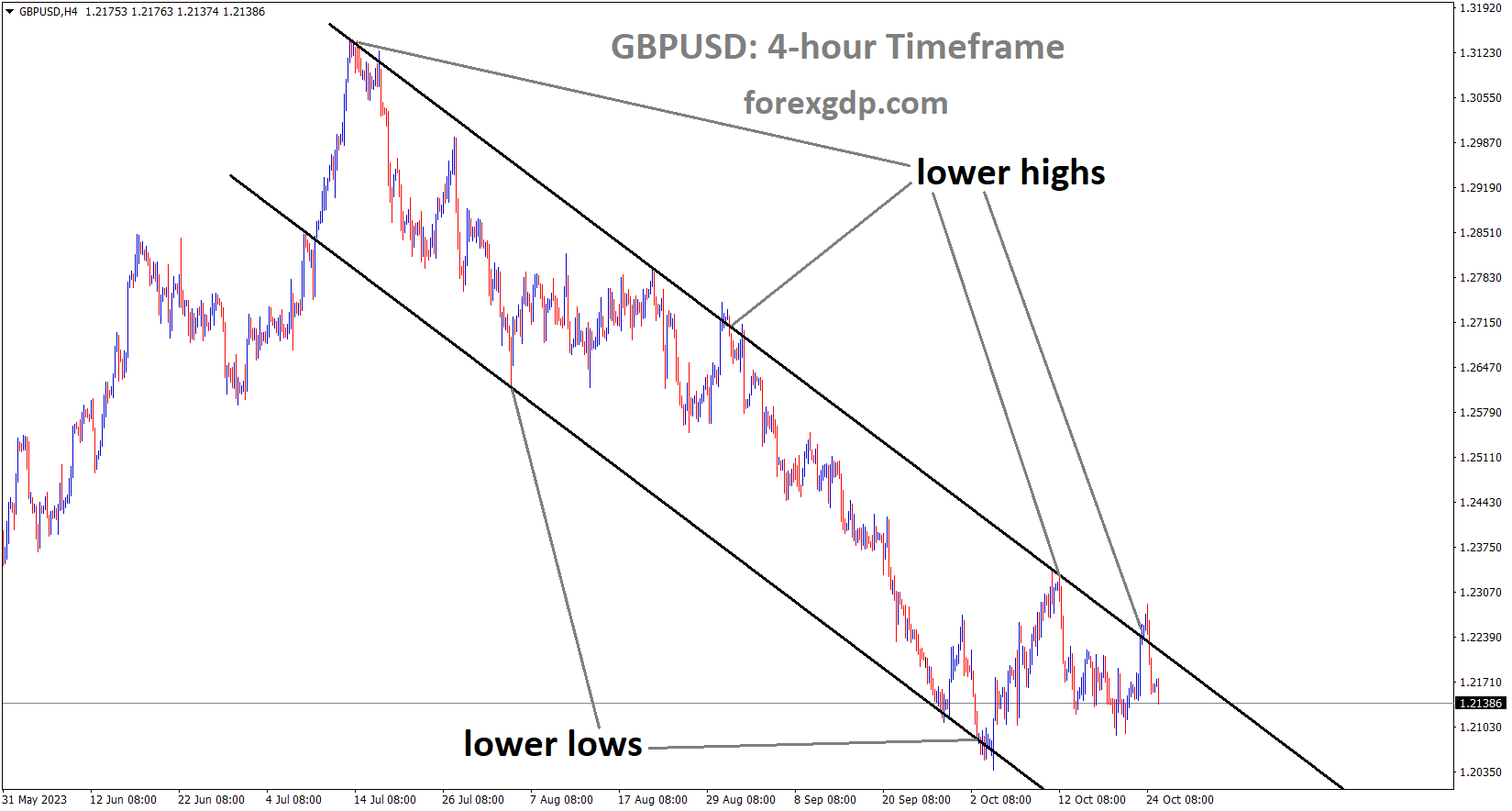

GBPUSD Analysis:

GBPUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

For the third consecutive month, UK PMI data readings have shown a decline, resulting in a weakening of the UK Pound against other currencies. It is widely anticipated that the Bank of England will maintain its current interest rates on November 2nd.

