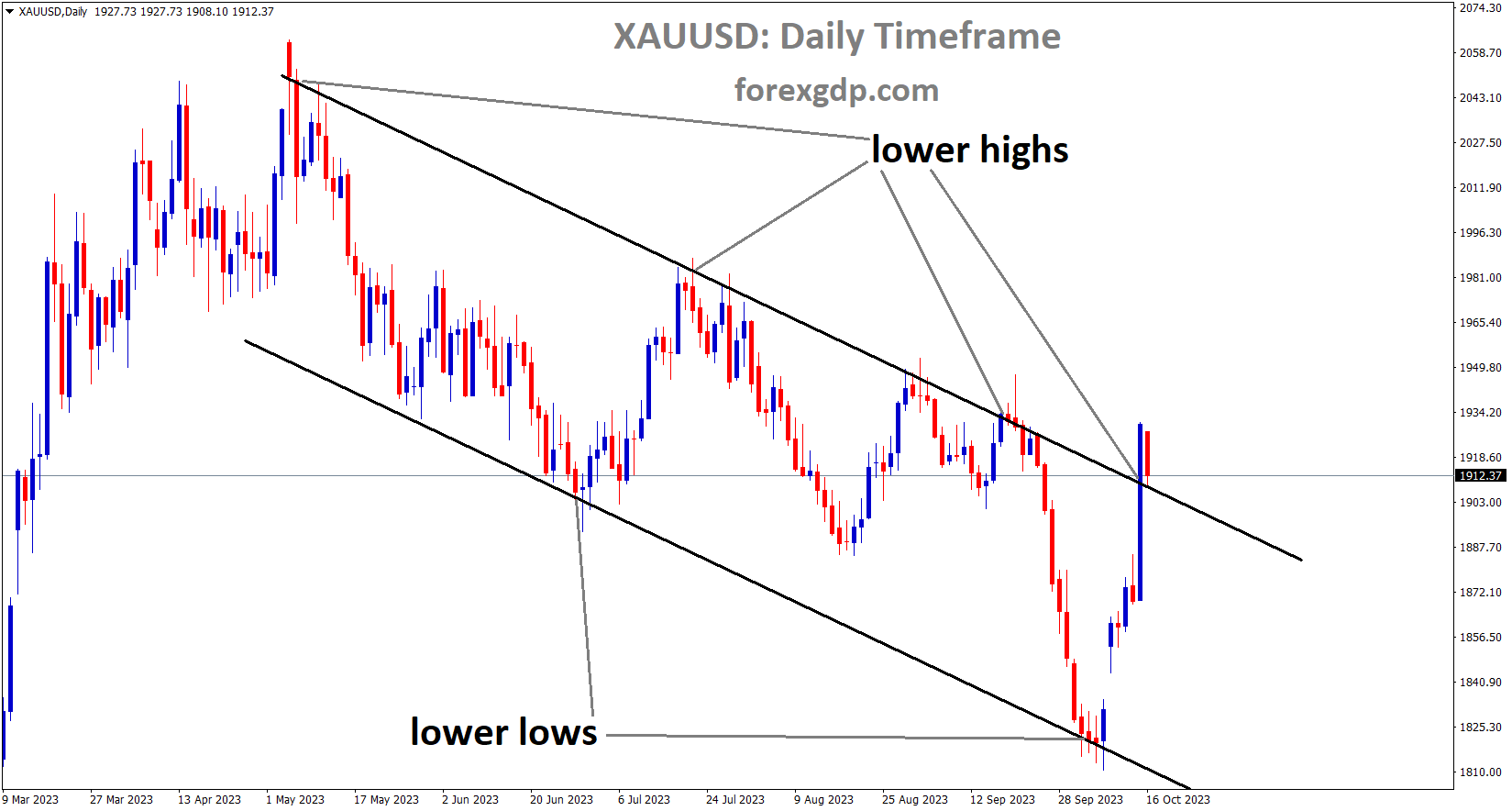

Gold Analysis

XAUUSD Gold price is moving in the Descending channel and the market has reached the lower high area of the channel

Gold prices have surged due to heightened tensions between Israel and Palestine, stoking fears of conflict. If these market uncertainties persist, they are likely to provide continued support for gold prices, pushing them into higher territory.

