USDCAD Analysis

USDCAD is moving in the Descending channel and the market has fallen from the lower high area of the channel

Bank of Canada Deputy Governor Vincent has noted that the Israel conflict is causing a supply shock and increased demand for oil. Tomorrow, Canadian CPI data is scheduled for release, and based on this data, the Bank of Canada will consider potential actions in its upcoming meeting next week.

USDCAD has extended its decline that began on Friday, moving further away from the 1.3700 level. This unexpected development coincides with a struggle in oil prices, following a 5% surge on Friday that marked a strong close to the week. The Bank of Canada (BoC), like many central banks worldwide, is closely monitoring geopolitical events that could potentially impact inflation. This scrutiny comes shortly after warnings from BoC Deputy Governor Nicolas Vincent, who cautioned that supply disruptions, limited competition, and technological changes might have permanently altered the pricing landscape. Deputy Governor Vincent also expressed concern about the possibility of companies continuing to raise prices at a faster and more substantial pace in the future.

Canadian inflation data is set to be released tomorrow, providing valuable insights. The consensus for year-on-year headline inflation is at 4%. The Bank of Canada (BoC) will likely be hoping for an inflation reading of 4% or lower, considering the upward trajectory of the headline figure since hitting a year-to-date low of 2.8% in June. If there is an acceleration in tomorrow’s data, it could lead to a hawkish revaluation of rate hike expectations for the BoC.

Gold Analysis

XAUUSD Gold price is moving in the Descending channel and the market has reached the lower high area of the channel

Gold prices are maintaining their stability as tensions in Israel escalate, with the growing presence of Iran in the conflict expected to further bolster this trend.

A positive risk tone that tends to undermine traditional safe-haven assets is pushing the precious metal to hold its offered tone going into the European session. Aside from that, rising US Treasury bond yields, bolstered by firming expectations for further Fed policy tightening, are another factor weighing on the non-yielding yellow metal. The downside for the gold price, on the other hand, is mitigated by the raging Israel-Hamas conflict. This, combined with growing consensus that the Federal Reserve (Fed) will leave interest rates unchanged for the second time in a row in November, should provide some support for the XAU/USD. Meanwhile, dovish Fed expectations keep bulls of the US Dollar (USD) on the defensive, limiting losses for the US Dollar-denominated commodity. Before placing directional bets, traders may also prefer to wait for clues about the Fed’s future rate-hike path. As a result, the focus will remain on Fed Chair Jerome Powell’s scheduled speech on Thursday, which will determine the next leg of the gold price’s directional move. Meanwhile, Tuesday’s US economic calendar, which includes monthly Retail Sales and Industrial Production figures, will be scrutinised for any impetus.

In the aftermath of the ongoing conflict between Israel and Hamas, which could escalate into a larger proxy war with Iran, the gold price may continue to attract some haven flows. The chief of the Israel Defence Forces has stated that the army will soon enter Gaza to decimate the Hamas terror group. Israel had urged Palestinians to flee to the southern enclave of Gaza City ahead of a large-scale ground assault against the terror attacks. The office of Israeli Prime Minister Benjamin Netanyahu has denied reports of a cease-fire to allow humanitarian aid in and Gaza residents with international passports to flee to Egypt. President Biden will visit Israel on Wednesday, according to Secretary of State Antony Blinken, to send a strong message of support to a key US ally. As part of its efforts to deter Iran and its proxies from expanding the conflict, the US military dispatched a second carrier strike group to the Eastern Mediterranean.

Iran has repeatedly warned that a ground invasion of the long-blocked Gaza Strip would be met with retaliation on other fronts. “The possibility of pre-emptive action by the resistance axis is expected in the coming hours,” Hossein Amir-Abdollahian, Iran’s foreign minister, said on Monday. In the absence of a change in the data, Philadelphia Fed President Patrick Harker stated on Monday that the central bank should keep rates steady. The US consumer inflation figures released last week, on the other hand, left the door open for another Fed rate hike before the end of the year. Prospects for further Fed policy tightening continue to support elevated US bond yields and act as a tailwind for the US Dollar. Traders are now looking for some impetus from the US Retail Sales data, though the focus will remain on Fed Chair Jerome Powell’s scheduled speech on Thursday. Retail sales in the United States are expected to rise by 0.3% in September, while sales excluding automobiles are expected to rise by 0.2% in the same month.

Silver Analysis

XAGUSD Silver Price is moving in the Descending channel and the market has reached the lower high area of the channel

Economists from Commerz Bank have noted that the demand for US dollars is primarily driven by the ongoing conflicts between Israel and Palestine. Additionally, they believe that if economic data continues to show a soft landing, it could further bolster the strength of the US Dollar, extending its positive performance over a longer period.

