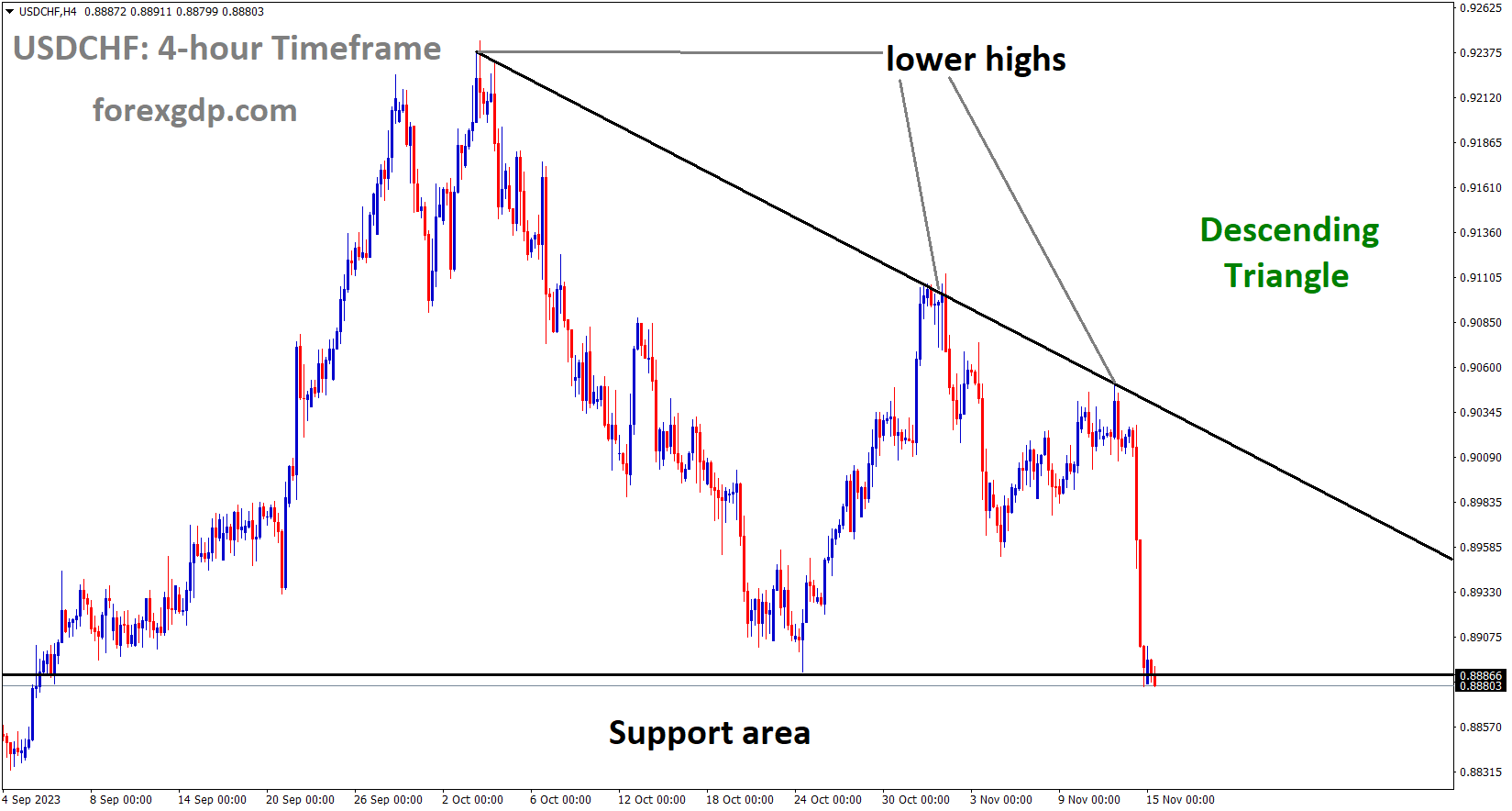

USDCHF Analysis:

USDCHF is moving in the Descending triangle pattern and the market has reached the support area of the pattern

SNB Chairman Thomas Jordan stated that a rate hike may be possible in the upcoming meeting if inflation does not reach the desired level. Decisions on future rate hikes will be made based on forthcoming economic data.