Gold prices have experienced a robust rally, primarily driven by increasing geopolitical tensions in the Middle East and growing expectations that the Federal Reserve (Fed) will refrain from further interest rate hikes this year. This precious metal saw a resurgence after a brief dip following the release of the United States Consumer Price Index (CPI) report for September, which revealed higher-than-expected headline inflation.

The rally in gold gained momentum as traders increasingly bet on the Fed maintaining the current interest rate levels at its November monetary policy meeting, especially after the CPI’s core inflation figures aligned with expectations. Although headline inflation exceeded consensus forecasts, driven in part by elevated global oil prices, gold quickly rebounded.

Additionally, Philadelphia Fed President Patrick Harker’s neutral commentary lent support to gold prices. Harker noted the absence of persistent inflationary concerns in recent data, suggesting that the central bank would likely keep interest rates unchanged.

The US Dollar and bond yields also saw a resurgence as stronger inflation data heightened the likelihood of an additional interest rate hike by the Fed in the latter part of 2023. The appeal of gold intensified further as geopolitical risks escalated with deepening tensions in the Middle East. Israel’s military actions in Northern Gaza added to the uncertainty.

Investor attention now shifts to Fed Chair Jerome Powell’s upcoming speech scheduled for next week. This speech will provide insights into the expected monetary policy actions at the November 1 meeting.

Gold prices surged sharply, nearing $1,920.00, recovering swiftly from the initial knee-jerk reaction triggered by the release of the US CPI data for September on Thursday. This precious metal is poised to deliver its strongest performance in seven months, fueled by the escalating Israel-Hamas tensions and growing confidence in the Fed’s decision to hold off on further interest rate increases.

The September inflation report revealed that headline inflation rose by 0.4%, surpassing expectations of 0.3%, mainly due to higher gasoline and food prices. The annual headline CPI remained steady at 3.7%, exceeding the anticipated 3.6%.

Both monthly and annual core inflation, excluding volatile oil and food prices, increased by 0.3% and 4.1%, respectively, in line with expectations.

The recovery of the US Dollar Index (DXY) to 106.60 from its 15-day low of 105.35 underscores increased confidence in the resilience of the US economy. Positive indicators include upbeat labor market conditions, improved factory activity, and a Services PMI above the 50.0 threshold.

Concerns about a global economic slowdown persist, as evidenced by stagnant inflation in China for September, falling short of the expected 0.2% growth. The Chinese economy continues to grapple with weak demand amid a rising unemployment rate.

The 10-year US Treasury yields experienced a robust revival, approaching 4.65%, as investors anticipated that inflationary pressures above the Fed’s desired 2% target could pose challenges for policymakers.

The persistent US inflation report has raised expectations of one more interest rate increase from the Fed in the remainder of 2023. According to the CME FedWatch Tool, there is a 92% chance of the Fed keeping interest rates unchanged at 5.25 to 5.50%, with around a 30% likelihood of an additional rate hike in either of the two remaining monetary policy meetings in 2023.

Some investors believe the Fed may opt for an additional 25 basis points (bps) rate hike to 5.50 to 5.75% later this year to ensure timely price stability. However, Boston Fed Bank President Susan Collins cautioned that further policy tightening could lose appeal if US bond yields remain elevated.

Fed Governor Christopher J. Waller advocates a “wait and watch” approach, as recent weeks have seen a sharp rise in 10-year US Treasury yields. The hope is that higher yields will help curb overall spending and investment, thereby contributing to inflation control.

Meanwhile, the University of Michigan reported a decline in the Consumer Confidence Index to 63.0 in October, compared to the expected 67.4 and the previous reading of 68.1.

On the employment front, the US Department of Labor revealed that Weekly Jobless Claims remained nearly unchanged, with 209K individuals claiming jobless benefits for the week ending October 6, slightly below the expected 210K.

Looking ahead, investors eagerly await Fed Chair Jerome Powell’s speech on October 19 before the Economic Club of New York, seeking insights into the monetary policy framework for November and the overall economic and inflation outlook.

