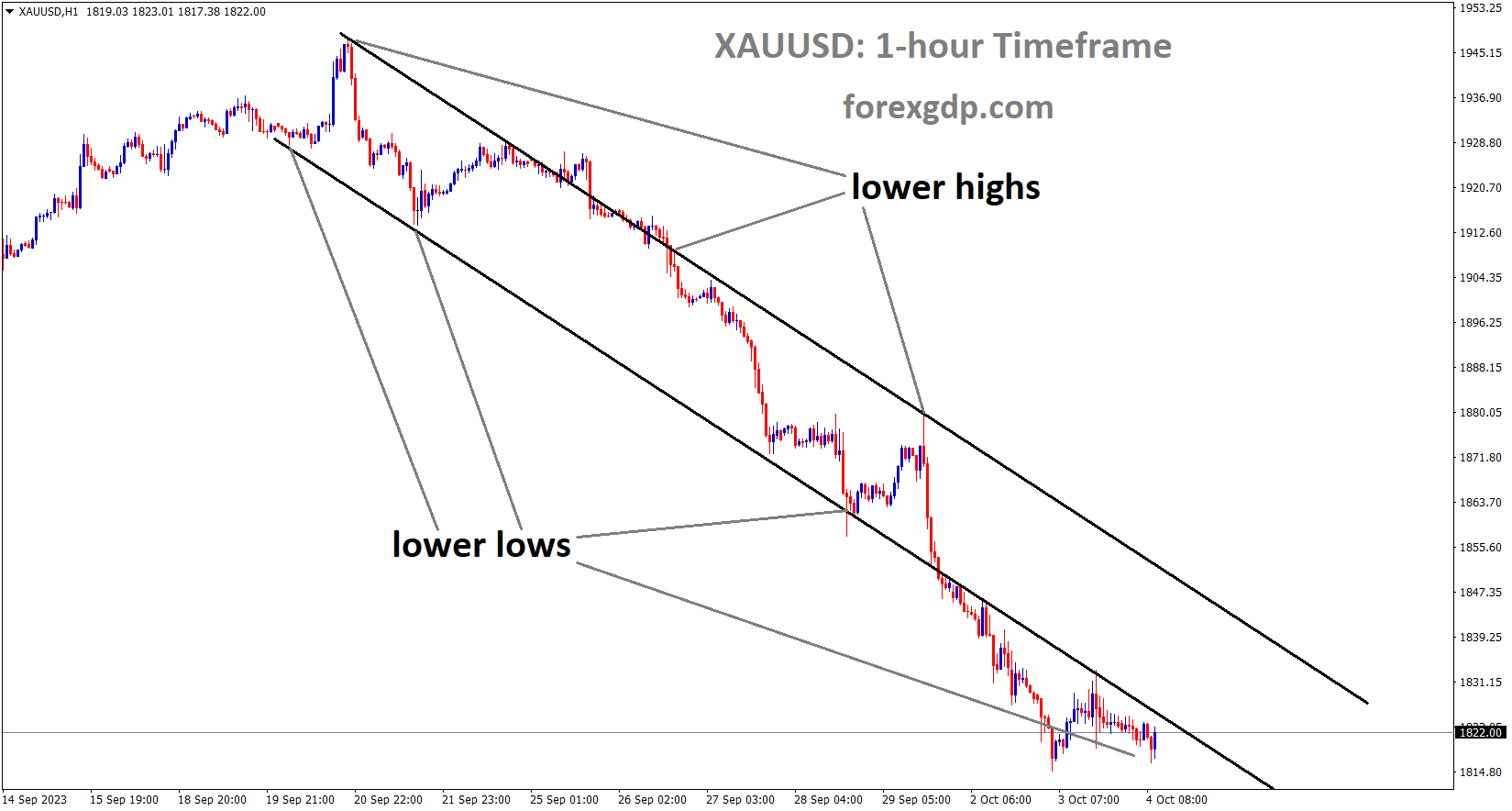

Gold Analysis

XAUUSD Gold price is moving in the Descending channel and the market has reached the lower low area of the channel

Since the beginning of the week, gold prices have declined relative to the US dollar; US Federal Reserve members have consistently stated that interest rates will continue to rise until the end of 2023. The USD strengthens versus counter pairs in light of this news