The USDCHF experienced a decline attributed to disappointing US inflation data. The US Bureau of Labor Statistics reported Consumer Price Index data for October, revealing an annual rate of 3.2%, below the anticipated 3.3%. Additionally, the US Core CPI showed a 0.2% increase, falling short of the expected 0.3%. This subdued inflation in the US reinforces market expectations that the US Federal Reserve will refrain from interest rate hikes in upcoming meetings.

The impact extends to US Treasury yields, with the 10-year bond yield witnessing a significant drop to 4.43%, and the 2-year rate at 4.83% as of the current press time. The Dollar Index (DXY) also experienced a decline of approximately 1.50%, reaching around 104.00, with current support bids near 104.10. Investors are eagerly anticipating the release of the US Producer Price Index and Retail Sales data to gain insights into the overall US economic landscape. Should these figures align with expectations, it could further exert pressure on the US dollar.

EURCHF Analysis:

EURCHF is moving in the Descending channel and the market has reached the lower high area of the channel

On the Swiss front, Swiss National Bank (SNB) Chairman Thomas Jordan indicated in an interview with local television station TeleZueri that he does not rule out the possibility of additional interest rate hikes in the future. Chairman Jordan stated that if the current monetary policy proves insufficiently restrictive for ensuring long-term price stability, another interest rate move may be necessary. He expressed uncertainty about whether the terminal rate has been reached. As the month progresses, attention will be on the Swiss ZEW Survey Expectations and Real Retail Sales for insights into whether the SNB will consider an interest rate increase in the December meeting. Current expectations appear to lean towards a 25 basis points hike.

GOLD Analysis:

XAUUSD Gold price has broken the Descending channel in upside

The Gaza area is currently under the control of Israel, intensifying tensions in the Middle East. This heightened sense of fear is prompting investors to turn to gold in the market. Additionally, support from US domestic data is contributing to the positive outlook for gold on the other side.

Gold prices are consolidating recent gains, reaching $1,971 during the early Asian session on Wednesday. The demand for precious metals is boosted by weaker-than-expected US inflation and a decrease in US Treasury yields. Additionally, rising geopolitical tensions contribute to safe-haven flows. The current gold price hovers near $1,960, experiencing a 0.10% loss for the day. Meanwhile, the US Dollar Index falls to the 104.00 area, the lowest level since early September. The decline in US Treasury bond yields, particularly the 10-year yield dropping from 4.60% to 4.45%, benefits gold, prompting a rebound from the $1,940 low.

The US Consumer Price Index results, showing a growth of 3.2% YoY compared to the previous 3.7% and below the market consensus of 3.3%, alleviate pressure on the Federal Reserve to tighten monetary policy further this year. This contributes to continued buying in the precious metal. The core measure of the CPI rose by 0.2% MoM and 4.0% YoY. In the Middle East, the Gaza Strip has been under total Israeli blockade since Hamas initiated an attack on Israel on October 7. Escalating geopolitical tensions in the region may increase demand for gold. Looking ahead, gold traders will monitor Chinese Industrial Production and Retail Sales data for October, scheduled for release on Wednesday. Weaker-than-expected data could raise concerns about an economic slowdown in the world’s second-largest economy. Later in the day, the US Retail Sales and Producer Price Index (PPI) will be released.

SILVER Analysis:

XAGUSD Silver price is moving in the Descending channel and the market has reached the lower high area of the channel

The October US Consumer Price Index (CPI) inflation rate is reported at 3.2%, significantly lower than the previous month’s 3.7%. If inflation continues to cool in the coming months, the Federal Reserve (Fed) might consider pausing rate increases.

Last month, inflation in the U.S. economy eased, partly due to the Federal Reserve’s assertive interest rate hikes, resulting in rates reaching multi-year highs. This indicates progress by policymakers in their efforts to restore price stability. According to the U.S. Bureau of Labor Statistics, the consumer price index remained unchanged in October on a seasonally adjusted basis, primarily influenced by a 2.5% decline in energy costs. As a result, the 12-month inflation rate dropped from 3.7% to 3.2%, a gradual yet positive development aligned with the Fed’s target of averaging a 2% inflation rate over time.