Silver Analysis

XAGUSD Silver price is moving in the Descending channel and the market has reached the lower high area of the channel

The US Dollar index experienced a modest correction following remarks from a Federal Reserve (Fed) speaker who indicated the possibility of additional interest rate hikes. Ongoing concerns about conflict in Israel and a surge in oil prices have amplified uncertainties surrounding the Fed’s upcoming meeting.

The index has retraced some of its recent two-day recovery, hovering around the 106.80 mark, as riskier assets showed signs of improvement early this week. While the index managed to regain some ground lost since the beginning of the month late last week, the US dollar’s momentum has waned in line with a renewed dovish sentiment expressed by Federal Reserve officials. Furthermore, despite the prevailing assumption that the Federal Reserve will maintain its tighter-for-longer policy for the time being, the likelihood of another interest rate hike before the year’s end has recently diminished.

Additionally, escalating geopolitical tensions originating from the Middle East, coupled with an increase in risk aversion, continue to provide potential support for the US dollar.

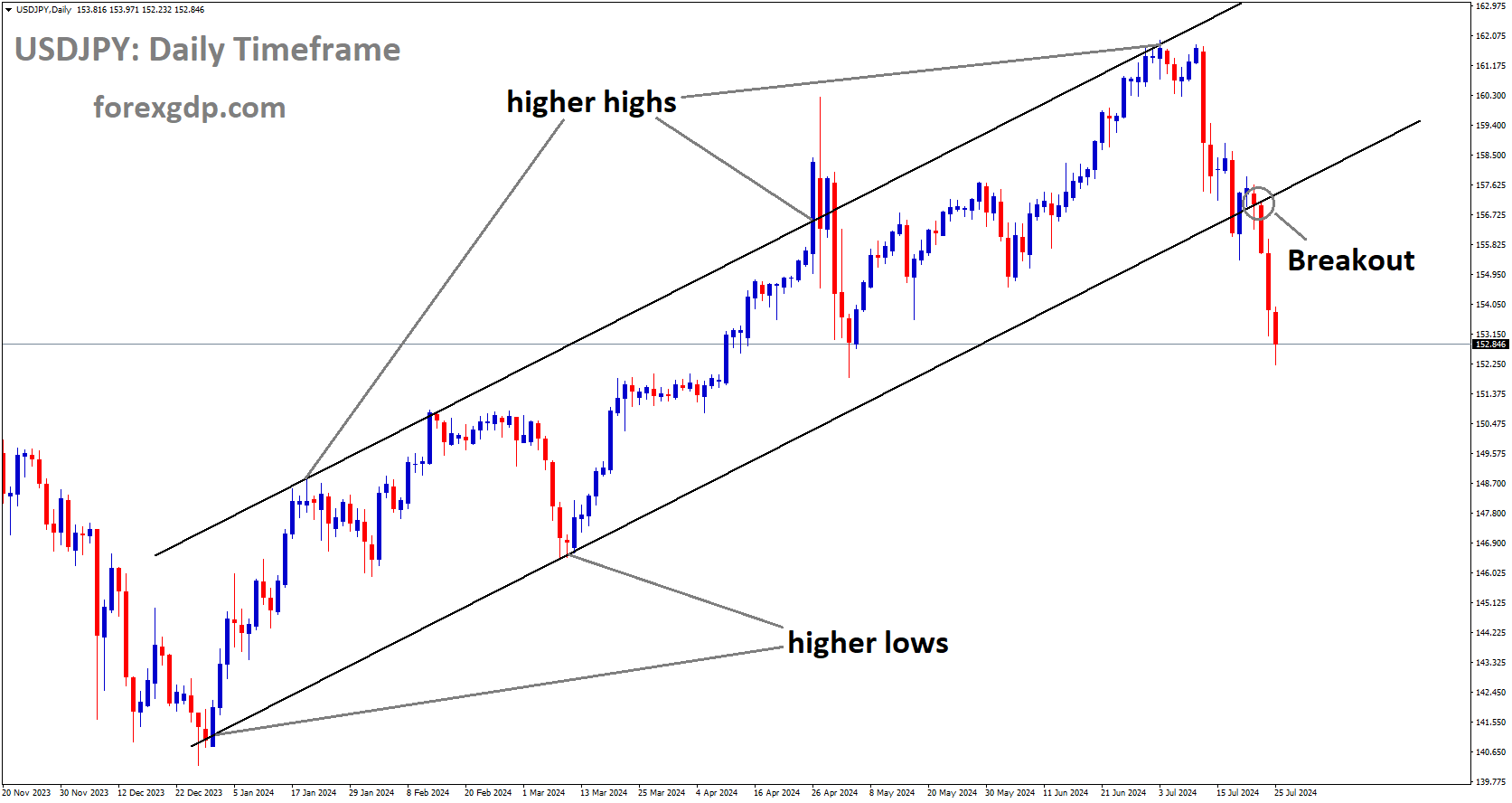

USDJPY Analysis

USDJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The Bank of Japan has emphasized the need for additional market intervention, affirming its commitment to maintaining existing stimulus measures. The Japanese Yen is gaining strength relative to other currencies due to heightened tensions in Israel.

The current environment for the US Dollar (USD) remains uncertain, largely influenced by the Federal Reserve’s (Fed) future decisions on interest rates. Several Fed officials have suggested that the central bank might hold off on a rate hike in November due to the recent surge in bond yields, which has tightened financial conditions. This uncertainty has kept the US Dollar Index (DXY) trading slightly lower, hovering around 106.50. Additionally, the USD faced challenges following the release of the preliminary US Michigan Consumer Sentiment Index for October, which showed a decline to 63.0 from the previous reading of 68.1, falling short of the expected figure of 67.4.