Economists at Commerz Bank have pointed out that the demand for US dollars is primarily linked to the ongoing conflicts between Israel and Palestine. Furthermore, they suggest that if economic data continues to indicate a soft landing, it could contribute to the US Dollar maintaining its positive momentum for an extended period.

Turning to the upcoming data calendar, the release of retail sales and industrial production figures in the US is anticipated, which is expected to garner market attention. A stronger indication of a soft landing in the economy would likely benefit the USD, as it would imply the Federal Reserve is less likely to reduce its key interest rates in the near future.

However, while disappointing data could emerge today, it is unlikely to deter economic optimists significantly, and therefore, it is unlikely to exert substantial downward pressure on the USD. Additionally, as long as the Middle East conflict persists without any signs of easing, the US Dollar is likely to continue experiencing demand in the market.

USDJPY Analysis

USDJPY is moving in an Ascending channel and the market has reached the higher low area of the channel

The United States has deployed 2,000 Marines to Israel in a move aimed at bolstering its readiness amid concerns about potential security threats emanating from Iran and Lebanon.

Finance Minister Shunuchi Suzuki of Japan has stated that there is no current necessity for foreign exchange (FX) intervention in the market. He refrained from providing any comments regarding the International Monetary Fund’s (IMF) statement on the topic of intervention.

As reported by CNN, the United States is dispatching a rapid response force of 2,000 Marines and sailors to the waters off the coast of Israel. This deployment is part of a growing presence of US warships heading toward Israel, with the intention of conveying a strong deterrent message to Iran and the Lebanese militant group Hezbollah, as confirmed by a defense official familiar with the operation.

Japanese Finance Minister Shunichi Suzuki, when asked about recent statements from an International Monetary Fund (IMF) official regarding currency intervention, chose not to provide additional comments. He did, however, emphasize that it was unnecessary to delve into the specific factors influencing currency movements. As of now, there are no further statements from the Japanese official on this matter. The IMF official had previously noted over the weekend that the recent decline in the Yen was attributed to fundamental factors, and the criteria for intervention had not been met.