For the eighth straight day on Wednesday, the gold price trades with a slight negative bias as it continues to struggle to show signs of a meaningful recovery. The early European session saw continued weakness in the precious metal, which is still very close to the nearly seven-month low that was reached on Tuesday. Additionally, the Federal Reserve’s hawkish outlook, higher US Treasury bond yields, and a bullish attitude towards the US Dollar support the likelihood that the precious metal’s decline over the previous two weeks will continue. The belief among market players is that the Federal Reserve will persist in tightening its monetary policy and maintaining higher interest rates for an extended period of time. This could potentially act as a hindrance to the price of gold, which is not yielding. The Job Openings and Labour Turnover Survey, or JOLTS report, which was released on Tuesday, confirmed the expectations. It revealed that job openings in the US unexpectedly increased in August amidst a spike in demand for workers and indicated that the labour market was still tight. This puts wage inflation back on the radar screen and coincides with an increase in consumer spending.

If inflation remains high, the Fed may be forced to continue raising interest rates until 2024. As a result of the outlook, the US fixed-income market experiences a prolonged selloff that drives the yield on the benchmark 10-year government bond to a record 16-year high and supports the US dollar. That being said, losses for the safe-haven XAUUSD could be constrained by oversold conditions on the daily chart and the general risk-off sentiment. Though attention is still fixed on the US NFP report on Friday, traders are now scanning the US ADP report and ISM Services PMI for short-term opportunities. The gold price is still facing selling pressure on Wednesday and is hovering around a multi-month low as a result of expectations that the Federal Reserve will continue to tighten its policies. The argument for at least one additional 25 basis point (bps) lift-off by the end of this year to return inflation to the 2% target was also supported by the remarks made recently by a number of Fed officials. According to the monthly JOLTS report, there were an estimated 9.61 million open positions in August, which represents a significant increase over the upwardly revised print of 8.92 million openings from the previous month. This may force the Fed to maintain its hawkish stance and raise interest rates at its upcoming monetary policy meeting in November, along with the ongoing high inflationary pressures.

Having negotiated legislation to extend the government’s deadline until November 17, Republican Kevin McCarthy becomes the first speaker of the US House to be removed from office. The revelation of GOP infighting and the ensuing chaos ahead of the 2024 election continue to negatively impact investor sentiment in addition to the threat of an impending recession. The current risk-off atmosphere, which favours conventional safe-haven assets, may discourage traders from making new bearish bets on the XAU/USD pair. Traders are now focusing on the ADP report, which is predicted to reveal that US private sector employers added 153K jobs in September, down from 177K jobs in August. The ISM Service PMI, which is expected to decline from 54.5 to 53.6 in September and should give the XAU/USD some momentum, is another item on the US economic docket.

Silver Analysis

XAGUSD Silver price is moving in the Descending channel and the market has reached the lowered low area of the channel

US Treasury Secretary Janet Yellen stated that the US economy is safer when semiconductor exports to China are stopped. We need more semiconductors for domestic use. Therefore, whoever believes that stopping exports is a bad idea is stupid.

At a Fortune CEO event in Washington on Tuesday, US Treasury Secretary Janet Yellen reaffirmed her belief that the US would prefer not to economically decouple from China. China has come to dominate vital supply chains for the US, especially for clean energy products. As a result, the US needs to diversify its sources of supply.

Economically speaking, the US does not want to separate from China. In the absence of a strong domestic semiconductor industry, the US would have national security issues. If we believe that the United States would be better off giving up on semiconductor manufacturing entirely, we are deluding ourselves.

USDJPY Analysis

USDJPY is moving in an Ascending channel and the market has fallen from the higher high area of the channel

According to Masato Kanda, Japan’s top currency diplomat, FX intervention is required for volatility rather than to target FX levels. He declined to provide an intervention regarding the decline in the USDJPY pair from the previous day.

It happened that for the first time since 2013, the yield on the 10-year Japanese Government Bond (JGB) hit 0.8%. The BoJ was under increased pressure to raise the yield-curve cap and get ready to abandon its negative interest rate policy. Concurrently, the US dollar (USD) continues its upward trend with the US Treasury yield. The yield on the 10-year note hit 4.865%, the highest level since 2007. The USDJPY fell almost 300 points from the 150.00 mark late on Tuesday due to speculation that the Japanese government was intervening in foreign exchange. Japan’s top currency diplomat, Masato Kanda, stated early on Wednesday that any intervention would focus more on volatility than forex levels, adding that it is customary for authorities to remain silent on whether or not they intervened. In addition, Chief Cabinet Secretary Hirokazu Matsuno of Japan stated on Monday that he will keep taking the necessary actions regarding foreign exchange, but he has not yet commented on whether Japan has intervened in the FX market. It is important to remember that last year, BoJ intervened at the 150.00 mark. Because of this, traders ought to exercise caution before making large, aggressive bets in favour of the USDJPY pair.