Amidst this uncertainty, the US Dollar may find support from safe-haven demand, given the escalating geopolitical tensions between Israel and Palestine. Reports suggest discussions have taken place between US officials and Israel regarding a potential visit by President Joe Biden to Israel, following an invitation from Israeli Prime Minister Benjamin Netanyahu.

Furthermore, the recent recovery in US Treasury yields from their recent losses may bolster the US Dollar (USD). As of Monday, the 10-year US Treasury bond yield stands at 4.65%, marking a 1.0% increase.

Meanwhile, the Bank of Japan (BoJ) is anticipated to intervene in the spot market to prevent further depreciation of the Japanese Yen (JPY). The BoJ has adopted a more dovish stance, eroding the safe-haven appeal of the JPY and providing support to the USD/JPY currency pair. The central bank has maintained its view that inflation is transitory and has not signaled any intentions to scale back its significant monetary stimulus measures.

According to S&P Global’s analysis of the Japanese economy and monetary policy, the rating agency expects that policy interest rates in Japan may start to rise in 2024.

Looking ahead, investors will closely watch the release of the US Retail Sales (MoM) data, with expectations for a 0.2% increase in September, compared to the previous reading of 0.6%. Additionally, attention will be focused on Japan’s Merchandise Trade Balance Total for September.

USDCHF Analysis

USDCHF is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

Swiss producer and import prices have dropped to 1.0%, down from a 0.80% decline in the previous month. The ongoing conflict in Israel is bolstering the appeal of safe-haven currencies, such as the Swiss Franc (CHF).

The ongoing uncertainty surrounding the Federal Reserve’s (Fed) future decisions on interest rates has created a complex and fluctuating environment for the US Dollar (USD). Concurrently, the Swiss Franc (CHF) appears to be gaining buying support in light of the ongoing military conflict in the Middle East, as it is traditionally considered a safe-haven currency during times of geopolitical turmoil. Investors seeking refuge in a stable and secure currency may be contributing to the strength of the CHF in the current geopolitical landscape.

Recent reports, citing an undisclosed source, have indicated discussions between US officials and Israel regarding the potential visit of President Joe Biden to Israel. This reported invitation comes from Israeli Prime Minister Benjamin Netanyahu.