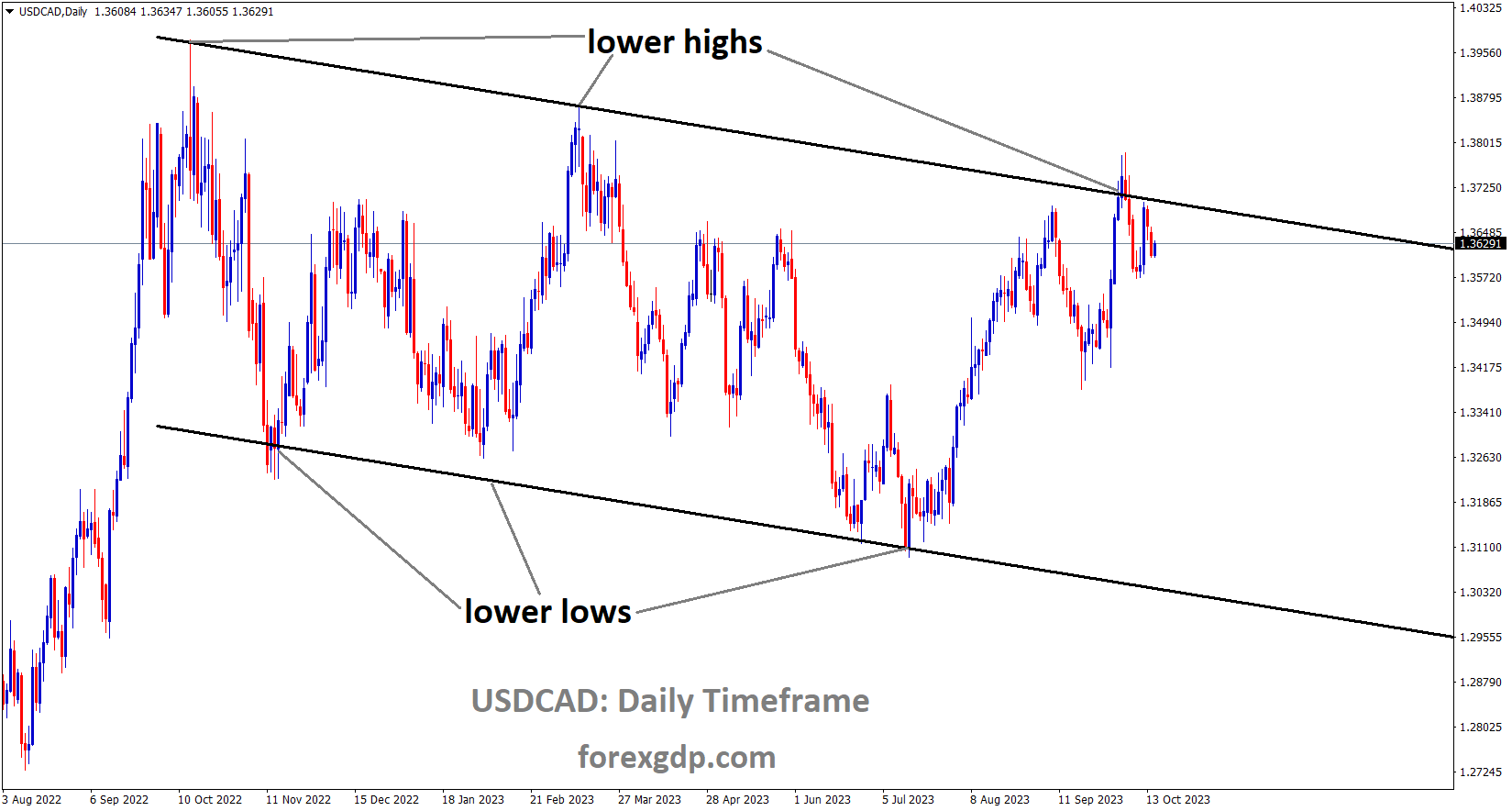

USDCHF Analysis

USDCHF is moving in an Ascending channel and the market has reached the higher low area of the channel

Due to concerns about potential conflict, safe-haven currencies such as the Swiss Franc have seen increased appreciation against their counterparts. Additionally, the US NY Manufacturing index experienced a decline, dropping from 1.9 in the previous reading to 4.6.

The recovery in US Treasury yields lends some support to the pair. Meanwhile, the US Dollar Index DXY, which measures the value of the USD relative to a basket of foreign currencies, is attracting some buyers at 106.32. The US Treasury yield recovers its losses, with the 10-year yield remaining at 4.746% as of press time. On Monday, the US NY Empire State Manufacturing Index for October fell to 4.6 from 1.9 the previous month, exceeding the market consensus of a 7.0 decline. The positive low-tier US economic data failed to lift the Greenback, and the Fed’s dovish comments continue to weigh on the pair. Chicago Fed President Austan Goolsbee maintained his dovish stance, saying that a drop in US inflation is not a blip, while Philadelphia Fed President Patrick Harker stated that the Fed should keep rates steady in the absence of a change in the data. Traders will take more cues from Fed speakers on Tuesday, including Williams, Bowman, Barkin, and Kashkari, who may offer hints about future monetary policy paths.

The US Marine Rapid Response Force will arrive in Israeli waters early Tuesday. A rapid response force of 2,000 Marines and sailors has been dispatched. According to CNN, it will join a growing number of US warships en route to Israel in an effort to send a deterrent message to Iran and the Lebanese militant group Hezbollah. However, rising geopolitical tensions between Israel and Hamas may boost the traditional safe-haven Swiss Franc while acting as a headwind for the USDCHF pair. Concerning the data, the Swiss Federal Statistical Office revealed on Friday that the country’s Producer and Import Prices fell 1.0% YoY in September, compared to the previous reading of a 0.8% drop. Monthly, the figures fell 0.1%, compared to a 0.8% drop the previous month. Investors will be watching the headlines about the Israel-Hamas conflict. The US Retail Sales for September will be released on Tuesday, with a 0.2% increase expected. The Swiss Trade Balance for September is due on Thursday. These figures may provide a clear direction for the USDCHF pair.