Despite a retreat in US Treasury bond yields and an overall positive risk sentiment, the safe-haven US Dollar has struggled to capitalize on its recent rebound from a one-month low. This situation has provided support for the GBP/USD pair. On the other hand, the downside for the US Dollar is limited by indications that the US economy is displaying resilience, even in the face of rising interest rates. This resilience is likely to allow the Federal Reserve (Fed) to continue its rate-hiking cycle in order to combat inflation.

The flash version of the US Purchasing Managers’ Index (PMI) data, released on Tuesday, showed that the manufacturing sector’s business activity moved out of contraction territory for the first time in six months. Additionally, services activity saw modest acceleration, and there were signs of easing inflationary pressures. In contrast, UK PMIs remained in contraction for the third consecutive month, leading to speculations that the Bank of England (BoE) might maintain its current stance in November. This cautious sentiment is holding back bullish movements in the GBP/USD pair.

Looking ahead, there are no significant market-moving economic releases scheduled for Wednesday in the UK, and the US economic calendar only includes the release of New Home Sales figures. Therefore, investors will be closely watching Fed Chair Jerome Powell’s speech during the US session for insights into the future path of interest rate hikes, which will impact USD demand and potentially provide momentum for the GBP/USD pair. Furthermore, the focus will remain on the US Core Personal Consumption Expenditures (PCE) Price Index, the preferred inflation gauge of the Fed, scheduled for release on Friday.

Gold Analysis:

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel

War tensions have eased following Israel’s successful recovery of hostages from Hamas. However, once the civilians were safely returned, Israel deployed troops for an attack, causing a slight decrease in gold prices in response to this news.

An agreement has been reached to provide aid to those affected in Gaza, and two Israeli hostages have safely returned home. These developments, along with ongoing negotiations, offer a temporary respite in what has otherwise been a turbulent war with the potential to escalate into a regional conflict. Although the fighting is expected to continue, Israel might consider postponing its ground offensive to ensure the safe return of more hostages. This marks a contrast from the relentless exchange of rockets that has characterized the conflict so far.

Given these developments, the gold market has seized the opportunity to reduce risk and reevaluate its next course of action. Panic buying of the safe-haven metal has driven gold prices higher, only encountering a loss of momentum around the $1985 level. Nevertheless, the likelihood of a significant pullback seems low, given that the war is far from over. $1937 could serve as potential support in case of a pullback, and any swift resurgence in tensions might quickly bring $1985 back into focus.

Silver Analysis:

XAGUSD Silver price is moving in an Ascending channel and the market has reached the higher low area of the channel

Leading up to the release of the US Q3 GDP data, the US Dollar tends to undergo a consolidation phase at a lower value. However, robust domestic data from the US is currently bolstering the US Dollar, pushing it to higher levels.

The Managing Director of the IMF, Kristalina Georgieva, has expressed concerns about the ongoing challenges facing the world. In the aftermath of the COVID-19 pandemic and amidst heightened geopolitical tensions, interest rates have risen, businesses are experiencing a slowdown, and vulnerable populations are grappling with higher prices. While interest rates are expected to remain at their current levels for an extended period, the rate at which inflation is decreasing remains slower than desired.

The US Dollar (USD), as measured by the US Dollar Index (DXY), experienced a notable increase on Tuesday, reaching approximately 106.25, marking a gain of nearly 0.50%. This rise can be attributed to several factors: weak European S&P PMI data contrasted with strong performance in American figures, indicating that the US economy is maintaining its resilience and bolstering the value of the US currency. Additionally, US Treasury yields rebounded, further supporting the upward trajectory of the USD.

Despite the Federal Reserve’s ongoing contractionary policies, the US economy seems to be holding steady compared to other economies. Attention has now shifted to key upcoming events, with preliminary Q3 Gross Domestic Product (GDP) estimates scheduled for release on Thursday and September’s Personal Consumption Expenditures (PCE) figures due on Friday. Investors are closely watching these releases to shape their expectations regarding future Fed decisions. While only a minority of traders anticipate a change in current interest rates by the central bank, Chair Powell’s speech on Wednesday will still be closely monitored.