Expectations among economists surveyed by Bloomberg News foresaw a 0.1% month-on-month increase and a 3.3% year-on-year increase in the headline Consumer Price Index. However, the actual core CPI, excluding food and energy to reveal longer-term economic trends, unexpectedly rose by 0.2% month-on-month, falling one-tenth of a percent below projections. The underlying gauge, compared to the previous year, grew by 4.2%, a slight decrease from September’s 4.3% increase.

While inflationary pressures are showing signs of moderation, the process remains slow and burdensome for consumers. The latest report is likely to support the Federal Reserve’s cautious approach, reducing the probability of further tightening in the current cycle. This data could also provide officials with the justification to adopt a less aggressive stance, potentially impacting U.S. yields and the U.S. dollar. Such a scenario might be favorable for gold prices. Following the release of the CPI report, the U.S. dollar, as measured by the DXY index, experienced a decline of over 0.7% on the day, influenced by a significant drop in U.S. Treasury yields. In contrast, gold prices rose, registering a 0.5% increase in early New York trading.

If the benign inflation figures persist, it may lead to a decline in rates heading into 2024. This could create conditions conducive to a substantial downward correction in the U.S. dollar, potentially benefiting precious metals like gold and silver.

USDCAD Analysis:

USDCAD is moving in an Ascending channel and the market has reached the higher low area of the channel

US domestic data, coming in lower than expected, provided a slight boost for the Canadian Dollar, primarily due to the rebound in oil prices in the market.

The Canadian Dollar is gaining strength due to a deviation from the forecast in the US Consumer Price Index inflation figures. The lower-than-expected data is fostering a risk-on sentiment in broader markets, boosting overall market confidence. The October US CPI came in at 0.0% month-on-month, failing to meet the forecast of 0.1% and contrasting with the previous 0.4%. The annualized CPI stood at 3.2%, down from the prior 3.7% and below the forecast of 3.3%.

This unexpected slowdown in inflation is fueling optimism among investors, suggesting that the Federal Reserve’s narrative of keeping interest rates higher for an extended period might not be as prolonged as previously assumed. The Canadian Dollar is reaching a five-day high and experiencing its highest bids in a week, driven by the US CPI miss.

Market expectations had been eager for a deviation in CPI figures, and the faster-than-anticipated cooling of inflation is encouraging investors to re-enter riskier assets, including the Canadian Dollar. Despite this positive development, the week still holds significant US data, with the Producer Price Index and Retail Sales for October scheduled to be released on Wednesday.