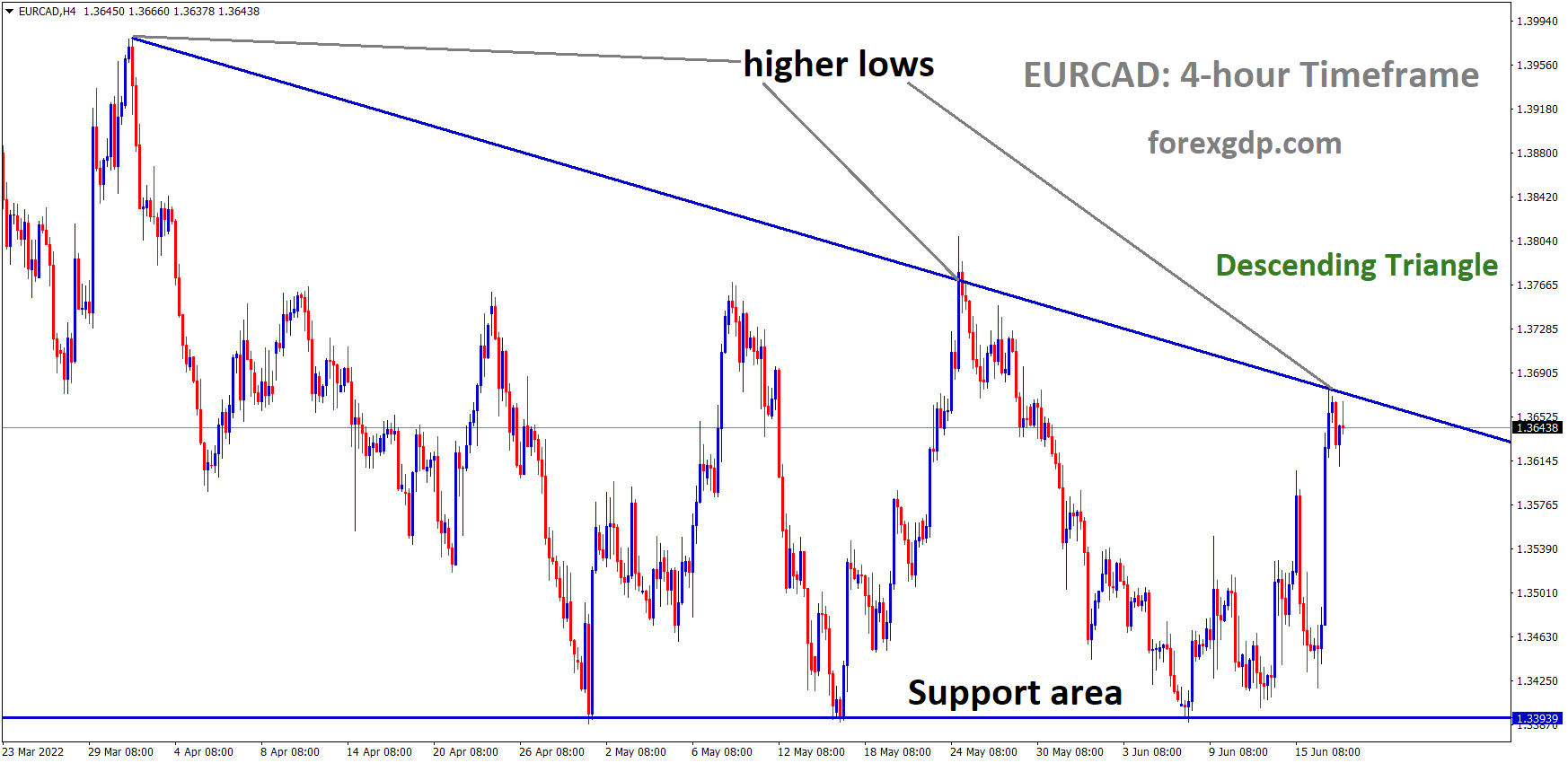

EURCAD Analysis

EURCAD is moving in the Descending Triangle and the market has rebounded from the support area of the pattern

In September, the German wholesale price index increased to 0.20%, falling slightly short of the expected 0.30%. On an annual basis, it declined to -4.1% from the previous -2.7%. The appreciation in oil prices is likely to exert downward pressure on Euro pairs.

Investors are eagerly awaiting the release of the ZEW Economic Sentiment Survey for October, with expectations that it will improve from -8.9 to -8.0. Currently, the major currency pair is trading at around 1.0559, experiencing a slight 0.02% loss for the day.

European Central Bank (ECB) President Christine Lagarde has conveyed to euro-area finance ministers that the ECB is closely monitoring energy prices and the ongoing conflict in Israel for potential inflation risks. In the meantime, ECB’s Chief Economist Philip Lane, in an interview, discussed how the ECB’s decision to raise interest rates took longer than the Federal Reserve (Fed) due to various factors. Lane emphasized that they intend to maintain high interest rates until inflation returns to 2%, although this may take some time.