In economic news, the Swiss Producer and Import Prices (YoY) data for September showed a decline of 1.0%, marking an increase from the previous month’s 0.8% decline. Meanwhile, the monthly data indicated a minor decrease of 0.1%, contrasting with the 0.8% decline observed in August. The Trade Balance for September is scheduled for release later in the week.

data for September showed a decline of 1.0%")

On the US front, multiple Fed officials have signaled the possibility of delaying a rate hike scheduled for November due to the recent surge in bond yields, which has led to tightened financial conditions. This development has acted as a headwind for the USD/CHF currency pair.

The US Dollar (USD) has faced challenges following the release of the preliminary US Michigan Consumer Sentiment Index for October, which showed a decline to 63.0 from the previous reading of 68.1, falling short of the expected 67.4. Consequently, the US Dollar Index (DXY) is trading slightly lower, hovering around the 106.50 level.

However, the recovery in US Treasury yields from recent losses may help support the Greenback. As of the latest data, the 10-year US Treasury bond yield stands at 4.67%, marking a 1.37% increase.

Looking ahead, market participants are keenly awaiting the release of US Retail Sales (MoM) data on Tuesday, with expectations for a 0.2% rise in September compared to the previous reading of 0.6%. This data release has the potential to influence market dynamics in the coming days.

EURUSD Analysis

EURUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

Economists at SoCGen have indicated that the European Central Bank (ECB) is unlikely to consider further tightening of monetary policy until the end of the year. This cautious stance is attributed to the economic recession in Germany and a general slowdown in domestic data across the Euro Zone.

Anatoli Annenkov, an economist at Société Générale, highlights looming threats to the Eurozone’s anticipated “soft landing” in the economic outlook, alongside growing concerns about potential upside risks to inflation. The European Central Bank (ECB) has primarily employed short-term policy rates to tighten monetary policy, but the recent increases in long-term bond yields have become increasingly significant since the last ECB meeting.

Given this evolving landscape, Annenkov suggests that the ECB should adopt a wait-and-see approach until there is more clarity regarding the economic outlook, possibly postponing any policy adjustments until March of the following year. The ECB surprised many last month when it suggested that further rate hikes might not be necessary, even before a clear upturn in core inflation, and without a defined tool to communicate an expected rate path. Concerns have persisted about the limited transmission of tighter policy to the longer end of the yield curve, with tepid quantitative tightening (QT) support.

is unlikely to consider further tightening of monetary policy until the end of the year")

Long-term bond yields have continued to rise since the September meeting, with Bund yields climbing nearly 40 basis points until early October. This surge has been driven by factors such as a supply/demand imbalance, inflation worries, and expectations of prolonged higher interest rates. The increasing long-term yields are likely to dampen calls for immediate policy tightening.

Furthermore, recent data releases have generally supported the ECB’s decision to pause tightening measures. However, the next comprehensive data on the state of the economy won’t be available until after the October meeting, with a full set of third-quarter GDP data expected by early December. Given the widely anticipated moderation in core inflation in the coming months, the March 2023 ECB staff projections may provide a more opportune time to evaluate the economic outlook.

Regarding the use of QT as a tool to combat inflation, the ECB has downplayed its effectiveness. Nevertheless, as policy normalization progresses, there may be slightly higher QT flows next spring, particularly with the conclusion of full reinvestments of the Pandemic Emergency Purchase Programme (PEPP) after a review of the operational framework. Moreover, to mitigate potential political backlash stemming from rising losses over the coming years, it’s possible that the ECB may agree to increase the minimum reserve requirement next year, with the impact on overnight rates dependent on the extent of this adjustment. Despite these measures, mounting losses could pose a political and public image challenge for the ECB for some years to come.

EURCAD Analysis

EURCAD is moving in the Descending triangle pattern and the market has rebounded from the support area of the pattern

Bank of Canada Governor Tiff Macklem has stated that the recent increase in long-term bond yields does not signal an impending recession in Canada. Instead, it provides an opportunity to consider tightening financing conditions during this month’s Bank of Canada (BoC) meeting. The surge in oil prices is contributing to the rise in the Consumer Price Index (CPI) in Canada.

Regarding the Canadian Dollar , Bank of Canada (BoC) Governor Tiff Macklem commented last Friday that the recent uptick in long-term bond rates should not be seen as a replacement for monetary policy, and there is no immediate recession on the horizon for the Canadian economy. Macklem further noted that the central bank would carefully consider the implications of tightening financial conditions resulting from the rising long-term bond rates in the lead-up to its upcoming policy meeting on October 25.