On the other side of the Atlantic, President Loretta Mester of the Cleveland Federal Reserve said on Tuesday that if the current state of the economy continues, she would probably support raising interest rates at the next meeting. She also mentioned that the Fed is probably at or close to its peak interest rate target. Raphael Bostic, the president of the Atlanta Fed, stated that action must be taken quickly but he will be patient. Aside from this, the Job Openings and Labour Turnover Survey (JOLTS) released on Tuesday showed that the total number of job openings for August was 9.6 million, up from 8.9 million (revised from 8.8 million) in the previous reading. This number was significantly higher than the 8.8 million estimate.

Nonetheless, this week’s US employment report may provide clues regarding the Federal Reserve’s (Fed) future monetary policy. The better-than-expected data might make the US currency more competitive. Market participants will be watching the US ISM Services PMI and ADP Employment Change, which are scheduled for release later on Wednesday in the US session. In the meantime, traders’ attention is still focused on the rumours that Japanese authorities are planning to interfere in the FX market. The US Nonfarm Payrolls data will be the main topic of discussion on Friday. Using the data as a guide, traders will look for trading opportunities around the USDJPY pair.

USDCAD Analysis

USDCAD is moving in the Descending triangle pattern and the market has reached the lower high area of the pattern

In September, the Canadian S&P Manufacturing PMI data was 47.5, lower than the anticipated 48.0. The slightly weaker Canadian dollar relative to other currencies as a result of the drop in oil prices.

At the time of writing, the US Dollar Index (DXY) is hovering around 107.10, close to the 11-month high set on Tuesday. The US Dollar (USD) is strengthening as a result of strong US employment data and higher US Treasury yields. US JOLTS Job Openings exceeded expectations, causing US Treasury yields to rise. On Wednesday, the 10-year US bond yield reached its highest level since 2007, reaching 4.85%. According to the JOLTS report, job openings increased to 9.61 million in August, up from 8.92 million in July, exceeding market expectations. Furthermore, the Fed’s hawkish tone in keeping interest rates higher for an extended period is reinforcing positive sentiment for the greenback.

If current economic conditions persist, Cleveland Federal Reserve President Loretta Mester indicated a preference for an interest rate hike at the next meeting. Atlanta Fed President Raphael Bostic, on the other hand, shared a patient outlook on the Fed’s policy outlook, stating that there is no rush to raise or lower rates.Market participants are looking forward to the release of US employment data, which includes the ADP report on Wednesday and the Nonfarm Payrolls report on Friday. The S&P Global Manufacturing PMI for Canada was released on Monday. The index fell from 48.0 in August to 47.5 in September, according to the report.

Furthermore, falling crude oil prices dragged down the commodity-linked CAD, as Canada is the leading oil exporter to the US. By press time, West Texas Intermediary (WTI) Crude Oil was trading at around $88.00 per barrel. Investors are likely to pay close attention to Canada’s Ivey Purchasing Managers Index in order to gain additional insight into the country’s business conditions.