After hitting a low not seen since late September, around 105.35 earlier in the session, the DXY Index made a notable recovery, reaching 106.25. This positive movement was supported by better-than-expected S&P Global Manufacturing PMI data for October, which came in at 50, surpassing the expected 49.5 and accelerating from the previous reading of 49.8. Additionally, the Services PMI exceeded expectations, registering at 50.9 compared to the anticipated 49.8, up from its prior reading of 50.1.

Meanwhile, US yields are on the rise, with the 2 and 5-year rates advancing toward 5.10% and 4.81%, respectively. The 10-year yield saw a slight retreat, moving towards 4.81%. According to the CME FedWatch Tool, the likelihood of a 25 bps rate hike in December remains low, at approximately 25%. The Tool also suggests that the market is pricing in a potential pause in November. With high-tier data releases expected on Thursday and Friday, all eyes are on the anticipated acceleration of US Q3 GDP and the expected deceleration in PCE inflation for September.

On Wednesday, Kristalina Georgieva, the Managing Director of the International Monetary Fund (IMF), addressed the current global economic situation. She pointed out that the Middle East crisis is unfolding at a time when global economic growth is sluggish, interest rates are elevated, and the cost of servicing debt has risen due to the impacts of COVID-19 and the ongoing conflict. Georgieva emphasized that this may not be the last shock the world faces, highlighting her concerns for the regions most affected by the conflict, where lives have been tragically lost, economic activity has been reduced, and countries like Egypt, Lebanon, and Jordan, heavily reliant on tourism, are already feeling the repercussions. She stressed the importance of taking early action and not hesitating to seek assistance from the IMF for debt restructuring.

Georgieva also addressed the recent shift in interest rates, noting that the world has experienced two decades of historically low rates and that a return to more normal interest rate policies is necessary. She acknowledged that the rapid increase from near-zero rates to higher levels is not ideal, but it’s the reality, and she urged everyone to prepare for a prolonged period of higher interest rates.

The good news, according to Georgieva, is that the tightening measures implemented are working, leading to a decrease in inflation. However, she expressed concern that the decline in inflation is not occurring rapidly enough. She stressed the importance of the green transition, despite its added costs, and highlighted that inflation is detrimental to economic growth, eroding investor and consumer confidence, with the most vulnerable in society bearing the brunt of its consequences. Georgieva emphasized that structural factors should not be an excuse to ignore the fight against inflation, as it has a detrimental impact on growth.

In conclusion, Georgieva emphasized the need to adapt to a world of more frequent and severe shocks. She called for increased agility to protect individuals and businesses from these shocks, making it a collective responsibility for everyone.

USDJPY Analysis:

USDJPY is moving in the Box pattern and the market has reached the resistance area of the pattern

This week, the Bank of Japan is convening for its board meeting, and there is a growing expectation that they may raise the Yield Curve Control (YCC) rate. According to reports from Nikkei News, the Bank of Japan is considering plans to purchase 10-year and 25-year bonds. If these bond purchases materialize and adjustments are made to the YCC, it is anticipated that the Japanese Yen (JPY) could strengthen in response.

Towards the end of this month, the Bank of Japan is scheduled to hold a two-day meeting, and the financial markets are speculating about potential adjustments to the central bank’s current yield curve control program. Recent, albeit unconfirmed, reports in the Nikkei newspaper have suggested that Bank of Japan officials may consider allowing long-term Japanese Government Bond (JGB) rates to rise, aligning with trends observed in global bond markets.

Under its ultra-loose monetary policy, the Bank of Japan has maintained low yields on longer-dated bonds, a strategy that has contributed to the weakening of the Japanese Yen and bolstered Japanese exports. However, in recent months, the yield differential between 10-year US Treasury bonds and Japanese bonds has widened due to the Federal Reserve’s ongoing interest rate hikes. This divergence has led Japanese investors to seek higher yields in the US dollar, resulting in a depreciation of the Japanese Yen.

In the lead-up to the Bank of Japan’s policy meeting, significant economic data releases are expected from the United States, including Q3 GDP figures and the latest indicators of inflationary pressures. Any of these releases has the potential to influence the value of the US dollar, and this may necessitate the Bank of Japan to moderate its stance in response to market movements ahead of its meeting.

