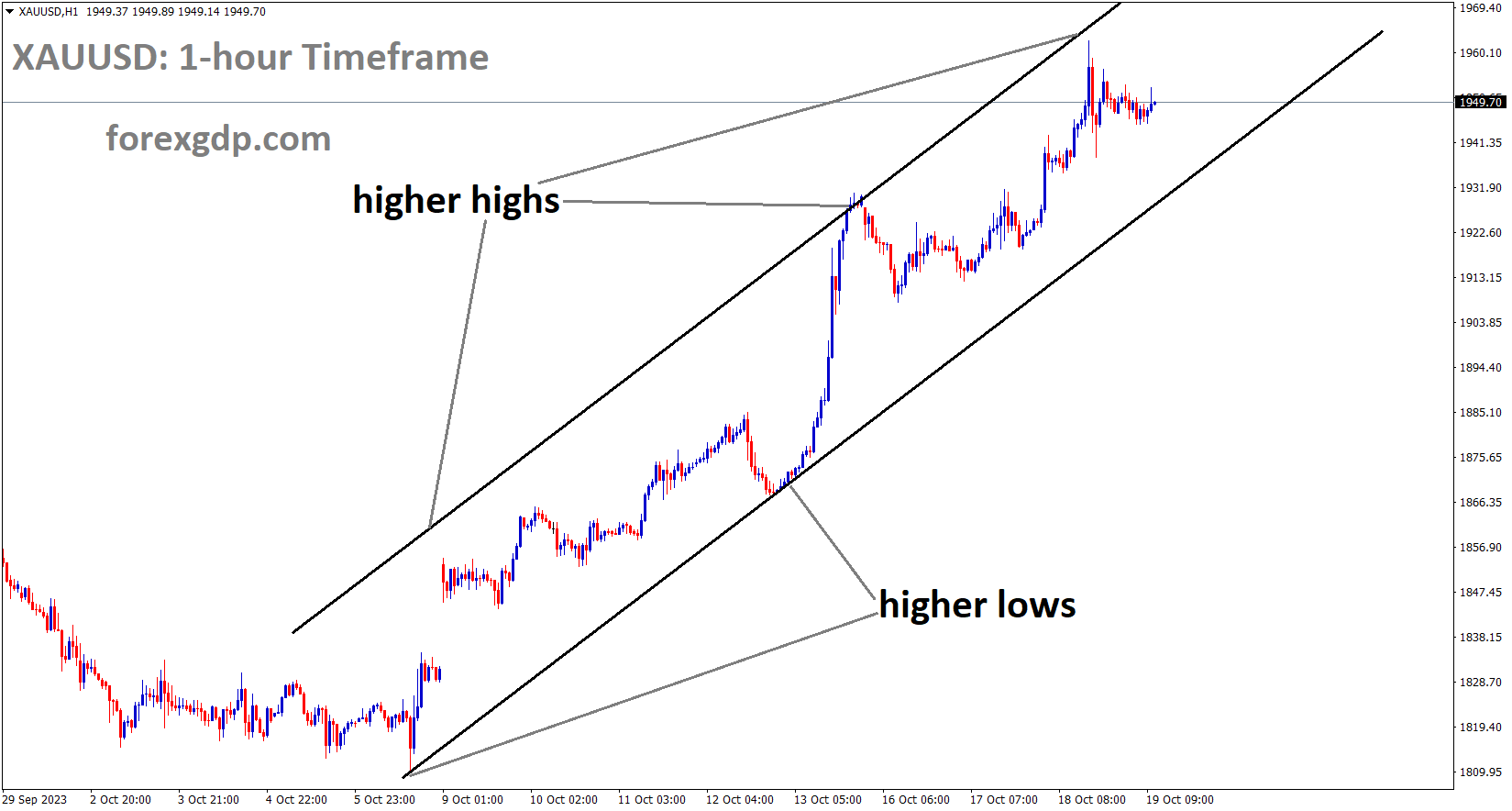

Gold Analysis:

XAUUSD Gold price is moving in an Ascending channel and the market has fallen from the higher high area of the channel

The escalating tensions surrounding the Gaza Hospital attack and the arrival of US President Joe Biden in Israel have heightened concerns in the Middle East. This increased sense of uncertainty in the market has driven up demand for safe-haven assets such as Gold.