Simultaneously, the recovery in oil prices is providing a boost to the commodity-linked Canadian Dollar, given Canada’s status as a prominent oil exporter to the United States. It’s worth noting that crude oil markets are recuperating from the impact of geopolitical tensions in the Middle East. This favorable development could potentially elevate the value of the Canadian Dollar (CAD).

GBPUSD Analysis

GBPUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

In October, the UK’s Rightmove house price index showed a month-on-month increase of 0.50%, up from the previous month’s 0.40%. However, on an annual basis, it declined by 0.80%, compared to the previous figure of 0.40%. Bank of England Governor Bailey has stated that further tightening of monetary policy is not feasible until the end of the year, and the central bank is patiently waiting for inflation to return to its 2.0% target.

The GBPUSD pair receives some support from the weaker US Dollar (USD). Market sentiment dominates as traders await key UK employment data and US Retail Sales figures scheduled for release on Tuesday. Recent data from Monday revealed that the UK’s Rightmove House Price Index increased by 0.5% month-on-month (MoM) in October, up from the previous 0.4%.

However, on an annual basis, the index declined by 0.8%, compared to the 0.4% drop in the previous reading. Over the weekend, Bank of England (BoE) Governor Andrew Bailey, during his remarks at the International Monetary Fund meetings in Morocco, expressed concerns about rising borrowing costs affecting the housing market and employment. He indicated that interest rates are likely to remain at the current 5.25%, as restrictive policy measures are necessary to bring inflation back to the 2% target.

GBPCHF Analysis

GBPCHF has broken the Box pattern in downside

On the other side of the Atlantic, investors are anticipating a potential interest rate hike by the Federal Reserve (Fed) before the year’s end, driven by higher inflation expectations and strong inflation data from the previous week. The University of Michigan (UoM) reported that one-year inflation expectations climbed from 3.2% to 3.8%, while five-year inflation estimates rose from 2.8% to 3%. Nonetheless, the US Michigan Consumer Sentiment Index data for Friday fell to 63.0 from the previous 68.1, missing the expected 67.4. Additionally, the US Consumer Price Index (CPI) for September showed an annual increase of 3.7% and a monthly increase of 0.4%. However, the dovish comments from Fed officials could temper the enthusiasm of bullish traders. Market participants will closely monitor the release of UK employment data on Tuesday. The Employment Change is expected to decline by 195,000 in August, and the ILO Unemployment Rate (3M) is expected to remain at 4.3%. Furthermore, US Retail Sales figures are set to be released, with an expected increase of 0.2%. These data points may provide clearer direction for the GBP/USD pair.

AUDCHF Analysis

AUDCHF is moving in the Descending channel and the market has rebounded from the lower low area of the channel

The RBA has the potential to introduce a digital currency into the market. According to Brad Jones, the assistant governor of the RBA, the era of digital asset tokenization is expected to arrive in the coming year.

Economists at UOB anticipate that China’s exports and imports are expected to show improvement this year, with exports shifting from a decline of -6.0% to -4.5%, and imports improving from -7.0% to -6.0%. However, it’s worth noting that China is currently grappling with an interest rate differential compared to other countries.

The Australian Dollar began the week by rebounding from a three-day losing streak, showing strength against the US Dollar on Monday. This currency pair faced challenges, possibly linked to shifting discussions regarding the US Federal Reserve’s (Fed) monetary policy trajectory. Investors will be closely monitoring the Reserve Bank of Australia’s (RBA) Meeting Minutes set for release on Tuesday, as well as employment data later in the week.

The RBA is also exploring the possibility of introducing a central bank digital currency (CBDC). Brad Jones, Assistant Governor (Financial System) at the RBA, discussed the tokenization of assets and money in the digital era at The Australian Financial Review Cryptocurrency Summit. Governor Jones highlighted the potential for tokenized money to yield significant cost savings, potentially amounting to billions of dollars, in the domestic financial markets.