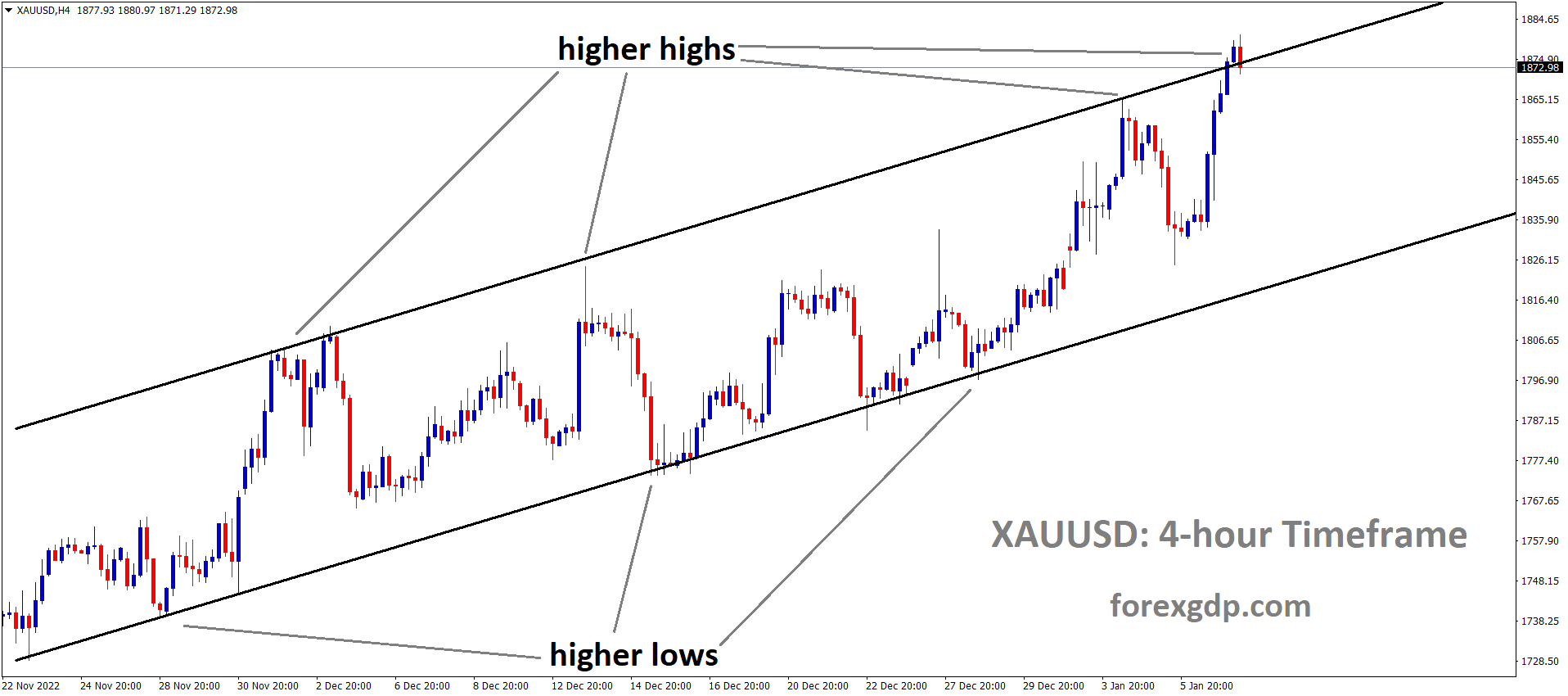

USDCHF Analysis

USDCHF is moving in an Ascending channel and the market has reached the higher high area of the channel

The Swiss CPI core rate fell to 1.3% from 1.5% in September. This CPI data falls far short of the 2% target, and the Swiss Franc falls against counter-pairs as the SNB refrains from selling foreign currencies.

Swiss inflation for September surprised on the downside, coming in at 1.7% versus a forecast of 1.8%, with the monthly rate falling by 0.1%. Meanwhile, the core CPI fell from 1.5% to 1.3%. The data backs up the Swiss National Bank’s decision to hold policy steady at its September meeting and reaffirms the bank’s stance that it is unlikely to raise interest rates further.

This is despite money markets pricing in the possibility of a hike by the end of the year. With inflation remaining comfortably below 2%, the SNB’s need to continue selling foreign currency to support the Swiss Franc diminishes. As a result, with rates appearing to be on hold, the SNB’s FX policy will be the next focal point, with a decision to stop selling foreign currency likely to weigh heavily on the Swiss Franc.

EURUSD Analysis

EURUSD is moving in the Descending channel and the market has reached the lower low area of the channel

The 10-year bond yield in the United States increased to 4.9% in August, up from 8.8 million in July. The US dollar continues to strengthen as a result of positive domestic data.

Midweek, the US Dollar continues to outperform its rivals as US Treasury bond yields rise. In the European morning, the US Dollar Index remains at multi-month highs above 107.00, and the 10-year US yield is closing in on 4.9%. In the second half of the day, the US economic docket will include ADP private sector employment and ISM Services PMI data for September, as well as August Factory Orders. Market participants will continue to pay close attention to central bankers’ comments.

The number of job openings in the United States on the last business day of August was 9.6 million, according to data released on Tuesday. This reading was significantly higher than the July reading and the market forecast of 8.8 million, attracting Federal Reserve (Fed) bets. As a result, US T-bond yields rose, Wall Street’s main indexes fell, and the USD maintained its strength during American trading hours. And, on a 216-to-210 vote, several Republicans in the House of Representatives joined Democrats in deposing Speaker Kevin McCarthy. Legislative activity in the House will be suspended until a new House Speaker is appointed. On October 10, Republicans will meet to discuss McCarthy’s replacement. Following this development, markets remain risk-averse, with another government shutdown deadline approaching on November 17. US stock index futures were last seen losing between 0.5% and 0.8%, reflecting the gloomy mood.