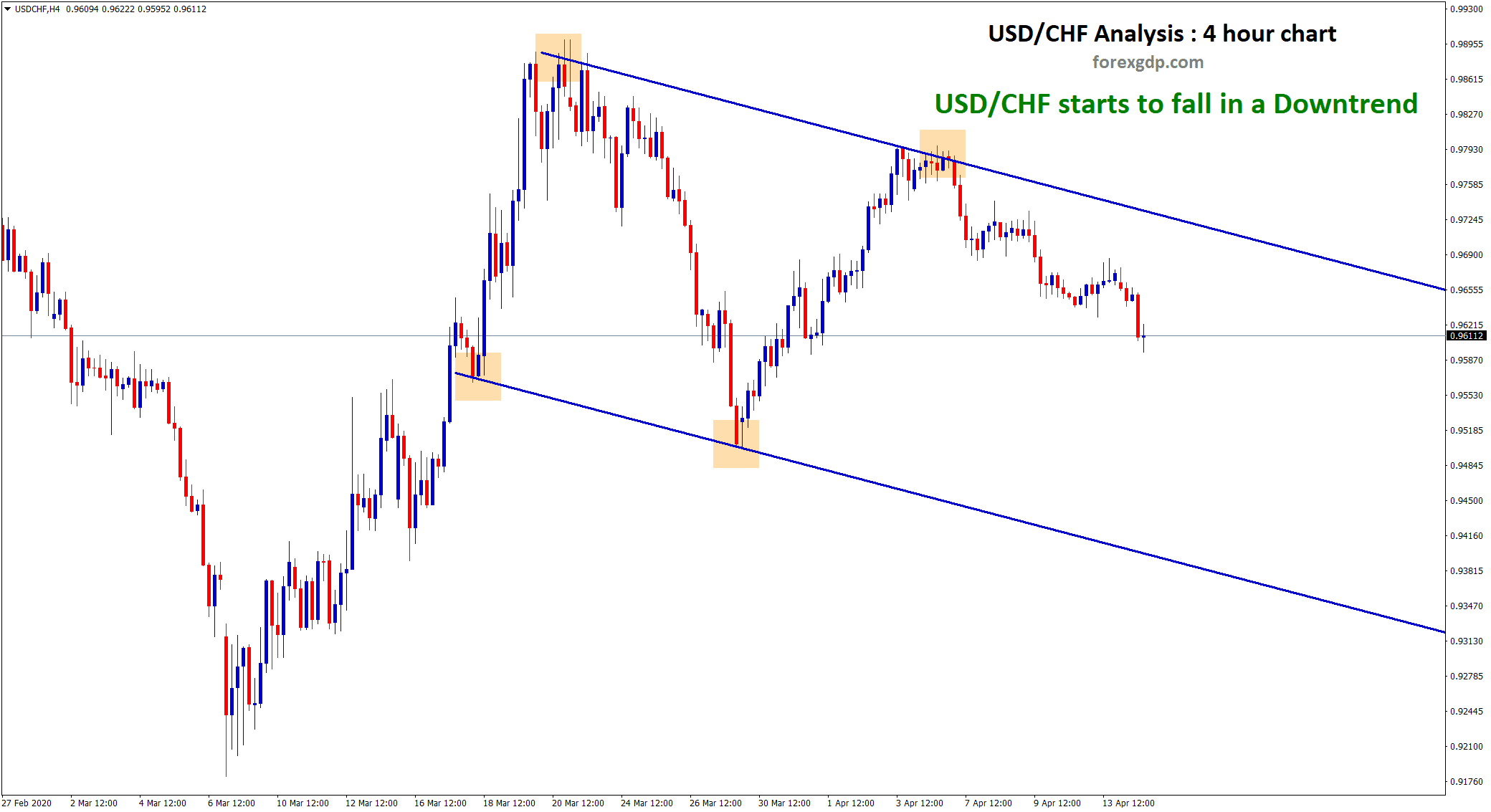

USDCHF Analysis:

USDCHF is moving in the Descending channel and the market has reached the lower high area of the channel

The Swiss Franc has strengthened in anticipation of the upcoming Swiss ZEW survey set for this week. The Swiss Franc has remained in a favorable position, influenced by the ongoing global conflicts. However, if the war situation stabilizes, it could lead to increased selling pressure on the Swiss Franc.