Gold continued to advance throughout the day due to heightened risk aversion among market participants. The increase in risk aversion stemmed from a tragic incident involving the explosion of a hospital in Gaza last night, which led to Israel and Palestine trading accusations for the incident. This event had widespread implications, reigniting concerns of a broader conflict and propelling Gold towards the $1950 per ounce mark.

In contrast, the United States witnessed another week of positive economic data, with retail sales exceeding expectations. As a result, there has been a slight increase in expectations for a rate hike by the Federal Reserve at their December meeting. In the meantime, Federal Reserve policymakers have been actively sharing their views this week, with many not ruling out the possibility of additional rate hikes but emphasizing the importance of upcoming data. Federal Reserve policymaker Waller stated today that if the real economy experiences a slowdown, the Fed may choose to keep interest rates steady.

One noteworthy development highlighted by the Fed is the upward movement in longer-dated US Treasuries. The US 10-year yield reached multi-year highs this week, marking a fresh high for 2023. Fed policymakers believe that the rise in yields for longer-dated Treasuries can assist in achieving their monetary policy goals. The chart below illustrates that the US 10-year yield is currently at levels last seen in January 2007.

Turning our attention to the situation in the Middle East, it’s essential to note the potential for escalation. As mentioned repeatedly over the past week, Iran has been the most vocal country in the region, given its strained relations with Israel. While direct involvement from any specific country is not expected at this point, understanding the dynamics of the Middle East suggests that escalation through proxy actors remains a credible possibility. Groups such as Hezbollah and potentially other smaller organizations in the region could become involved with support, funding, or weapons from regional countries. Any development that brings the United States more prominently into the conflict could trigger another surge in Gold prices. The $2000 price level will continue to be in jeopardy the longer the conflict persists without a ceasefire or resolution, and it should be closely monitored in the days ahead.

Silver Analysis:

XAGUSD Silver price is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

XAGUSD Silver price is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The Federal Reserve’s Beige Book release did not bring any surprises to the markets. Economic activity in the United States is on the rise, driven by robust consumer spending and growth in labor wages.

The US Dollar, as measured by the US Dollar Index, surged to a high near 106.60. The release of the Federal Reserve Beige Book did not bring any surprises compared to the September report on economic activity. Furthermore, mixed housing data released earlier in the session had little impact on the USD.The United States continues to demonstrate strong economic activity, as evidenced by recent reports, including S&P Global PMIs, Industrial Production, and Retail Sales. The Beige Book described the near-term economic outlook as “stable” with a hint of slightly weaker growth. It also noted mixed trends in consumer spending and an easing of labor market tightness across the nation.

At the time of writing, the US Dollar DXY is at 106.55, reflecting a 0.35% daily gain. Global stock indexes are experiencing significant losses, leading investors to seek refuge in the USD.In terms of housing data, Building Permits for September came in at 1.475 million, surpassing the 1.450 million forecast but still lower than the previous figure of 1.541 million. Housing Starts in September saw an increase, but it fell short of expectations, registering at 1.358 million, below the forecasted 1.380 million but above the previous reading of 1.269 million.

Meanwhile, US yields are experiencing a slight uptick, with the 2-year, 5-year, and 10-year rates rising to approximately 5.20%, 4.92%, and 4.91%, respectively. According to the CME FedWatch tool, the likelihood of a 25 basis points rate hike at the December meeting has risen to nearly 42%.

USDCHF Analysis:

USDCHF is moving in an Ascending channel and the market has reached the higher low area of the channel

Historically, the Swiss Franc has been considered a safe-haven currency during times of conflict. The recent events, such as the bombing of a Gaza Hospital by Israel resulting in numerous civilian casualties and escalating tensions in the Middle East, have further bolstered support for the Swiss Franc as a refuge currency.

US Treasury yields have risen, and the US Dollar (USD) has strengthened. The US Dollar Index (DXY) has surged to 106.63. Specifically, the 10-year Treasury yield has reached 4.965%, marking its highest level since 2007, while the 2-year Treasury yield remains at 5.251%.

Federal Reserve (Fed) officials, in a Wednesday statement, reiterated their commitment to maintaining current interest rates. Fed Governor Christopher Waller mentioned that it’s premature to determine if further policy rate adjustments are required, emphasizing the importance of data in shaping their decisions. Meanwhile, Fed Bank of New York President John Williams stated that the central bank needs to maintain a restrictive monetary policy for a period to counter inflation, further pushing up US bond yields amid robust US economic growth.