On a related note, the National Bureau of Statistics of China reported a decrease in Chinese inflation for September. This development could exert downward pressure on the Australian Dollar (AUD) and indicates ongoing economic challenges despite recent government stimulus efforts aimed at achieving a 5% growth target.

The US Dollar Index (DXY) gained momentum after robust US data releases during the previous week, with US inflation exceeding expectations and initial jobless claims coming in lower than anticipated. Investor sentiment appears to incorporate the possibility of another Federal Reserve (Fed) interest rate hike. Additionally, the rebound in US Treasury yields from recent losses may provide support for the US Dollar (USD), which is also benefiting from safe-haven demand amidst rising geopolitical tensions between Israel and Palestine.

Australian Consumer Inflation Expectations for October were reported at 4.8%, showing a slight increase from September’s figure of 4.6%. The previous rebound in inflation, primarily driven by elevated oil prices in August, raises the likelihood of another interest rate hike by the RBA.

Chinese Consumer Price Index (CPI) data for September came in at 0% (YoY), declining from the previous reading of 0.1% and falling short of market expectations of a 0.2% increase. Additionally, the Producer Price Index dropped to 2.5% from a 3% decline in August, missing the expectation of a 2.4% downturn.

")

The ongoing conflict in the Middle East adds another layer of complexity to the situation. This geopolitical factor could potentially prompt the RBA to implement a 25 basis points (bps) interest rate hike, reaching 4.35% by year-end.

There have been discussions between US officials and Israel about a possible visit by US President Joe Biden to Israel, reportedly initiated by Israeli Prime Minister Benjamin Netanyahu, according to an undisclosed source cited by Reuters.

US Consumer Price Index data for September exceeded forecasts, with annual figures expanding at a consistent rate of 3.7%, slightly surpassing estimates of 3.6%. US Initial Jobless Claims for the week ending on October 6 showed a slight decrease, despite an increase of 209K, slightly below the forecasted 210K.

Finally, on Friday, the preliminary US Michigan Consumer Sentiment Index for October showed a decline to 63.0 from the previous reading of 68.1, falling short of the expected figure of 67.4. US Treasury bond yields also saw a recovery on Monday, with the 10-year US Treasury bond yield standing at 4.66%, up by 1.04%. Investors will closely monitor the release of US Retail Sales data on Tuesday, with an expected rise of 0.2%. Additionally, the Reserve Bank of Australia (RBA) meeting minutes and employment data are scheduled for release in the coming week, which will be important data points to watch.

UOB Group Economist Ho Woei Chen, CFA, provides an analysis of the latest trade balance data from the Chinese economy. In terms of USD, both exports and imports experienced a contraction of -6.2% year-on-year in September, although the declines showed some narrowing compared to the previous month.

There is a growing belief that China’s export outlook is gradually improving. However, the pace of this recovery remains vulnerable to various risks, including tightening financial conditions in developed markets, global inflationary pressures, and ongoing geopolitical tensions. On the other hand, the relatively modest improvement in imports, despite a substantial volume of commodity purchases in September, may indicate a less optimistic outlook for domestic demand in general.

Considering the more favorable base effect for the remainder of the year, it is expected that both exports and imports will continue to exhibit improved performance. Consequently, there is a revision in the forecast for exports, which is now projected to decline by -4.5% (up from -6.0%), and for imports, which are forecasted to decrease by -6.0% (an improvement from -7.0%) in 2023.