Geopolitical tensions in the Middle East continue to cast a shadow over the market and bolster the Swiss Franc (CHF). Currently, the CHF is trading near 0.8928, registering a 0.05% decline for the day. Notably, the US Purchasing Management Index (PMI) data released on Tuesday exceeded expectations. The flash Composite PMI for October surged to 51.0 from 50.2. Concurrently, the US S&P Global Manufacturing PMI for October outperformed with a reading of 50, surpassing the market’s anticipation of 49.5. This marks the first time in six months that the manufacturing sector has not fallen below the 50 threshold. The Services PMI also showed strength, rising to 50.9, exceeding consensus forecasts.

On the flip side, the Richmond Manufacturing Index for October retreated to 3 from the previous reading of 5, falling short of market expectations. The positive US economic data has eased concerns that tighter monetary policies and higher borrowing rates would dampen investment and industrial activity. Nevertheless, market participants will be closely monitoring US growth figures and the core Personal Consumption Expenditure Index (PCE) data for fresh market direction. Stronger-than-expected data could boost the US Dollar and provide tailwinds for the USD/CHF pair.

However, the escalating tensions in the Middle East could limit the pair’s upside potential and drive investors toward safe-haven assets like the Swiss Franc. In the previous week, Switzerland’s trade surplus widened more than anticipated in September, with the Trade Balance reaching 6,316 million compared to the previous month’s 3,814 million, surpassing the market consensus of 3,770 million. Exports also saw a substantial increase, rising from 20,932 million to 24,795 million month-on-month in September, while Imports climbed from 17,118 million to 18,480 million during the same period.

Market participants will closely watch the Swiss ZEW Survey Expectations for October. Additionally, later this week, the preliminary estimate of the US Q3 Gross Domestic Product (GDP) will be released on Thursday, followed by the US Core Personal Consumption Expenditure Index (PCE) data on Friday. These events could provide clear direction for the USD/CHF pair in the coming days.

EURCHF Analysis:

EURCHF is moving in the Descending channel and the market has fallen from the lower high area of the channel

Germany’s business activity and Composite PMI have reported lower figures than anticipated, signaling a potential recession looming over the Eurozone. Consequently, Euro currency pairs experienced a decline against their counterparts in the past day.

The decline in the common currency’s value can be attributed to disappointing economic data in the Eurozone. To provide some context, the S&P Global composite PMI for October showed that German business activity continued to contract, heightening concerns of an impending recession in Europe’s largest economy. This economic fragility could challenge market expectations that interest rates will remain elevated for an extended period, despite the European Central Bank’s statements, potentially putting regional bond yields under pressure.

We will gain more insights into the thinking of policymakers later this week when the European Central Bank announces its monetary policy decision. However, it is widely anticipated that the institution, under the leadership of Christine Lagarde, will hit the pause button after having implemented a 450 basis point tightening over the past ten meetings. Market participants have already factored in this expected pause, underscoring the importance of closely monitoring the guidance provided, with a specific focus on President Lagarde’s communication. If the central bank chief signals that this pause is not merely a short break to gather more data but rather marks the end of the tightening cycle, it could lead to significant depreciation of the euro.

EURCAD Analysis:

EURCAD is moving in the Descending triangle pattern and the market has fallen from the lower high area of the pattern

The upcoming Bank of Canada monetary policy meeting is widely anticipated to keep interest rates unchanged. Over the past three months, there has been a decline in GDP, retail sales, and job growth. Therefore, it is expected that the Bank of Canada will aim to maintain the current interest rate if feasible.

The Bank of Canada is scheduled to announce its monetary policy decision for October this Wednesday. Under the leadership of Tiff Macklem, the central bank is widely expected to maintain its benchmark interest rates at the current 22-year high of 5.0%, thereby keeping borrowing costs stable for the second consecutive month. This aligns with recent statements made by senior officials.

Regarding forward guidance, the central bank might indicate a willingness to consider further tightening of policy to maintain its commitment to fighting inflation. However, it may express a less resolute stance, given the deteriorating economic conditions.