In terms of economic data, US Building Permits for September came in at 1.475 million, surpassing the expected 1.45 million. Housing Starts reached 1.35 million, falling short of the market consensus of 1.38 million, as reported by the US Census Bureau on Wednesday. The Fed Beige Book update indicated little to no change in the US economic outlook between September and early October, suggesting that the data might not prompt the Federal Open Market Committee (FOMC) to deviate from its current guidance.

The Swiss Franc (CHF) is garnering attention amid escalating geopolitical tensions in the Middle East, driving demand for traditional safe-haven assets like the Swiss Franc. Additionally, Swiss Producer and Import Prices for September showed a 1.0% year-on-year decline, following a previous drop of 0.8%. On a monthly basis, the figures declined by 0.1% compared to a previous drop of 0.8%.

Traders are closely monitoring upcoming events, including US Jobless Claims, the Philly Fed index, and Existing Home Sales scheduled for later on Thursday. All eyes are on Fed Chair Jerome Powell’s speech in the North American session; any hawkish comments regarding the policy outlook could attract buyers to the US Dollar. Furthermore, Swiss trade data for September will be released on Thursday, providing potential guidance for the USD/CHF pair. These developments could offer clarity on the direction of the currency pair.

EURUSD Analysis:

EURUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

The September Eurozone Consumer Price Index (CPI) inflation rate stood at 0.30%, aligning with the anticipated figures. European Central Bank (ECB) President Lagarde remarked that both inflation and wage growth have exceeded initial expectations.

Global tensions are escalating as the conflict between Israel and Hamas in the Gaza Strip continues to intensify. In a recent rocket strike on a hospital in Gaza, one of the largest civilian death tolls in recent history occurred, with over 500 individuals seeking refuge in the hospital tragically losing their lives. Both Israel and Hamas have blamed each other for the strike, further deepening the conflict.

Meanwhile, in the United States, there is growing political uncertainty as the US Congress faces challenges in selecting a new Speaker of the House. Two votes in two days have failed to secure a nominee. This paralysis in Congress comes at a critical time as the US is only 30 days away from the end of a short-term funding stopgap that was secured in the eleventh hour earlier this month.

EURCHF Analysis:

EURCHF is moving in the Descending channel and the market has reached the lower low area of the channel

As the US approaches another potential partisan funding clash in mid-November, uncertainty is on the rise. Investors are becoming increasingly cautious and are turning to safe-haven assets, resulting in the strengthening of the US Dollar (USD) and pushing US Treasury yields to multi-year highs. The 10-year Treasury yield reached 4.928% on Wednesday, its highest level since 2007.

On the economic front, the European Union’s Index of Consumer Prices (CPI) for September met expectations, with CPI inflation at 0.3%. European Central Bank (ECB) President Christine Lagarde noted that underlying inflation remains robust, and wage growth continues to be historically high.

EURJPY Analysis:

EURJPY is moving in the Box pattern and the market has fallen from the resistance area of the pattern

The Bank of Japan has upgraded its assessment report for six out of nine regions, indicating improved performance in these areas. This upgrade comes in the backdrop of inflation picking up momentum and a prevailing trend of moderate growth in business and wages.

Investors are eagerly awaiting the release of Japanese inflation data on Friday, hoping for new insights. The National Consumer Price Index (CPI) in Japan, excluding fresh food, is anticipated to exhibit a year-on-year increase of 2.7%, down from the previous reading of 3.1%.

In a quarterly report, the Bank of Japan (BoJ) has raised its assessment for six out of nine economic regions in Japan. The report highlights that Japan’s economy has experienced a moderate recovery across all regions. However, it also notes that in several areas, exports and output have remained relatively stable without significant growth.

Earlier this week, Japanese Finance Minister Shunichi Suzuki refrained from commenting on potential currency intervention. Masato Kanda, Japan’s top financial diplomat, emphasized that the Japanese Yen continues to be viewed as a safe-haven asset, benefiting from the influx of funds seeking safety amid escalating geopolitical tensions in the Middle East. Kanda reaffirmed that if there were excessive fluctuations in the currency market, authorities would not hesitate to take measures such as adjusting interest rates or intervening in the market. This highlights the possibility of intervention in the foreign exchange market by Japanese authorities in the future.