On the economic front, data from Monday revealed that German Wholesale Prices increased by 0.2% on a month-on-month basis in September, falling slightly short of the market consensus of a 0.3% rise. On an annual basis, the figure declined by -4.1% compared to the previous reading of -2.7%. Looking ahead, market participants will closely monitor the ZEW Economic Sentiment Survey for October

GBPJPY Analysis

GBPJPY is moving in the Descending channel and the market has fallen from the lower high area of the channel

The UK’s Consumer Price Index (CPI) data for the third quarter is set to be released tomorrow. However, the recent increase in oil prices is expected to have a negative impact on the data in the upcoming quarter. The Bank of England has indicated its intention to keep interest rates unchanged until inflation subsides.

Wednesday’s upcoming UK inflation data is expected to show decreases in both headline and core inflation. However, there is a potential risk of an upside surprise in the headline measure due to recent spikes in oil prices, which include volatile items like food and fuel. The UK has experienced a more prolonged period of elevated inflation than initially anticipated. The Bank of England has consistently maintained that inflation would eventually see substantial declines due to base effects and a more stable energy market.

Additionally, the pace at which average earnings are rising is a concern for the Bank of England. The latest data indicates a 3-month average earnings growth (including bonuses) of 8.5% year-on-year. Given the central bank’s stance on keeping interest rates unchanged at their current levels, policymakers are likely hoping for a continued downward trend in overall prices. Some positive developments have emerged in the form of weaker job data, which the bank anticipates will contribute to bringing inflation closer to its 2% target.

AUDUSD Analysis

AUDUSD is moving in the Descending channel and the market has rebounded from the lower low area of the channel

The RBA Meeting Minutes reveal that interest rates will be maintained in the upcoming months due to a cooling trend in inflation data.

The Reserve Bank of Australia (RBA) released the minutes of its October monetary policy meeting on Tuesday, emphasizing that the case for keeping interest rates unchanged was stronger. Additional insights from the RBA minutes indicated that more comprehensive data on inflation, employment, and updated forecasts would be available at the November meeting. During the October meeting, the board had deliberated between raising rates by 25 basis points or maintaining the status quo.

Board members collectively assessed that the rationale for keeping interest rates steady carried more weight. They also took note that data concerning inflation, employment, and updated economic projections would be accessible for review at the upcoming November meeting.

Members acknowledged significant concerns regarding potential upside risks to inflation. Progress in reducing inflation in the service sector had been sluggish. The board had a limited tolerance for a slower return of inflation to the target range. They cautioned that if inflation persisted at higher levels than expected, additional tightening might be necessary.

AUDCHF Analysis

AUDCHF is moving in the Descending channel and the market has rebounded from the lower low area of the channel

The rising prices of houses had the potential to bolster consumption, potentially signaling that monetary policy might not be as restrictive as initially assumed. However, it was highlighted that the full effects of previous interest rate hikes might not become apparent in economic data for several months.

Data suggested that the Australian economy had continued to experience modest growth in the September quarter. Board members believed that the labor market had reached a turning point, though they noted few signs of a wage-price spiral taking shape.

The decline in the Australian dollar against the US dollar had somewhat eased monetary conditions, albeit only marginally. The trade-weighted Australian dollar remained only slightly lower than its level at the beginning of the year, which limited its impact on imported inflation.

Furthermore, the board expressed concerns about potential challenges in the Chinese economy and their possible spill-over effects on Australia if not adequately contained.

NZDUSD Analysis

NZDUSD is moving in the Box pattern and the market has reached the support area of the pattern

The third-quarter inflation data for the New Zealand Dollar came in at 5.6%, which was lower than the anticipated 5.9%. This reading led to a decline in NZD currency pairs against their counterparts.

Following the release of local inflation data, the New Zealand Dollar exhibited a cautious weakening.

In the third quarter, New Zealand’s Consumer Price Index (CPI) recorded a 5.6% increase compared to the previous year, which fell short of the expected 5.9% outcome. Additionally, when compared to the previous quarter, the headline inflation within the local economy expanded by 1.8%, slightly below the expected 1.9% result.

This data has resulted in a softer-than-anticipated inflation report, which holds significant implications for the Reserve Bank of New Zealand (RBNZ). The RBNZ utilizes interest rate adjustments to influence inflation and economic growth, effectively setting monetary policy. Given the CPI figures, the central bank may approach its policy decisions with more caution than previously anticipated. Consequently, this has tempered expectations of further interest rate tightening, potentially signaling a shorter duration of restrictive rates. These developments have, in turn, had a dampening effect on demand for the New Zealand Dollar, which is evident in the decline of NZDUSD following the release of the CPI report.

Considering these factors, the Kiwi Dollar may be susceptible to vulnerability in the near term, and it’s worth monitoring the evolving price action.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/