EURCHF Analysis

EURCHF is moving in the Descending channel and the market has fallen from the lower high area of the channel

The Euro is falling against counter pairs ahead of Eurozone PPI and retail sales data. The ECB’s Lagarde speech is also scheduled for today, and retail sales are expected to fall 1.2% from 1% last month.

Market participants are looking for new impetus from the Eurozone Producer Price Index PPI and Retail Sales. In addition, President Lagarde of the European Central Bank ECB will deliver a speech on Wednesday.

The annual Eurozone Retail Sales for August are expected to fall 1.2%, compared to the previous reading of 1%.

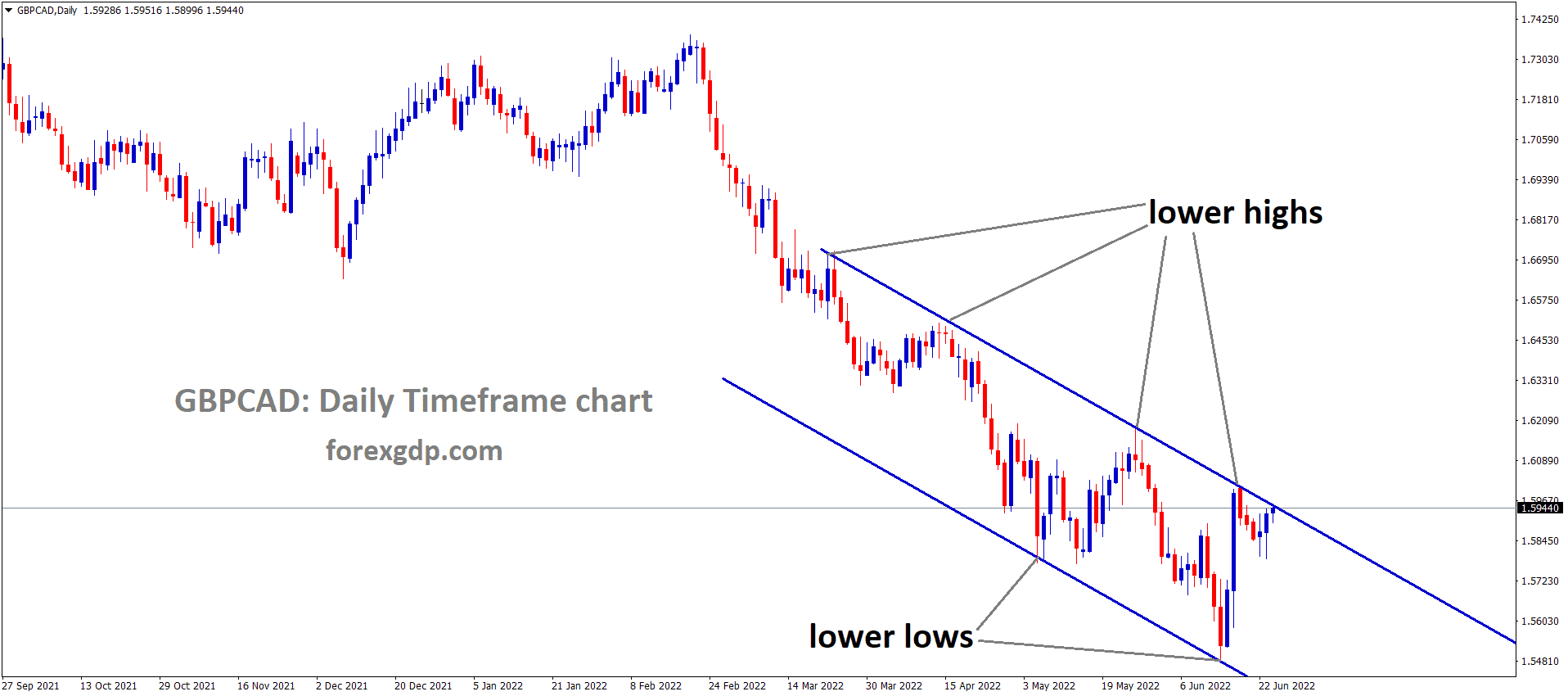

GBPUSD Analysis

GBPUSD is moving in the Descending channel and the market has reached the lower low area of the channel

GBP is weak against the USD as a result of the Bank of England’s decision to keep interest rates unchanged last month. Additional tightening places the economy in a recessionary state as consumer spending falls and business operations slow.