GBPUSD Analysis:

GBPUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

The inflation rate in the UK currently stands at 6.7%, surpassing the 5.5% target set by UK Prime Minister Rishi Sunak. In response to this elevated inflation, the Bank of England may need to consider implementing interest rate hikes in upcoming meetings as a measure to rein in inflationary pressures.

The Pound Sterling (GBP) encountered selling pressure around the 1.2200 level following an attempted recovery spurred by the United Kingdom’s inflation data release. The Office for National Statistics (ONS) reported that September’s inflation figures remained slightly higher than anticipated. This development could have implications for the GBPUSD pair, as the stalled inflation report increases the likelihood of the Bank of England (BoE) considering further tightening measures in their November monetary policy meeting.

The persistence of a higher Consumer Price Index raises questions about whether UK Prime Minister Rishi Sunak can uphold his commitment to reducing inflation to 5.5% by year-end. The repercussions of heightened inflationary pressures are expected to further impact the UK’s housing sector, which has been grappling with elevated borrowing costs.

The UK Office for National Statistics reported a steady inflation report for September, with the monthly headline inflation rising at a faster pace of 0.5%, surpassing expectations of 0.4% and the previous rate of 0.3%. Annual headline CPI data also exhibited steady growth, reaching 6.7%, higher than the estimated 6.5%. Core inflation, which excludes volatile food and oil prices, expanded by 6.1%, slightly surpassing the consensus of 6.0% but decelerating from the August reading of 6.2%. Producers increased prices for goods and services at factory gates by 0.4%, falling short of expectations and the previous release of 0.9% and 0.8%, respectively.

A persistent inflation report is expected to pose challenges for BoE policymakers, who are working diligently to bring inflation down to the target level of 2%. On a related note, partial labor market data added pressure to the Pound Sterling as the ONS reported soft wage data while employment numbers were postponed until October 24.

Average Earnings, excluding bonuses, for the three months leading up to August softened to 7.8%, as predicted, from the previous rate of 7.9%. During the same period, Average Earnings, including bonuses, decelerated to 8.1% from the consensus of 8.3% and the prior release of 8.5%. This slowdown in wage growth is attributed to weakening labor demand both domestically and in overseas markets.

BoE policymaker Swati Dhingra commented on the soft wage report, indicating that the labor market is loosening, and she does not anticipate further wage growth momentum. Last week, Dhingra mentioned that the central bank might consider rate cuts if the growth rate remains below expectations. Elevated interest rates set by the BoE have had a significant impact on the property sector, as evidenced by UK property website Rightmove’s report that home asking prices rose at the slowest pace since 2008, reflecting a slowdown in housing demand due to higher mortgage rates.

The market sentiment remains cautious as concerns mount over the outcome of US President Joe Biden’s visit to Israel. Discussions with Israel Prime Minister Benjamin Netanyahu regarding a potential ground assault in Gaza have the potential to draw in more Middle-Eastern players and escalate conflicts. Despite robust Retail Sales data for September, the US Dollar Index (DXY) has remained relatively stable near 106.00.

US Retail Sales experienced robust growth of 0.7%, driven by increased demand for automobiles and dining out. Economic data excluding automobiles also rose by 0.6%, nearly doubling expectations. Investors are now eagerly anticipating a speech from Federal Reserve (Fed) Chair Jerome Powell, scheduled for Thursday. Powell’s remarks will be closely watched to determine whether he aligns with his colleagues in favoring an unchanged interest rate policy or delivers a more hawkish guidance.

GBPCAD Analysis:

GBPCAD is moving in an Ascending channel and the market has reached the higher low area of the channel

The Canada Housing Corporation has released data for housing starts in the month of September, indicating a figure of 270,000, surpassing the expected 240,000 and the previous reading of 250,000. However, the Canadian Dollar has experienced a slight decline, primarily attributed to the decrease in oil prices.

The latest housing data from Canada exceeded expectations, with the Canada Mortgage and Housing Corporation reporting a Housing Starts s.a (YoY) figure of 270.5K for September. This surpassed market expectations of 240.0K and the previous reading of 250.4K. However, the Canadian Dollar (CAD) has seen a decline, which is closely tied to the drop in Crude Oil prices.

Meanwhile, tensions in the Gaza Strip have escalated following a rocket attack on a hospital, resulting in the tragic death of over 500 civilians. Accusations and blame-shifting between Israel and Hamas regarding the explosion at the building have further intensified the conflict.