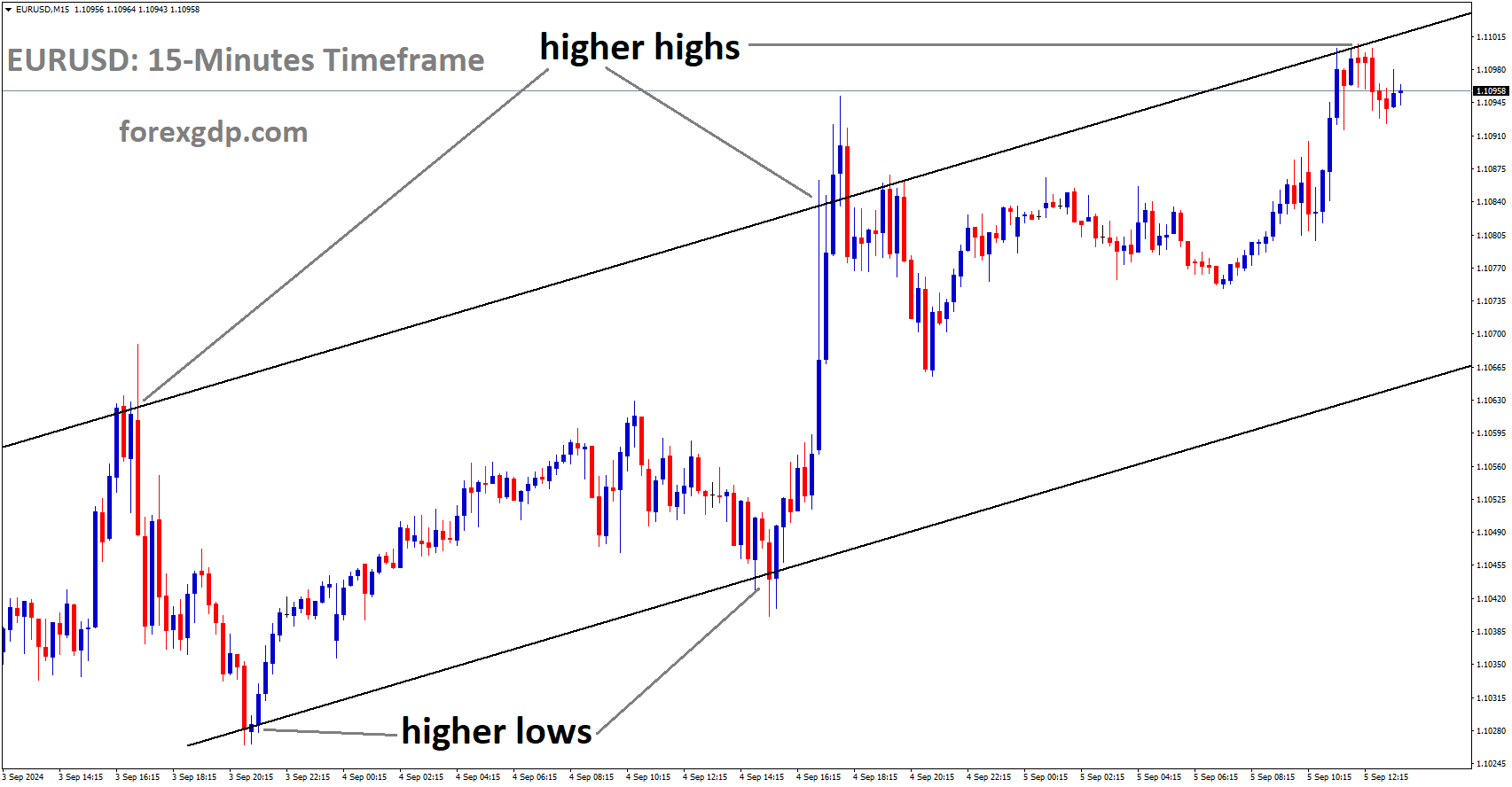

EURUSD Analysis:

EURUSD is moving in an Ascending channel and the market has reached the higher high area of the channel

The Euro currency has gained more advantage from the weakness in US domestic data reported yesterday. The Federal Reserve (FED) now has an opportunity to consider pausing rates in the coming months, contributing to the Euro’s positive movement against the USD this week.

The US Dollar is experiencing some buying activity, recovering from Tuesday’s dip to a one-week low, posing a challenge for the EURUSD pair. Despite the USD’s upward movement, there is a lack of strong bullish conviction amid a growing consensus that the Federal Reserve has concluded its policy-tightening efforts. This sentiment was reinforced by softer US consumer inflation figures, revealing a stable headline Consumer Price Index (CPI) in October and a year-on-year rate slowdown from 3.7% in September to 3.2%, marking the smallest increase in two years.

Investors swiftly adjusted their expectations, anticipating the Fed to maintain interest rates, and the current market pricing suggests a potential rate cut starting in May 2024. This resulted in a significant overnight drop in US Treasury bond yields, potentially restraining aggressive USD bullish positions and helping to limit downside pressure on the EURUSD pair.

As a cautious approach, it is advisable to await clear follow-through selling before confirming a potential peak in spot prices and considering aggressive bearish trades. Investors are now turning their attention to the US economic calendar, with the release of the Producer Price Index, monthly Retail Sales figures, and the Empire State Manufacturing Index scheduled for the early North American session. These, coupled with US bond yields and broader risk sentiment, are likely to drive demand for the safe-haven US Dollar, providing new momentum to the EURUSD pair.

EURNZD Analysis:

EURNZD has broken the Ascending channel in down side

In October, China’s retail sales increased by 7.4%, while the Industrial Production reading came in at 4.6%, surpassing the previous 4.5%. These positive readings contributed to a strengthening of the NZD Dollar against other currencies.