In September, when the Bank of Canada decided to hold rates steady, it cautioned that the country’s economy was entering a period of weaker growth characterized by a noticeable drop in consumption and housing production. Preliminary data for the third quarter have affirmed this outlook, with GDP remaining stagnant in July and showing only modest improvement in August. Given the rapid deceleration in economic activity and the easing of consumer price inflation, which currently stands at 3.8% year-on-year, the central bank is facing mounting pressure to adopt a more cautious and less hawkish approach. This could involve a more balanced communication strategy to avoid causing undue market volatility. Any indication that policymakers prioritize economic growth over inflation control is likely to have a negative impact on the Canadian dollar.

AUDUSD Analysis:

AUDUSD is moving in the Descending triangle pattern and the market has fallen from the lower high area of the pattern

The Australian Dollar saw a significant surge today following the release of Q3 CPI data, which exceeded expectations at 5.4%, surpassing the previous figure of 5.3%, and notably higher than the 6.0% recorded earlier. In response to these inflation figures, RBA Governor Michelle Bullock emphasized the importance of effectively managing inflation and suggested that raising interest rates could be an option to achieve this goal.

The Australian Dollar saw an uptick following the release of the Q3 CPI data, which outperformed expectations at 5.4% year-on-year, surpassing forecasts of 5.3% and the previous reading of 6.0%. Of particular note, the quarterly headline CPI for September registered at 1.2%, exceeding the anticipated 1.1% and the previous 0.8%. This indicates a re-acceleration of inflationary pressures.

preferred trimmed-mean CPI measure also revealed a year-on-year figure of 5.2%")

The Reserve Bank of Australia’s (RBA) preferred trimmed-mean CPI measure also revealed a year-on-year figure of 5.2% for the end of September, surpassing estimates of 5.0% and the previous 5.9%. The quarter-on-quarter trimmed-mean CPI reading of 1.2% exceeded the forecasted 1.0% and the previous figure. Today’s CPI data is undeniably concerning, especially when considering the RBA’s preferred trimmed mean measure.

AUDCHF Analysis:

AUDCHF is moving in the Descending channel and the market has reached the lower high area of the channel

Some observers may find solace in the fact that the annual inflation rate has decreased, but it’s important to recognize that this decrease is primarily due to base effects rather than an accurate reflection of the current economic landscape. When comparing the quarter-on-quarter headline CPI for Q3 2022 (1.8%) with today’s Q3 2023 figure (1.2%), it becomes evident that inflation has reignited over the third quarter, contributing to the lower annual number.

Leading up to today’s CPI release, the RBA provided interesting commentary. RBA Assistant Governor Chris Kent mentioned the possibility of further tightening to ensure that inflation, which remains elevated, returns to target. The October meeting minutes emphasized the Board’s low tolerance for a slower return of inflation to the target rate, with future rate hikes contingent on incoming data and evolving economic outlook. Governor Michele Bullock noted the persistent challenges posed by various shocks and the potential for inflation to return to target more slowly than anticipated. She emphasized the Board’s commitment to preventing a protracted deviation from the inflation target, indicating their readiness to raise the cash rate further if necessary.

AUDNZD Analysis:

AUDNZD is moving in an Ascending channel and the market has fallen from the higher high area of the channel

In October, the US Composite PMI data exhibited an increase from 50.2 to 51.0. Additionally, the Services PMI climbed to 50.9, while the Manufacturing PMI rose to 50.0. These positive developments strengthened the US Dollar in comparison to the New Zealand Dollar (NZD).

Conversely, the conflict between Israel and Gaza showed signs of easing tensions, which led to a stronger NZD against other currencies.

The recent rise in sentiment is influenced by several factors. First, the postponement of Israel’s ground assault plan in Gaza has provided support to the pair, improving risk sentiment. Additionally, China’s announcement of its intention to issue more sovereign debt has contributed to this optimistic outlook. Furthermore, positive developments emerged from constructive dialogues between the United States and China during their initial economic working group meeting, further boosting market confidence.

It’s important to note that the situation in the Middle East had initially created unease among investors due to concerns about potential escalation and regional disruptions. However, ongoing diplomatic efforts are actively working towards easing tensions in the Israel-Hamas Gaza Strip conflict.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/