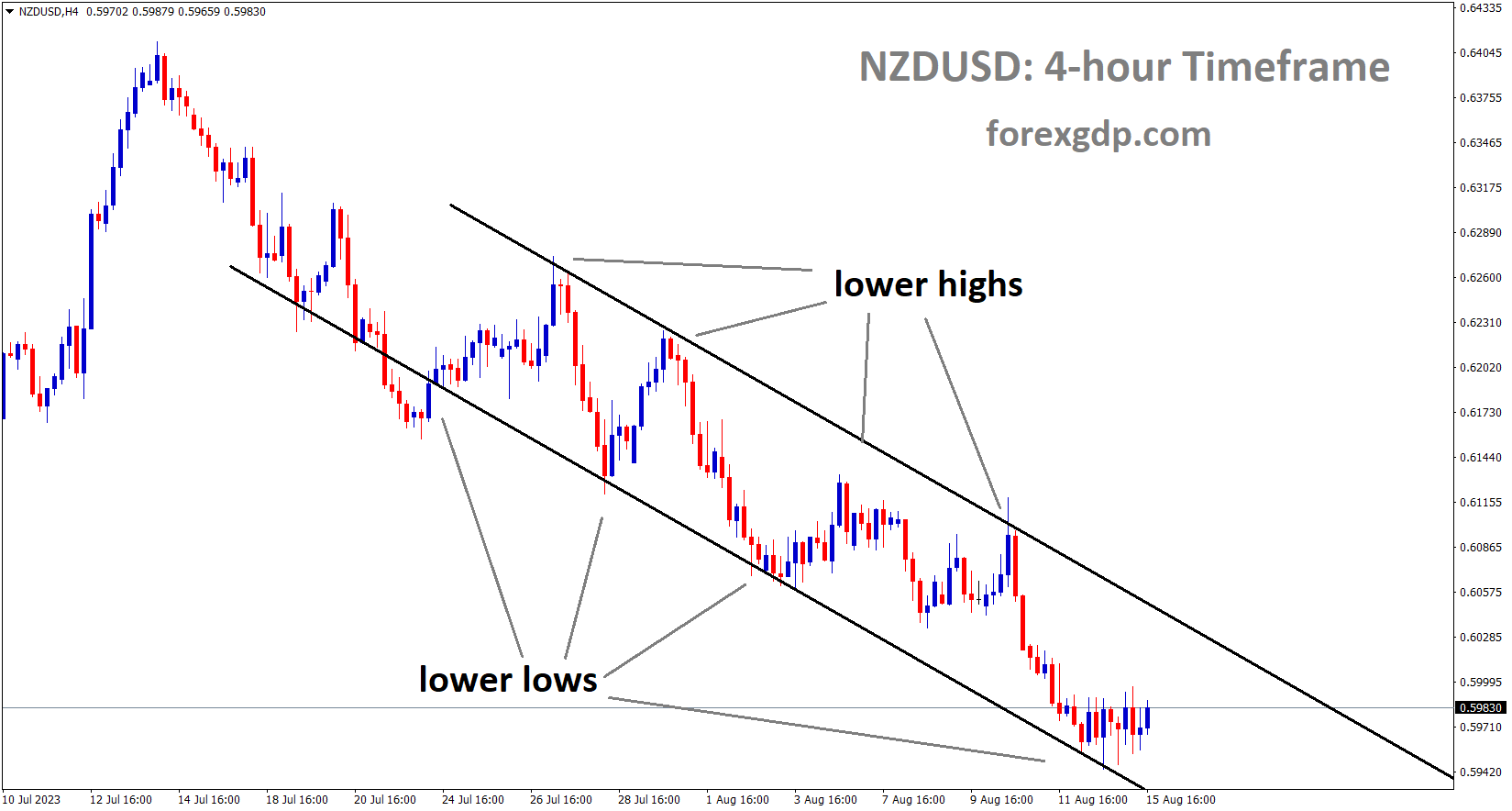

NZDUSD Analysis

NZDUSD is moving in the Box pattern and the market has rebounded from the support area of the pattern

The election results strongly favor the opposition party, and with Q3 CPI data set to be released this month, it is evident that the Reserve Bank of New Zealand (RBNZ) does not have any immediate plans for further tightening until inflation shows signs of coming down.

NZDUSD concluded the week with a significant decline. ANZ Bank’s economists assess the outlook for the New Zealand Dollar (Kiwi). While the Kiwi hasn’t precisely formed a triple-bottom pattern, it has come close, and the technical outlook could turn negative if it establishes a new cycle low.

Although there were some surprising elements in the election outcome, it largely aligned with the polls. The robust performance of the opposition party has removed a source of uncertainty, despite ongoing coalition talks. Today, the Q3 CPI data is set to be released, and it holds significant importance for the Reserve Bank of New Zealand (RBNZ), which, in turn, affects short-term interest rates and the Kiwi’s performance.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/