China’s National Bureau of Statistics reported a 4.6% year-on-year increase in Industrial Production for October, slightly surpassing consensus estimates and the 4.5% growth recorded in the previous month. Additionally, Retail Sales for the past 12 months through October exceeded market expectations, showing a 7.4% advance. However, the positive indicators are overshadowed by the less favorable release of Fixed Asset Investment, which rose by a 2.9% year-on-year rate during the reported month, falling short of the anticipated 3.1% and the September reading.

GBPUSD Analysis:

GBPUSD is moving in an Ascending channel and the market has reached the higher high area of the channel

In October, UK inflation data recorded a sharp decline to 4.6% from the previous month’s 6.7%. The Pound Sterling market is eagerly anticipating the release of the high-impact Consumer Price Index data for the United Kingdom in October, scheduled for Wednesday and to be provided by the Office for National Statistics. In the preceding month of September, the UK CPI exhibited an annual growth rate of 6.7%, mirroring the pace observed in August and surpassing market expectations of a 6.5% increase. The Core CPI index also showed acceleration, reaching 6.1% year-on-year in the reported month, compared to a 6.2% increase in August and exceeding the 6.0% forecast.

Despite the persistent high inflation level, the Bank of England (BoE) maintained the benchmark interest rate at a 15-year high of 5.25% during its November policy meeting, with the possibility of another interest rate hike left open. The BoE adjusted its policy statement language, indicating that the Monetary Policy Committee’s projections suggest a need for a restrictive monetary policy for an extended period. BoE Chief Economist Huw Pill reiterated the importance of maintaining a restrictive monetary policy to meet the inflation target.

In contrast, the updated forecasts from the Bank revealed a flatlining British economy in the coming years. The BoE projections also anticipated a decline in inflation to 4.8% in October, nearly two points lower than September. The central bank attributed the expected drop in inflation to economic slowdown and the diminishing impact of last year’s gas price surge, suggesting a forthcoming resumption of the downward inflationary trend.

Leading up to Wednesday’s inflation data release, Pound Sterling traders are considering the latest wage inflation data, indicating a 7.7% 3-month year-on-year rise in Average Earnings excluding Bonus in September, slightly lower than the 7.8% increase recorded in August. However, this wage growth data is not anticipated to significantly influence the BoE’s policy outlook, given the acknowledged uncertainties about official labor market data in the November policy statement.

Expectations for Bank of England tightening have diminished, with the World Interest Rate Probability gauge by Bloomberg suggesting a 10% likelihood of a hike on December 14, rising modestly to around 20% for February 1. The first cut is already largely priced in for August 1. Projections for the headline annual UK Consumer Price Index in October suggest a rise of 4.8%, a considerable drop from the 6.7% increase in September but still more than twice the BoE’s 2.0% target. Core CPI inflation is expected to decrease to 5.8% year-on-year in October compared to September’s 6.1%. On a monthly basis, Britain’s CPI is projected to rise by 0.1%, following the 0.5% growth reported previously. Analysts at TD Securities anticipate a sharp drop in UK headline inflation in October, aligning with the BoE’s forecast, largely attributed to base effects in the energy component. Services inflation is expected to remain below the BoE’s forecast, reinforcing the belief that the Bank is finished with rate hikes.

CADJPY Analysis:

CADJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The Q3 GDP for Japan showed a contraction of 0.5%, contrasting with the 1.2% in the previous reading. On an annualized basis, a contraction of -2.1% was reported, a significant decline from the 4.8% in the previous reading. The Japanese Yen continued to exhibit weakness in the market following the release of this data.

The preliminary readings for the third quarter (Q3) 2023 Gross Domestic Product (GDP) figures indicate that Japanese economic growth was -0.5% quarter-on-quarter, falling short of the expected -0.1% and contrasting with the 1.2% growth seen previously. Additionally, the Annualized GDP contracted by 2.1%, a notable deviation from the anticipated 0.6% decline and the 4.8% expansion in the previous period.

AUDCHF Analysis:

AUDCHF has broken the Descending channel in upside

The Australian Bureau of Statistics reported that the Wage Price Index for the third quarter increased by 1.3% quarter-on-quarter, in line with expectations and surpassing the 0.8% recorded in the previous quarter. On an annual basis, the Australian Wage Price Index reached 4.0%, exceeding the market’s anticipated 3.9% figure for the same period and surpassing the 3.6% recorded in the previous reading.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/