The US Dollar USD is nearing a 10-month high as a result of the Federal Reserve’s Fed hawkish stance, and this is a key factor acting as a headwind for the GBP/USD pair. Investors appear to believe that the US Federal Reserve will continue to tighten monetary policy and keep interest rates higher for an extended period of time. Furthermore, several Fed officials recently backed the case for at least one more rate hike by the end of the year to return inflation to the 2% target. In addition, the most recent monthly JOLTS report revealed that there were an estimated 9.61 million open jobs in August, a significant increase from the previous month’s upwardly revised reading of 8.92 million openings. The data suggested that wage inflation is likely to return, forcing the Fed to extend the rate-hiking cycle into 2024.

This drives the yield on the benchmark 10-year US government bond to a new 16-year high and supports the USD.Meanwhile, the extended selloff in the US fixed-income market adds to worries about economic headwinds caused by rapidly rising borrowing costs. This, in turn, dampens investors’ appetite for riskier assets, benefiting the safe-haven Greenback yet again. Furthermore, the Bank of England’s BoE surprise on-hold decision in September continues to weigh on the British Pound GBP and contributes to the GBPUSD pair’s capitulation.

The aforementioned fundamental backdrop appears to be firmly in favour of bearish traders, though the daily chart’s oversold Relative Strength Index RSI warrants caution before positioning for any further losses. Market participants are now looking for fresh imputes ahead of the US macro data – the ADP report on private-sector employment and the ISM Services PMI – later in the early North American session.

AUDNZD Analysis

AUDNZD is moving in the Descending channel and the market has reached the lower high area of the channel

The Australian Dollar fell after the RBA maintained the interest rate at 4.10%. However, one more rate hike is expected before the end of the year. The Australian Dollar will be moving in this week ahead of US domestic news.

The Australian Dollar AUD is treading water in an attempt to snap a two-day losing streak. The AUDUSD pair, on the other hand, is under pressure due to risk-off sentiment and a stronger US Dollar USD. Furthermore, the pair fell following the Reserve Bank of Australia’s RBA interest rate decision on Tuesday. In the most recent policy meeting, Australia’s central bank chose to maintain the status quo, keeping the current interest rate at 4.10% unchanged. This decision may put pressure on the Australian couple. Nonetheless, a rate hike is possible, with expectations pointing to a peak of 4.35% by the end of the year. This forecast corresponds to the persistent rise in inflation above the target. The US Dollar Index DXY reached an 11-month high as a result of positive US employment data and higher US Treasury yields. US JOLTS Job Openings exceeded expectations, causing US yields to rise. The 10-year US Treasury yield has risen to its highest level since 2007.

Furthermore, market concern about the US Federal Reserve’s Fed interest rate trajectory is contributing to the Greenback’s positive sentiment. The RBA chose to keep the Official Cash Rate OCR at 4.10%, in line with widely held expectations, which may put pressure on the Australian Dollar. Michele Bullock, the newly appointed governor of the RBA, stated in her inaugural monetary policy statement that additional tightening of monetary policy may be required.Bullock stated that recent data point to inflation returning to the target range. While inflation in Australia has peaked, it remains high and is expected to remain so for some time.

The 10-year US Treasury yield reached 4.85%, its highest level since 2007. US JOLTS Job Openings increased to 9.61M in August, up from 8.92M in July. The market anticipated a drop to 8.80M figures. Cleveland Federal Reserve President Loretta Mester stated on Tuesday that if the current economic situation holds, she is likely to favour an interest rate hike at the next meeting. Atlanta Fed President Raphael Bostic commented on the Federal Reserve’s policy outlook, saying, “I am not in a hurry to raise, and I am not in a hurry to reduce either.” He emphasised patience, indicating that there is no need for further action at this time. Traders are looking forward to the release of US employment data, which includes the ADP and ISM reports on Wednesday and the Nonfarm Payrolls on Friday. On Thursday, the Australian Trade Balance will be examined.

NZDUSD Analysis

NZDUSD is moving in the Box pattern and the market has reached the Support area of the pattern

Because the RBNZ Reserve Bank of New Zealand held the interest rate today, the NZD Dollar fell against other currencies.

The New Zealand dollar NZDUSD is losing ground for the third day in a row as a result of the US Federal Reserve’s (Fed) interest rate hike. Furthermore, the Reserve Bank of New Zealand (RBNZ) decided to maintain the Official Cash Rate (OCR) at 5.5%, as widely expected, adding to the pressure on the Kiwi pair.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/