AUDUSD Analysis:

AUDUSD is moving in the Descending channel and the market has reached the lower low area of the channel

In September, the Australian unemployment rate was reported at 3.6%, which was slightly better than the expected rate of 3.7%. However, only 6.7K jobs were added, falling significantly short of the anticipated 20K and well below the previous month’s figure of 64.9K. Following the release of this data, the Australian Dollar experienced a decline.

The Australian Dollar faced a decline today in response to a mixed employment report released by the Australian Bureau of Statistics (ABS). The currency had already shown signs of vulnerability leading up to this data release. In September, the unemployment rate stood at 3.6%, which was lower than the expected 3.7% and the previous rate. However, only 6.7k jobs were added during the month, falling short of the anticipated 20k increase and the previous figure of 64.9k. Regrettably, there was a loss of 39.9k full-time positions, although 46.5k part-time roles were added. Additionally, the participation rate decreased from 67.0% to 66.7%, contributing to a marginal decrease in the headline unemployment rate.

Earlier this month, the Reserve Bank of Australia (RBA) opted to maintain interest rates at 4.10%. However, subsequent events have added an element of uncertainty. Assistant Governor Chris Kent of the RBA expressed concerns last week about the time it takes for monetary policy changes to take effect and suggested that further tightening might be necessary to combat persistently high inflation. Furthermore, this week’s release of the RBA meeting minutes revealed a board that was closer to considering a rate hike than previously indicated. The minutes stated that the board had a limited tolerance for inflation taking longer to return to target than expected, with future interest rate adjustments contingent on incoming data and evolving risk assessments.

RBA Governor Michele Bullock further emphasized the challenges facing the Australian economy during a recent summit. She highlighted the impact of successive external shocks on inflation and the tendency for people to adjust their inflation expectations in response. She warned that such adjustments could entrench higher inflation levels. As a result, the upcoming release of third-quarter Australian CPI data, scheduled for next Wednesday, holds significant importance for the Australian Dollar. Economists surveyed by Bloomberg anticipate a year-on-year headline inflation rate of 5.2%, down from the previous 6.0%, but still significantly above the RBA’s target range of 2-3%.

NZDUSD Analysis:

NZDUSD has broken the Box pattern in downside

New Zealand’s recent Consumer Price Index (CPI) report has come in below expectations, indicating that the Reserve Bank of New Zealand (RBNZ) is inclined to maintain its current interest rates in the upcoming meeting. Additionally, the latest data suggests that China’s economic growth is proceeding at a moderate pace.

The New Zealand Dollar (NZD) hit a fresh year-to-date low of 0.5851 against the US Dollar (USD) on Wednesday, driven by a surge in risk aversion and rising US Treasury bond yields. Geopolitical tensions have strengthened the US Dollar’s position at the expense of higher-risk currencies like the New Zealand Dollar. Currently, the NZD/USD pair is trading around 0.5855, marking a 0.69% decrease. Market sentiment remains fragile, with Wall Street registering losses.

US President Biden’s visit to the Middle East has failed to ease concerns about a potential escalation in the region. Iran has heightened its rhetoric against Israel, adding to the geopolitical tensions. An explosion at a Gaza hospital has reignited fears among traders, leading to a surge in global bond yields.

report has come in below expectations")

On Tuesday, US Retail Sales and Industrial Production data portrayed a robust economy. However, this data did not alter the dovish stance of the latest US Federal Reserve (Fed) officials, despite inflation running nearly twice as high as the Fed’s target. In today’s US data, there was a mix of positive and negative indicators. Housing Starts for September increased by 7%, surpassing expectations, while Building Permits declined by -4.4%. Given this backdrop, one might have expected a reevaluation for a more hawkish Fed stance. Nevertheless, money market futures have largely dismissed the possibility of a 25-basis-point interest rate hike in November, although expectations for rate hikes in December and January remain, with the odds at 51.65%.

Turning to New Zealand, the recent Consumer Price Index (CPI) report indicated that inflation remains elevated, suggesting that the Reserve Bank of New Zealand (RBNZ) is likely to maintain its stance of keeping interest rates higher for an extended period. Despite data from China showing the economy is growing at a faster pace than anticipated, a deterioration in sentiment has prompted capital outflows from currencies perceived as risky, flowing toward safe-haven alternatives.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/